META - MicroCloud Hologram: Promising Market But Latest Financials Suggest Caution

2023-09-13 05:41:11 ET

Summary

- MicroCloud Hologram's stock price has risen over 334% YTD, prompting a closer look at the company, which provides holographic advanced driver assistance systems and other holographic solutions.

- The holographic display market is projected to see healthy growth, indicating a promising future but HOLO's revenues have nosedived in H1 2023 and provisions for doubtful accounts are up too.

- The company also faces competition from big US based tech companies as well as homegrown ones, which indicate need for caution for now.

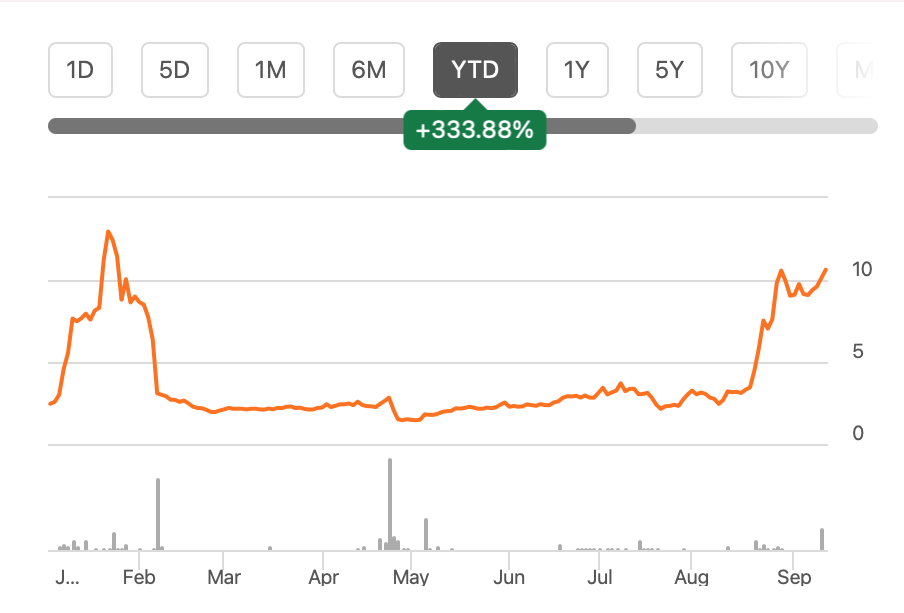

China's holographic technology company MicroCloud Hologram ( HOLO ) has done exceptionally well at the stock markets this year, with an over 334% rise in its price year-to-date [YTD]. This calls for a closer look at what’s really going on with it and of course, whether it’s a good buy right now.

{kind=link}

What it does

The company describes itself as “one of the leading holographic digitalisation technology service providers in China”, in terms of revenue and intellectual property rights [IPRs].

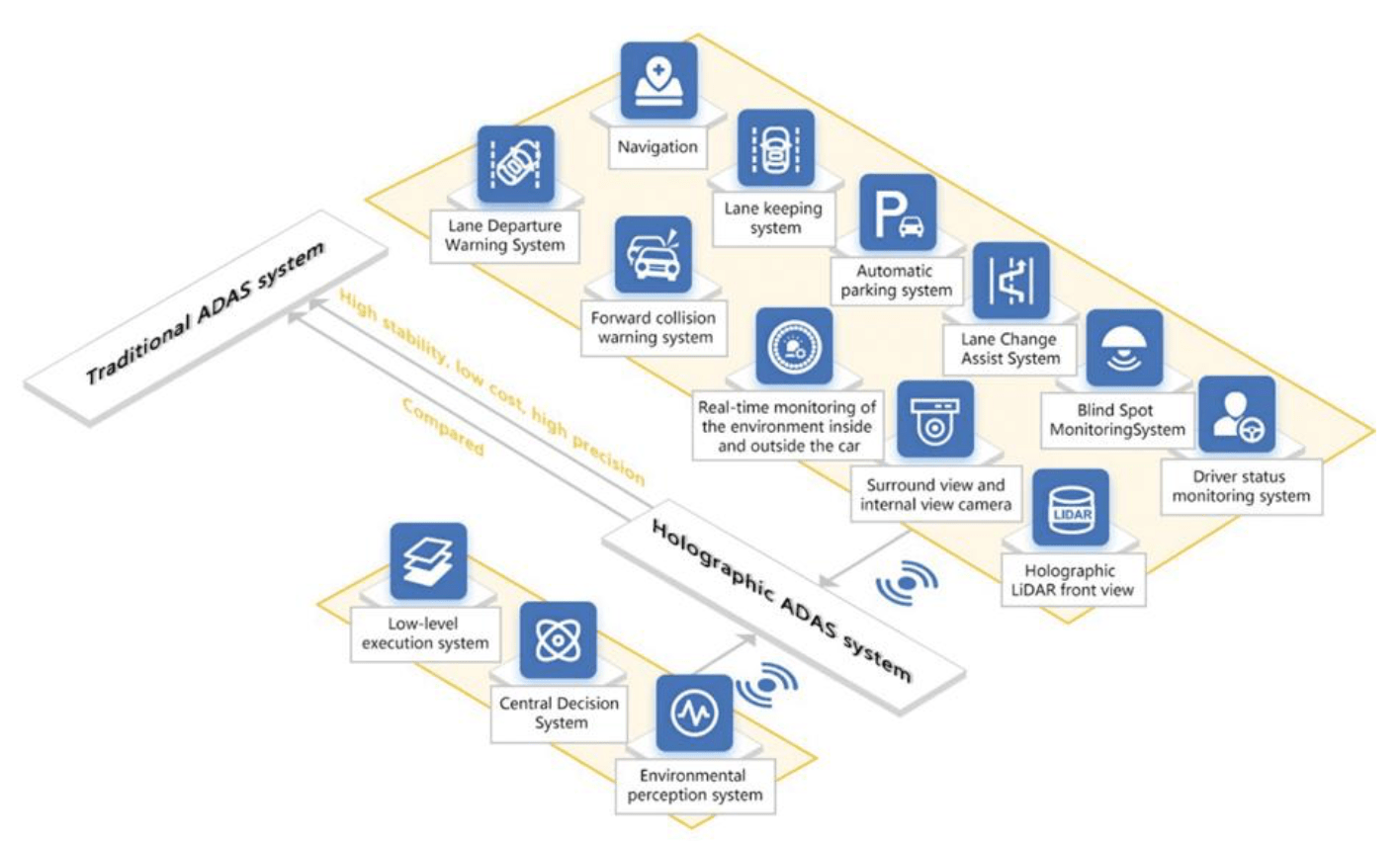

It provides holographic advanced driver assistance systems [ADAS], which can monitor the environment around the vehicle in real time, supporting in functions like navigation, lane changing and forward-collision warning systems. It has both a cost and precision advantage over traditional ADAS, and the company is a direct supplier to automotive brands for this service.

{kind=link}

Supporting the system are its holographic light detection and ranging [LiDAR] solutions, which are also counted as services separate from the ADAS. These include efficient image processing technologies, point cloud algorithm architecture and sensor chip design. It also provides advertising and software development kit services.

MicroCloud Hologram also expanding into new products like virtual holographic human being, which can be an answer to ChatGPT in that it provides answers for a variety of questions. Most recently, it has made a foray into healthcare , with treatments for patients with functional disorders. It also already works with government agencies and software developers.

Market opportunity

The holographic display market has a promising future, with projections of a compounded annual growth rate [CAGR] of 29.1% between 2021 and 2030 to reach a size of USD 11.7 billion. The company itself has seen good growth of 29% in revenues and 11.8% in customers in 2022.

That there's sufficient demand for its products and services is evident in the fact that it earns revenues from a number of customers. This also reflects greater potential stability than if it were dependent on only one or two key clients. It has only customers with over 10% share in operating revenues. And around 60% of its revenues are made up for by its biggest 10 customers.

The financials

Weakening revenues

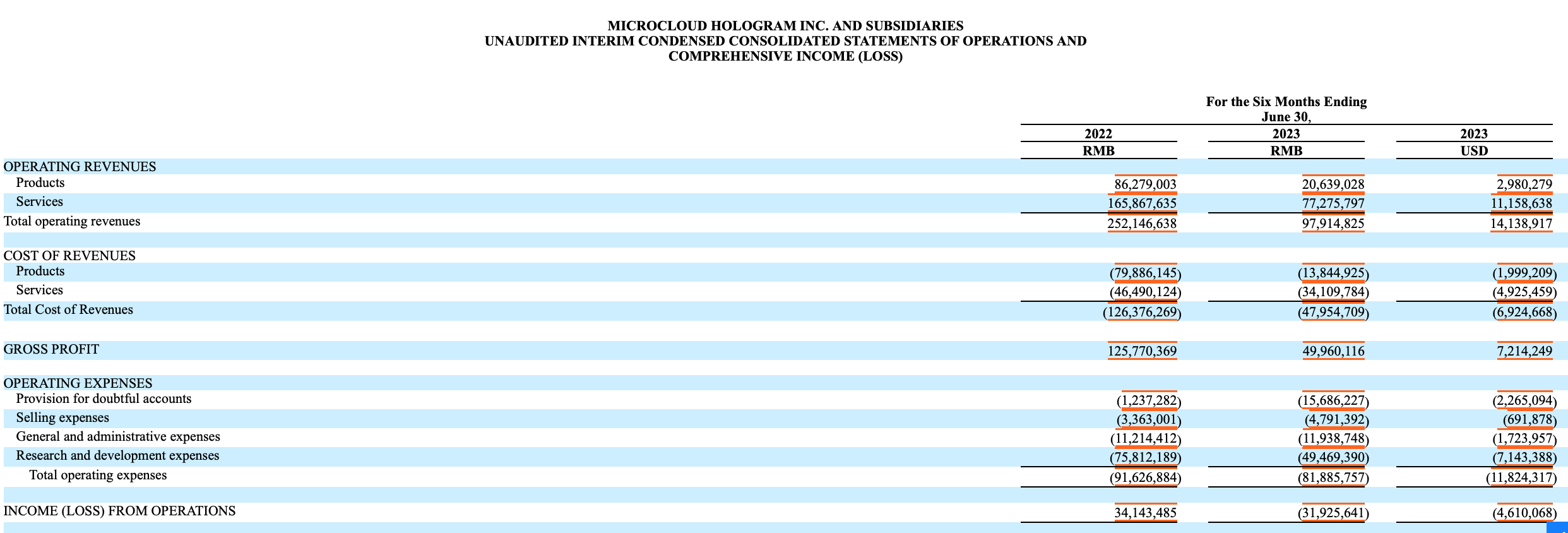

The company’s 2022 revenue numbers, as seen below were strong, driven by the company’s business development efforts. However, come 2023, for which we have numbers up to June 30, 2023 (H1 2023), the operating revenues took a nosedive, declining by 61.2%.

{kind=link}

For the first quarter, the company attributed its weak performance to the state of the global economy, which it said hasn't quite recovered. It also mentions China’s Spring Festival holiday, which resulted in lower consumer demand. No details are available for the second quarter so far.

While the explanation for the holiday season is understandable, that of global demand, not so much. In fact, in the first quarter of this year, China had opened up after lockdowns in 2022. It follows that demand should have actually improved during this year.

This, combined with an almost 13x year-on-year (YoY) increase in provision for doubtful accounts is actually a big red flag to me. The number had already risen by 4x YoY in 2022, and now it is even bigger. While the company is indeed growing its customer base, this reflects that the quality is probably not the best.

Declining R&D expenses

It’s also disappointing to see a 35% in research and development expenses, which is crucial spending for the company’s technological innovations. There's some comfort to be found from the fact that the company more than doubled its spending on the head in 2022 from the year before. Still, it's something to follow in the next updates.

Healthy gross margin

There’s something to be said for the company’s gross margins, though, which actually improved to 51.2% during H1 2023, compared to 49.9% during H1 2022, and 45.8% for the full year 2022. After recording an operating and even net profit in 2021, it has however fallen into a loss at both levels now on account of increased expenses. Not all the expenses are bad though, they are part of the company’s growth.

The risks

There are also risks to consider here. The first is competition. There are companies across the world that are innovating in holographic , including the tech heavyweight Microsoft ( MSFT ). More generally, companies like Apple ( AAPL ), Meta Platforms ( META ) and Nvidia ( NVDA ) are also engaged in the AR/VR space . As the market matures, it's quite possible that the company could face even stiffer competition.

Even if we factor in that China’s technology market could get increasingly insulated from big American tech companies given current climate of mistrust between the US and China, the fact is that there’s homegrown competition too. One example is WiMi Hologram ( WIMI ), which too is listed on NASDAQ.

That geo-political stresses could impede its expansion is another risk to consider, though it can be balanced by lesser competition in the home market. There’s also the risk of the industry still being relatively new. It’s entirely possible that the adoption of holographics in its target industries isn't fast enough or its technologies don't get adopted. Its latest revenue dip is already a cautionary sign.

What next?

HOLO’s market multiples look rather high after its price rise this year, with a trailing twelve months [TTM] price-to-sales (P/S) ratio at 9.5x compared to 2.6x for the tech sector. While the company’s growth was good in 2022 and there might be investor optimism on its latest innovations, I’m not sure if these are enough to justify the multiple. Moreover, the fact that it seen a sharp drop in the first quarter of 2023 definitely makes a case against it.

The company’s big provisions for doubtful accounts also indicate a need for caution. There are also risks to further growth from competition, including from big tech companies and the growing stresses between the US and China.

Still, for now I do believe that there could be potential for it in the fast growing holographic market over time. And all said and done, its share price has risen by just 7% since listing, despite its big rise this year. I’m going with a Hold on MicroCloud Hologram.

For further details see:

MicroCloud Hologram: Promising Market But Latest Financials Suggest Caution