SCS - MillerKnoll Still Offers Potential Despite Recent Pain

Summary

- MillerKnoll has not been treated kindly by the market as of late, with shares falling due to concerns about the future.

- Near term, the company may see some weakness, but recent financial performance has been solid and shares are cheap.

- Ultimately, this makes the firm a good prospect for value-oriented investors to consider.

The debate over how efficient the market is will likely never be settled. Personally, I believe that the market can be irrational and inefficient for some period of time. This can even be for months on end, and perhaps even longer. One company that I do believe is the victim of this inefficiency is furniture and lifestyle retailer MillerKnoll ( MLKN ). Despite management reporting sales and cash flow figures that have exceeded what the company reported only one year earlier, the stock has taken a beating over the past several months. Some of this decline may be due to the fact that analysts are expecting a bit of weakness for when the company does report third-quarter results. But absent a material deterioration in the company's operations, I believe that some upside is warranted from here.

Difficult times

In early July of 2022, I found myself asking whether or not MillerKnoll made for an attractive prospect for investors who are value-oriented. Driven in large part by a merger that created the MillerKnoll that we know today, there was a great deal of uncertainty regarding the company and its future prospects. This uncertainty, however, paved the way to my realization that shares of the company were cheap and that the company's stock probably did warrant some upside from where it was trading at. At the end of the day, I ended up rating the firm a 'buy' to reflect my view that shares should outperform the broader market for the foreseeable future. Unfortunately, that has not exactly come to pass. While the SP500 is up 1.8%, shares of MillerKnoll have seen downside of 10.8%.

{kind=link}

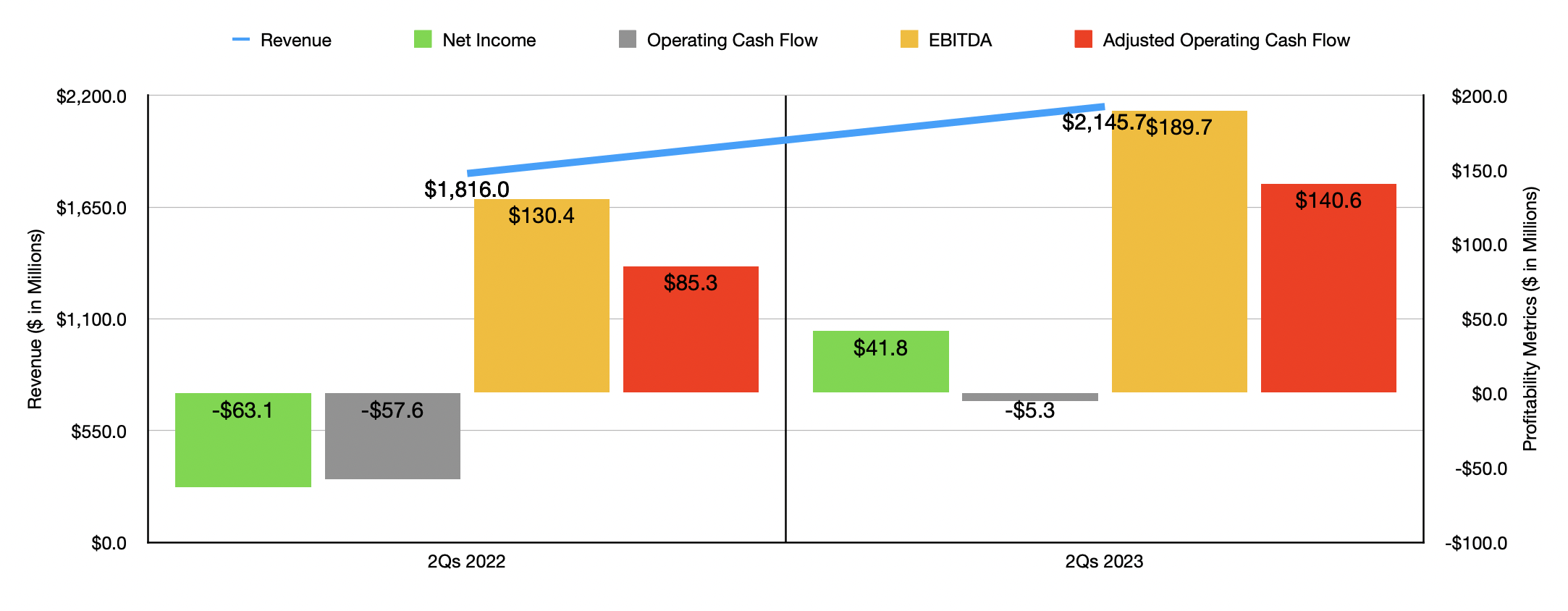

This kind of return disparity may make you think that the company was showing significant signs of weakness. But that's not the case. Consider how the firm performed during the first two quarters of its 2023 fiscal year, neither quarter of which had been reported on when I last wrote about the firm. During that time, sales came in at $2.15 billion. A good portion of this growth, admittedly, was driven by the firm's acquisition activities. This contributed $163.8 million to the firm's sales increase. An extra operating week in the first half of the 2023 fiscal year was responsible for another $52.7 million of the sales increase. However, this was more than offset by a $55.3 million hit associated with foreign currency fluctuations. After making these necessary adjustments, we get organic sales. That number came out to $1.98 billion, which translates to a 9.6% rise over what the company reported the same time one year earlier. On the organic side, the company benefited to the tune of $130 million from increased prices that were passed on to its customers. But it also benefited from international volume increases that added $77 million to the firm's top line, even as Americas volume and retail volume changes impacted sales negatively by $36 million.

On the bottom line, the picture also improved. The firm went from generating a net loss of $63.1 million in the first two quarters of the 2022 fiscal year to generating a profit of $41.8 million. Operating cash flow went from negative $57.6 million to negative $5.3 million. But if we adjust for changes in working capital, it would have moved higher from $85.3 million to $140.6 million. Also on the rise was EBITDA. According to management, it jumped from $130.4 million to $189.7 million.

{kind=link}

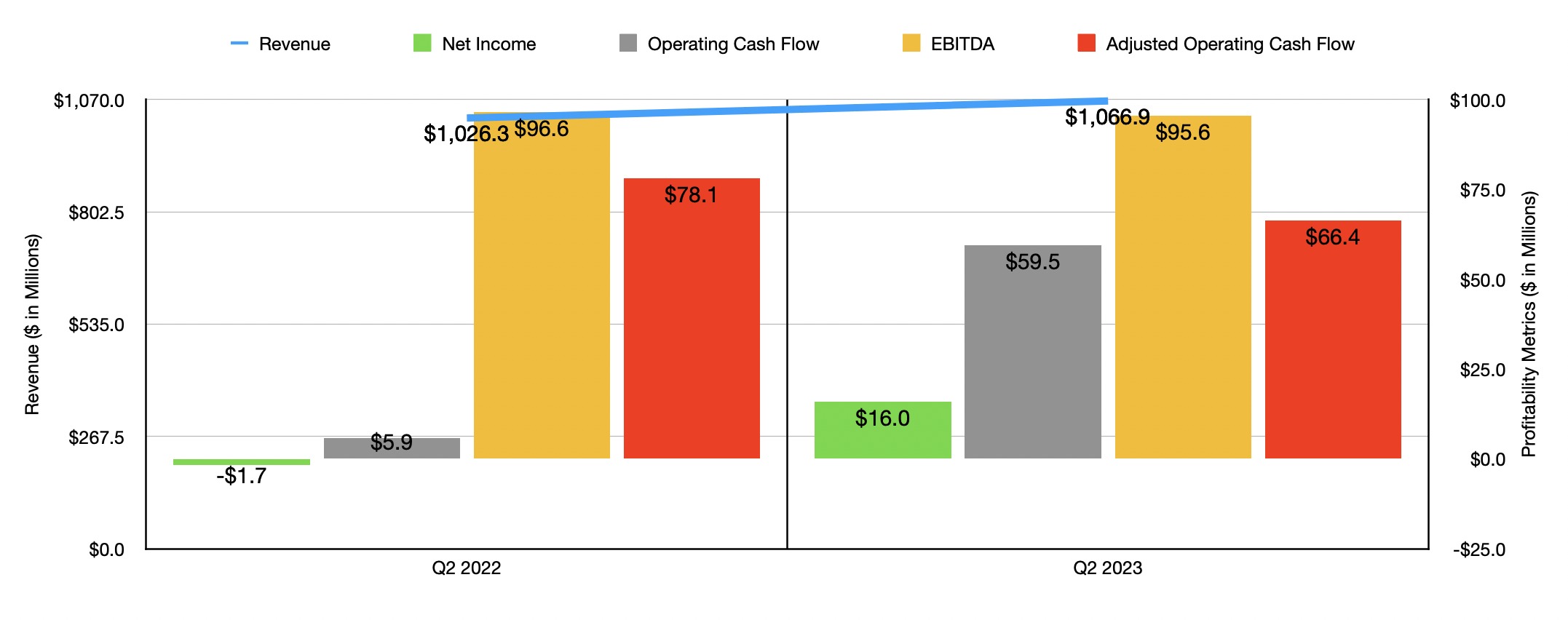

For those worried about a potential weakening as time goes on, I would recommend to focus some on results for the second quarter alone. Sales for that time came in at $1.07 billion. That's up slightly from the $1.03 billion reported only one year earlier. The firm's bottom line went from a net loss of $1.7 million to a net profit of $16 million. Operating cash flow moved up by a multiple of 10 from $5.9 million to $59.5 million. Though if we adjust for changes in working capital, it would have dipped from $78.1 million to $66.4 million. EBITDA managed to fall slightly from $96.6 million to $95.6 million.

Of course, we should also be paying attention to what the future holds. Management has not yet revealed when they intend to release financial results covering the third quarter of the 2023 fiscal year. But we do know that the firm has forecasted sales of between $980 million and $1.02 billion. This is lower than the $1.03 billion the company reported the same time of the 2022 fiscal year. It's important to note that analysts are very bearish about the business on this front. They are currently forecasting revenue of only $999 million. On the bottom line, management said that adjusted earnings per share should be between $0.40 and $0.46. This would compare to adjusted earnings per share the same time one year earlier of $0.28 and GAAP earnings per share of $0.16. Analysts, meanwhile, are forecasting GAAP earnings of about $0.37 per share, with adjusted earnings climbing to $0.42 per share.

{kind=link}

If we annualize results experienced so far for the 2023 fiscal year, we see that the company should generate adjusted operating cash flow of $323.9 million and EBITDA of $604.2 million. Based on these numbers, the company is trading at a forward price to adjusted operating cash flow multiple of 5.6 and at a forward EV to EBITDA multiple of 5.1. These numbers are very low on an absolute basis. But even if we assume that financial performance was to revert back to what it was in the 2022 fiscal year, shares would still be quite cheap, as you can see in the chart above. As part of my analysis, I compared the company to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 4.3 to a high of 15.9. Even using data from the 2022 fiscal year, we can see that two of the four companies that had positive results are trading cheaper than MillerKnoll happens to be trading for. Meanwhile, using the EV to EBITDA approach, we get a range of between 6.4 and 9.1. In this scenario, only one of the companies was cheaper than our target, while another was tied with it.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| MillerKnoll |

| 9.2 |

| 7.4 |

| HNI Corporation ( HNI ) |

| 15.9 |

| 7.4 |

| Steelcase ( SCS ) |

| N/A |

| 9.0 |

| Interface ( TILE ) |

| 13.7 |

| 6.4 |

| Pitney Bowes ( PBI ) |

| 4.3 |

| 9.1 |

| ACCO Brands ( ACCO ) |

| 6.9 |

| 7.7 |

Takeaway

What we are dealing with at this point in time is some uncertainty about the future. It looks as though both management and analysts are forecasting some top line weakness for the third quarter. But on the whole, the company seems to be doing quite well for itself. The stock is cheap and it's difficult to imagine a scenario where shares look any worse off than fairly valued. Given these factors, I do believe that the firm still makes sense as a 'buy' candidate at this time.

For further details see:

MillerKnoll Still Offers Potential Despite Recent Pain