MODN - Model N: Downgrading To Neutral On Deceleration

- Value software stock Model N has been one of the milder decliners within the software sector, losing only 13% of its value this year.

- Fundamentals have held up against expectations, though growth is decelerating due to lapping a major acquisition last year.

- Sequentially, subscription revenue growth is stalling, raising potential go-to-market concerns.

- Trading at ~4x forward revenue, Model N is still cheap, but higher-quality companies are also trading in the same neighborhood.

When it comes to planning for a rebound, I think stock selection is of paramount importance. A rising tide lifts all boats (should the S&P rally by year-end, which is my base-case assumption), but investors will do much better by cherry-picking high-quality, beaten-down stocks with the most valuation rope to climb.

And as we work through this choppy trading year, we should be keen to trade out positions as the landscape changes. Model N ( MODN ), in particular, is a company I've had a change of heart on.

Now, through this year, Model N has been a fortuitous performer. Year to date, the stock has lost only 13% of its value (versus 40% or more for many other SaaS names) - which is a reflection of its milder valuation versus its peers. At the same time, however, I do think Model N's relative outperformance is at an end.

For investors who are not familiar with this company: Model N is a revenue management software platform specifically designed for technology and life sciences companies. Its products include pricing management/CPQ/deal structuring tools that are available in larger "portfolio" software vendors like Salesforce ( CRM ) or Oracle/NetSuite ( ORCL ). Model N is what we would consider "verticalized" software - with functionality specifically tailored to its target industries that purportedly offer a better fit than generic, cookie-cutter software.

Relatively speaking, Model N's traction is impressive. It counts among its customers some of the most recognizable names in its target industries, including: Pfizer ( PFE ), Intel ( INTC ), Johnson & Johnson ( JNJ ), Gilead Sciences ( GILD ), Micron ( MU ), AMD ( AMD ), and Abbott ( ABT ). Yet at the same time, recent results have us wondering: where can Model N grow from here?

Last year, Model N made a major acquisition, taking over the Business Services segment at Deloitte. The strategy here was to combine a consultation/"professional services" arm to help Model N customers onboard to their platform. This acquisition was accretive to both revenue and EBITDA; but now, one year post-acquisition, Model N's reported growth rates are looking a lot milder.

So, yes, Model N is a value stock. But I'm not sure it has enough "juice" to rally, especially since many other software stocks are now trading in its valuation neighborhood despite showing superior growth.

At Model N's current share price near $27, the company trades at a market cap of $989 million. After we net off the $170 million of cash and $130 million of debt on Model N's most recent balance sheet, the company's resulting enterprise value is $948 million.

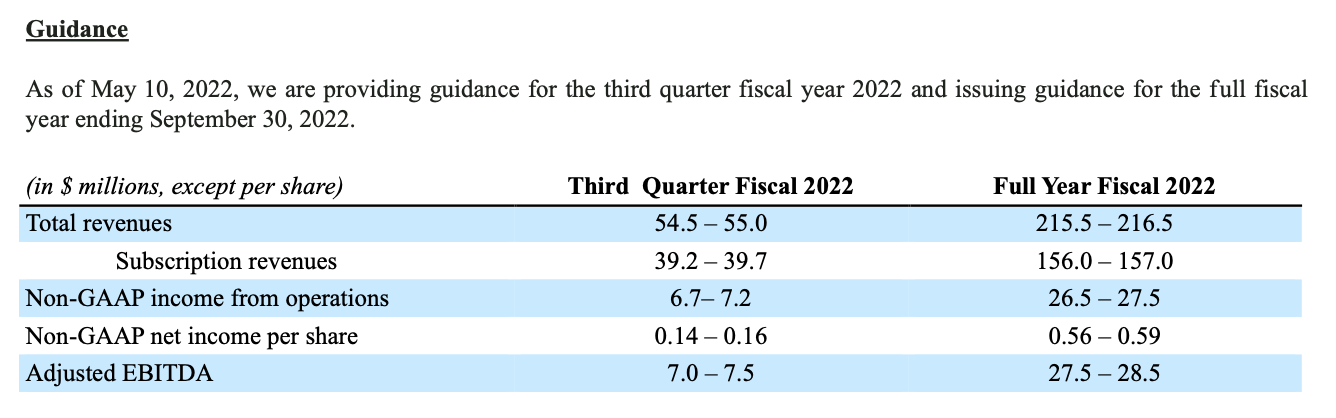

For the current fiscal year, Model N is guiding to $215.5-$216.5 million in revenue, which is a slight boost from its prior outlook given in Q1 of $212-$214.5 million. It's also assuming a 13% adjusted EBITDA margin on this revenue profile and guiding to $27.5-$28.5 million in adjusted EBITDA.

{kind=link}

This puts Model N's valuation at:

- 4.4x EV/FY22 revenue

- 33.9x EV/FY22 adjusted EBITDA

From a bottom line perspective, Model N's adjusted EBITDA is still too thin to justify an earnings-based multiple. The ~4x revenue multiple looks cheap, but due to the severe correction in the tech sector, there are now a number of higher-growth and higher-quality stocks trading in the same neighborhood, shown below:

Any of these names, in my view, are far better contenders to invest in for a rebound in the ~3.5-5.0x forward revenue multiple bucket.

The bottom line here: If you've held onto Model N since the start of the year, congratulations - its losses have beaten the S&P 500 by a few points, and vis-a-vis the rest of the software sector, Model N has done quite a bit better. But now that reported growth rates are slowing down, subscription revenue growth looks a bit sluggish, and valuation is now more in line with higher-performing peers, I'm updating my rating on Model N to Neutral. You'll do better investing elsewhere from here on out.

Signs of a slowdown

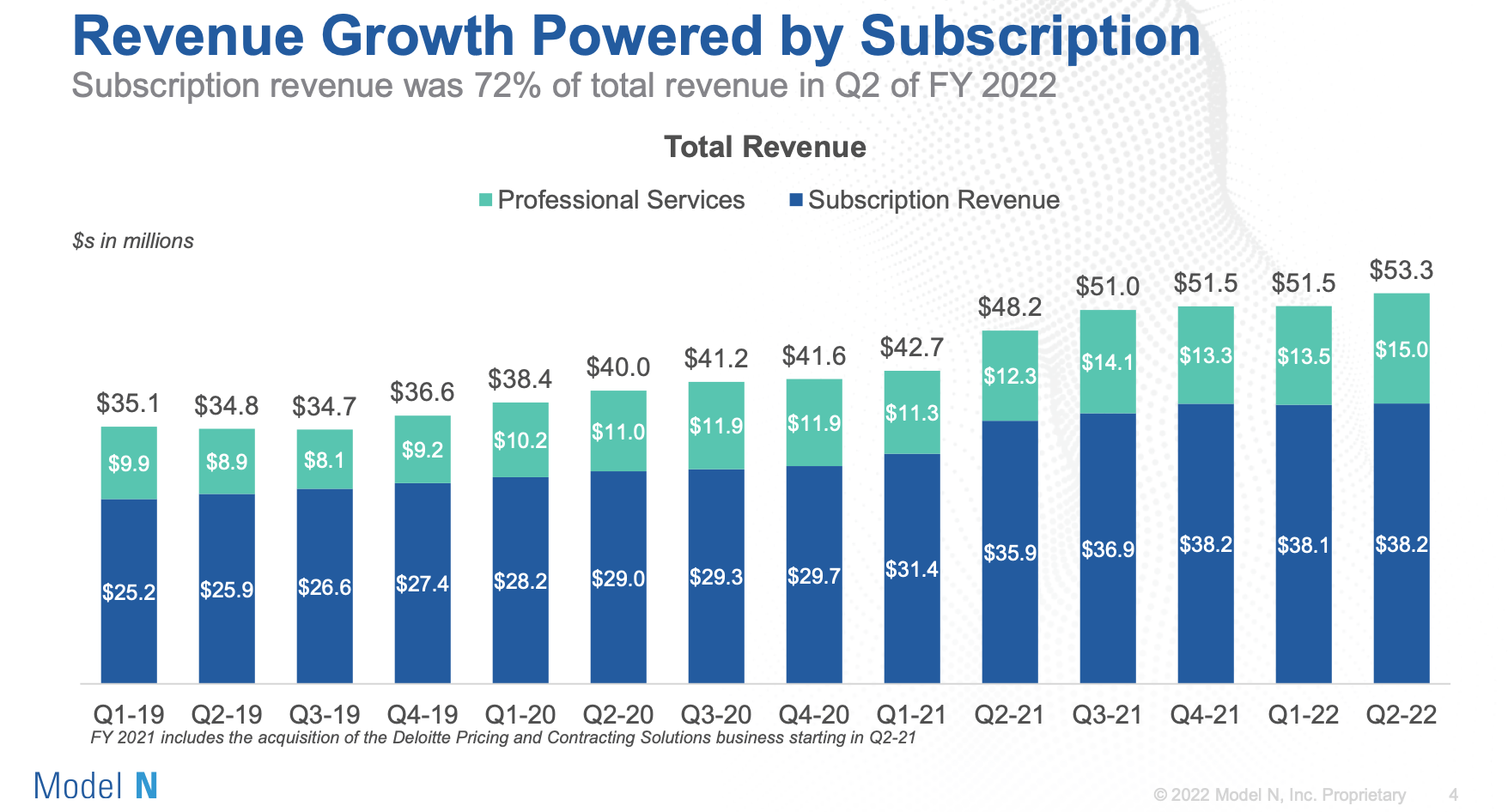

In Q2 (the fiscal quarter for Model N ending in March), Model N grew its revenue at an 11% y/y pace to $53.3 million, outpacing Wall Street's expectations of $51.3 million (+6% y/y).

{kind=link}

This revenue growth slowed down versus 22% y/y growth in Q1, but to a large extent, this was already expected - as Model N is finally lapping the Deloitte acquisition that closed in the second quarter of last year.

That's not my main concern - the bigger red flag here is that Model N's subscription revenue has been flat over the past three quarters. If you look at the revenue trend in the chart above, you'll notice that subscription revenue has held flat at ~$38 million over the past three quarters.

Now, there are counterbalancing points here. First, the company did note that bookings performance was strong in both Q1 and Q2, which was what prompted the slight guidance boost for the rest of FY22. So, perhaps looking at data just through Q2 may be short-sighted, and growth may improve as those bookings materialize into revenue.

Second, the company is still growing subscription ARR at a 16% y/y pace - and some declines in maintenance revenue may be offsetting growth in SaaS. CEO Jason Blessing's prepared remarks on the Q2 earnings call point to potential acceleration in ARR growth in the back half of the year:

As a reminder, during the year we continue to expect strong growth in SaaS revenue to be offset by declines in maintenance revenue, as cloud migrations, accelerate. To give you a better indication of our success in transitioning from on premise to SaaS, we have begun disclosing SaaS ARR. This represents the annualized value of our-daily subscription revenue for the most recent quarter. As we've noted on our last couple of earnings calls, we anticipated a more challenging quarter in Q2 from a comparison standpoint. This did transpire in the second quarter, as we finished with $89.9 million in SaaS ARR which was up 17% on a year-over-year basis. While our trailing 12-month net dollar retention on SaaS was 116%, both of these numbers were slightly below recent trends, but again as we previously commented we expect SaaS ARR growth to accelerate over the second half and exit the year at our 20% growth target."

I would be hesitant, however, to bake in any expected strength before it materializes, especially if net retention rates are trending downward. Based on backward-looking revenue trends alone, this looks like a business that is flatlining and is reaching a saturation point in its relatively niche end-market.

Key takeaways

In my view, Model N has had a good run relative to the rest of the market, but it's running out of steam. I'm concerned about flatlining subscription revenue growth and slightly pessimistic commentary on a downtick in net retention rates. At a ~4x forward revenue multiple, Model N is still cheap, but not so much cheaper relative to higher-performing software stocks to warrant holding.

For further details see:

Model N: Downgrading To Neutral On Deceleration