MODV - ModivCare: Earnings Power Asset Factors A Major Headwind To Bullish Re-Rating

2023-07-18 01:42:39 ET

Summary

- ModivCare continues to present a balanced investment debate, with mitigating factors on both sides of the fence.

- The company's unit economics show mixed performances, although efficiencies were a takeout from its Q1 numbers.

- Despite this, MODV's economic characteristics do not imply a re-rating is on the horizon, in my opinion.

- Net-net, reiterate hold.

Investment briefing

Since my April publication on ModivCare Inc. ( MODV ) there have been numerous updates to the investment case. I had urged investors to hold off buying MODV in the last report, based on a number of factors:

- Insufficient returns on new capital - you're looking at 14%, in FY'20, negative 4.6% in FY'21, negative 2.7% in FY'22.

- In my opinion, the company's return on new capital could average 0%-6% going forward.

- Negative operating leverage, on average, since 2019 at least. This isn't conducive to growth in owner earnings.

- Despite the growth in intrinsic value of 23% per year from FY'18-'22, it had to reinvest 238% of earnings to do this. Investing at 238% for 23% = not attractive in my investment cortex. By all measures, my estimates have similar trends going forward.

Moving to the present day, there are a number of updates that investors must understand prior to making any investment decisions on MODV. Chief among these are the financial and sentimental deltas that have cropped up over the last 3-months of trade. Net-net, I reiterate MODV a hold, noting headwinds to growth, returns on capital, and valuation, and I'll run through all of the major updates to the investment thesis here today.

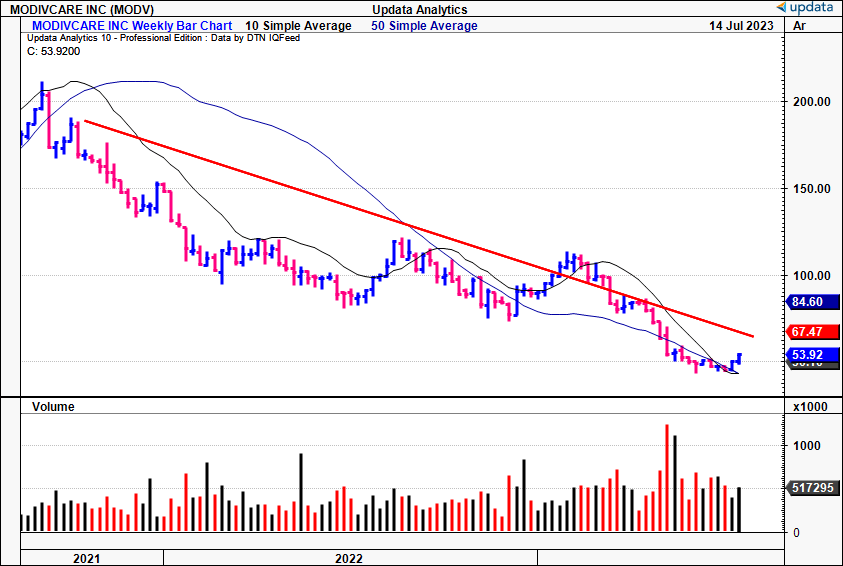

Figure 1. MODV equity performance, FY'21-date [weekly bars]

{kind=link}

Changes to critical investment facts

First and foremost, MODV affirmed its FY'23 guidance with its Q1 FY23 numbers, calling for $2.575Bn-$2.6Bn at the top line on adj. EBITDA of $225-$235mm. I'd note this is an important statement, given the firm's long term aspirations of printing $3Bn in turnover on ~$300mm in adj. EBITDA by FY'25.

1. Top-line breakdown

Turning to the Q1 numbers , total revenues were up 15% YoY to $662mm on adj. EBITDA of $50mm, flat YoY. Upsides were driven by a 17% YoY increase in mobility and double-digits in the home division. It pulled this down to a net loss of c.$4mm.

Figure 2.

Data: Author, MODV SEC Filings

Looking at the divisional takeouts:

- The NEMT business grew sales to $469mm, underscored by a 5% growth in average monthly members and a 12% increase in revenue per member per month ("pm/pm"). It drew $35mm in pre-tax earnings on this, helped by a 100bps YoY reduction in transport costs from Q4 last year.

- Breaking down sales from its home division, personal care revenues were up 9% YoY to $174mm. A good sign was that the 900bps came from a 4% increase in hours. There are major benefits of increasing hours within any realm of broad healthcare. For one, it helps recruitment and retention efforts, in this instance for caregivers on MODV's books. It also boosts productivity for the top line- you see this in the 400bps growth in revenue per hour MODV clipped in Q1.

- The problem for MODV in its personal care segment is twofold in my opinion:

- Reimbursements are trending lower, and will land between 3-5% this year. This is likely to clamp profitability economics for the company in my view.

- Pre-tax margins are below 10% for the segment, thus a paltry contribution to the top line, and thus, for shareholder earnings. Combined, you can't expect the capitalist floodgates to open, and investors to start piling in on factors of earnings growth, or value-add.

- As a result, the company plans to consolidate 12 critical business functions, in this arm of its business, so that 100% of its personal care team aligns with a centralized management. This, it hopes will see margins lift to ~12%.

- Perhaps the standout was the 35% YoY growth in its remote patient monitoring ("RPM") business. It clipped $18.7mm in turnover for the quarter. This was all momentum built around the company's acquisition of Guardian Medical Monitoring, made back in FY'22.

Furthermore, it booked 35% EBITDA margin on this- nearly 3.5x the personal care segment. It is therefore no secret where MODV should continue its focus, in my view.

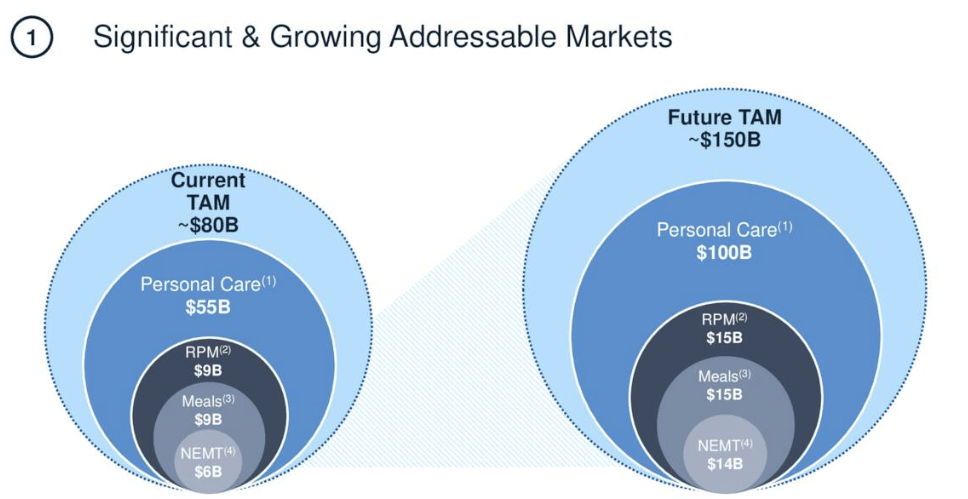

Figure 3. Lower-margin personal care segment tipped for biggest addressable market

{kind=link}

2. Unit economics are mixed moving forward

Further breakdown on the above, you'll note several talking points around the company's unit economics. These factors feed into my reiterated neutral view on the company, and the changes exhibited in Q1 set the stage for what to expect moving forward.

One, in its mobility division, MODV employs a partnership model with various providers of care. On this, its preferred providers accounted for ~17% of the company's patient trips, up from 11% the year prior. Naturally, this helped the average cost per trip drift lower YoY. Noteworthy progress was also made in a 7% sequential reduction in calls per trip, down 14% compared to the previous year. Additionally, missed trips were reduced by ~10% sequentially. Should these trends continue it is positive. First, it should drive turnover to its mobility segment, and then, with the efficiencies, add to unit profitability as well. Management look to NEMT unit costs/trip reducing from $42/trip to $35-$38/trip by FY'25.

Two, the personal care business relies on a combination of same-facility growth, and new facility additions to expand. MODV opened 2 de novos in Q1, with plans to open >10 by the end of the year. Therefore, knowledge of the capital charge on each new facility is paramount. Net PP&E increased $8.1mm sequentially into Q1, implying an average charge of $4.05mm for both facilities. Keeping this same convention as a basic assumption, gets me to a $40.5mm investment allocation to de novos this year. Whilst these are basic assumptions, this would reduce owner earnings by that amount if true, so we'd expect at least that in extra post-tax earnings over the coming 12-months to justify the moves in my opinion.

Three, regarding contract payables, these were down $7mm as expected. As a reminder, MODV's contract liabilities pertain to overpayments, and liabilities on specific NEMT contracts it holds. However, the company anticipates a large settlement in Q2 that was previously expected to be spread throughout the year. Hence, it will likely book CFFO at a similar pace to Q1, which resulted in a ~$3mm outflow.

Hence, there are mixed feelings about the investment facts of MODV's unit economics going forward. On the one hand, there's good improvements in its mobility offerings, but at the same time, I'm cautious on the firm's propensity to add value through its capital investment programs. This supports a balanced view.

3. Returns on new capital a headwind to attract investment

I covered this extensively in the last publication, so it is not so much a change in theme as it is an update to my numbers. I'd discovered the firm delivered 9.7% return on new capital from FY'18-'22, producing $120mm in additional earnings from $1.24Bn investment.

This is not attractive in my eyes, because investors have earned multiples of this return themselves simply riding the benchmark. In that vein, what value has MODV added during this time? Basically none from an investors perspective, and, if you strip the pandemic-era anomaly out of the equity markets, MODV sits right where it does 5-years ago as direct evidence of this. The market isn't silly-it knows exactly what, and where capital is most valuable.

This is quantified in the series below. The chart shows the rolling TTM NOPAT generated off the existing capital MODV committed over the last 3 years. A firm should beat the market's return on capital in order to create value for shareholders (long-term market averages are in the realms of 10-12%). Hence, MODV hasn't met this litmus test-the economic profits, those earnings above or below the hurdle rate- haven't come in higher than 12% each period. In that vein, all of the business growth MODV has embarked on has been destructive to its intrinsic valuation. I mentioned the market is very wise on this point- it won't reward companies where the growth in earnings comes at a cost to equity holders, by not meeting the cost of capital. As you'll not in the chart, my estimates have these trends to continue moving forward, with no reversal in sight.

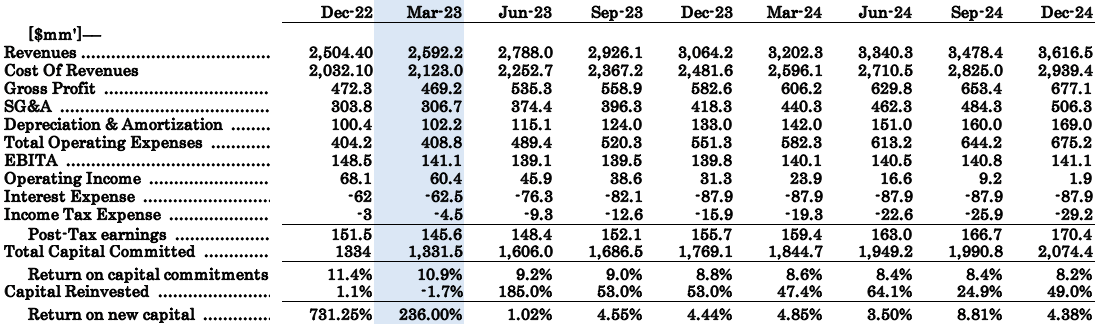

Figure 4.

Data: Author, MODV 10-Q's

Valuation

As a result of the updates from its Q1 numbers, I've made a set of adjustments to my own modelling. I've got MODV to do $3Bn in turnover this year, marginally ahead of management's view, and it wouldn't be unreasonable to see it pull this to $100-$155mm in post-tax earnings in my view. This, on the company's planned investments, would result in a ROIC of 8.8% for the year, again behind the hurdle rate. Further, the incremental returns I've got fall short too at 4.4%.

The market has fairly low expectations for it too- at the current market cap of $763mm, the market expects $91.5mm in post-tax earnings from the company this year, assuming a 12% discount rate (91.5/0.12= $763). That calls for 35% growth on FY'22 EBIT of $68.1mm, assuming the same discount rate. This is reasonable and fair in my view, but fairly priced at the current stock price.

Investors are selling MODV cheaply at 7.8x forward earnings, and 0.3x sales. To me this says investors are parting with their stock with little objection, perhaps looking to unload on the same circumstances. It's also priced at 20x forward EBITDA, which to me, isn't worth paying based on the lacklustre forward returns on capital in my estimates.

Discussion

Resultantly, there is no means for me to advocate to buy MODV at 7.8x forward, no matter how large the discount (it's 60% to the sector as I write). When looking at the company's economic characteristics, in my view, the discount is warranted, and doesn't represent a mispricing.

In that vein, a neutral viewpoint is supported, in line with my previous estimates. Despite the many changes discussed here, we arrive at the same starting point- hence why these points needed to be discussed in the first place. You need a gauge of what the investment updates mean, and what it means for the company (and its equity stock) going forward. Subsequently, I reiterate MODV as a hold, and no price above $45/share would be enough to get me interested, based on the valuation calculus outlined earlier. Reiterate hold.

Appendix 1. MODV revised forward estimates.

Note: In all instances, rolling TTM figures are shown, representing the last 12 months up until the end of each respective forecast period. (Data: Author)

{kind=link}

For further details see:

ModivCare: Earnings Power, Asset Factors A Major Headwind To Bullish Re-Rating