BABA - MercadoLibre: Expensive But Formidable Execution

2023-11-20 16:30:19 ET

Summary

- MercadoLibre reported Q3 earnings with a double beat on GAAP EPS and revenue, leading to a 4% increase in stock price.

- The company saw strong growth in income from operations, total revenue, and gross merchandise volume.

- Mercado Pago, the company's payment platform, showed robust growth and increased user engagement, positioning itself as a comprehensive financial service provider.

- While the company is expensive it has a formidable execution track record even with a deteriorating market outlook.

- As such, we rate the company as a buy.

On the 1st of November, MercadoLibre (MELI) reported its Q3 earnings. The company posted a double beat with a GAAP EPS of $7.18, which beat by $1.35, and revenue coming in at $3.8B, which is a positive surprise of $250M.

As a result, MercadoLibre’s stock jumped up 4%. Nonetheless, the stock is still down close to 30% since its ATH at the moment of writing, but at the same time the stock is still up over 75% year-to-date.

As you can see below, the stock is up over 11% in the last 5 days. This shows how fast it can go in investing.

Ycharts

Now, let’s take a look at the numbers!

Valuation

Before diving into the latest quarter results, I want to take a brief moment to look at the explosive growth MercadoLibre has experienced over the last few years.

As you can see in the chart below, MELI has been able to grow its revenue and gross profit in a very impressive manner. The company has a revenue CAGR since 2015 of close to 40% and a gross profit CAGR of over 35% since 2015.

Stock Info

In addition, MercadoLibre has a 56.61% gross margin, which is very impressive, this indicates that the company has a strong pricing power.

Furthermore, the company has a ROIC of 15.05%. This indicates that for each $100 it invests in its business it generates an additional $15.05 in operating income. While this is decent, we would love to see this increase in the future. Nonetheless, you can see in the chart below, that this is in a clear uptrend, which is promising.

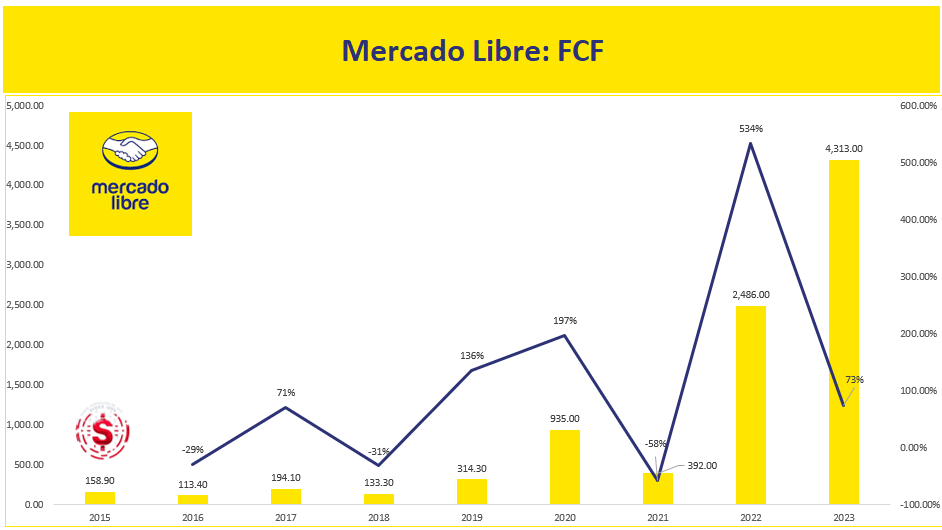

Last but not least, MercadoLibre has a strong track record of FCF growth. MELI has a 5Y FCF CAGR of 68.84% or an FCF CAGR of over 44% since 2014. This is impressive, as you can see in the chart below.

{kind=link}

Nonetheless, MELI isn't cheap, but the quality that MercadoLibre stock brings deserves a premium, as we have shown above.

The impressive revenue and FCF growth alongside the 50%+ gross margin can only be found in a few businesses. This shows the quality of MercadoLibre.

For example, the company has a PE of 75, but this PE has been much higher in the past and it is rapidly decreasing as the earnings continue to grow, as you can see in the chart below.

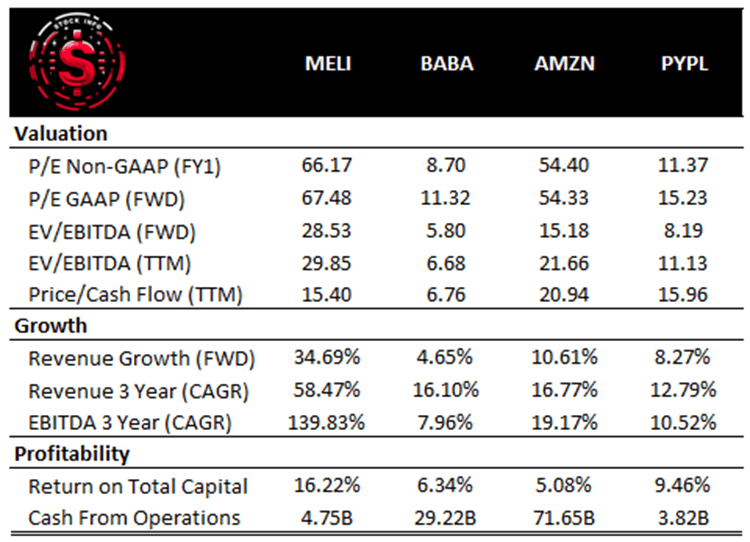

Now, let's take a quick look at 2 major competitors in Alibaba (BABA) and Ebay (EBAY), as all in all MELI's core product is its marketplace. Nonetheless, we will also take a look at Amazon (AMZN), as a lot of people like to call MercadoLibre the Amazon of Latin America.

As you can see, MELI's PE is pretty similar to AMZN's. Nonetheless, AMZN's growth is not nearly as impressive as MELI's in the most recent years. On the other hand, we have both EBAY and BABA, which are much cheaper. EBAY isn't a growth company anymore and is simply a marketplace.

BABA is still a growth company, which I like at its current valuation, but has much lower growth and has a serious discount because it is a Chinese company and as such there is some geopolitical risk involved.

When we take a look at price to FCF, we can see that MELI is much cheaper than AMZN. Nonetheless, it is twice as expensive as Alibaba. But, we have to keep in mind that MELI is still growing aggressively in comparison to the others.

We took a quick look at MELI compared to BABA, AMZN and PayPal (PYPL). As you can see MELI is expensive compared to the others, but its growth and EBITDA is also much higher. For example, the 3Y revenue CAGR of MELI is 58.74%, the second in the list is AMZN with only 16.77%.

In addition, MELI's return on total capital beats the other companies by a mile. The return on total capital for MercadoLibre is 16.22% compared to 9.46% for PayPal and 6.34% for BABA

{kind=link}

All in all, I believe MercadoLibre is a fabulous stock to hold for the long-term, but one has to be careful if growth starts slowing down as this could cause a significant shock to the stock price.

The Numbers

Now let's take a look at the latest quarter.

We will be looking at some metrics from MercadoLibre’s earnings presentation these provide us with all the core numbers we need.

Mercado Libre’s Q3 Presentation

Let’s go over them together, most importantly we can see that one of the most important metrics for MELI, the income from operations came in at $685M or 18.2%. This is incredibly strong considering MercadoLibre grows extremely fast.

Despite the strong margin, the company remains committed to investing in various aspects of the business, such as logistics, new businesses like insurance, and development.

The total revenue came in at $3.8B, which is an increase of 69% YoY. Most notably, revenue in Mexico grew 60% year-on-year, while Brazil posted a 40% revenue growth year-over-year. MELI’s CFO, Martin de los Santos, mentioned that these two countries have again increased their contribution to the total revenues.

Mercado Libre’s Q3 Presentation

In the following slide, you can see the evolution of the net revenue starting from Q3’22. MercadoLibre has been able to grow its net revenues at an impressive 7% CAGR per quarter since Q3’22, or an increase of 69% YoY revenue adjusted.

Mercado Libre’s Q3 Presentation

As mentioned above, income from operations came in at $685M, this is a new record and makes this the 4th consecutive quarter of income growth. In addition, the company saw margin expansion as a result of strong business growth and cost discipline.

Mercado Libre’s Q3 Presentation

Furthermore, MELI saw accelerated growth in Gross Merchandise Volume ((GMV)) and the number of items sold in all of their main geographies. So what caused this you might ask?

Mercado Libre’s Q3 Presentation

Improvements in logistics, fulfillment penetration, and better delivery promises led to increased user engagement. In addition, MercadoLibre achieved a record of 50 million+ unique buyers and gained market share, especially in Brazil and Mexico.

Mercado Libre’s Q3 Presentation

In addition, Items sold is up 26% YoY to 357M, which you can see in the slide below.

Mercado Libre’s Q3 Presentation

Total Payment Volume ((TPV)) increased 121% YoY to $47.3B. Most notably, Mercado Pago reported robust off-platform Total Payment Volume ((TPV)) across its main countries.

The number of users and engagement metrics increased as Mercado Pago positioned itself as a comprehensive financial service provider.

Mercado Libre’s Q3 Presentation

A quick reminder on what off-platform TPV is: Off-platform TPV is the total money a payment company handles outside its main system, like when you use their service to pay on other websites or apps.

This metric helps the company see the full extent of their payment processing.

Mercado Libre’s Q3 Presentation

Let’s take a deeper look at Mercado Pago, as this was one of the main reasons to buy MELI.

Mercado Pago, The Key Of The Thesis

Mercado Pago has the potential and has proven to be a key driver for growth.

MercadoLibre developed an in-house payment system, and has not split off its payment solution.

Mercado Pago is a digital financial platform that allows you to manage your finances in a simple way. With Mercado Pago, you can handle everything from your pocket to your sales. It offers services such as Pix, credit card, loans, and more. You can receive payments as you prefer and increase your sales with options like Point machine, QR code, payment link, or the option that your customers prefer.

You can see this a little bit like an in-house PayPal to give a comparison. Nonetheless, PayPal is obviously much larger and more advanced at this moment in time. You can read more about my bullish stance on PayPal here.

Mercado Pago is available in all of South America’s biggest markets and offers a whole range of payment solutions. I’m not going to go too in-depth on what Mercado Pago exactly entails in this piece.

However, I will look at the results as they are the main driver of the revenue growth as I indicated above.

{kind=link}

I already mentioned that Mercado Pago saw strong growth, but it also saw increased engagement, with more users utilizing remunerated accounts and other asset management solutions in Brazil and Argentina. There was also an improvement in Net Promoter Scores ((NPS)) in Mexico.

Osvaldo Giminez, who is responsible for the credit business, mentioned that the company accelerated the origination of credit products with longer durations in Brazil, issuing over 1 million credit cards during the quarter, surpassing $1B for the first time ever. This was due to the observation of improved spreads and a positive trend in credit quality in the region. This caused the online payment solutions side of the business to experience strong growth across the region.

In addition, the company continues to improve its underwriting models, which allowed Mercado Pago to offer larger credit lines with longer durations.

Furthermore, MercadoLibre stated that it believes credit cards play a crucial role and will continue to play a crucial role in driving consumption in Brazil.

As can be seen in the slide below, digital account TPV increased by 188.7% YoY to $17.6B, which is 37.21% of the total TPV. Meanwhile, in Q3 of last year, Digital Account TPV accounted for 32.92% of the total TPV. As such, we can say that digital account TPV is rapidly growing across all countries.

Mercado Libre’s Q3 Presentation

To end this paragraph about Mercado Pago, I want to discuss the following question from Kaio Prato, an analyst from UBS asked an interesting question:

Out of your almost 50 million unique FinTech users, how many clients see Mercado Pago as a principal digital account nowadays? If you have some percentage of the principality that you can share. And how much do you think you can achieve in the future?

Osvaldo Giminez responded that while the exact percentage of users viewing Mercado Pago as a principal digital account was not disclosed, it was mentioned that various metrics indicate an increasing number of users using multiple products, including consumer credit, credit cards, asset under management, and TPV generated by credit and debit cards.

Mercado Libre’s Q3 Presentation

Guidance

As some of you might be aware, the company doesn’t give any guidance.

Nonetheless, Marcos Galperin the Founder and CEO of Mercado Libre mentioned the following:

We are really happy with the way the business has been evolving last 24 months, at least, really growing very nicely, gaining market share and lately also gaining scale and increasing margins. As you know, we don't guide, but there are many exciting things going on, particularly, obviously, AI.

That hopefully will enable us to provide our users a better experience, enable us to launch innovative ideas, and also scale and gain efficiencies, whether it is in customer service, or whether it is in fraud prevention, or whether it is in the way our developers, 15,000 developers, go about developing and performing quality control, et cetera. So obviously, looking forward for the next three years, I think that's a key thing to look into.

In addition, a big reason they don’t give guidance is because MELI focuses on long-term results rather than quarterly or even yearly goals. This perfectly aligns with the vision of long-term investors in our opinion. As such, we believe MercadoLibre wants long-term shareholders who have confidence in the company's execution in the long run.

{kind=link}

Important for growth companies is to look at stock-based compensation, which can be a huge drag on the stock performance if it is a high amount. An analyst from Goldman Sachs asked the following:

If you're looking at the KPIs that determine compensation across the exact team or leadership team, how do you think these will evolve from here, again, thinking maybe over a multiple-year basis?

In response to that question, CEO Marcos Galperin emphasized that the compensation strategy for executives and key employees is based on long-term results. He states that the long-term retention program is a six-year program. In addition, he states that the company operates in a very dynamic environment, with a lot of growth opportunities, and that they are a very dynamic business.

As such, KPIs for compensation are focused on long-term performance and will continue to evolve as new businesses gain scale and relevance. The company's compensation and incentive structure is designed to encourage investment and innovation in the right areas.

Risk

MercadoLibre faces several key risks that warrant consideration for potential investors.

One primary concern is the volatility of the economies and political landscapes in the countries where the company operates. These regions are more politically and economically unstable than the U.S., leading to significant potential discrepancies between revenue growth in local currencies and dollar-denominated revenue growth.

In addition, the company is exposed to various economic risks, such as the impact of hyperinflation in Latin America or Argentina. These issues could substantially influence MELI’s financial performance, underscoring the importance of a proactive risk management strategy.

Another substantial risk is the intense competition prevalent in the e-commerce sector. Amazon has been steadily gaining ground in Brazil , a crucial market for MELI, since 2012. This poses a tangible threat to MELI’s market share and growth prospects, necessitating a vigilant approach to maintaining its competitive edge.

Despite these formidable challenges, MELI has showcased resilience, with its management adeptly navigating the intricacies of the Latin American market.

However, it's crucial to recognize that these risks may dissuade more risk-averse investors from considering the company for investment.

Therefore, a comprehensive evaluation that weighs the potential rewards against the associated risks is paramount, especially when contemplating an investment in high-growth stocks like MELI.

Conclusion

In conclusion, MercadoLibre's Q3 earnings report demonstrated impressive financial performance, surpassing expectations with a double beat on GAAP EPS and revenue. MELI’s resilience in a dynamic market is noteworthy, especially given the challenging macroeconomic environment.

Furthermore, MercadoLibre continues to invest in key aspects of its business, such as logistics and new ventures like insurance.

The company's commitment to growth is evident, reflected in the 69% YoY revenue increase and a record-breaking income from operations.

Notably, MercadoLibre's engagement with users is on the rise, driven by improvements in logistics, fulfillment, and delivery promises, resulting in a record 50 million+ unique buyers and significant market share gains.

The growth in Total Payment Volume ((TPV)), particularly off-platform TPV, showcases the strength of Mercado Pago, a key driver in the company's growth strategy. Mercado Pago's diversified financial services and expanding user engagement, including credit card issuance and improved credit quality, bode well for Mercado Libre's future prospects.

The focus on long-term results aligns with a vision for sustained growth. The company's agility in adapting KPIs for compensation to evolving business dynamics underscores its commitment to investment and innovation.

In essence, MercadoLibre's Q3 results indicate its resilience and adaptability in a dynamic market, with a strong focus on long-term growth, which aligns perfectly with a long-term investors mindset.

We believe the risks are of no concern at this moment in time as MercadoLibre has a strong track record and has shown resilience as we mentioned earlier.

As such, we rate the stock as a buy due to its impressive metrics and for investors with a 10Y+ investment horizon. In any case, if MELI drops significantly without any major changes to the fundamentals MELI is an excellent buy.

For further details see:

MercadoLibre: Expensive, But Formidable Execution