META - Meta Platforms: A Big Move To Capitalize On The Proliferation Of Meta Quest

2023-06-27 13:01:46 ET

Summary

- Meta Platforms, Inc. introduced Meta Quest+, a subscription service for its virtual reality headsets, offering access to specialized gaming content.

- The service could generate significant high-margin revenue if it can leverage its large user base and build a diverse content library.

- Despite potential long-term success, initial adoption may be slow, and the company faces competition from well-established gaming firms.

So far, all things related to the metaverse that Facebook parent Meta Platforms, Inc. ( META ) has come out with have failed to really gain the kind of traction and generate the kind of revenue that the market would have liked to see. But the good thing about the company is that it generates a significant amount of cash flow alrighty and it can utilize that cash flow in order to continue rolling out new and interesting initiatives.

The latest such attempt was revealed on June 26th, when management announced the launch of Meta Quest+. Playing off of the Meta Quest headset that the company is now in the third generation of building, Meta Quest+ Is the company's first subscription service that's founded off of the idea that consumers might be willing to pay a regular monthly price for access to specialized gaming content. This is a big move for the company. In the short run, it's unlikely to move the needle much in terms of revenue. But in the long run, it does have the chance of creating a lot of value for the company.

Introducing Meta Quest+

On June 26th, the management team at Meta Platforms confirmed that, effective July 1st, users of its Meta Quest 2 and Meta Quest Pro headsets will be able to subscribe to a monthly service that will entitle them to receive access to two handpicked virtual reality games each month. For July, the first two games being offered up are called Pistol Whip and Pixel Ripped 1995 . And in August, the games that the company is launching are Mothergunship: Forge and Walkabout Mini Golf . Those who sign up no later than July 31st will receive their first month of the service priced at only $1. But each month after that, the price will be $7.99, or $59.99 per year if paid up front.

So far, the company has struggled to make significant progress on its metaverse investments. In 2022 , for instance, its Reality Labs segment, which focuses on all things metaverse, including its Meta Quest headsets, generated revenue of $2.16 billion. Despite that, it reported an operating loss of $13.72 billion. That followed a $10.19 billion loss during 2021. And more likely than not, the company will lose money on the segment this year as well. These investments and the lack of fruit that they have so far been responsible for bearing, caused shares of the company to fall more than 70% at one point late last year. But as the market has come to terms with the overall health of the company more broadly and as the market looks forward to the opportunities presented by AI, shares have staged a remarkable comeback.

It is my opinion that the launch of this subscription service will initially struggle to gain traction. But in the long run, if Meta Platforms plays its cards right, it could prove to be a big money maker for the enterprise. I say this based in part on the sheer size of Meta Platforms and what the company has accomplished so far with its virtual reality headsets. Across the entire family of platforms that Meta Platforms has, the company boasts 3.81 billion monthly active users. Of these, 3.02 billion utilize the service daily.

Leveraging this astronomically large network, Meta Platforms sold, by October of last year, an estimated 20 million of its virtual reality / augmented reality headsets. Although the company has not provided any official estimates, some sources maintain that the number of monthly active users of these headsets came out to 6.37 million in October of 2022. Almost certainly, that number is higher today, though we have no idea by how much. We do know, however, that, come this fall, Meta Platforms will be selling the new Meta Quest 3, with a starting price of $499.99 for the 128-gigabyte version. This, combined with the company's decision to lower pricing this fall on the older version of the device should help to fuel further growth.

Despite these fairly impressive numbers, it is also true that the company has in many respects struggled to make its investments in the virtual reality and augmented reality market work. For instance, late last year, the company had to significantly revise lower its expectations when it came to its Horizon Worlds platform. For those who don't know, Horizon Worlds is a "social universe" that allows users to create and visit different spaces so that they can hang out, play games, meet people, and more. After early explosive growth following the company's decision to expand the experience to all Meta Quest users throughout the U.S. and Canada, growth slowed significantly. According to some reports , only about 9% of the worlds that were built were visited by 50 or more people. And the company was forced to decrease its expectations for the number of monthly active users by the end of 2022 from 500,000 to 280,000 because of this.

Author

*Revenue, with $ in Millions.

In the event that Meta Platforms can grow its subscription service to all of the monthly active users currently patronizing the Meta Quest platform, and if they all pay monthly instead of annually, that would work out to roughly $611 million of additional revenue per year, much of which would be incredibly high margin in nature. But with billions of monthly and daily active users across the company’s family of apps, it wouldn't take much for this to become a line of business that generates a few billion dollars of high margin revenue per year. In the table above, you can see some hypothetical scenarios for what the financial picture of the service might look like.

As I said earlier in the article, I expect adoption for this subscription to be rather slow. This is because the primary draw to the platform is the ability to pick any two games per month. But at the start, it will only have two games to choose from. It will take several months at that pace before it builds up a meaningful library of content that might serve as a draw for a rather diverse set of users. There is also risk that the company is taking a top down approach to this as opposed to a bottom up approach. Prioritizing a set number of games each month and hoping customers latch on is risky because the company is then leading from the objective of generating strong revenue as opposed to leading with the goal in mind of creating a quality experience that consumers will gravitate toward.

{kind=link}

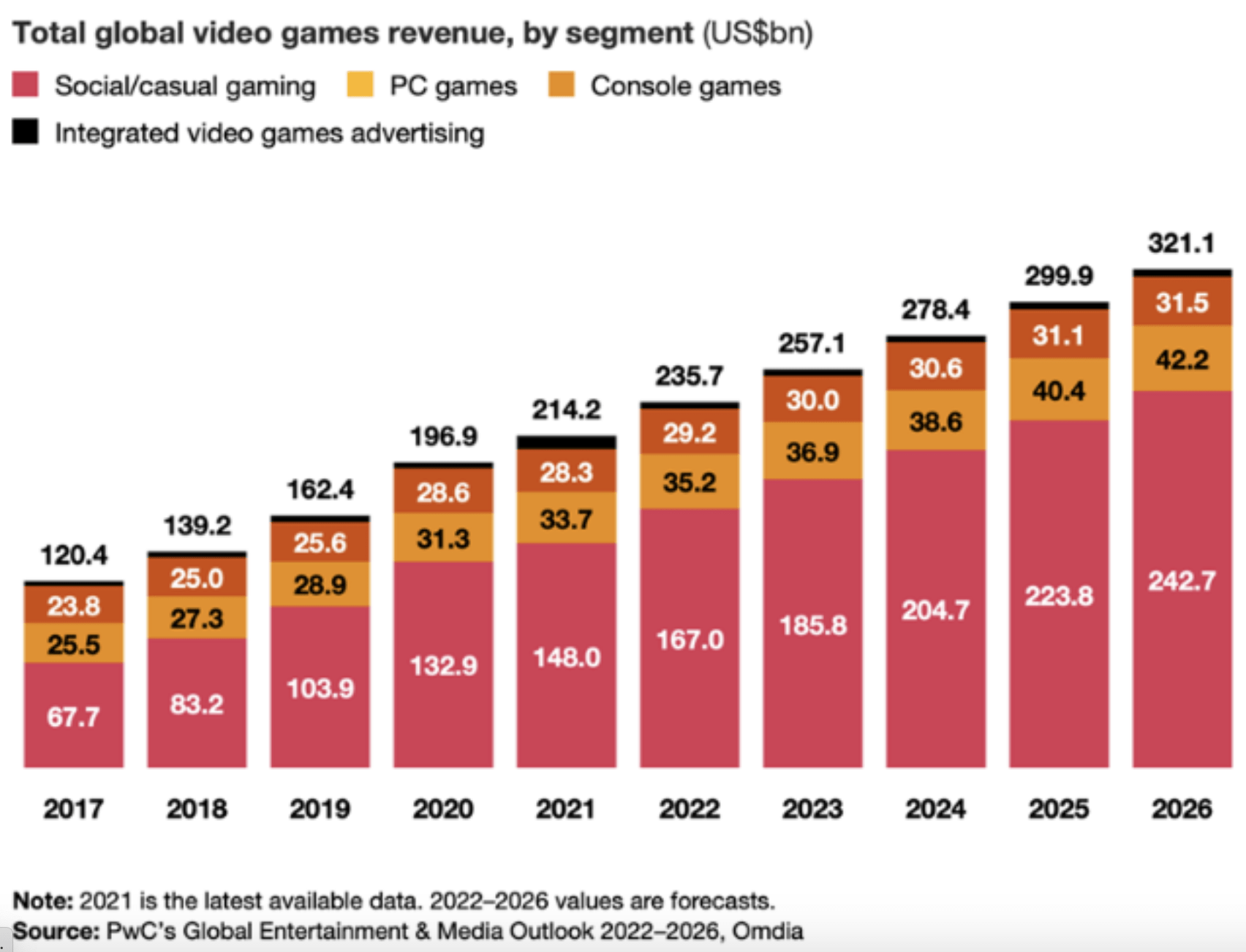

While I applaud the company's decision to get into the $257.1 billion gaming market, $185.8 billion of which is focused on social and casual gaming, I do also believe that a more appropriate approach by the company would have been to follow the direction that Microsoft ( MSFT ) has with its planned acquisition of Activision Blizzard ( ATVI ). Entry into this market by acquisition is incredibly common and it allows companies to immediately establish themselves as significant players in the market.

Another example of this strategy can be seen by looking at Activision Blizzard and its purchase of King Digital back in 2015. That deal cost the company $5.9 billion. Over the past three fiscal years, revenue generated by King Digital has grown from $2.16 billion to $2.79 billion, while operating profits have grown from $857 million to $1.12 billion. 243 million of the 365 million monthly active users that Activision Blizzard’s properties serve are strictly through King Digital. Instead, Meta Platforms is trying to grow its own gaming operations from virtually scratch, meaning that it has to nudge out well established firms that already have captive audiences. This certainly can be done given the massive network that Meta Platforms has. But it is the more difficult road to travel.

Re-evaluating shares

Late last year, I made a very contrarian decision and decided to pull the trigger on shares of Meta Platforms. I placed a modest amount of my capital into the stock after units had almost completely bottomed out. In retrospect, I wish I had allocated a lot more to that investment, because it ended up being one of the most successful I have made over the past year or so. By the time I cashed out earlier this year, I very nearly doubled my investment in the company. I based my decision to buy off the idea that the company can shut down its metaverse operations at any moment and see its cash flows skyrocket in response. Shares of the business were very cheap and the core of the enterprise was healthy.

Almost as big a mistake as not putting in enough capital to the investment was my decision to sell when I did. In early February of this year, I ended up downgrading the company from a ‘strong buy’ to a ‘buy’. It was shortly after that that I ended up selling off my units in the company, with the final chunk of shares being sold off on March 10th. Since the publication of that downgrade article , shares of the company have shot up another 47.5% at a time when the S&P 500 (SP500) is up only 3.6%. When you run the math, what ended up being nearly a double for me could have been a triple.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Meta Platforms |

| 15.7 |

| 15.0 |

Using the same numbers as I used in my most recent article valuing the company, but adjusting for the continued increase in share price we have seen, I calculated that the firm is trading at a forward price to operating cash flow multiple of 15.7 and at an EV to EBITDA multiple of 15. For a slow growing firm that is admittedly an industry leader, this is not a bad price. I am also encouraged by the company’s other initiatives, such as its Meta Verified offering.

I do think the firm is likely to succeed when it comes to this latest endeavor as well. But I also believe that the road will be a fairly long one that shareholders will have to put up with. As for how shares are priced and what that means moving forward, I would argue that the market probably has yet to fully account for the value that the business offers. But I also think that further upside from here is now likely to be anywhere near what it has been over the past several months.

Takeaway

Based on all the data provided, I will say that Meta Platforms, Inc. is making some interesting moves. If the company can build a healthy and vibrant ecosystem of content and if it can leverage its unparalleled network to distribute both its headsets and its subscription services, then it could very well go on to generate many billions of dollars of additional high margin revenue each year moving forward. Add on top of this how Meta Platforms shares are priced, and I still remain bullish enough to have the company rated a "buy." But I would also argue that if Meta Platforms stock appreciates another 10% to 15%, a further downgrade to a "hold" would probably be warranted.

For further details see:

Meta Platforms: A Big Move To Capitalize On The Proliferation Of Meta Quest