CA - Midstream Income For Life

2023-09-06 07:00:00 ET

Summary

- The article discusses the simplicity and carefree nature of a one-year-old's life compared to the complexities of adulthood.

- The rising costs of life, particularly in the energy sector, are highlighted as a challenge for individuals.

- Three energy companies are recommended - Enterprise Products Partners, Energy Transfer, and Enbridge - as potential investments for dual profit potential and reliable dividends.

This article was coproduced with Leo Nelissen.

Sometimes I really think about how simple my one-year-old grandson’s life is.

Asher doesn’t read the news. Or pay the bills. Or even know what the news or bills are.

What a happy state of existence!

Then again, he also has people dictating what he eats, when he eats, how he eats, and where he eats. As well as why he eats what he eats when, how, and where.

The same goes for naptimes, bedtimes, playtimes, the toys he has, what he wears… Pretty much his whole entire world is determined by outside forces. Which, I’m sure, can get frustrating.

I’ve seen the proof since, like most babies (and, let’s face it, most adults too), Asher isn’t always fond of being told “no.” Then again, considering the news and bills due these days…

Maybe the tradeoff is worth it?

Life is expensive. And involved. And as we keep seeing through the economic headlines (and in person), it’s getting more expensive and involved still. Sure, the inflation rate is down, but inflation itself is not.

It’s just headed higher more slowly than before. So any additional money we can bring in is important to talk about.

That’s why I’ve been writing this “Income for Life” series. First, I published “ REIT Income for Life .” Then it was “ BDC income for Life .”

And now we’re onto a third installment, this one focused on energy.

Get Your Fair Share of These Electrifying Energy Profits

Energy, of course, is part of the reason why life is so expensive right now.

It’s not the entire reason, mind you. I’m well aware of that and not trying to start any fights about what else is and isn’t involved in our pocket pains.

But I think we can all agree that the fuel situation isn’t helping. As the cost of transportation goes higher – whether by plane, ship, truck, or whatever – the price tags of everything else tend to follow. This only makes sense for anything that needs to be transported, from raw goods to finished products at the end of the manufacturing line.

There’s no escaping it. Whether you’re shopping for a house, new furniture and appliances, food, or whatever you buy from Amazon, costs are up.

So why not profit from those expenditures if possible? Which, as “Energy Income for Life” is about to show you, it is.

I’m not talking about buying and selling oil directly, mind you. Commodities trading is complex and volatile. It’s not a headache I care to have. And I wouldn’t wish it on anyone else who doesn’t have the time, money, knowledge, and wisdom it takes to make it work.

I believe in investing in companies that do have all that going for them instead. Let them deal with all the industry ins and outs.

I just want to kick back, relax, and take a cut of the profits. Or, perhaps I should put it this way considering how much else there is to deal with these days…

I don’t want another set of responsibilities on my shoulders if I don’t have to. Which, in this case, I don’t.

Neither do you.

Plentiful Portfolios and Dividends-a-Plenty

That’s one small part of why energy fits so perfectly into my “Income for Life” series. The companies that deal with and in it perform a certain way, offering essential services wrapped up in neat little boxes tied with bows.

Take real estate investment trusts, or REITs. They own entire portfolios of properties, where they’re in charge of finding tenants, maintaining tenants, and collecting rent from those tenants.

REIT investors don’t have to worry about any of that hassle. (And take it from a former landlord… it can be a major hassle.)

Business development companies, or BDCs, meanwhile, are financial institutions that lend money to the otherwise “unlendable.” Businesses that can’t easily find fiscal backing– whether because they’re small, struggling, or in a problematic industry – can very often turn to a BDC for help.

The BDC researches them, determines the most viable terms to work with them, and monitors the borrower and borrowings from there. Then they summarize all of that for their investors to read over while sipping on a cup of coffee or tea.

Maybe even a cocktail on some sandy beach.

Energy companies do the same, just with portfolios of… well… energy.

You could argue that description fits a larger array of stocks than I’ve mentioned above, I know. So here’s the real reason to keep reading: Dual profit potential.

REITs and BDCs reward their shareholders:

- By guiding their companies into growth and stock-price appreciation

- With safe, reliable, income-inflating dividends.

And so do the energy companies I’m about to dive into. Today, I’ve got three particular picks to recommend.

Two of them are dividend aristocrats with plenty of growth potential!

Before we continue, bear in mind that MLPs do not technically pay dividends. They are called distributions . Also, shares are called units . For everyone’s convenience, I’ll go with dividends and shares in this article, as not all picks are MLPs, so please do not be confused.

Enterprise Products Partners L.P. ( EPD ) - 7.5% Yield

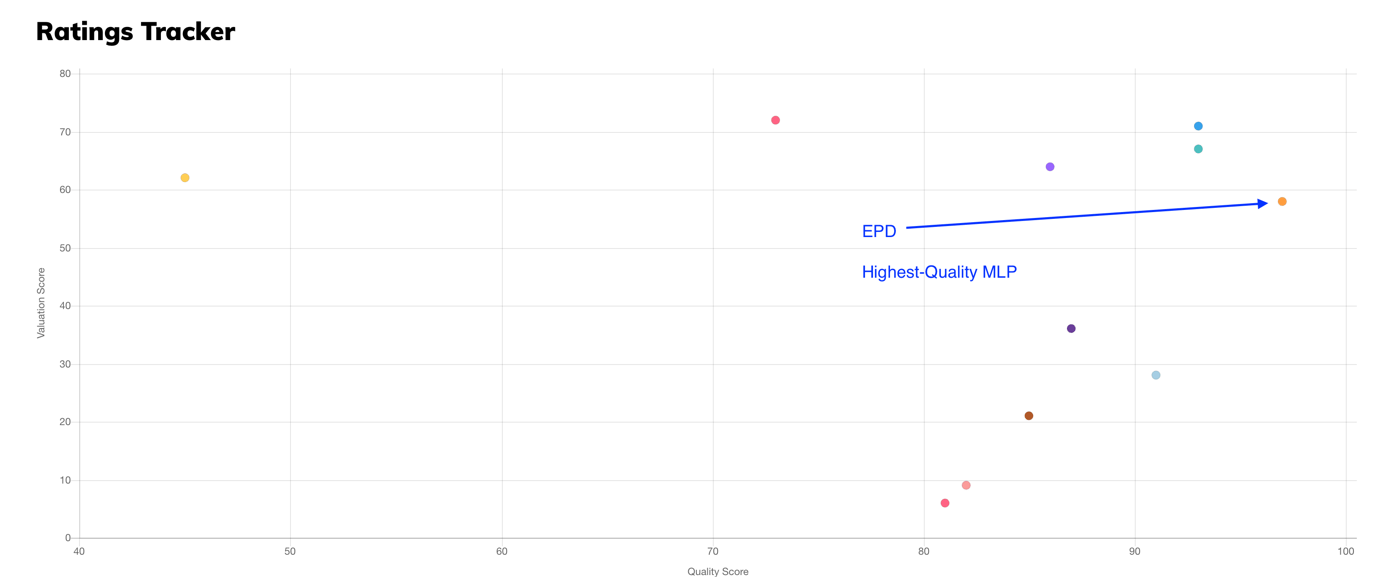

I start this article with the gold standard of midstream companies. The company isn’t just one of the oldest and best-managed master limited partnerships, or MLPs, but it also enjoys our highest quality ratings among midstream companies.

{kind=link}

As the sub-title already shows, that company is Enterprise Products Partners.

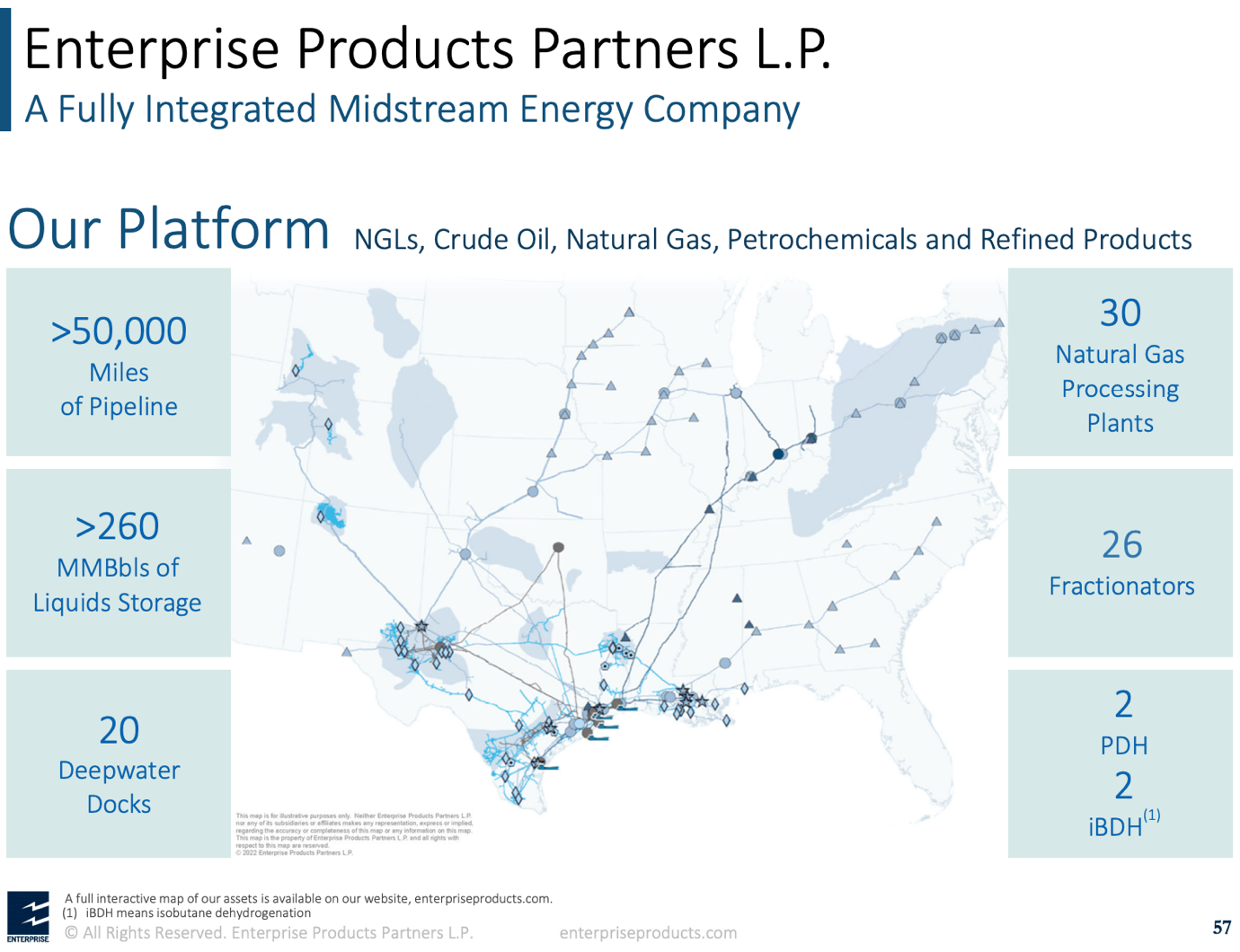

Founded in 1968, Enterprise Products Partners has become one of the most important companies in the North American energy grid, as it now manages more than 50,000 miles of pipeline, storage capable of holding more than 260 million barrels of liquids, 30 natural gas processing plants, 25 fractionators to produce value-added products, and 20 deep-water docks to service overseas energy demand.

{kind=link}

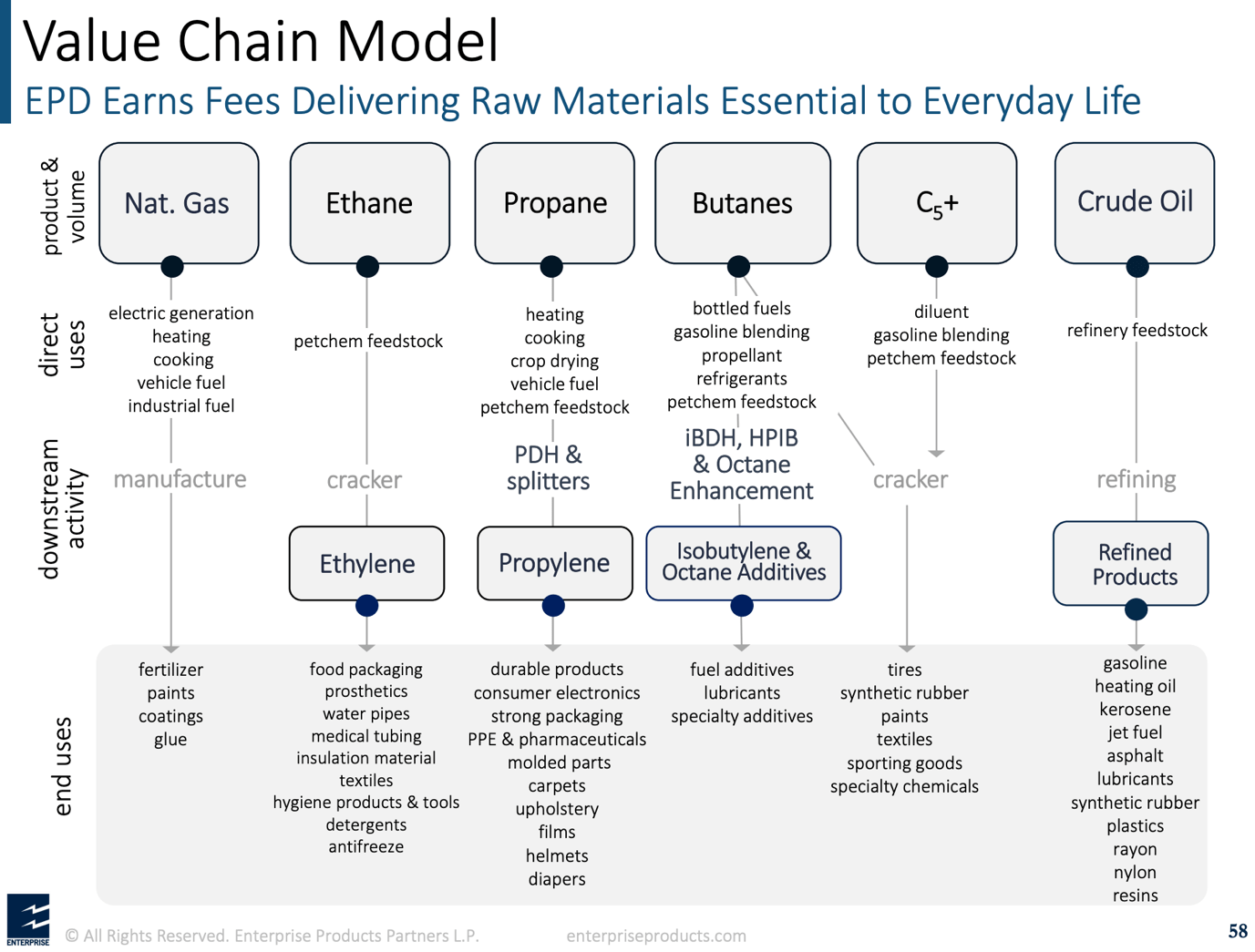

Last year, the company made roughly 42% of its money in the Natural Gas Liquids Pipelines & Services segment. 32% of its sales came from the Crude Oil Pipelines & Services segment. The remaining dollars came from Petrochemical & Refined Products Services and Natural Gas Pipelines & Services.

Essentially, this giant combines all important feedstocks to buyers that turn these into products we use every day. This includes fertilizers, food packages, water pipes, medical supplies, helmets, diapers, lubricants, tires, paints, and obviously gasoline and diesel.

{kind=link}

In addition to this, the company helps companies expand production in critical areas like the mighty Permian basin, the only basin capable of keeping American shale production in an uptrend.

In 2023/2024, the company is bringing four new gas plants online, scheduled to increase processing by 1.2 billion cubic feet per day.

On top of that, the company helps America to increasingly export its fossil fuels. This isn’t just a benefit in light of rapid middle-class growth in emerging markets but also a necessity in light of the Ukraine war, where fossil fuels are used as leverage.

Right now, Europe barely receives any natural gas from Russia, putting tremendous pressure on the U.S. to keep the lights in Europe from going out.

One of the reasons – if not THE reason – why EPD is such a high-quality stock is its consistent financial performance. Like its peers, the company is spending billions on new infrastructure. However, the company is older and had a large (profitable) network in place when others were still in the early phases of expansion.

A lot of MLPs cut their dividends in 2015 when high investment requirements met imploding commodity prices and lower demand.

EPD did not cut its dividend.

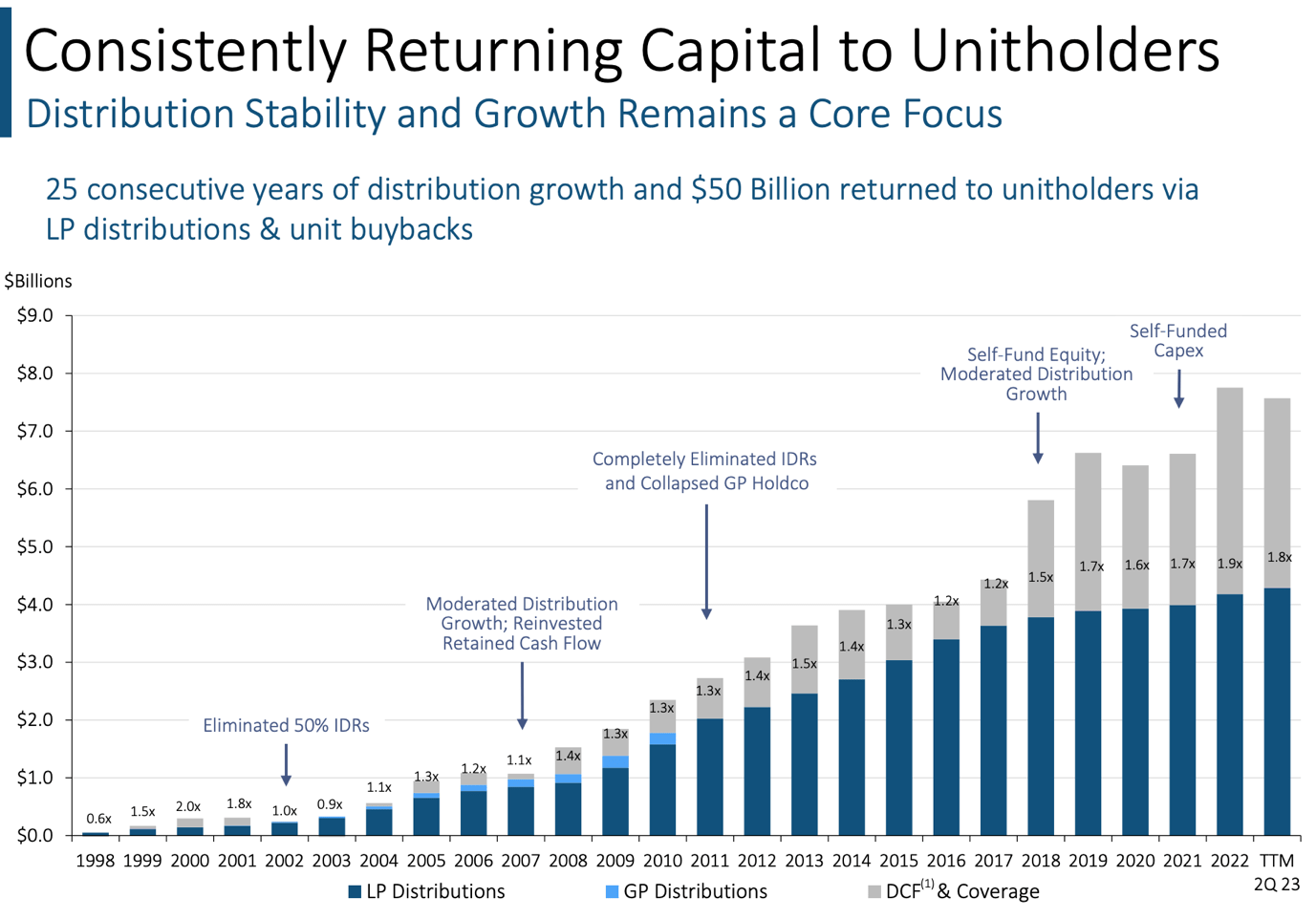

Even better! EPD is a dividend aristocrat with 25 consecutive years of dividend hikes.

Since 1999, the company has covered its dividend every single year, using its consistently rising distributable cash flow.

{kind=link}

This dividend isn’t just backed by consistently rising distributable cash flow but also a healthy balance sheet.

The company enjoys an A- credit rating with an average weighted cost of debt of just 4.6%. It has no debt maturities in 2023.

Next year, the company is expected to generate $5.8 billion in free cash flow, which implies a 10% free cash flow yield. This covers the 7.5% dividend and investments in growth/maintenance with a wide margin of error.

Author, Based on analyst estimates

With regard to growth, the dividend has a 5-year CAGR of 2.8%, which beats the Fed’s inflation target.

While it needs to be seen what the company is up to, it is not unlikely that dividend growth will accelerate a bit in the next few years.

The current market capitalization of the company, along with its expected net debt and potential EBITDA, puts its estimated EBITDA for 2024 at 8.9x.

This also includes the minority interest income streams the company doesn't fully own, which are valued at roughly $1.0 billion.

Despite this, the valuation is still attractive when compared to the company's usual trading range of close to 10x EBITDA.

Based on this, the company's fair value is estimated to be 18% above its current unit price.

iREIT has a Buy rating on the stock.

Energy Transfer LP ( ET ) - 9.1% Yield

Energy Transfer is a comeback stock.

During the pandemic, the company cut its dividend. Now, it’s back with a very bright future ahead!

Seeking Alpha

With a market cap exceeding $42 billion, this giant is going back into the M&A game.

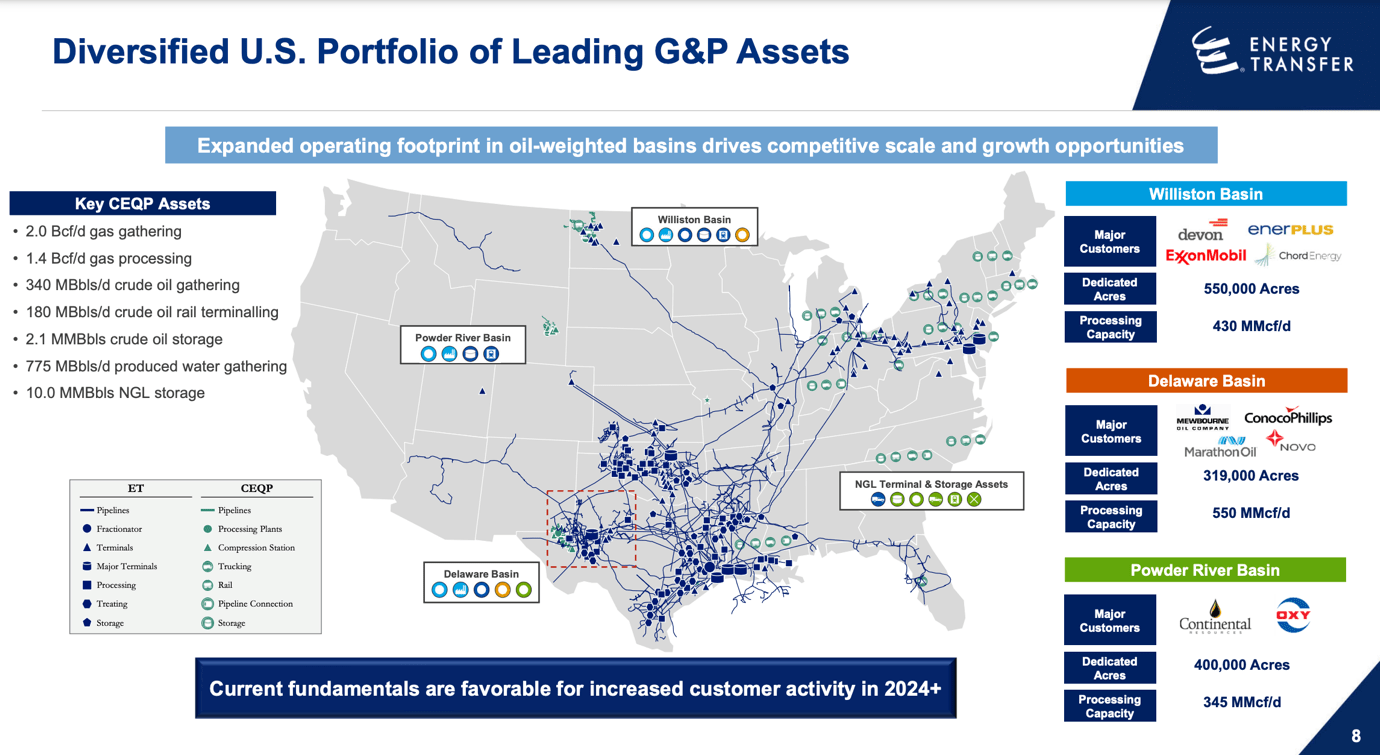

Last month, it made an offer to buy Crestwood ( CEQP ) in a $7.1 billion deal (including debt), which would make it one of the best-diversified midstream giants.

ET would expand its footprint in oil-weighted basins and increase its exposure to some of the Nation’s largest upstream companies. The deal is subject to regulatory and shareholder approval. The deal might close in the fourth quarter.

{kind=link}

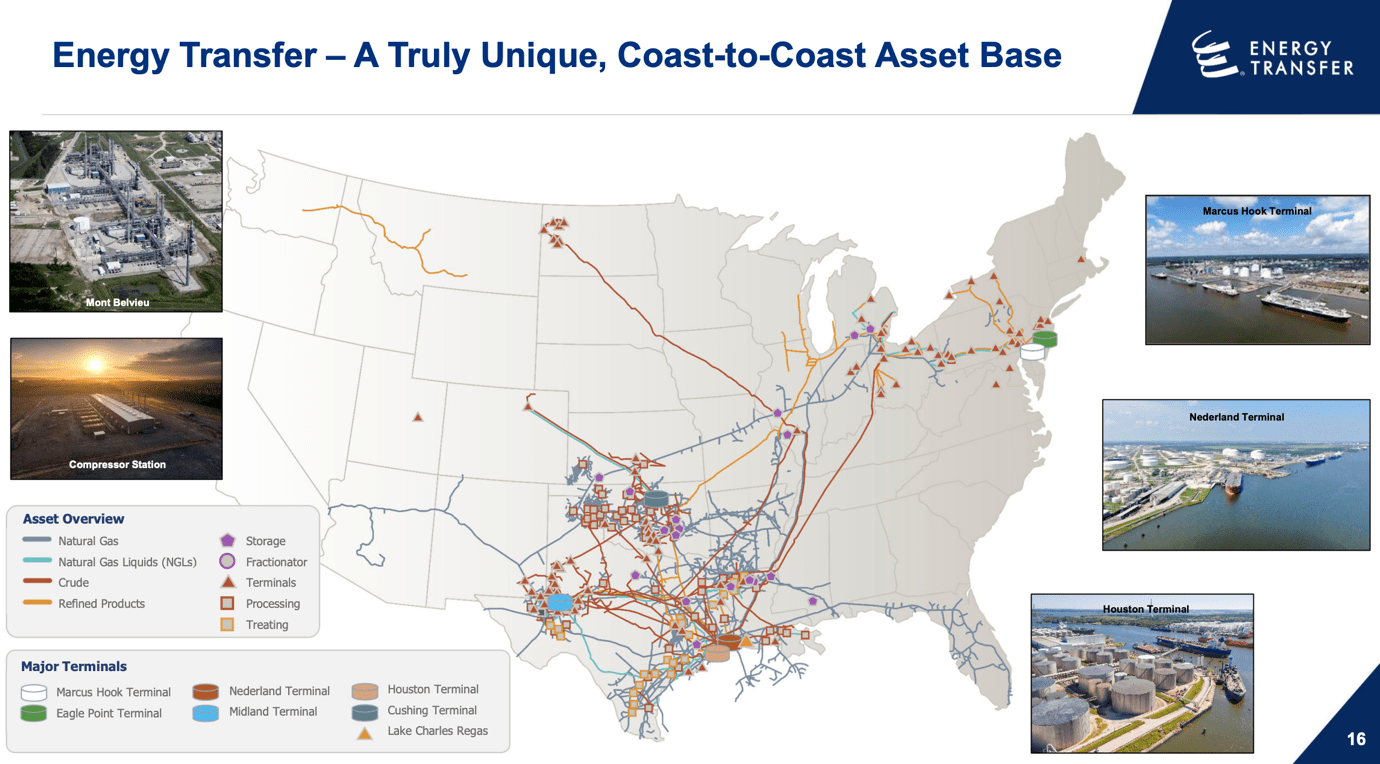

Even without these assets, ET is one of the largest midstream companies in North America, servicing all major basins in the South, the Powder River basin, and the Williston basin.

{kind=link}

The company owns 34% of Sunoco LP ( SUN ), which distributes motor fuels to independent dealers and operates 76 retail stores in Hawaii and New Jersey.

While its market cap is a pretty good indicator of its size, there are a few impressive numbers I want to share with you. For example, the company gathers roughly 20 million MMBtu of gas per day and transports more than 4 million barrels of crude oil per day. It is capable of exporting roughly a quarter of that in its own facilities.

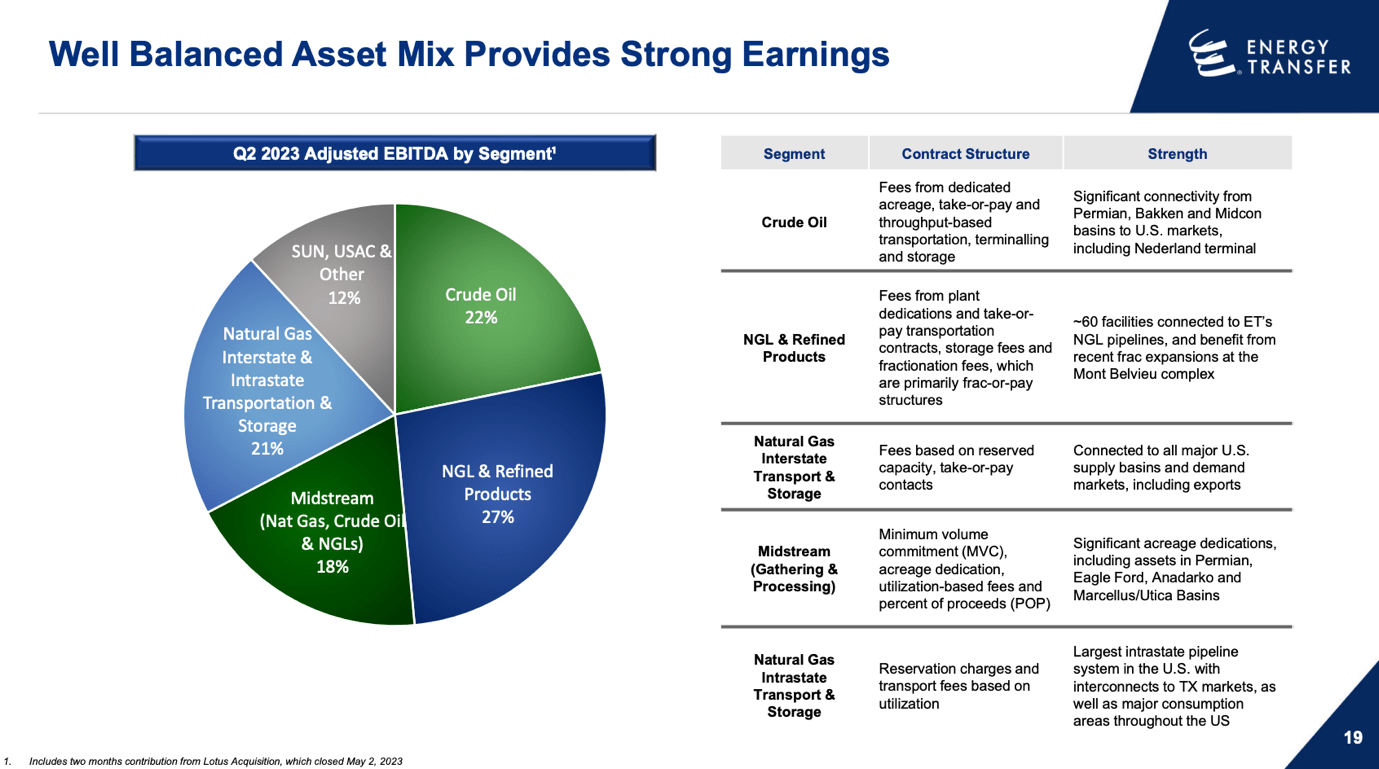

90% of its EBITDA is dependent on fees, which means that commodity price fluctuations aren’t a major issue – at least not compared to companies that actually produce oil and gas.

{kind=link}

Energy Transfer is also a stock that shows a lot of conviction from its management. Not only does it have one of the highest insider ownership rates in the country (>12%), but it is also mainly owned by retail investors, who own roughly 50% of all units.

Thanks to its mature business and strong tailwinds consisting of rising global demand for natural gas, oil, and refined products, the company is in a good spot to protect and grow its dividend while focusing on growth opportunities.

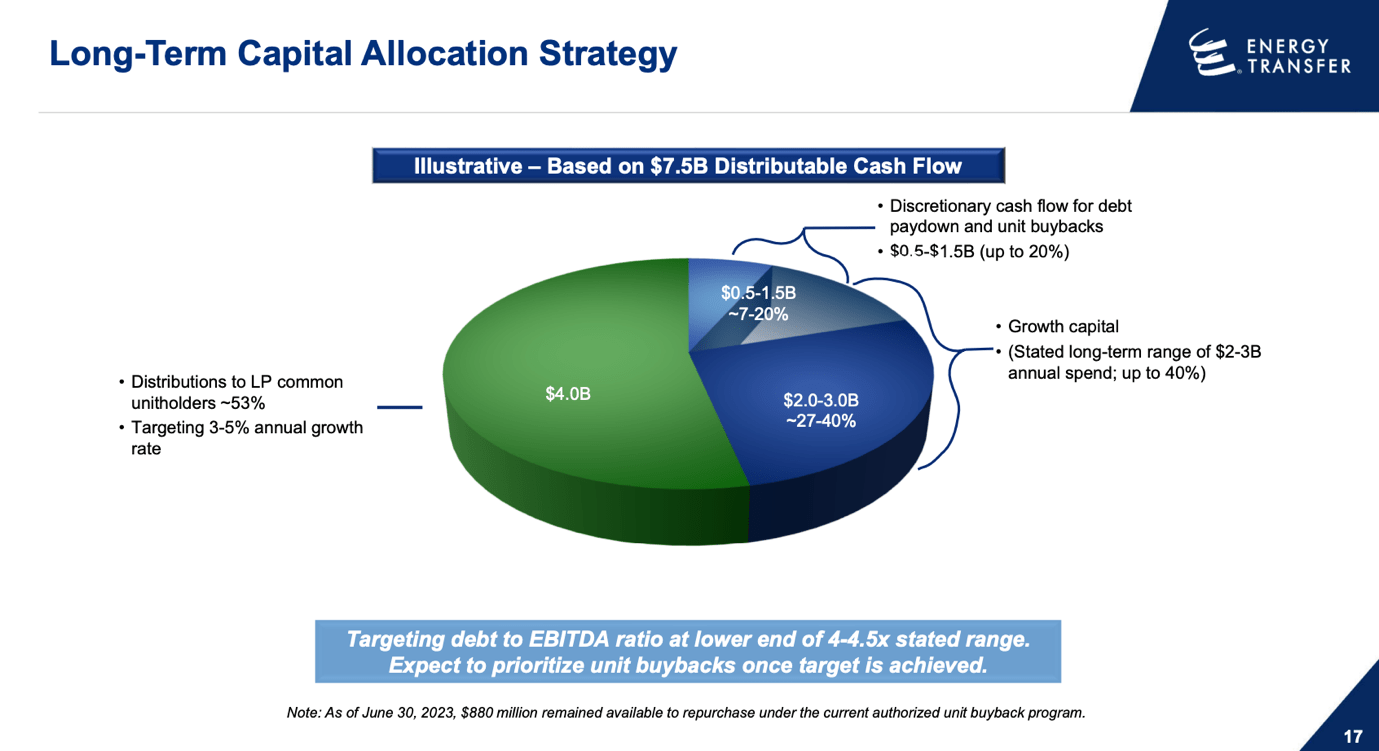

The company’s long-term capital allocation strategy aims to distribute more than half of its distributable cash flow to shareholders. Roughly a quarter of its discounted cash, or DCF, will be used to grow the business. 7% to 20% will be used to reduce debt and buy back units/shares.

{kind=link}

Thanks to its focus on debt reduction, the company has a much healthier balance sheet.

It is expected that the net debt at the end of this year will be $50.3 billion, which is likely to decrease gradually to $46 billion by 2025. Taking into account the gradual increase in EBITDA, the estimated net leverage ratio for 2025 is 3.4x EBITDA.

The company's current credit rating is BBB-, which is one level below the company's target rating of BBB. With a positive outlook from Fitch, a rating upgrade may be imminent.

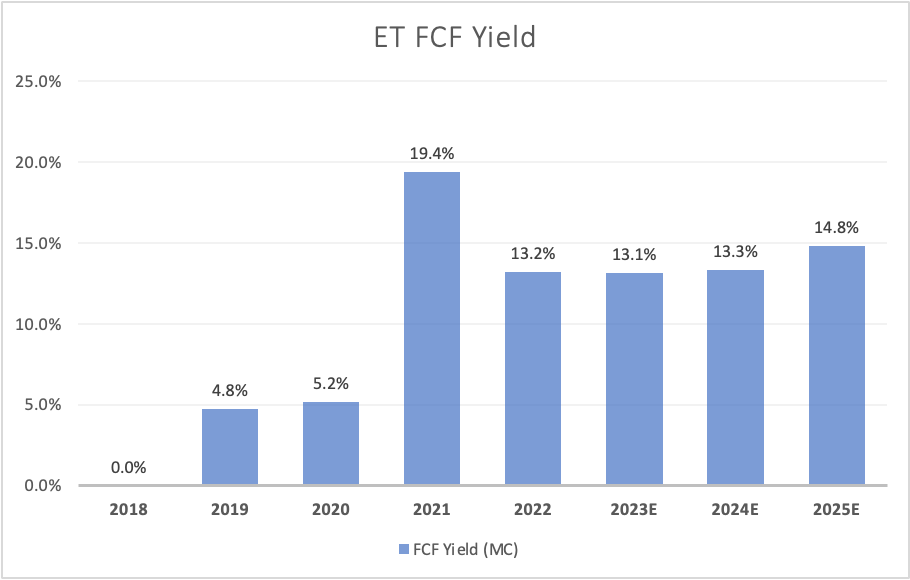

With regard to its dividend, the company has a juicy 9.1% yield, which comes with strong free cash flow protection. The company is expected to maintain a 13% free cash flow yield before a surge to 15% in 2025. Please note that free cash flow takes growth and maintenance capital spending into account.

{kind=link}

In other words, the dividend is safe, not only because of a healthy balance sheet but also because the company is finally producing consistent free cash flow.

This also helps the company’s valuation. After all, a 9.1% yield is a huge deal! It’s the highest yield we discuss in this article.

The company is trading at just 7.4x NTM EBITDA, which is below any of its peers. While ET has a history of cutting its dividend, it is now a much stronger player, which warrants a higher valuation.

Seeking Alpha

The current consensus analyst price target is $17. This is 25% above the current price.

Given the bigger picture, that’s more than fair!

Enbridge Inc. ( ENB ) - 7.3% Yield

The third midstream company is no MLP. Enbridge is a Canada-based C-Corp, which means it does not issue a K-1 form.

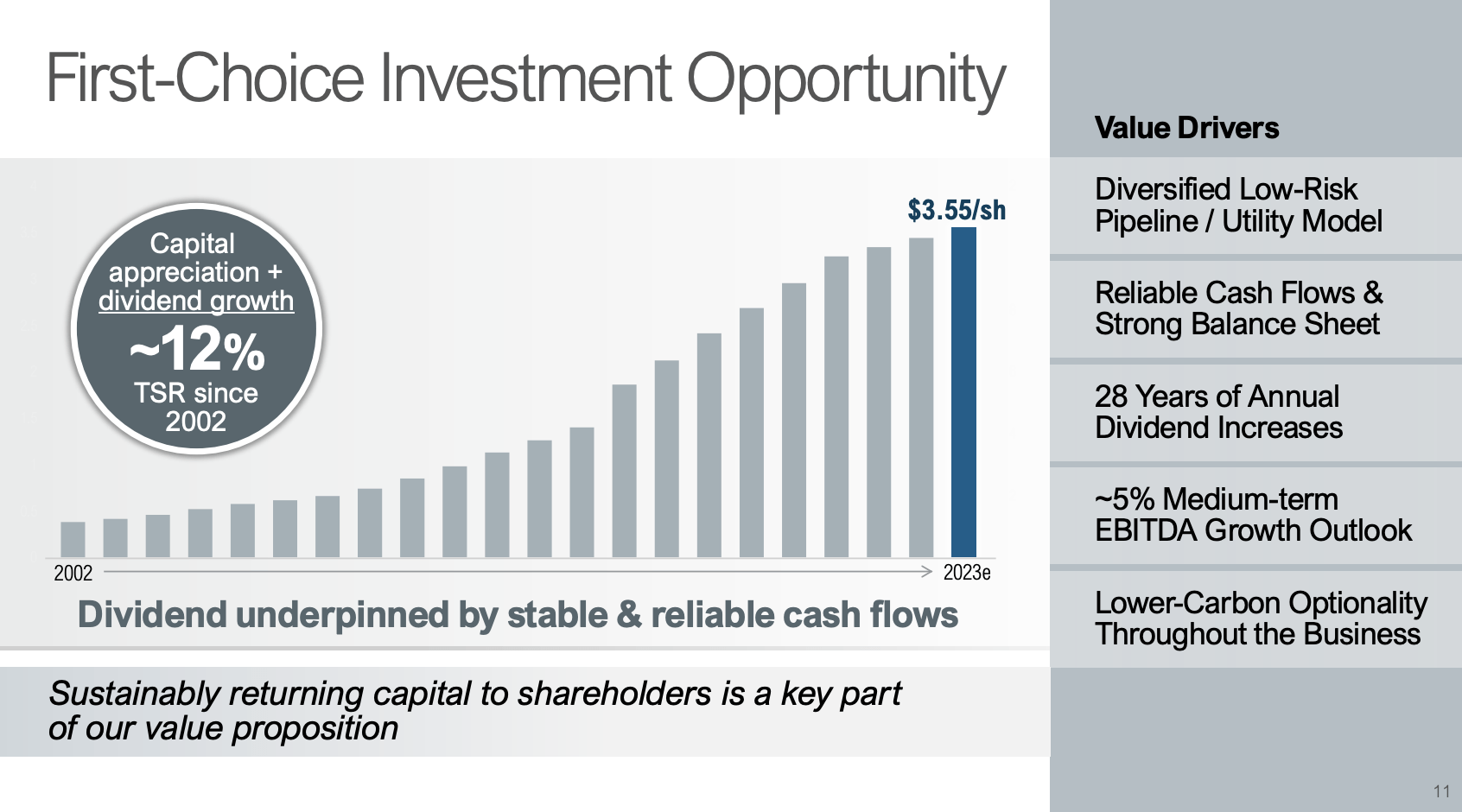

Like its American peer, Energy Products Partners, it’s one of the most reliable dividend payers in the industry. The company has a track record of 28 consecutive annual dividend increases. Since 2002, the dividend has been hiked by 12% per year.

{kind=link}

However, in this case, investors need to be aware that Enbridge pays its dividends in Canadian dollars, which means dividend growth for foreign investors is dependent on the Canadian dollar.

The company currently pays CAD 0.8875 per share per quarter, which translates to a yield of 7.3%.

Taking a step back, Enbridge is a giant. With a market cap of $72 billion, the company is a giant in its industry, connecting energy producers to customers in North America and Europe.

Headquartered in Calgary, the company operates the world’s longest and most complex crude oil and liquids transportation system, with more than 17,800 miles of active pipelines in North America.

Every day, the company delivers more than 3 million barrels of crude oil and liquids via its Mainline and Express networks.

The company transports roughly 30% of total North American crude oil production, 65% of U.S.-bound Canadian exports, and 40% of total U.S. crude oil imports!

{kind=link}

Not only does this company have a massive moat, but it also has a well-covered dividend.

This year, the company is expected to generate $8.9 billion in free cash flow, which results in a 9.1% free cash flow yield, indicating an 80% cash payout ratio that supports the safety of the dividend.

On top of that, the company has a BBB+ credit rating and a highly favorable business model.

For example, 98% of the company's anticipated 2023 EBITDA comes from regulated assets or long-term take-or-pay contracts.

Approximately 51% of these assets fall under the take-or-pay plus category. These assets are backed by extended agreements with inflation protection and cost-sharing provisions.

Enbridge

Roughly 47% of the EBITDA is characterized by low risk, resembling utility-like stability with minimal volatility.

The company also enjoys one of the strongest customer bases. 95% of its customers have an investment-grade rating, meaning it is unlikely to suffer from bankrupt customers in the event of severe economic weakness.

While this goes for many of its peers, ENB is at the very top when it comes to benefiting from strong customers.

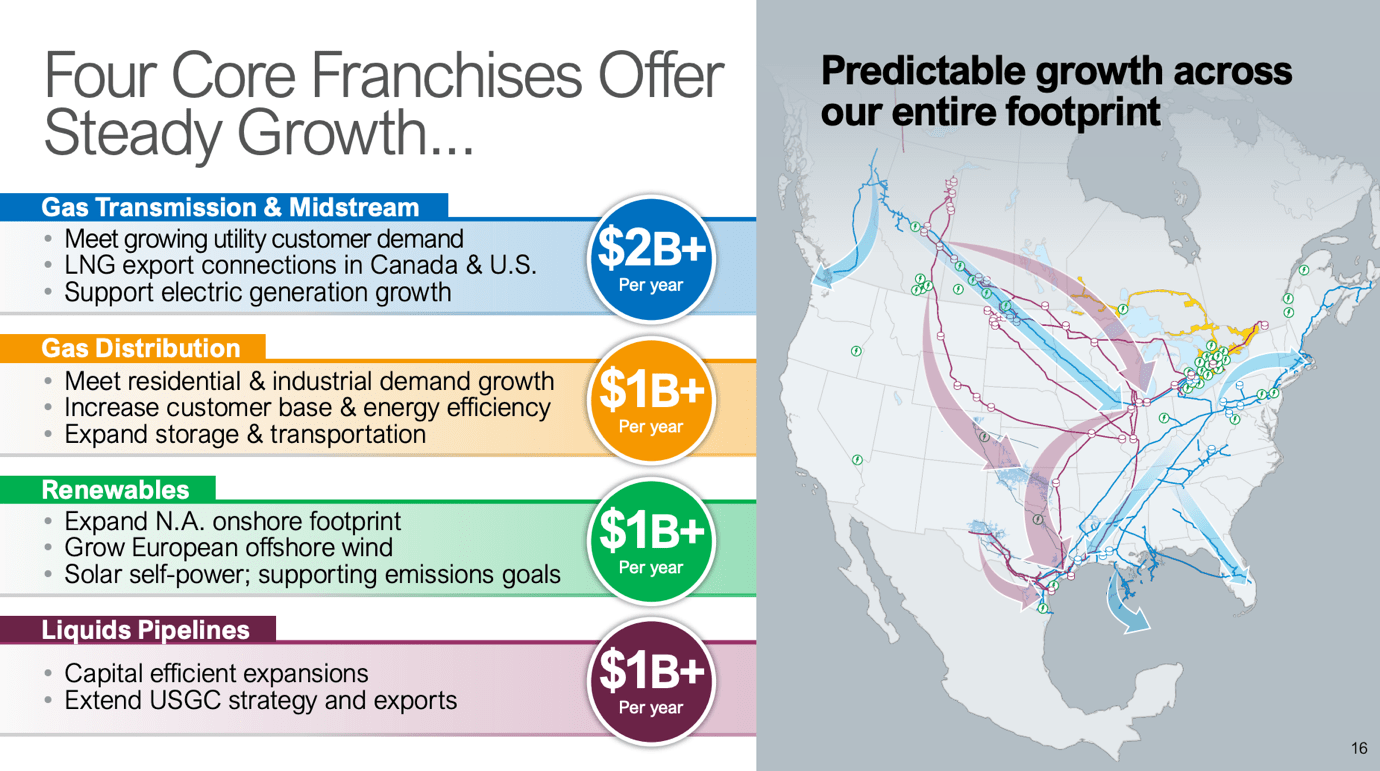

Enbridge is also growing through strategic investments. For example, the company aims to boost its market share in the Gulf Coast’s LNG exports. It targets a market share increase from 15% to 30% by 2030, making Enbridge one of the most important players in America’s plans to become a go-to-market for liquid natural gas.

Enbridge

These growth programs are expected to provide the company with roughly 5% average annual compounding EBITDA growth in the 2022-2025 period, boosted by toll escalators (higher prices for pipeline usage), organic expansions, and growth projects.

Enbridge

Bear in mind that the company is growing without risking the safety of its dividend, as the aforementioned free cash flow numbers account for maintenance and growth CapEx.

Having said that, ENB isn’t having a good year. The stock is down 9% in New York. Shares have lost a quarter of their value since the 2022 peak.

Shares are now trading at 11.6x forward EBITDA. As the valuation chart we discussed in the Energy Transfer part of this article showed, it’s one of the most expensive valuations. However, the company usually trades close to 16x EBITDA, which reflects its stronger financials and growth potential.

Seeking Alpha

Analysts currently give the stock a consensus price target of $43, which is 21% above the current price.

This is fair. On a longer-term basis, I expect higher and more consistent gains, backed by consistent dividend growth and the benefit from growth investments in new energy projects like LNG.

Takeaway

In today's world of complex financial decisions and ever-rising expenses, it's easy to feel overwhelmed. But as I explored the world of "Income for Life," focusing on energy investments, I found a way to simplify and secure my financial future.

Just like my one-year-old grandson, Asher, who lives a carefree life without worrying about bills or news, I realized that I don't need the added responsibility of managing commodities trading. Instead, I've discovered a strategy that allows me to kick back and relax while still reaping the benefits of the energy sector's growth.

Three compelling picks stand out:

- Enterprise Products Partners : This venerable company, boasting a 7.5% yield, plays a crucial role in the North American energy grid, managing pipelines, storage facilities, and more. Its consistency, dividend aristocrat status, and robust financials make it a standout choice.

- Energy Transfer : Emerging stronger from a dividend cut during the pandemic, ET offers a 9.1% yield. Its diversified assets and focus on debt reduction, coupled with solid free cash flow, make it an enticing comeback play.

- Enbridge Inc .: With a 7.3% yield, ENB is a Canadian energy giant renowned for its reliability. It excels in delivering crude oil and liquids, boasting an impressive customer base and a commitment to growth without compromising its dividend's safety.

While these picks have different strengths, they all promise dual profit potential: stock price appreciation and dependable dividends. In a world of uncertainties, these energy investments offer a sense of security and the potential for financial freedom.

For further details see:

Midstream Income For Life