AMZN - MercadoLibre: The Best Is Yet To Come

2023-09-09 12:00:00 ET

Summary

- It is apparent that MELI's vertically integrated offerings has directly contributed to its growth flywheel across online retail, logistics, fintech/ bank, and advertising.

- Advertising may also eventually be a long-term bottom-line driver, thanks to the segment's "EBIT margins in the high 70s, low 80s."

- Therefore, it is unsurprising that MELI has smashed expectations in FQ2'23, outperforming most growth metrics while being highly profitable.

- We remain confident that its H2'23 focus on market share gains is not overly aggressive, with its reliance on debt to moderate due to its expanded retained earnings.

- We maintain our Buy rating for the MELI stock, with a long-term price target of $2.05K.

The MELI Investment Thesis Remains Highly Convincing

We previously covered MercadoLibre, Inc. ( MELI ) in July 2023, discussing BofA's downgrade thanks to Brazil's new cross-border tax rule , which resulted in a drastic pullback in its stock valuations and prices.

We had concluded that the correction had been overly done, since the company still boasted well-diversified offerings across online retail, logistics, fintech/ bank, and advertising.

For now, MELI has outdone itself again in FQ2'23, by reporting revenues of $3.42B ( +12.5% QoQ / +31.5% YoY ) and GAAP EPS of $5.16 (+30.3% QoQ/ +112.4% YoY).

Its consumer base remains sticky as well, with expanding Gross Merchandise Volume of $10.5B (+11.7% QoQ/ +22% YoY) and Total Payment Volume of $42.1B (+13.7% QoQ/ +39.4% YoY), despite the region's high inflationary pressures.

It is apparent that MELI's highly strategic flywheel has shown excellent results, with the e-commerce directly feeding into its in-house logistics segment, while similarly offering credit lines to sellers, processing consumer payments through Pago, and providing BNPL/ credit cards to buyers.

This is on top of its growing advertising segment, with an annualized FQ2'23 revenues of $672M. This development matters, since it may eventually be long-term bottom-line driver, with the management previously hinting the segment's "EBIT margins in the high 70s, low 80s. "

We have already seen Amazon ( AMZN ) achieve great success thus far, with an annualized advertising revenues of $42.72B (+12.4% QoQ/+22% YoY) by the latest quarter. This is on top of the Insider Intelligence expecting its global digital ad market share to grow to 12.4% in 2023 (+0.7 points YoY).

As a result of its multi-channel offerings, we believe that MELI still has a massive runway for growth, attributed to the nascency of the fintech/ e-commerce markets in Latin America at 11.7% in 2022, compared to the US at 21.7% in Q1'23.

In addition, MELI dominates the region's e-commerce sales with a market leading share of 21.6% and a mindshare leadership at 747.1K of monthly visits . This compares well to AMZN's market share of 37.8% in the US and 2.6B of monthly visits .

Furthermore, we are not seeing signs of deceleration for Latin America's appetite for fintech offerings. For example, PIX , the Instant Payment System launched by the Brazilian government in November 2020, has already recorded a tremendous expansion in total number of monthly transactions to 3.54T (+7.5% MoM/ +71.8% YoY) by July 2023.

PIX also recorded a monthly transaction volume of R$1.42T (+4.4% MoM/ +52.6% YoY) by July 2023, or the equivalent of $286.21B, (based on the exchange rate of 1 Brazilian Real to $0.20 at the time of writing).

These point to the high adoption/ growth cadence for fintech/ digital wallets in Brazil, with things still looking extremely promising in the intermediate term. This development is important indeed, since the country comprised 53.8% of MELI's revenues in 2022 (-1.5 points YoY).

As a result of MELI's vertically integrated offerings feeding into its growth flywheel, we remain confident that the company's H2'23 focus on market share gains is not overly aggressive indeed.

Investors may expect incremental expansion in its H2'23 operating expenses from those reported in FQ2'23 at $1.14B ( -4.2% QoQ / +11.7% YoY ) and capital expenditure from $114M (+28% QoQ/ +15.1% YoY), respectively.

Inversely, we are confident that MELI's reliance on long-term debts of $4.76B (-1.4% QoQ/ +7.4% YoY) may moderate from here, thanks to its increased retained earnings of $1.37B (+23.4% QoQ/ +122.2% YoY) in the latest quarter.

So, Is MELI Stock A Buy , Sell, or Hold?

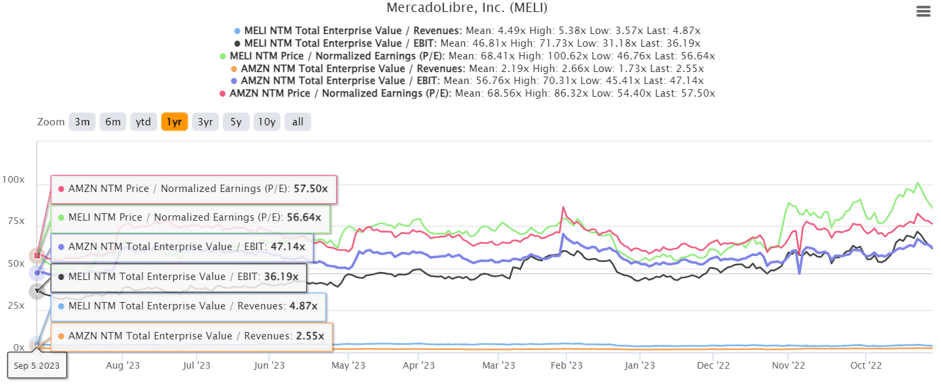

MELI 5Y EV/Revenue, EV/ EBIT, and P/E Valuations

{kind=link}

S&P Capital IQ

Despite the promising developments, MELI trades at NTM EV/ Revenues of 4.87x, NTM EV/ EBIT of 36.19x, and NTM P/E of 56.64x, moderated compared to its 1Y mean of 4.49x/ 46.81x/ 68.41x, respectively.

For now, we believe that the stock appears to be trading at reasonable valuations, since it is expected to generate an impressive top/ bottom line CAGR of +25%/ +56.2% through FY2025, compared to its historical CAGR of +52.3%/ +19.2% between FY2016 and FY2022.

Investors must also note that due to Latin America's geopolitical uncertainty, the MELI stock's valuations have been somewhat discounted compared to its e-commerce peer, AMZN at NTM EV/ EBIT of 47.14x and NTM P/E of 57.50x.

As a result of these factors, we are optimistic that MELI is still a viable long-term play here, attributed to the excellent +43.2% upside potential to our long-term price target of $2.05K, based on the consensus FY2025 EPS estimate of $36.29 and its NTM P/E.

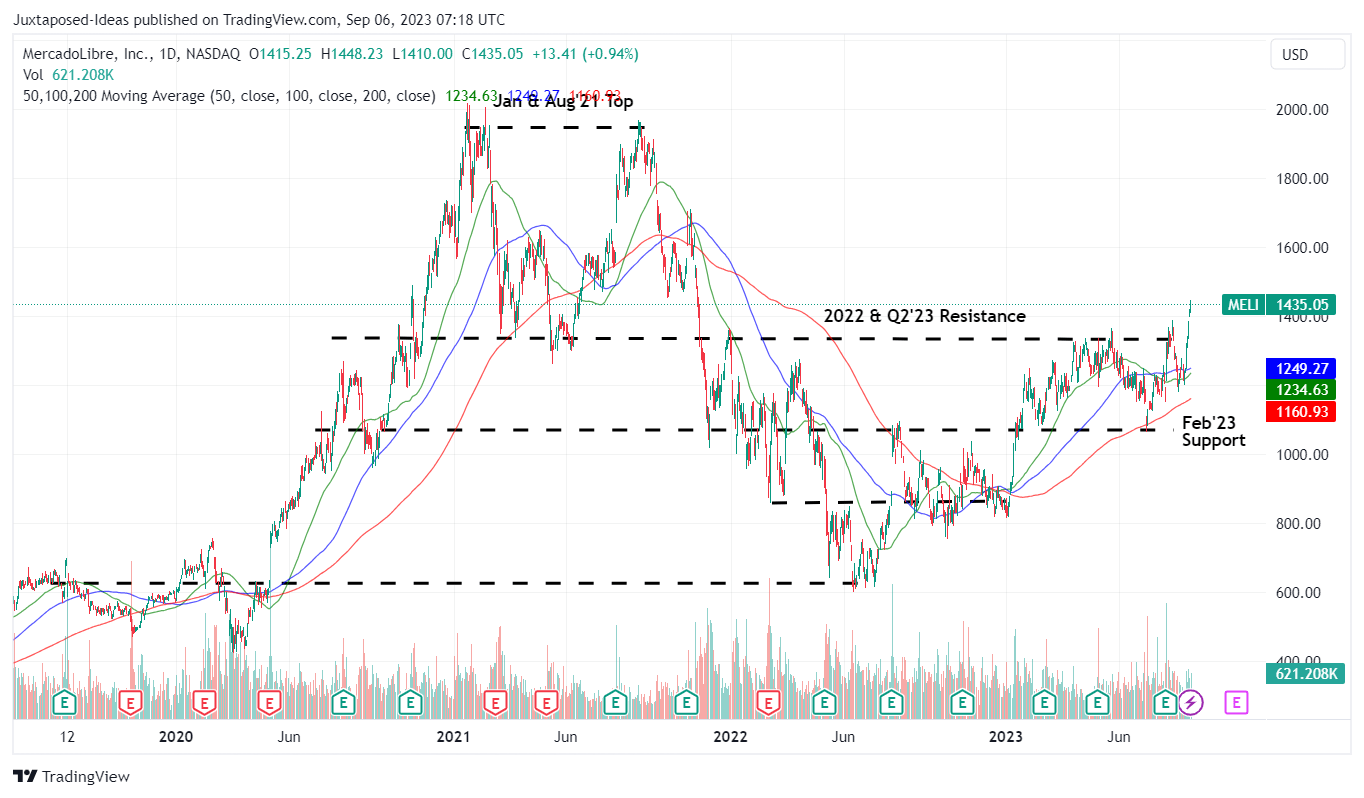

MELI 5Y Stock Price

{kind=link}

Trading View

For now, it appears that MELI has momentarily broken out of its previous resistance levels of $1.35K, with it remaining to be seen if the rally is sustainable.

However, we are also confident that the stock's previous February 2023 support level of $1.1K will hold, especially due to its FQ2'23 outperformance. Therefore, investors looking to add may still do so, depending on their dollar cost averages.

We maintain our Buy rating for the MELI stock.

For further details see:

MercadoLibre: The Best Is Yet To Come