MODV - ModivCare: ROIC And Continuing Value Are Narrowing - Rating It A Hold

Summary

- Here we took a hard-data approach to examine the investment and continuing value for ModivCare, Inc.

- We note the company displays a loose affinity to the kind of equity premia we are chasing exposure to.

- Return on investment and bottom-line earnings have tightened in recent periods for MODV – an unhealthy combo.

- We see that shares are overpriced even at 0.75x book value and demonstrate there's a lack of compelling value on offer.

- We rate MODV a hold on a $103 valuation.

Investment summary

An understanding of a company's value proposition is paramount in making the most informed investment decisions. It is our philosophy to separate measures of corporate value into two segments - investment and earnings - to gauge exactly what we're buying, what's on offer, and if it's worth the cost. Here we examined ModivCare Inc. ( MODV ) in this same light and found there to be a lack of compelling value on offer. AS FCF yields and return on investment have dwindled in recent periods, and forward-looking estimates narrowing as well, valuations are no longer supportive of the long-term buy thesis. We rate MODV a hold on a $103 valuation.

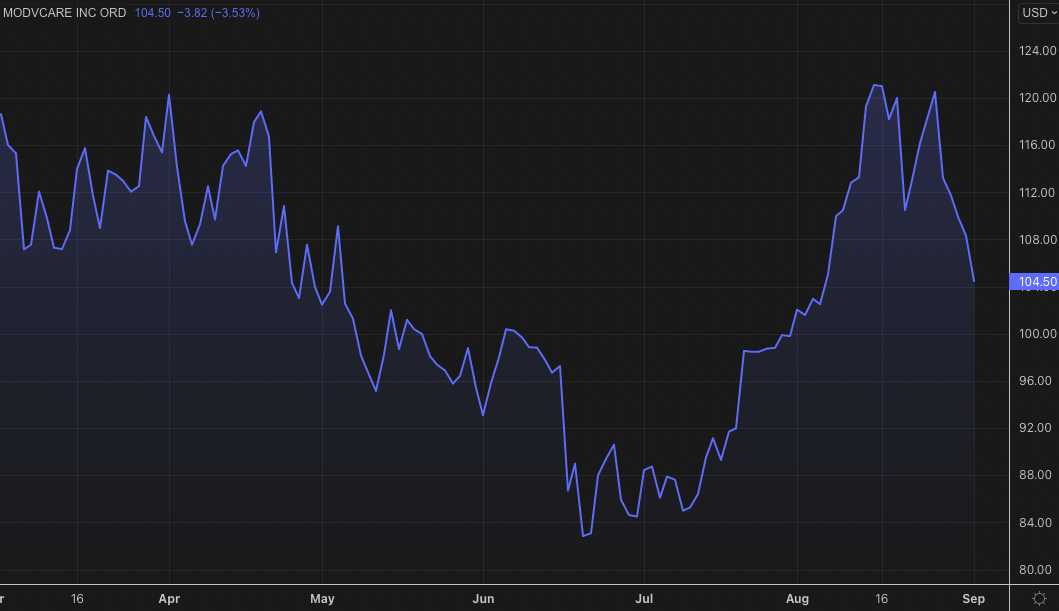

Exhibit 1. MODV 6-month price action

MODV has participated in the June relief rally but blown off the peal with a double-top that saw shares rejected at the c.$120-$122 mark.

{kind=link}

Whilst revenues climb, FCF yield has dwindled

Quarterly operating revenues have continued to bulk up since FY19 on a sequential basis, as seen in Exhibit 2. For instance, Q2 FY22 service revenue came in at $628 million ["mm'] for the year, a year-on-year growth schedule of 32%. The non-emergency medical transportation ("NEMT") segment gained 23% YoY and contributed $449mm to the top line. Growth was underscored by a more favourable revenue mix. This comprised a ~14% YoY gain in average monthly members, a ~500bps increase in revenue per trip and an 18% increase in trip volume. Meanwhile, personal care turnover was $163mm for the quarter and saw growth from $110 the year prior. Upside was driven by an additional ~$42.5mm in incremental revenue from the CareFinders acquisition.

However, despite the upsides at the top-line, this hasn't carried through to the P&L on a GAAP or non-GAAP basis. We note that FCF margin has been thinning since FY20, after a large change in net working capital [discussed below] alongside operating margin. Hence, the spread between top/bottom line is widening for MODV, and this weakens the fundamental momentum looking ahead. Note, investors currently realize a 3.4% FCF yield, in-line with FY19 levels but at a FY22 market capitalization.

Exhibit 2. Thinning FCF margins and yield since FY20 on a sequential basis

Data: HB Insights, MODV SEC Filings

Keep in mind that the narrowing FCF margin/conversion would be preferred if the return on investment comfortably beat the WACC hurdle, and, if there is adequate capital available. Firstly, short-term obligations are poorly covered from liquid assets and cash at just 0.7x cover. Moreover, cash & equivalents has also narrowed from $290mm-$88mm in the last quarter. There may, therefore, be some drain and pull on liquidity with these measures.

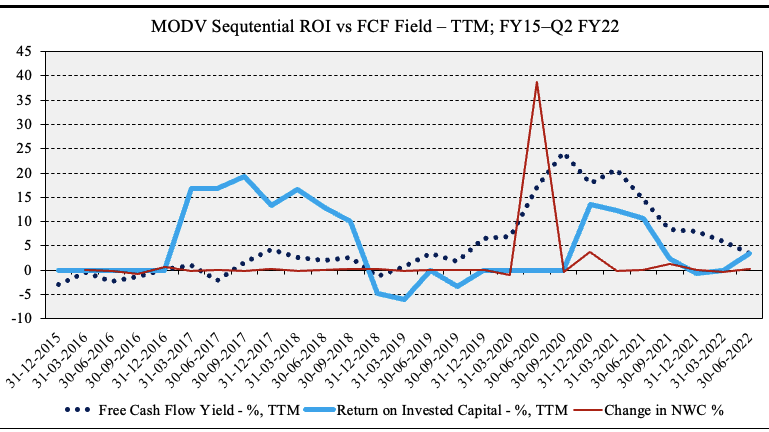

As seen in Exhibit 3, MODV's trailing 12-month ("TTM") FCF yield [a measure of corporate and shareholder value] has closely tracked its return on investment ("ROIC") on a sequential basis since FY18. As such, both have been declining since FY20, and therefore profitability is a concern for the company with this data in mind.

Exhibit 3.

Data: HB Insights

Explaining the jump in FY18-FY19, is 367% QoQ change in net working capital ("NWC") in Q3-Q4 FY20. This saw net working capital [including cash] jump from $141mm to $674mm in one reporting period. Note, that a positive change in NWC generally equates to less FCF, and this is reflected precisely in Exhibit 4. Note that, following the large spike in NWC, both ROIC and FCF immediately began to reverse course.

As a result, FCF yields and ROIC have continued to narrow on a sequential basis in each period subsequent to this event. Nevertheless, the large change in MODV's net operating assets [short-term accruals] is a key factor that has altered the company's return on capital cycle.

Exhibit 4. FCF yield and return on investment both narrowing since large change in NWC ack in FY20 at the start of the pandemic

Data: HB insights, MODV SEC Filings

{kind=link}

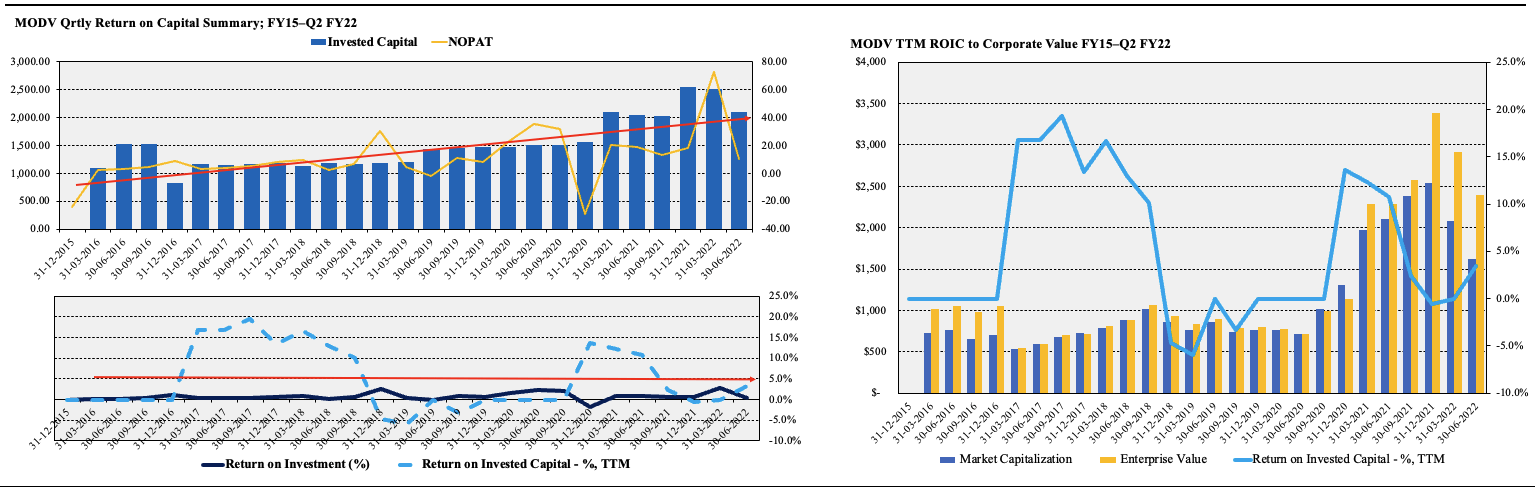

As seen in Exhibit 5, return on investment is now back below pre-pandemic levels, however, we are paying well above pre-pandemic market capitalization [and enterprise value]. Meanwhile, as the level of invested capital has increased over time, net operating profit after tax ("NOPAT") has been bottom heavy and turned course, thus clamping the rate of investment return for MODV.

Exhibit 5. ROIC print is back at FY19 actuals although we are paying FY22 market capitalization

Data: HB Insights, MODV SEC Filings

{kind=link}

Valuation

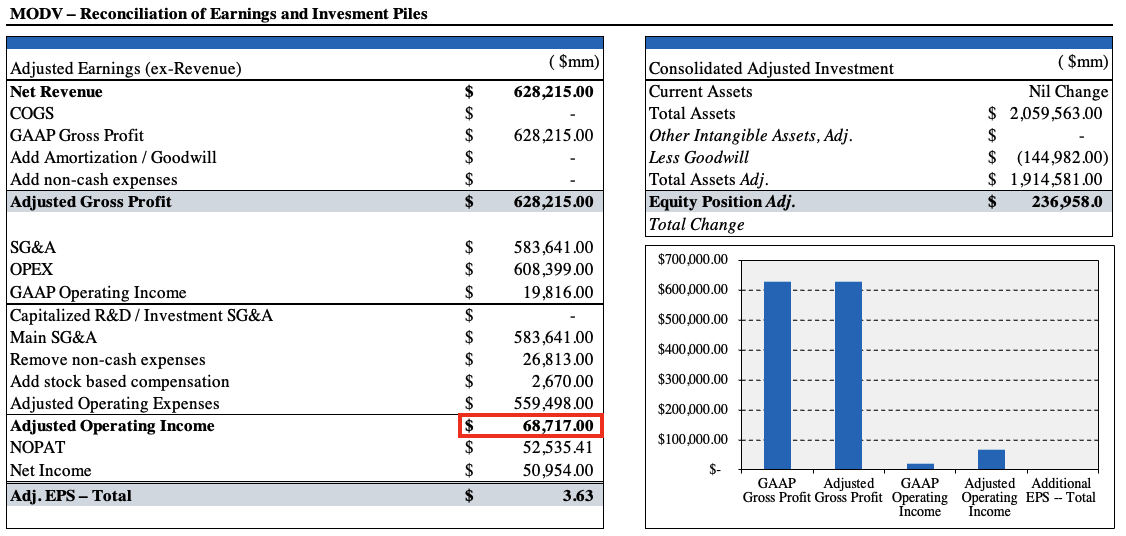

In order to extract a figure of true corporate value, we first must reconcile a few items on the income statement and balance sheet. Goodwill in particular is of note. It arises due to the acquisition method of accounting, that is highly subjective. For instance, in its 10-Q , regarding the acquisition of CareFinders, the company notes re the $236.7mm goodwill asset on the transaction as follows:

"The acquisition preliminarily resulted in $232.2 million of goodwill as a result of expected synergies due to future customers driven by expansion into different markets, an increase in market share, and a growing demographic that will need home care solutions. All of the acquired goodwill is deductible for tax purposes."

Hence we adjust for $1.44 Billion of goodwill on the balance sheet and arrive at an adjusted shareholder equity of $236.9mm, down from a reported $381.9mm.

That's the investment pile of MODV's valuation sorted. For earnings, we had to reconcile ~$30mm in non-cash expenses and stock based compensation and see it print $68mm in operating income and $52mm in NOPAT [$3.71 per share]. This resulted in an adjusted net income of ~$51mm and adjusted earnings of $3.63 per share - up from $0.20 reported. As seen in Exhibit 6, the reconciliations help earnings performance drastically.

Exhibit 6. Reconciliation of GAAP measures - note, shareholder equity includes all recognized intangibles.

Data: HB Investments US Equity Fund

{kind=link}

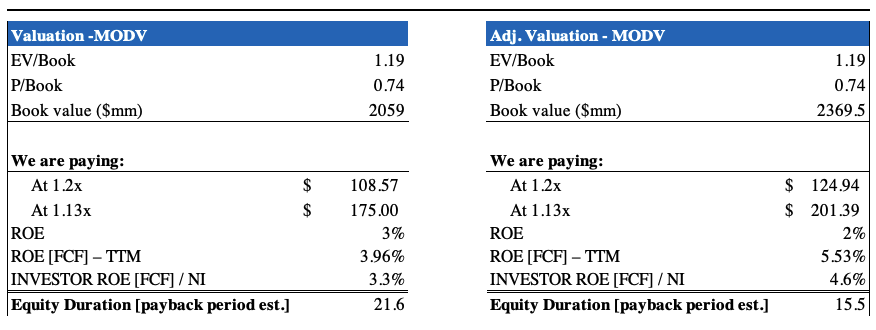

On these figures shares trade at 1.2 enterprise value ("EV) to book value, and ~0.75x price to book. On first glance, this represents compelling value. But does it? When we adjust for the above, at these multiples, we'd be paying an exorbitant $201 per share, and $124 even at 0.74x book value. Moreover, investor ROE is unattractive with a payback period of 15-21 years from current levels of FCF. Question is, is it worth paying an implied $124-$201 for what's on offer earnings wise?

Exhibit 7.

Data: HB Investments US Equity Fund

{kind=link}

After examining this in the valuation model below, that seeks to cover a breadth of sentiment and inputs, shares are valued at $127. On this basis, paying 1.2x EV/book value is very unattractive - paying $201 to get $125. Even at market cap multiples of 0.74x this is unattractive. Interestingly, at a cost of equity of 10.7%, the stock looks expensively priced on a forward-looking basis. Things even out when looking at trailing earnings. Alas, blending all three sees the stock priced fairly at $123.

Exhibit 8. We also note the market rejected MODV 2x at ~$120-$122 in a double top chart pattern that's seen in Exhibit 1.

Data: HB Insights

Depending on how one looks at this, there could be value. We are asked to pay an implied $124-$201 in value after adjustments, only to receive a stock that's worth $123 based on forward earnings [38% downside]. But, we'd be actually paying $104.50 [current market price] to receive this amount - again, it depends on one's framework.

Moreover, at price to book multiples, we'd be receiving 81bps to the upside based on differential in $124.94 in implied price to $123 in implied value. Pricing this differential this to the current MODV share price values it at $103.60.

We believe the stock doesn't present with compelling upside capture at this point as we use the book value to gauge the company's investment value, and adjusted earnings to gauge continuing value. We see MODV is reducing ROIC and FCF yield and looks asymmetrically priced to the downside. This in mind, we rate MODV a hold with a $103.60 valuation.

For further details see:

ModivCare: ROIC And Continuing Value Are Narrowing - Rating It A Hold