TSLA - Microsoft Is A Cash Cow Blue Chip: Here's When To Snap Up Shares

Summary

- Of the largest 10 stocks in the S&P 500, there are only three that I think have valuations in the ballpark of being reasonable.

- These three stocks are Microsoft, Google, and Berkshire Hathaway.

- We dive into Microsoft, which is near where I would buy it, but not yet there.

- Why Microsoft's business is such a juggernaut, and where I think you should snap up some stock in light of a tighter Fed and falling market valuations.

Redmond, Washington,-based Microsoft ( MSFT ) is the second largest company by market cap in America, second only to Apple ( AAPL ). Microsoft has shown a unique ability to reinvent itself nearly three decades after its ubiquitous Windows software first started making the company billions of dollars in annual profits . If you're a long-time Microsoft holder, you've made a bunch of money.

Today, Microsoft is still a great business.

- Millions of people use Microsoft Office on a daily basis.

- The Azure cloud business continues to grow massively.

- And if MSFT's acquisition of Activision Blizzard ( ATVI ) closes, the combined company will be the third largest video game company in the world. Interestingly, Warren Buffett bet billions of dollars this year that the deal will close.

To these points, investing would be super easy if all you had to do was pick the most profitable companies and invest in them. This isn't completely wrong per se, because historically the infamous "disposition effect" keeps the stocks of great companies cheaper than they should rationally be. However, since I started writing for Seeking Alpha in 2018, stock valuations have essentially done nothing but go up, forcing investors to pay more and more for each dollar of future earnings. When I started writing here, I could often write articles with titles like " Back up the truck ," and " 25% downside + 100% upside ." Now all the low-hanging fruit has been picked, and the metaphorical nights are getting colder, with winter on the way.

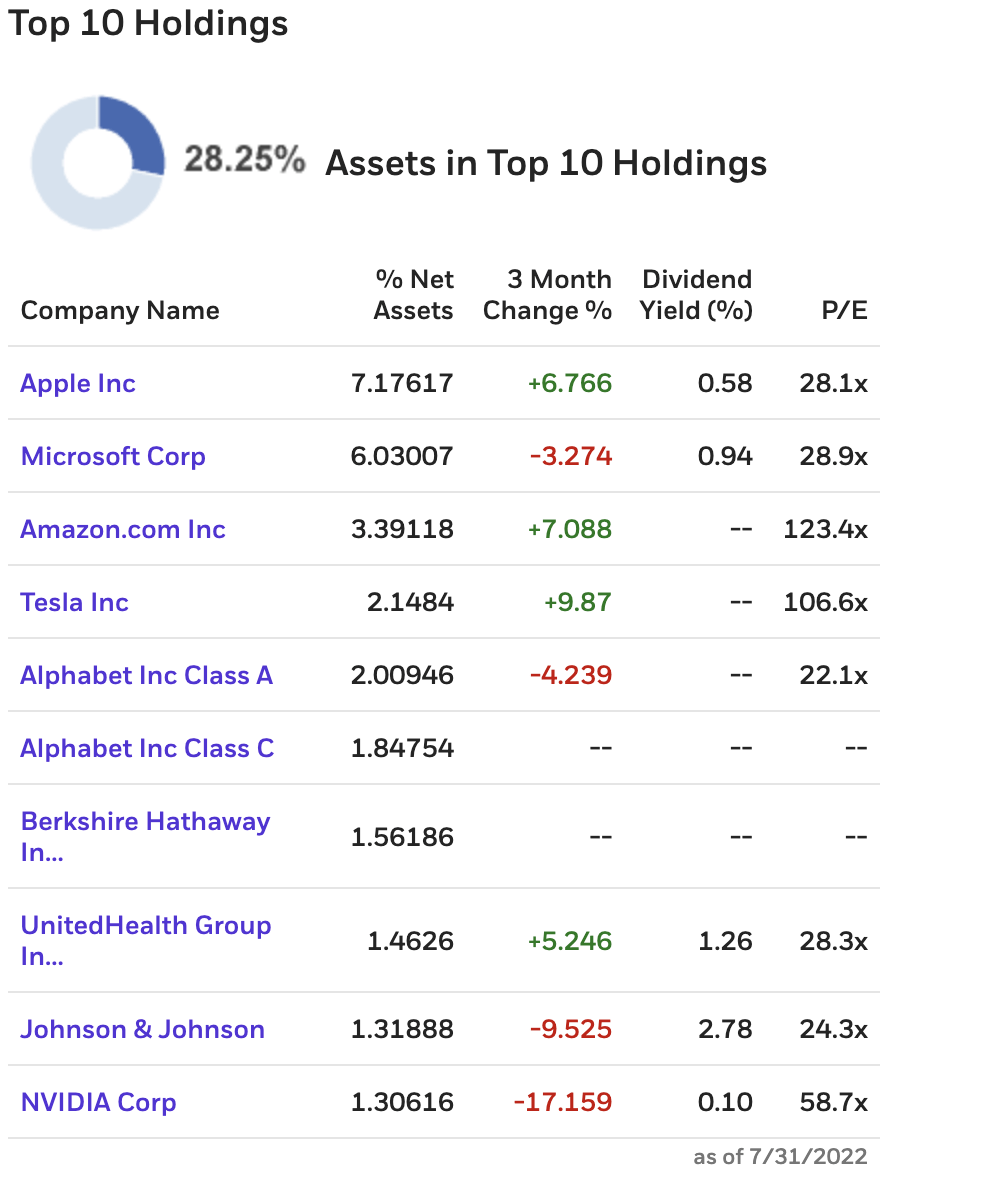

Taking a quick glance at the top 10 holdings of the S&P 500 as of July 31st ( SPY ) shows this.

{kind=link}

SPY Top 10 Holdings (Etrade)

Apple is trading for 28x 2021 earnings, and analysts are projecting single-digit growth going forward. 2021 earnings were themselves pumped up by thousands of dollars in stimulus checks per household, bringing into question the company's ability to even sustain what it made in 2021. Amazon ( AMZN ) and Tesla ( TSLA ) both trade over 100x earnings, which is historically perilous to expect for companies of their size. UnitedHealth ( UNH ) and Johnson & Johnson ( JNJ ) both trade for fairly high multiples as well, and are prime targets for any future healthcare reform, at the very least threatening their ability to grow earnings. And Nvidia ( NVDA ) is down big this year but still trades for nearly 60x earnings. NVDA has been compared with good reason to Cisco ( CSCO ) in 2000.

That leaves Microsoft, Google ( GOOG ) (GOOGL), and Berkshire Hathaway (BRK.A) ( BRK.B ) MSFT has a 29x multiple on 2021 earnings but much better forward growth prospects than Apple according to analysts. Similarly, Google's multiple is pretty reasonable given its long-term growth prospects, and a substantial portion of Berkshire's value is in Apple stock, but BRK.B trades at a beautiful discount to Apple. These are the stocks that you should look to pick up in a downturn. I'm comparing these stocks with 2021 earnings because I pulled them in bulk, for MSFT I'll compare with 2023 earnings below. I'd be cautious about extrapolating 2021 earnings with some stocks but MSFT's earnings are stickier than most tech or consumer discretionary companies.

Meanwhile, Back At The Farm

Here's how Microsoft's business has been performing.

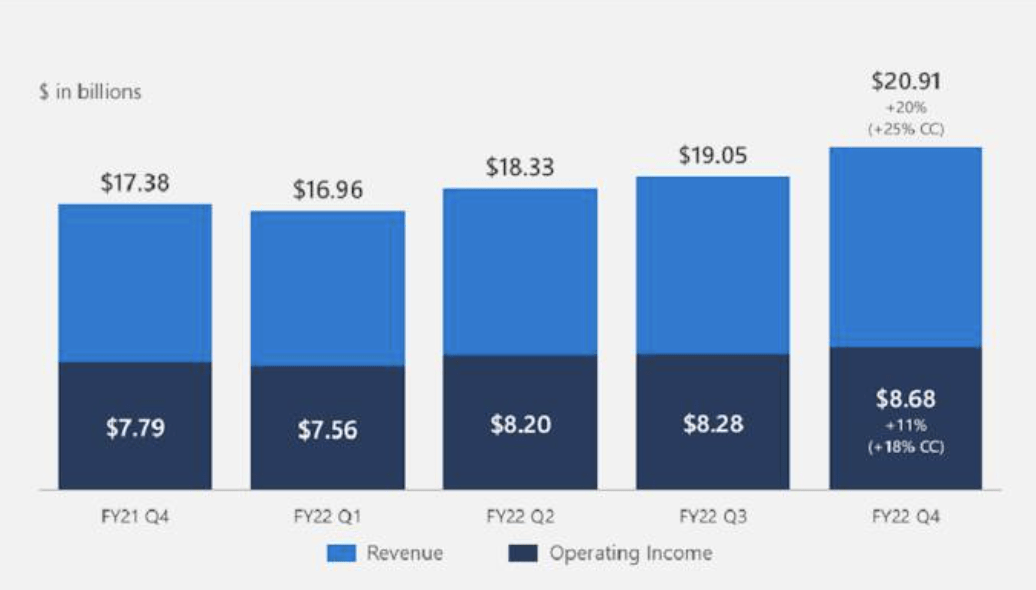

Cloud

Amazon has similar exposure to the cloud through AWS, but Microsoft is out-competing them and taking market share . In one of the fastest growing markets in tech, Microsoft is again showing an impressive ability to make inroads against an entrenched market leader with massive resources. Going forward, I would expect this trend to continue as Amazon is forced to grapple with the reality of running a global logistics business with 1.6 million employees and trying to defend AWS's market share– a two-front war. It's not necessarily zero-sum since the cloud market is rapidly growing, but the rest of Microsoft's business is so much more attractive than Amazon's to me and MSFT carries less downside risk and valuation risk as well. Despite a stronger dollar, Microsoft grew cloud revenue by roughly 20% over the last year . This was discussed in MSFT's most recent quarterly earnings conference call .

Cloud Revenue and Profit (Billions)

{kind=link}

Office/Productivity

Microsoft Office has followed the tech industry's grand plan of switching from mainly selling products to mainly selling subscriptions. It's been a good plan – going from a one-time sale model to a subscription model has improved Microsoft's revenue from Office dramatically. MSFT has seen good growth in this segment as well (note that they include their LinkedIn acquisition in this category as well). As with cloud computing, industry observers have called for huge growth in this market over the next 10 years as the workforce continues to become more decentralized after the initial shock of the pandemic. One area that's expected to see big growth is so-called " enterprise content management ," which is the management of documents, spreadsheets, contracts, and scanned images. Box ( BOX ) is one of the big players in this space now – I wouldn't be surprised to see Microsoft either make them a buyout offer or clone them the way they've done, taking on Zoom ( ZM ) with Microsoft Teams.

MSFT Productivity & Business Processes Revenue

{kind=link}

Microsoft Productivity Revenue (FY 2022 Investor Presentation)

Gaming

Microsoft buries its gaming revenue with the legacy business from Windows and other catch-alls, but they're now making a huge push in gaming. This line of business has been more or less stagnant, but the push is intended to get the ball rolling, tying Microsoft in even deeper with the global video game market, which is expected to grow 12% or so annually over the next five years. Specifically, Microsoft is acquiring Activision Blizzard, the controversial but profitable video game company best-known for the game Call of Duty. Of course, MSFT already owns Xbox, so this is vertical integration at its finest. If you own the console, the operating system, and you own the video game company all in one, then you don't have to split the profit with anyone.

{kind=link}

The offer is for $95 per share, but ATVI trades for a bit less than $79 as of my writing this. Warren Buffett, one of the world's foremost merger arbitrageurs has bought billions in ATVI stock – he'll pocket $95 per share if the deal is successful. The deal is expected to close by June of 2023 but requires antitrust approval in several countries . Merger arbitrage is not a new thing – it was outlined as a strategy by Benjamin Graham in his books. I believe the strategy is underused by investors. Buffett has used the merger arbs extensively over the last six decades, including heavily in the 1980s .

If there's one trade here I would make, it would probably be to tail Buffett's judgment on ATVI. The stock price hasn't changed much since the announcement, so you're getting more or less the same deal as Buffett here.

MSFT Valuation and Target Price

The overall market's valuation is too high. First, earnings aren't sustainable without massive stimulus juicing the economy, and second, price-to-earnings multiples are too high compared with what you can get in cash as the Fed jacks up rates to fight inflation. I covered this extensively this week in my first and second pieces on Jackson Hole and encourage readers to review my thoughts on the macro picture.

Market-wide , stock prices have risen faster than business profits over the past few years, and Microsoft is unfortunately not an exception to this trend. However, Microsoft's valuation is better than its large S&P 500 peers, and of course, Microsoft's business is better run as well. This doesn't necessarily mean you should pay 30x earnings for it because it will drag down your future annual returns, but at worst, Microsoft is on the high side of a range where you might consider the stock fairly valued.

I believe the broad stock market is overvalued by a bit less than 20% at current prices as the post-pandemic economic hangover slowly resolves. Microsoft has an excellent underlying business, but I expect the Fed and the economy to drive the stock over the next 6-12 months. Ballparking off of FY 2023 earnings estimates for MSFT of roughly $10.25 per share, and applying a 20-21x multiple, you get a target price for buying MSFT at around $205 to $215. That's around 20% lower than the current price. That's where I'd buy it. But if you're OK with a 25x multiple, then MSFT is a buy at $255 or so, or only about 3% lower than the current price. If you buy now, you might get 9% annual returns, but if you can score the stock for $210, you're looking at more like 15% annually.

In any case, compared with some other popular stocks trading at 50-100x earnings that could fall 50% and not even become cheap, MSFT has a much better risk/reward. This is fairly typical for blue chip stocks, which are often good businesses trading for premium valuations, so you have to stalk them for a good chance to buy. Historically, growth stocks trade at a large valuation premium in bull markets but trade closer to the market median in bear markets, giving justification to this approach. Since so much MSFT is held by ETF investors, the macro environment is going to dictate the valuation in the short run.

Bottom Line

Microsoft is a great business, but the stock is connected to the broader market which is fighting the Fed's efforts to drain excess liquidity out of the system. If you buy MSFT now, I think you're getting decent long-term compensation but likely to face some declines in the near term. For this reason, I'd rate MSFT a hold and look to pick up MSFT stock about 20% lower than the current price. For a Buffett-approved trade you can do right now, look at buying ATVI and waiting for the deal to close.

For further details see:

Microsoft Is A Cash Cow Blue Chip: Here's When To Snap Up Shares