META - Microsoft: Buying Opportunity In The Making

Summary

- Compared to many other big tech companies, Microsoft Corporation could report great quarterly results with revenue still increasing 10%.

- Microsoft is not completely recession-proof, but its subscription model and the efforts to widen the company's moat will probably lead to stable performance.

- Microsoft stock might be fairly valued, but I see further downside potential in the coming quarters.

Among the major U.S. technology companies, Microsoft Corporation ( MSFT ) – together with Apple Inc. ( AAPL ) – is one of the businesses that is still trading rather closer to previous highs. This might be a funny way to put it, as Microsoft also has declined about 30% from its previous highs and Apple declined about 27%. However, both have performed better than the Nasdaq 100-Index (NDX), which has declined about 34%. And they have performed much better than Alphabet ( GOOG ) – which declined about 41% - as well as Amazon – which declined about 55% - and much better than Meta Platforms ( META ) – which declined 70% (all numbers at the time of writing).

In the following article, we take a look and try to answer the question if the outperformance compared to its “peers” is justified. And as the stock has declined about 24% since my last article was published (in which I argued that Microsoft might be fairly valued), we have to ask once again if Microsoft is a bargain now.

Quarterly Results

In October 2022, Microsoft reported results for its first quarter of fiscal 2023, and the company showed it can still report high growth rates. Revenue increased from $45,317 million in the same quarter last year to $50,122 million this quarter – resulting in 10.6% year-over-year growth (and revenue increased even 16% in constant currency). Operating income also increased from €20,238 million in Q1/22 to $21,518 million in Q1/23 – an increase of 6.3% year-over-year.

Microsoft Q1/23 Investor Presentation

{kind=link}

However, diluted earnings per share declined 13.3% from $2.71 in the same quarter last year to $2.35 this quarter, and free cash flow also declined from $18,370 million in Q1/22 to $16,915 million in Q1/23 – a decline of 7.9% year-over-year.

When looking at the three different segments, “More Personal Computing” saw its revenue slightly decline from $13,366 million in Q1/22 to $13,332 million in Q1/23. The other two segments contributed to revenue growth with “Productivity and Business Processes” increasing 9.5% year-over-year to $16,465 million and “Intelligent Cloud” could increase revenue 20.2% YoY to $20,325 million.

{kind=link}

And despite potential headwinds, analysts are still expecting revenue to increase in the mid-to-high single digits in fiscal 2023 while earnings per share are expected to grow in the low-to-mid single digits.

Subscription Model

The stock of Microsoft performed better than many of its big tech peers (see above). Microsoft only declined about 34% since its all-time highs while Alphabet declined about 42%, Amazon declined about 54% and Meta Platforms declined even 65%. When looking at the revenue growth rates in the last four quarters, we can clearly identify a reason why Meta Platforms performed so horrible and revenue growth for Alphabet also slowed down quite a bit.

| YoY Revenue growth/decline | Last Quarter | -2 Quarters | -3 Quarters | -4 Quarters |

|---|---|---|---|---|

| Meta Platforms | ||||

| -4.47% | ||||

| -0.88% | ||||

| 6.64% | ||||

| 19.95% | ||||

| Alphabet | ||||

| 6.10% | ||||

| 12.61% | ||||

| 22.95% | ||||

| 32.39% | ||||

| Amazon | ||||

| 14.70% | ||||

| 7.21% | ||||

| 7.30% | ||||

| 9.44% | ||||

| Microsoft | ||||

| 10.60% | ||||

| 12.38% | ||||

| 18.35% | ||||

| 20.09% |

But these numbers alone don’t show us why Microsoft’s stock performed better (as growth rates also slowed down). Aside from many other reasons (valuation multiples can play a role), the subscription model of Microsoft might be one of the main reasons for the better performance. While Meta Platforms and Alphabet are relying heavily on advertisement for revenue and Amazon is generating most of its revenue by one-time sales (as every shopping decision is a new one and I might purchase my items somewhere else although Amazon Prime is lessening that effect), Microsoft is generating a huge part of its revenue by a subscription model. And of course, LinkedIn is generating part of its revenue by advertisement and Microsoft is also generating revenue by one-time sales, but recurring revenue is quite high.

Companies might stop advertisements (or reduce the amount spent) when times are difficult, and shoppers might reduce the amount spent during a recession. However, I (and many others) won’t terminate my subscription of Microsoft 365 and companies probably won’t stop using Microsoft Teams or terminate contracts for Microsoft Azure.

Performance During Recession

However, it would be wrong to call Microsoft recession-proof. When looking at the chart we can see that Microsoft did not react to the recession in the early 1990s, but the company was in its high growth phase back then. From 2000 going forward, Microsoft reacted to every recession. And especially when looking at earnings per share, we see several declines after the Great Financial Crisis.

One could argue now that Microsoft has a different business model today than it had 10 years ago. While Microsoft was dependent on one-time sales (for example people purchasing a new computer today with a new operating system) it is now generating a significant part of its sales from subscriptions. And while the purchase of a new computer might be postponed during a recession, subscriptions are much stickier. And we can make the argument that Microsoft sales and EPS could be more stable during the next recession.

Widening Its Moat

And Microsoft generating more and more sales by subscriptions is widening the moat of the business. Another example how Microsoft is widening its moat is by making products like Microsoft Teams embedded more and more in everyday working routines. During the last earnings call , CEO Satya Nadella commented:

As we emerge from the pandemic, we are retaining users we have gained and are seeing increased engagement, too. Users interact with Teams 1,500 times per month on average. In a typical day, the average commercial user spends more time in Teams chat than they do in e-mail, and the number of users who use four or more features within Teams increased over 20% year-over-year.

Teams is becoming a ubiquitous platform for business process. Monthly active enterprise users running third-party and custom applications within Teams increased nearly 60% year-over-year, and over 55% of our enterprise customers who use Teams today also buy Teams Rooms or Teams Phone.

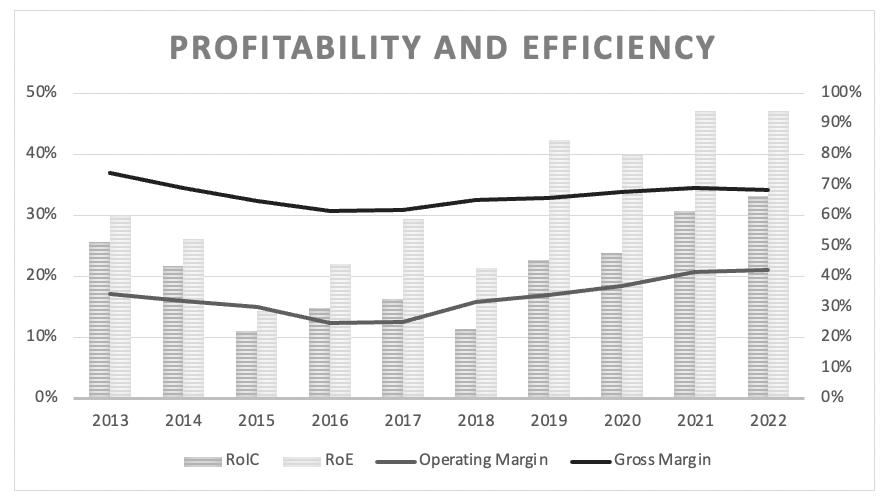

And Microsoft already has an extremely wide moat around its business, which is not only based on its brand name, but also on network effects and switching costs (see my first article about Microsoft for more details). The job of a CEO is to widen the economic moat – and so far, Nadella is doing a great job. And once again, the economic moat is also visible in the reported numbers.

Microsoft: Gross margin, operating margin, return on invested capital (Author's work)

{kind=link}

Not only could Microsoft improve its margins in the last few years again – which is a good sign – the company also reported an average return on invested capital of 21.19% in the last ten years. And such a high number is usually a clear sign for a wide economic moat around a business.

Activision Blizzard Deal

Almost a year has passed since Microsoft announced its intent to acquire Activision Blizzard ( ATVI ) and although Microsoft has expected the process to take some time (about a year), we must assume it will take several more months before a decision is made. Microsoft is still confident that the deal is going through, but major regulatory agencies like the Federal Trades Commission are fighting the deal. While the UK antitrust agency recently announced its review will take until late April 2023, the FTC has filed a suit to block the acquisition in December 2022.

Microsoft certainly wants to acquire Activation Blizzard – however it can just wait as it is neither dependent on the acquisition nor does it need any financing. With $107.3 billion in very liquid assets on its balance sheet ($22.9 billion in cash and cash equivalents as well as $84.4 billion in short-term investments) Microsoft is positioned to acquire Activision Blizzard at any time.

Intrinsic Value Calculation

The question remains if Microsoft is not only a great business but also a bargain. When looking at the price-earnings ratio, Microsoft is trading for 24 times earnings right now, which is clearly below the average of the last ten years (which was 29.03). But before jumping to the conclusion that Microsoft is a bargain, we should neither forget that the last ten years saw extraordinary valuation multiples for many companies nor that a valuation multiple of 24 is not a low number. And when looking at the price-free-cash-flow ratio, Microsoft is trading for 27 times free cash flow – above the 10-year average of 23.25.

When looking at the valuation multiples, we should not forget that Microsoft is growing with a high pace and simple valuation multiples don’t reflect high growth rates. Instead, we are always using a discount cash flow calculation to determine an intrinsic value for a stock. In the last four quarters, Microsoft generated $63,334 million in free cash flow and when assuming a 10% discount rate as well as 7,458 million in diluted outstanding shares, the company must grow about 7% in the next ten years followed by 6% growth till perpetuity in order to be fairly valued (would lead to an intrinsic value of $227.89).

It is hard to argue that Microsoft should not be able to achieve these growth rates – at least when looking at past performance. In the last ten years, Microsoft grew earnings per share with a CAGR of 17.04% and in the last five years the average growth rate was even 28.92%. But we should not get carried away as we are facing at least two (potential) problems.

Problem I: Margin contraction

A first problem could be contracting margins. When looking at Microsoft in the last three decades, we don’t see clear contractions during recessions. However, we also see Microsoft reporting much lower margins in most years compared to right now and some reversion to the mean is not unlikely (despite us being able to argue with an improved business model).

Problem II: High growth rates

High growth rates are usually not a problem – however, they can be problematic when investors assume extremely high growth rates will continue in the years to come. At some point a reversion to the mean is likely and we saw above that Microsoft already had to report declining earnings per share several times in the past. When looking at the chart we see that phases of high growth have often been succeeded by phases of moderate growth rates.

Both risks are not clear risks that emerge on the horizon – we are rather talking about possibilities and potential risks we should take into account. And all in all, I would be confident that Microsoft should be able to grow in the mid-to-high single digits and could be fairly valued right now.

Technical Analysis

Although Microsoft could be fairly valued, I assume the stock will decline further in the coming quarters – hand in hand with the overall market. And therefore, it makes sense to identify support levels where we could buy the stock.

Microsoft Monthly Chart (TradingView)

{kind=link}

In theory, Microsoft could fall back to its breakout level. A pullback to that level happens quite often. However, in case of Microsoft, it would mean the stock will decline to a range between $55 and $60, which is quite unrealistic. This would result in a decline of 83% and although we saw several stocks decline that much, I don’t see this happening for Microsoft.

A more reasonable (and in theory also possible) target for Microsoft could be the area around $90. At this level we find the 23.6% Fibonacci retracement as well as the 200-months simple moving average, which is often the price area where stocks find the bottom in a bear market. This would still result in a decline above 70% and still seems like a steep decline – but it is possible. With $9.33 trailing twelve months earnings per share this would result in a P/E ratio of 10 (assuming EPS does not decline for Microsoft) and that is certainly possible. And during the Dotcom bubble and again in 2011, Microsoft has been trading for such a valuation multiple.

A third support level would be around $140. At this level, we have the COVID-19 lows set in March 2020. Additionally, we have the 38.2% Fibonacci retracement at $142.50. And we also have an increasing trendline, which has been in place since 2009 (white trendline). We would hit the trendline at the end of 2023 or beginning of 2024 (at that price level).

And although Microsoft might be fairly valued at this point, I still think we are facing downside risk. Most likely, growth rates will slow down in the coming quarters, and I think we will see lower valuation multiples for Microsoft. I actually see Microsoft declining to about $140 being the most realistic case. With earnings contracting, this would lead to a reasonable P/E ratio between 15 and 20.

Conclusion

I still would be cautious about Microsoft. On the one hand, it seems fairly valued right now as 8% growth for the next ten years seems like an achievable target. But we must assume that Microsoft growth rates might slow down in the quarters to come, which would also lead to lower valuation multiples. Without much doubt, Microsoft is a great business with a wide economic moat, but we saw in the past (or for some companies already in 2022) what can happen to great businesses once investor expectations are not fulfilled.

For further details see:

Microsoft: Buying Opportunity In The Making