MODV - ModivCare: A First Take

Summary

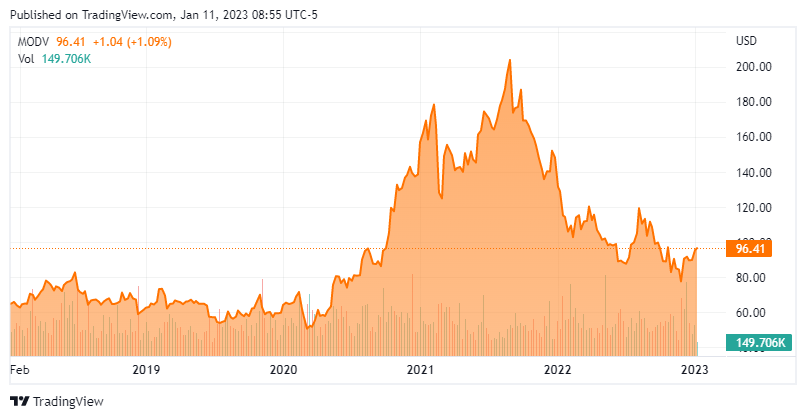

- Shares of Medicaid and Medicare transportation provider ModivCare (MODV) are down over 50% from their Sept 2021 peak as cost inflation and its deteriorating Matrix investment have weighed.

- The company has entered two higher margin businesses that should benefit from its lengthy relationships with managed care organizations.

- Trading at a 12 P/E on FY23E earnings and a price-to-FY23E sales of 0.5, the recent insider buying into this thinly traded stock merited further investigation.

- A full investment analysis follows in the paragraphs below.

I have always found that mercy bears richer fruits than strict justice .”? Abraham Lincoln

Today, we take a look at a small cap name in a unique niche of the healthcare space. The stock has been hit hard by cost inflation and an ill-timed investment. The pullback has left the stock trading at 50% of annual sales and triggered some recent insider buying. An analysis follows below.

{kind=link}

Company Overview:

November Company Presentation

ModivCare Inc. ( MODV ) is a Denver, Colorado based provider of supportive care services on behalf of public and private insurance firms and their patients. For approximately two decades, these services primarily included non-emergency medical transportation (NEMT) and then expanded into personal care (November 2020), and remote patient monitoring (September 2021). The company also owns a 43.6% stake in CCHN Group Holdings – more on that investment below. ModivCare was established as The Providence Service Corporation in 1996, went public in 2003 – raising net proceeds of $36.2 million at $12 a share – and rebranded to its current moniker in 2021. Shares of MODV trade for around $96.00 a share, equating to a market cap of approximately $1.35 billion.

November Company Presentation

Divisions

The impetus behind its recent expansion into other supportive care services was two-fold: to leverage its existing relationships with managed care organizations into cross-selling or bundling opportunities; and to expand into businesses with higher margins than its transportation service. With these recent adds, the company views its operations through two divisions (Mobility and Home), but essentially three operating segments with a fourth possibly incoming.

November Company Presentation

Mobility/NEMT . The company’s largest revenue generator is its legacy Mobility unit, which is its NEMT segment. It enables eligible members, who would otherwise be hindered by limited mobility or financial resources, access to healthcare and social services. Operating in all 50 states and the District of Columbia, the Uber ( UBER ) for the elderly is on pace to manage ~100 million trips for ~36 million members of predominantly Medicare Advantage and Medicaid programs in FY22. The vast majority (~85%) of its revenue is derived from capitalized contracts, where the payor remits a fixed amount per eligible member. The other 15% is billed when an actual service is provided. For the last twelve months (LTM) ending September 30, 2022, NEMT generated Adj. EBITDA of $172 million on revenue of $1.7 billion, or ~65% of total. ModivCare is the number one provider of NEMT, with a ~28% share of a ~$6 billion market (FY21) that is expected to grow to ~$14 billion by FY24. Its main competitors are all non-publicly traded concerns: Medical Transportation Management, Southeastrans, Veyo, and Access2Care. Owing primarily to regulatory issues, Uber and Lyft ( LYFT ) have stayed out of NEMT to date.

Home . The Home division was spawned when the company acquired personal care business Simplura Health Group in an all-cash transaction totaling $575 million in November 2020. That transaction was followed by the purchase of Care Finders Total Care for a cash consideration of $340 million in September 2021. These two concerns comprise the Personal Care Services [PCS] segment of the Home division, which places non-medical personal care assistants, home health aides, and nurses – totaling over 16,000 – predominantly with Medicaid patients in need of assistance with daily living activities and companionship. Located in seven eastern states, PCS generates ~87% of its revenue from services performed in Pennsylvania (34%), New York (34%), and New Jersey (19%). In the LMT ending September 30, 2022, PCS was responsible for Adj. EBITDA of $66 million on revenue of $649 million (27% of total), providing 27 million hours of care.

PCS operates in a $55 billion total addressable market (2019) that is highly fragmented, with the top three players commanding <5% of the market. However, that opportunity is expected to grow to ~$100 billion by 2024.

November Company Presentation

The other segment under Home is Remote Patient Monitoring [RPM], which was established with the acquisition of VRI Intermediate Holdings for $315 million cash in September 2021 and bolstered by the purchase of Guardian Medical Monitoring for a net cash consideration of $71.3 million in May 2022. RPM’s high-touch platform enables emergency response, vital sign checks, and medication management out of three 24/7 care centers that communicate via 250+ different monitoring devices. The segment has over 230,000 members, most who are very satisfied with its service, having given it a net promoter score of 86. RPM accounted for LTM (pro forma) Adj. EBITDA of $27 million on revenue of $76 million, or 3% of total. Management pegs RPM as a $9 billion total addressable market (2020) – with competing offerings from the likes of Medtronic ( MDT ), Koninklijke Philips’ ( PHG ) Philips Healthcare, DexCom ( DXCM ) , and Honeywell’s ( HON ) Life Sciences division – that is expected to grow to $15 billion by 2025.

Leveraging its transportation expertise, ModivCare is toying with the idea of entering the $9 billion nutritional meal delivery business, which would become part of its Home division. Currently running a pilot program partnered with a food service provider, the company has delivered more than two million meals. That said, it is unclear if this business line is a top priority for the recently installed CEO.

Matrix Investment

In addition to its expanding core operations, ModivCare owns a 43.6% interest in CCHN Group, which operates under the Matrix Medical Network banner. It is a national network of community-based clinicians who deliver in-home and on-site services, as well as a fleet of mobile health clinics that provide diagnostics and healthcare. When the pandemic struck, this risk assessment business logically got involved in Covid-19 testing but also entered the clinical trial patient recruitment business, which proved a mistake. After generating Adj. EBITDA of $113.3 million on revenue of $414.6 million in FY20 – a 51% surge over FY19 thanks to Covid-19 testing – its top line slowed significantly in 2H21, finishing FY21 with Adj. EBITDA of $67.5 million on revenue of $398.3 million. Matrix was compelled to take a $111.4 million asset impairment charge in 4Q21, reflecting a significant slowdown in its clinical solutions segment after Covid-19 testing dried up.

November Company Presentation

After taking a $38.5 million hit to its equity investment due to Matrix’s poor performance in FY21, ModivCare elected to terminate it as a separate reportable segment and created a Corporate unit, under which this investment and other items are currently housed. Then in 3Q22, Matrix was compelled to take another asset impairment charge (of $82.2 million) – this time related to its clinical trial business – resulting in another equity investment write down ($36.1 million) for ModivCare. Once viewed as a valuable piece to the company’s story, Matrix has devolved into a significant drag. Complicating matters: majority owner Frazier Healthcare is a private equity firm that invested in Matrix in 2016 and as such is likely looking for the exit.

Share Price Performance

After trading to $40.40 in the throes of the 2020 pandemic selloff, shares of MODV rallied 425% to $211.94 in September 2021 as its NEMT offering and Matrix were perceived as pandemic winners and investors applauded its expansion into the PCS and RPM businesses. However, with Matrix’s 3Q21 revenue declining 44% year-over-year and ModivCare’s FY21 non-GAAP earnings (without Matrix) projected to be 4% lower than FY20 at $7.89 – hurt by cost inflation – the market adjudged that a ~22 PE on FY21 earnings (at that time) was far too expensive and initiated a three and a half month selloff (aided by the turmoil in the overall economy) that saw its shares dip below $100 by early February 2022. Except for a recent dip below $80 a share, its stock has predominantly spent most of 2022 in a range of $85 to $115. The CEO was dismissed in August 2022 and was replaced by the CFO, a position still unfilled.

3Q22 Results & Outlook

The second impairment charge was part of ModivCare’s 3Q22 financial report of November 3, 2022, in which it announced non-GAAP earnings of $1.61 a share and Adj. EBITDA of $51.8 million on revenue of $647.8 million versus $1.63 a share (non-GAAP) and Adj. EBITDA of $44.3 million on revenue of $493.1 million. Although the Adj. EBITDA increase looked encouraging, it was a function of contributions from acquisitions made over the prior 12 months.

November Company Presentation

Management did raise its top-line FY22 guidance from $2.39 billion to $2.46 billion but elected to keep its FY22 Adj. EBITDA forecast unchanged at $215 million – all based on range midpoints – as the higher revenue estimate reflected pass throughs of higher costs to customers. The adjustment served to highlight the low-margin nature of the business, with FY22E Adj. EBITDA margin lowered from 9.0% to 8.7%.

November Company Presentation

Balance Sheet & Analyst Commentary:

To acquire businesses for its new division (as well as others for NEMT), ModivCare has spent $1.3 billion since 2020, onboarding debt of $1 billion in the process. As of September 30, 2022, it held cash of $73 million and had access to an additional $325 million of liquidity through a revolving line of credit. With pro forma TTM Adj. EBITDA of $224 million, its net leverage was a noteworthy 4.0, although management felt confident in its ability to eventually deleverage to 3.0.

November Company Presentation

Like its share count of 14.1 million, ModivCare’s following is small, but bullish, comprised of Barrington (outperform rating; $138 price target), Stephens (outperform; $145), Jefferies (Buy; $150) and Deutsche Bank (buy; $130). On average, they expect the company to earn $6.72 a share (non-GAAP) on revenue of $2.47 billion in FY22, followed by $7.54 a share (non-GAAP) on revenue of $2.61 billion in FY23, representing gains of 12% and 6%, respectively.

Chairman of the Board Christopher Shackelton, representing the interests of Coliseum Capital Management, used the stock’s recent dip below $80 a share as an opportunity to add 90,743 shares to his firm’s position, which now hovers just below 10%. News of this purchase triggered a three-day 18% rally back above $90 a share.

Verdict:

The insider has a long-term view that stronger margins from ModivCare’s new businesses and demographic tailwinds will win the day. In the meantime, ModivCare’s margin gets compressed because of increases in caregiver wages, higher fuel costs, and other labor (driver) related wages. That said, the company has restructured many of its contracts so payors will participate in the absorption of these elevated expenses. Assigning a zero value to Matrix, ModivCare trades at a 12 P/E on FY23E EPS, a 0.5 price-to-FY23E sales, and an EV/pro forma TTM Adj. EBITDA of 10 – not outrageously cheap given its 55% decline over the past 15 months. Its recent rally notwithstanding, its stock is still poking around for a bottom, which will not come until at least the release of the company’s 4Q22 financials, when it will likely provide its FY23 outlook. Until then, expect shares of the still predominantly low-margin transportation business to trade mostly sideways. Owing to its extremely low float – the company would benefit from a five-for-one stock split – the illiquidity in the option market does not lend itself to a covered call strategy. As such, the recommendation is to remain on the sidelines for now.

For children are innocent and love justice, while most of us are wicked and naturally prefer mercy .”? G.K. Chesterton

For further details see:

ModivCare: A First Take