MODN - Model N: Where Do We Go From Here? (Ratings Downgrade)

2023-08-22 05:00:00 ET

Summary

- Tech stocks have seen a decline in the Q2 earnings season, including revenue-management software company Model N.

- Model N is struggling to show substantial growth and justify its market cap, putting it in a precarious position in the tech industry.

- Despite having a large total addressable market, Model N's growth rate is relatively low compared to competitors like Salesforce.com.

- Profits haven't kept up enough to justify Model N's >$1 billion market cap.

Almost without exception, the early summer rally in tech stocks has been wiped out during the August earnings season. Even among companies that are reporting strong results, stocks are falling as investors realize that fundamentals can't justify that valuations that have quietly ballooned since the start of the year.

Model N ( MODN ) is in this boat. The revenue-management software company has dropped approximately 10% since reporting results in early August, and year to date, the stock has shed more than 30%.

I previously wrote on Model N back in May , and my assessment on the company back then was neutral - though now, after seeing the company's fiscal Q3 (calendar Q2) results show continued deceleration and incapability of driving meaningful profit expansion, I no longer think Model N has much appeal at all. With short-term interest rates sitting above 5%, why invest in a non dividend-paying, not-GAAP profitable company that is barely growing?

Given the lack of fundamental catalysts and the company's relatively disappointing results, I am downgrading my viewpoint on Model N to bearish. It's best to sell here and invest elsewhere.

Large TAM? Current growth rates show a company that is incapable of capturing this market

Model N is sitting in what I'd consider to be a tech company's "no man's land." It has stopped showing fierce growth rates, but at the same time, its bottom-line progress is insufficient to justify the company's market cap from an earnings basis. And so, quarter after quarter, the story here remains the same: a company that is unable to grow substantially beyond its current station, which is effectively a death sentence in the tech industry. In tech, you either grow larger and dominant in your space, or you flame out into irrelevance (the lucky few get acquired, but Model N's financial profile and debt load aren't really conducive to an M&A takeout).

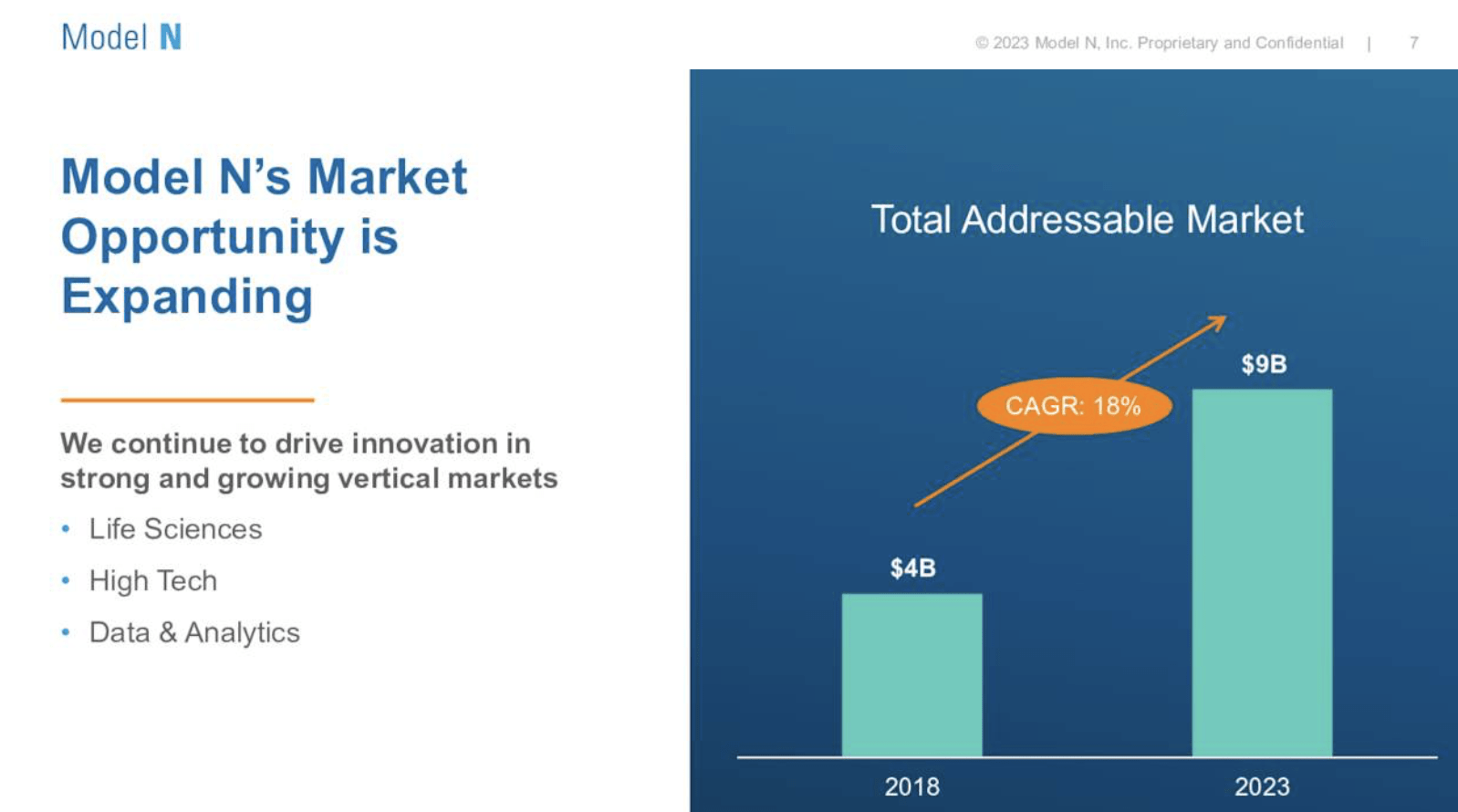

All along, Model N continues to cite that it has a large total addressable market despite its niche of only serving two industries (tech and life sciences: and the reason it specializes in these two sectors are because these companies have complicated revenue arrangements which Model N software is intended to help manage), which it estimates at $9 billion in 2023.

Model N TAM (Model N Q3 earnings deck)

{kind=link}

But the question is: if Model N's market is truly that large, and its current ~$250 million annualized revenue run rate is only 3% penetrated into this market, why is Model N only capable of relatively low 13% y/y growth?

For comparison's sake: Salesforce ( CRM ), one of Model N's core competitors in revenue management and who is unencumbered by serving only specific industries, also grew revenue at a 13% y/y in the fiscal first quarter on a constant-currency basis - despite generating nearly $10 billion in quarterly revenue, or more than 100x Model N's current scale. In other words, sluggish growth for a company so small is discouraging.

It's also worth noting that Model N doesn't lack a stable of high-powered customers. The chart below shows that it already does business with the likes of Intel ( INTC ), Abbott ( ABT ), Pfizer ( PFE ), Johnson & Johnson ( JNJ ) - the list of blue-chip firms that are already Model N clients goes on and on.

Model N customers (Model N Q3 earnings deck)

{kind=link}

This begs the question, then: where exactly does Model N go from here? And without major growth prospects ahead of it, will the company ever scale to meaningful profitability that can justify further expansion in its stock? This is the driving reason behind my downgrade to bearish in this stock.

Q3 download

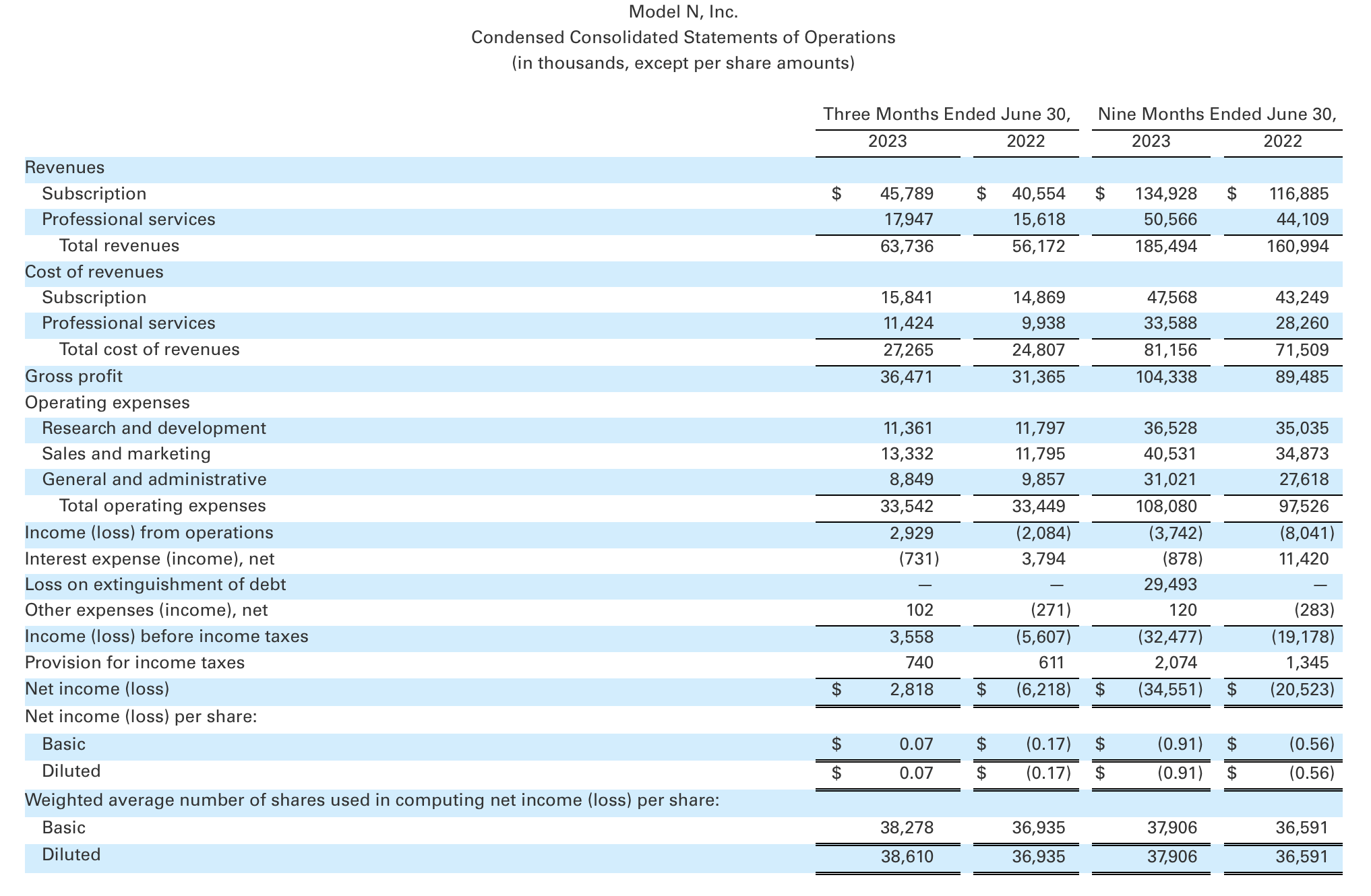

Let's now go through Model N's latest quarterly results in greater detail. The fiscal Q3 (June quarter) earnings summary is shown below:

Model N Q3 results (Model N Q3 earnings deck)

{kind=link}

Model N's revenue grew 13% y/y to $63.7 million, essentially in-line with Wall Street's expectations of $62.2 million (+11% y/y) and decelerating four points versus 17% y/y growth in Q3.

The company continues to cite soft macro conditions as a drag on its results. Increased deal scrutiny from customers' exec teams continues to slow down sales cycles, requiring additional approvals before getting the ultimate green light. Fortunately, the company reports that it believes this trend has stabilized and isn't getting worse. It believes these conditions hurt the timing of deals only, but that ultimately projects will still close.

Model N's SaaS transition is also nearly complete. SaaS ARR grew 28% y/y to $129.2 million, and SaaS is now over 60% of the company's total subscription revenue.

What devastated investors more than Q3 results, however, was soft commentary surrounding the company's outlook for 2024.

Without providing exact guidance, CFO John Ederer noted as follows on the Q3 earnings call:

Finally, looking ahead to fiscal 2024, this is a particularly challenging time to provide a five-quarter outlook given the timing nuances that Jason discussed earlier. While pipeline is improving for the second half of the calendar year and while there's a lot of interest around the future potential for data and analytics coming out of Rainmaker, we want to be prudent in our approach and focus on what we have line of sight to today.

In FY 2024 we will have some similar trends and challenges. First, we continue to target SaaS ARR growth of 20% for the year but certain quarters notably Q2 next year will be challenging due to tough year-over-year comparisons.

Second, we have seen more impact from the macro environment on our software-enabled subscription service offerings, and expect lower growth from these offerings next year. And then third the decline in maintenance revenue will again be a headwind potentially approaching a 50% decrease next year.

Rolling all of these factors up, we would expect revenue growth next year that is in line with our Q4 guidance. Hopefully, there will be some upside from the recent build in pipeline but we'll wait to see how the next couple of quarters go and update all of you at the appropriate time."

Revenue growth "in line with Q4 guidance" implies decelerating to just 7% y/y growth going forward, despite easier 2023 comps stemming from macro softness.

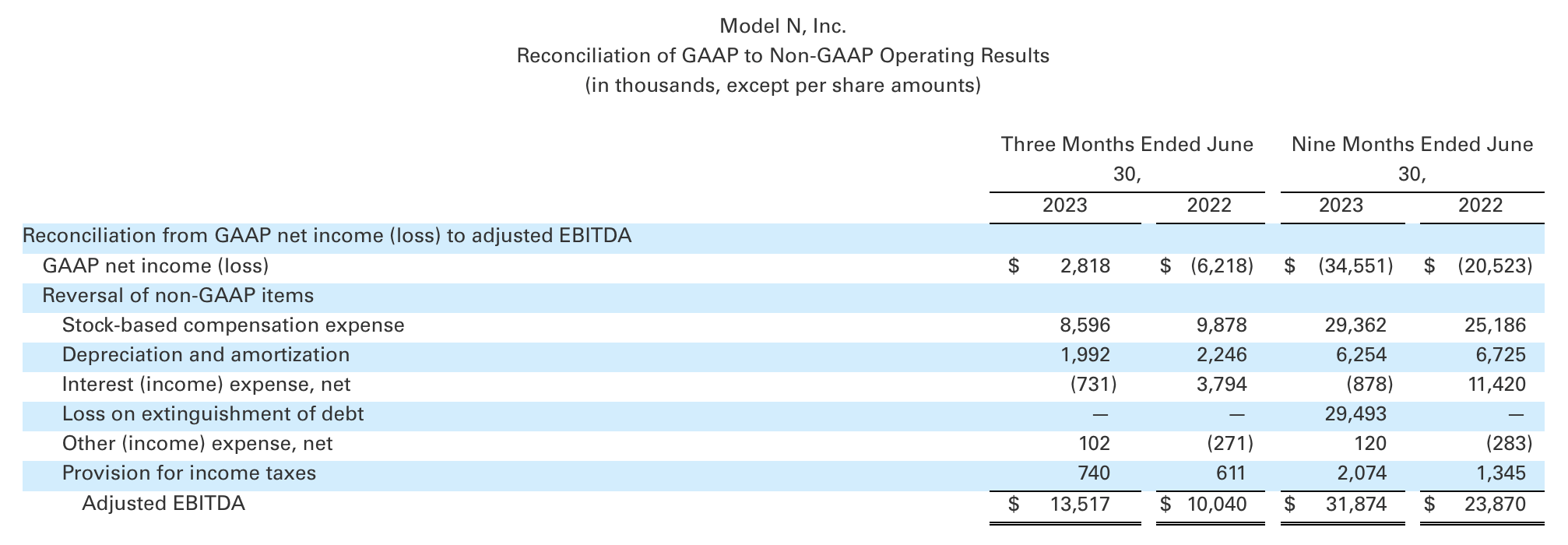

The one bright spot is in profitability, where Model N grew adjusted EBITDA 34% y/y to $13.5 million, representing a 21% margin - three points better than the year-ago Q3 margin of 18%.

Model N adjusted EBITDA (Model N Q2 earnings deck)

{kind=link}

Still, however, these levels of profitability are hardly sufficient to justify Model N's valuation.

Valuation and key takeaways

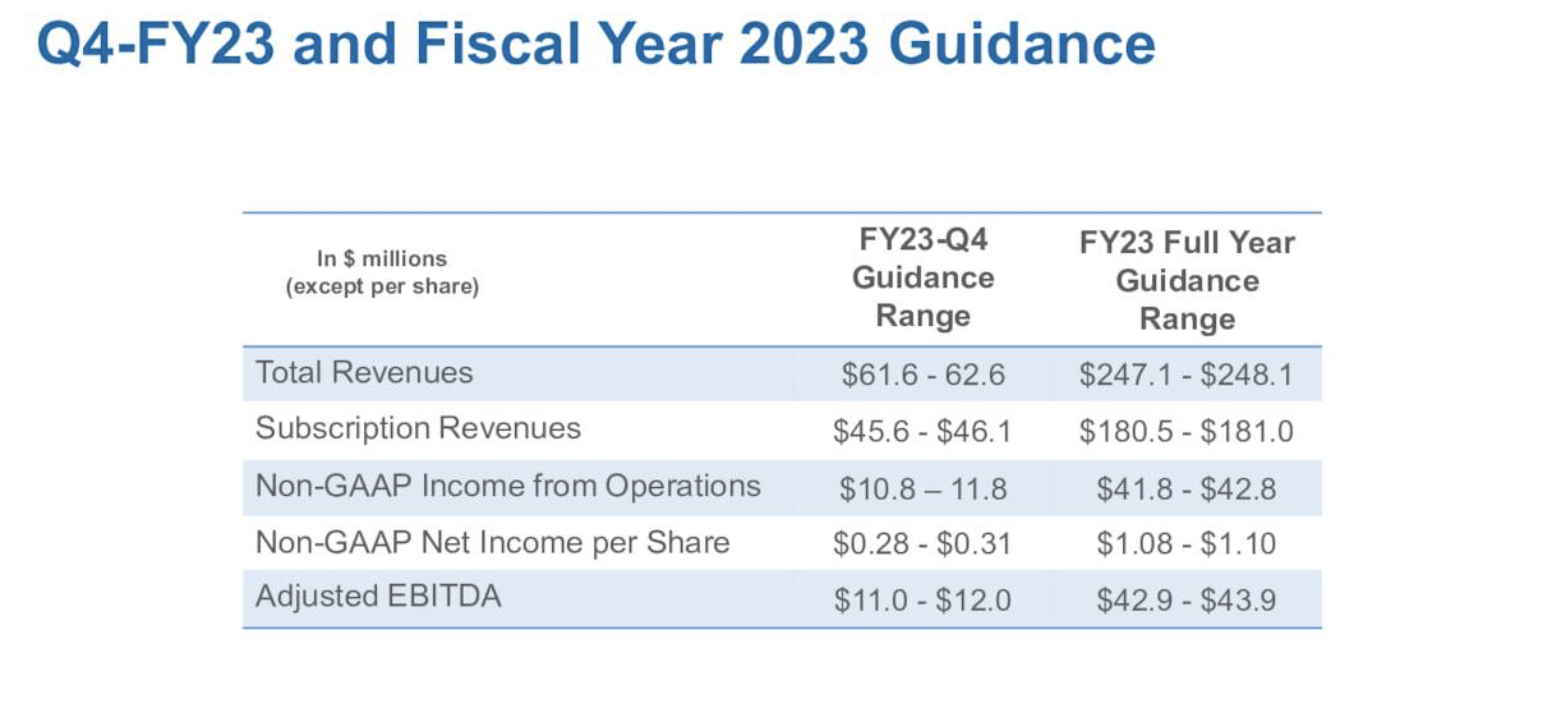

At current share prices near $28, Model N trades at a market cap of $1.06 billion. After we net off the $299.6 million of cash and $279.9 million of debt on Model N's most recent balance sheet, the company's resulting enterprise value is $1.04 billion.

Model N guidance (Model N Q2 earnings deck)

{kind=link}

Against full-year expected revenue of $247.1-$248.1 million and adjusted EBITDA of $42.9-$43.9 million, Model N's multiples stand at:

- 4.2x EV/FY23 revenue

- 24.0x EV/FY23 adjusted EBITDA

To me, these valuations aren't enticing enough to try to catch the falling knife here. It's time to ditch this stock and invest elsewhere.

For further details see:

Model N: Where Do We Go From Here? (Ratings Downgrade)