MEI - Methode Electronics: Still Not A Buy Even After The Big Correction

2023-12-21 06:37:23 ET

Summary

- MEI's stock price has corrected by over 34% since July and is still under selling pressure.

- Q2 FY24 results showed a decline in net sales, mainly due to underperformance in the automotive and interface segments.

- Technical analysis indicates bearish price action, with the stock breaking its 200 ema and support level, suggesting further downside risk.

I wrote on Methode Electronics (MEI) in July, and I warned investors that MEI seems to be under selling pressure and to avoid it. Since then, its stock price has corrected by more than 34%. It recently posted Q2 FY24 results , and I will analyze it in this report. I think it is still not the best time to buy MEI, even after such a big correction, and I will discuss the reasons behind my saying it. I assign a hold rating on MEI.

Financial Analysis

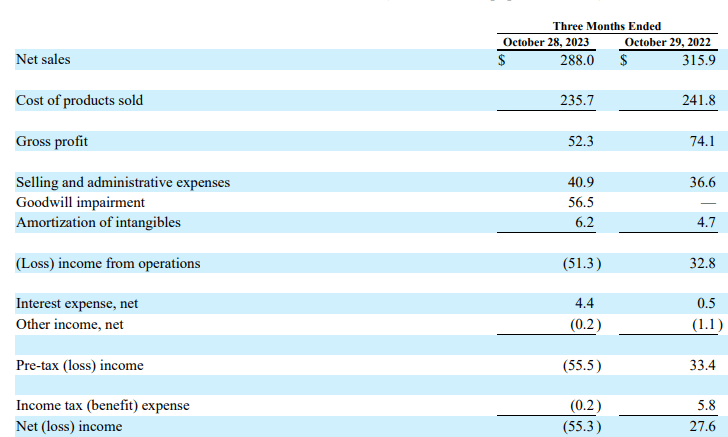

It recently posted its Q2 FY24 results . The net sales for Q2 FY24 were $288 million, a decline of 8.8% compared to Q2 FY23. Underperformance in its automotive and interface segments was the main reason behind the sales decline. The sales from the automotive and interface segments declined by 21.6% and 17% in Q2 FY24 compared to Q2 FY23. The decline in automotive segment sales was mainly due to lower sensor sales in Europe due to the overstocked e-bike market and the UAW strike in North America. The low demand for its data solutions products affected the interface segment. It suffered a goodwill impairment charge of $56.5 million in Q2 FY24. So if we exclude this charge, then its adjusted operating income comes out to around $6 million, which is way lower compared to the Q2 FY23 operating income of $33.3 million. The margins and operating income were both affected by higher freight and labor costs and operational inefficiencies.

{kind=link}

Its adjusted net income for Q2 FY24 was $2.4 million, compared to $27.6 million in Q2 FY23. Higher interest expense also affected its profitability, other than lower sales and operational inefficiencies. The current picture of MEI looks worse than when I covered it last time. The sales saw a dip, and the overstocked e-bike market can continue to present challenges to the company in the coming quarters. Its margins are already under pressure due to high labor and freight costs, and if the sales continue to dip, then it might get worse for them. Additionally, its increasing long-term debt is also a matter of concern. Its long-term debt as of October 2023 stands at $329 million, which was $303.6 million in April 2023. So, the high freight costs and increasing debt can restrict its profitability.

Technical Analysis

{kind=link}

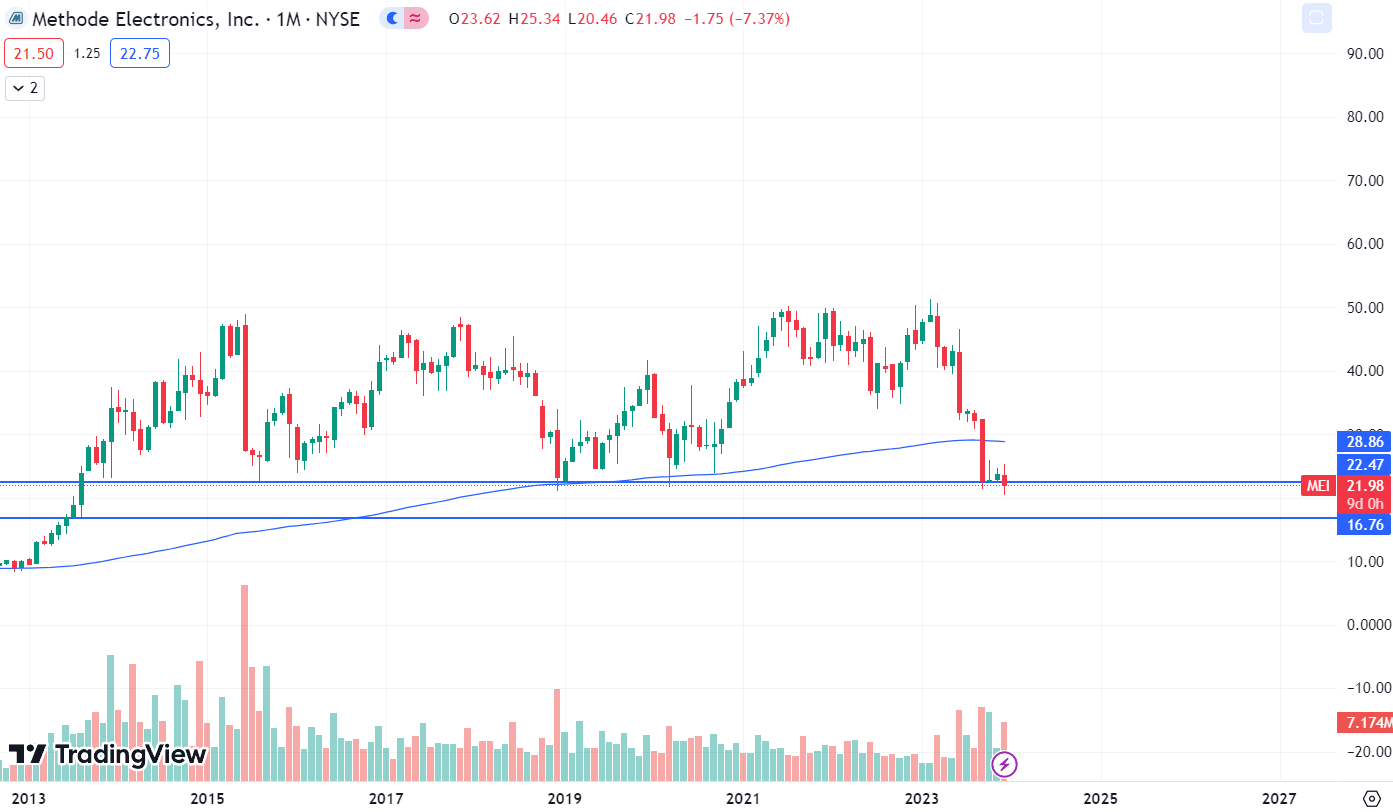

It is trading at $22. I am doing a monthly time frame analysis of MEI, and I just have to say one thing. It doesn’t look good for MEI because the price action is quite bearish. The stock price has broken its 200 ema and the support level of $22.5. Talking about why the breaking of 200 ema is alarming. The stock has broken its 200 ema for the first time since 2012. Even during the COVID crash, the stock price took support from its 200 ema, but didn’t break it. However, in September 2023, the stock broke the 200 ema with a huge red candle, which shows that there is a weakness in the stock. In addition, it also broke its support level of $22.5. The $22.5 level was a support zone for the stock for the last ten years. So, the stock breaking the support zone is a bearish sign. So, considering these two factors, I think there is a lot of selling pressure present in the stock, and it would be good to avoid it. The next support for the stock is at $17, which is around 23% lower than the current price level. Hence, the downside risk is high in this case. So I advise you to avoid it.

Should One Invest In MEI?

Generally, when a stock is near a strong support zone, it is usually time to accumulate a stock. But this is not the case in MEI. Despite correcting so much in recent times, I think it is best to avoid MEI. Its financial condition isn't looking good; sales growth has dropped, margins are still under pressure, and rising debt might pose a threat to its profitability. Looking at the market conditions, I think the market isn't offering any significant growth opportunities. The overstocked e-bike market in Europe might hamper its sales growth, at least in the short term. Its valuation aspect also doesn't provide any opportunity. It is trading at a P/E [TTM] ratio of 25.75x, which is above the sector median of 22.16x. Hence, despite the big fall MEI has experienced in recent times, I believe it is not the right time to buy it. It is struggling financially, and the technical chart is alarming. Hence, one should avoid MEI.

Risk

Most of their earnings come from business dealings with the automobile and commercial vehicle industries. Negative factors that impact these industries also have an adverse effect on their operations, finances, and business. Automobile production and sales are quite cyclical and rely on several variables, including customer confidence and preference, in addition to the overall state of the economy. Any negative event that results in a decline in sales volumes in these industries or in an overall downturn in the business of their customers in these industries could harm their business and operational results. Examples of such events include recessions, industry slowdowns, rising interest rates, rising fuel costs, costly or restrictive regulations, excessive inflation, prolonged disruptions in one or more of their customers' production schedules, labor disturbances, or work stoppages.

Bottom Line

Its share price has fallen over 30% percent in recent times, and despite correcting so much, I think it is still not the best time to buy it. MEI is struggling financially; the technical chart is quite bearish, and the stock price can fall even further. So, I think it is not the best time to buy it; hence, I stay with my rating of hold.

For further details see:

Methode Electronics: Still Not A Buy Even After The Big Correction