ASAN - monday.com: Great Upside Driven By Higher Enterprise Adoption And Expanding Margins

2023-12-29 14:36:49 ET

Summary

- The stock of monday.com has climbed 55% YTD and shows signs of enduring growth, driven by robust product developments and increasing enterprise customers.

- monday.com has a large and growing addressable market, with a projected revenue growth of 39% in 2023 and 28% in 2024, as the company turns profitable on a non-GAAP basis.

- The company's multi-product strategy, strong net dollar retention rate, and efforts to win more enterprise customers contribute to its bullish case.

Editor's note: Seeking Alpha is proud to welcome Amrita Roy as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Introduction and Investment Thesis

monday.com (MNDY) is an enterprise productivity cloud software company that has demonstrated signs of enduring growth driven by a robust set of product developments in the productivity software suite, an increase in the share of enterprise customers with a net dollar-based retention rate of 110%, and improving profitability as management remains laser-focused on operational efficiency. The stock is up 55% YTD, outperforming both the S&P 500 and the Nasdaq 100.

Based on my quantitative and qualitative analysis of Monday, I believe Monday stock has an upside of at least 20% from current levels with a price target of $230. The company operates in a large and growing addressable market with a robust product portfolio that can clearly penetrate further to gain more market share. On top of that, the management's disciplined approach to boosting operational efficiency, coupled with a favorable macroeconomic backdrop, lays out the required foundation for the company to continue to grow profitably while boosting investor confidence.

About Monday

Monday is best known for providing cloud solutions for work management and enterprise collaboration. The company's multi-product enterprise solutions have grown in popularity, especially amongst enterprise customers, earning Monday consistent leadership recognition as Gartner's Magic Quadrant™ Leader for Collaborative Work Management .

Monday offers its customers enterprise solutions via three product verticals:

-

Monday Work Management: to build and manage enterprise project workflows for the general organization

-

Monday Sales CRM: manage upmarket customer relationships for enterprise clients

-

Monday Dev: Primarily product development software to optimize application development and IT Service management workflows

In addition, Monday recently launched its Monday AI Assistant to assist teams in building their workflows in the enterprise cloud.

The company uses a combination of subscription-based pricing and seat-based pricing to charge its customers for access to its workplace productivity suite of cloud solutions. In my view, this combination of per-period subscription and per-seat pricing is more advantageous to Monday since the company is still experiencing growth in its large clients that contribute $50,000 or more to Monday's Annual Recurring Revenue ((ARR)).

Building the bull case for Monday

Monday posted 38% YoY revenue growth in Q3 2023. Meanwhile, it also improved its gross margin from 86% a year ago to 88% in Q3 2023, and at the same time, it significantly reduced its operating loss by 90% on a YoY basis. The company is projected to grow its revenue by 39% in 2023, as per management's guidance, (and by 28% in 2024 as per consensus estimates). Management also expects the company to turn profitable on a non-GAAP basis, growing its earnings by 300% in 2023 and then by 20% in 2024.

While the company's financial performance is indicative of the underlying strength in the company's overall strategy and execution, I will now lay forth my arguments for why I believe there is a long-term investment case for Monday.

Monday has a large TAM. It's still growing.

As per its latest Investor Day , Monday's total addressable market is expected to grow from $101B in 2023 to $150B in 2026, which represents a compounded annual growth rate of 14%. The total addressable market size is calculated by summing the sizes of the following markets, which correspond to the most common use cases on the platform: Project and Portfolio management ($45B TAM), Sales force productivity and management ($30B), application development ($17B) and IT service management ($9B).

Since Monday serves different verticals, I think the company should be able to grow its market opportunity rapidly over the coming years as the company ramps up product innovation into more verticals over time.

During this period of time, I expect Monday to grow its revenue between 25%-28%, which will then allow it to gain market share from 0.7% in 2023 to 1.1% by 2026. This will take place as long as management stays focused on driving robust product innovation across its platform for its new and existing set of customers. And so far, the strategy is playing out well, as can be seen below.

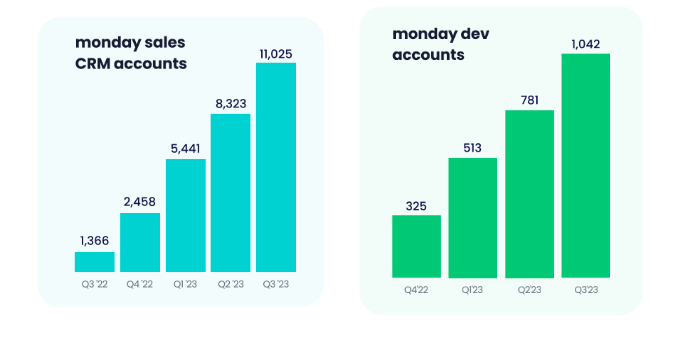

A Multiproduct strategy that promises to accelerate revenue growth through cross-sell and upsell opportunities in the existing customer cohort.

As per the latest Q3 earnings, Monday's new products, specifically Monday Sales CRM and Monday Dev continue to show remarkable cross-sell opportunities, having grown 32% and 33% on a quarter-over-quarter basis. It is important to note that while Monday Sales CRM and Monday Dev are currently open to a selection of existing customers, they will be rolled out to all customers by the end of Q1 2024.

{kind=link}

Currently, just about 33% of Monday's customers will have used Monday Sales CRM or Monday Dev in 2023. This means that as Monday rolls out the products to all customers by Q1 2024, there is going to be a sizable boost from upselling as renewals come due.

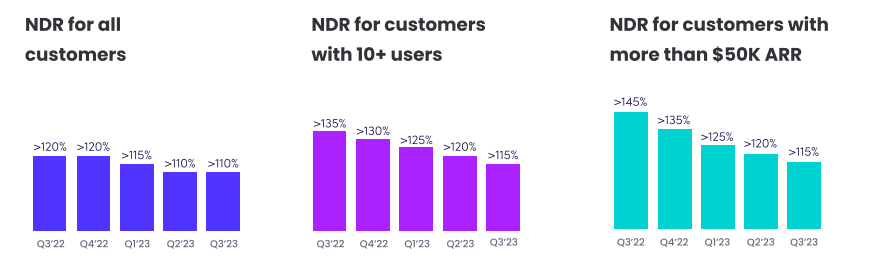

As Monday builds out its multi-product strategy, one of the key metrics I will be looking at is the net dollar retention rate, which tells me whether the company is generating more additional revenue from upsells, cross-sells, or expansion within existing customer accounts. The current net dollar retention rate for Monday stands at 110% for all customers and is above 115% for enterprise customers with $50,000+ in ARR. This is an indication that the multi-product strategy is working, in my opinion, as large customers adopt more of Monday's products, thus laying the foundation for revenue expansion down the line. However, I would like to point out that the net dollar retention rate has fallen on a YoY period, as it was >120% for all customers a year ago and >135% for customers with more than $50k in ARR.

Increasingly sharp focus on improving operational efficiency and profitability

Monday has an impressive balance sheet, with a solid cash position of $1.05B and very little debt on its balance sheet. Furthermore, the management expects the company to turn profitable on a non-GAAP basis in 2023, with earnings per share of $1.53. Plus, I believe that the current state of its cash position enables the company to invest strategically in growth initiatives, such as Artificial Intelligence, in order to best position itself relative to its competition. Monday recently launched its Monday AI Assistant, which is designed to build project workflows for Monday's enterprise customers in the cloud. I see a huge opportunity for greater lateral adoption of Monday's products, driven by its AI Assistant, that will be rolled out to all customers next year.

Looking at operating margins, Q3 non-GAAP operating margin came in at 13%, which improved by 4% points on a sequential basis. One of the biggest drivers for the improvement in operating margin has been the drop in the overall share of Sales and Marketing expenses as a percentage of revenue. In Q3 2022, Sales and marketing expenses accounted for 60% of revenue, while in Q3 2023, it dropped to 54% of revenue.

FY 2023 Q3 Shareholder Letter

In other words, the company is becoming more efficient, as it can drive incrementally higher revenue with less sales and marketing spend. At the same time, R&D expenses as a percentage of total revenue also dropped from 19% in Q3 2022 to 15% in Q3 2023, which contributed to boosting the overall operating margin. Moving forward, the management expects R&D as a percentage of revenue to be in the high teens as they build out their product suite and scale the WorkOS platform both horizontally and vertically.

Overall improving macroeconomic conditions will bolster worldwide IT spending growth in 2024

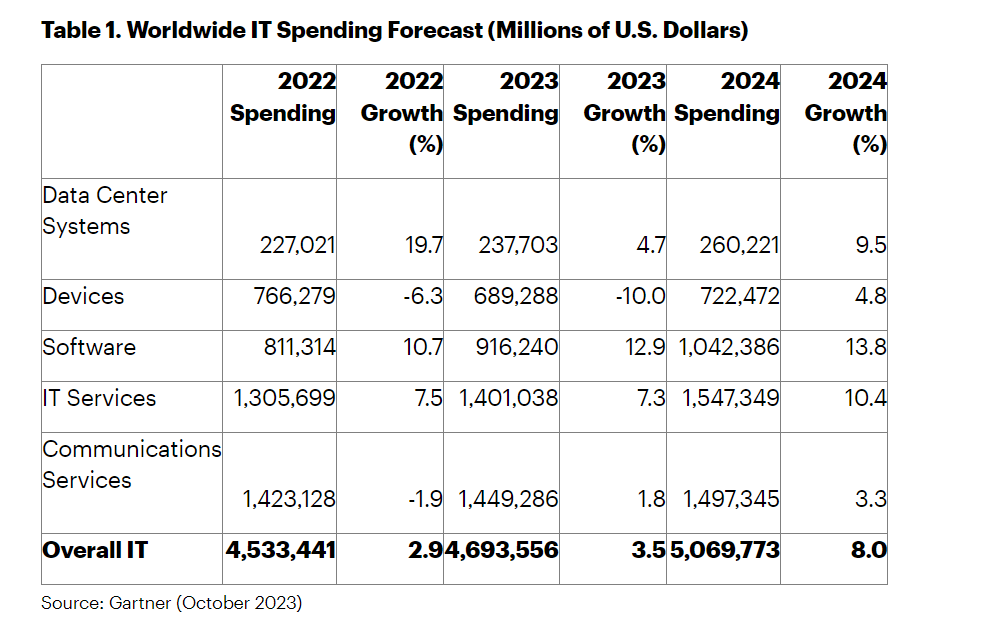

While 2022 and 2023 were tough for companies as management tried to cut back spending and optimize cost structures as the Federal Reserve embarked on one of the toughest interest rate hiking cycles, broad economic indicators point to inflation trending lower from current levels. As a result, the Federal Reserve will most likely start to lower rates as soon as March 2024 in order to ensure that the US economy does not tip into a recession. Meanwhile, the software and IT services segments will see double-digit growth in 2024, largely driven by cloud spending at 13.8% and 10.4%, respectively, as per Gartner . This should bode well for the overall macro narrative for Monday in 2024.

{kind=link}

The bear case for monday.com

So far, we have seen that the company's multi-product strategy, along with its robust financial discipline, has enabled the stock to climb back up from its lowest price of $73 in November 2022 to $189 in December 2023 (as of this writing), thus climbing 158% from an all-time low and 55% YTD. While there are quite a few tailwinds that can continue to push the stock to climb higher, I am also listing some potential threats to the bull case.

Monday may be risking long-term product innovation by cutting R&D spend to optimize operating margins in the short term

In the earlier section, we saw that Monday was improving its overall margin by optimizing its spend on Sales & Marketing and R&D. While I am not too concerned about optimizing spend on Sales & Marketing to improve operational efficiency, I am cautious about the long term threat of curtailing too much spend on R&D to lose market share to competitors. Monday's competitors Atlassian (TEAM), Asana (ASAN), and Smartsheet (SMAR) have R&D spends of 50%, 48%, and 23% of revenue, much higher than Monday's R&D spend, currently at 15% of revenue. While in the short term, it can lead to higher operating margins, the rapidly evolving landscape, especially pertaining to integrating AI within the enterprise tech stack, is critical for Monday to stay ahead of the curve. If it fails to do so in the long term, short-term investor confidence may soon fizzle out.

Net Dollar Retention rate is slowing down

While net dollar retention is still strong at 110% for all customers and over 115% for customers with more than $50,000 in ARR, I can observe slowdowns in the Net Dollar Retention. A year ago, overall net retention was 120% for all customers, 10% higher than today. But, most importantly, the dollar retention for customers with more than $50K ARR was 145%. This is indicative, that while existing customers are still excited about new product launches, there is a growing spend fatigue amongst them. Moving forward, should we see further deterioration in net dollar retention, it would be a very clear indication that Monday's ability to retain its customers' enterprise spend is falling behind.

{kind=link}

Tying it all together - I believe there is a 21% upside from current levels

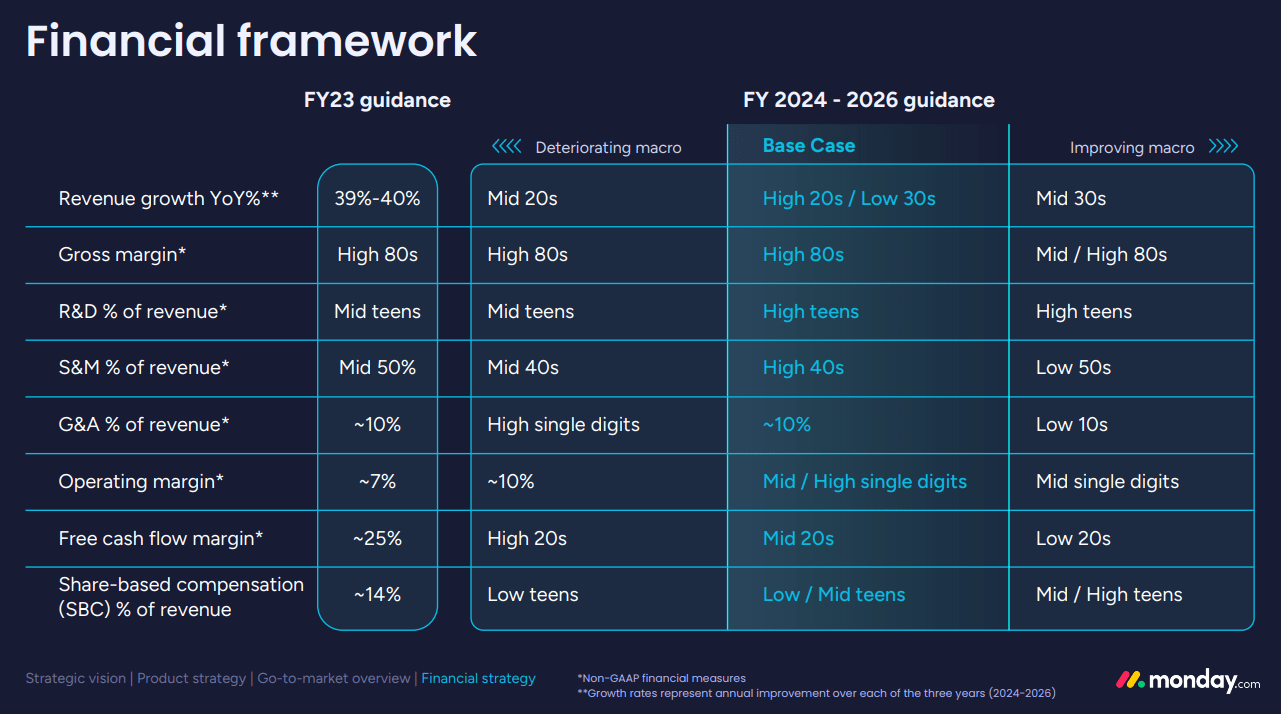

In 2023, Monday is expected to turn profitable on a non-GAAP basis. Moving forward, if I take management's base case scenario from its Analyst day, it expects a non-GAAP operating margin of mid- to high-single-digits between 2024 and 2026. Therefore, assuming that the non-GAAP operating margin grows to 7.5% in 2024, driven by efficiency in streamlining Sales and Marketing Spend, and revenue grows 27% as per consensus estimates, non-GAAP operating income should grow approximately 20% on a YoY basis. This would translate to adjusted earnings per share of approximately $1.8. This would mean that Monday is currently trading at a forward price-to-earnings ratio of 102. This may seem expensive at first. However, since Monday is a growth stock, it wouldn't be fair to base my investment decision simply on my outlook for the next year.

Instead, my preferred method would be to look at a 10-year horizon so that I can build a more meaningful set of assumptions that will enable me to assess if the stock is overvalued, undervalued, or fairly valued.

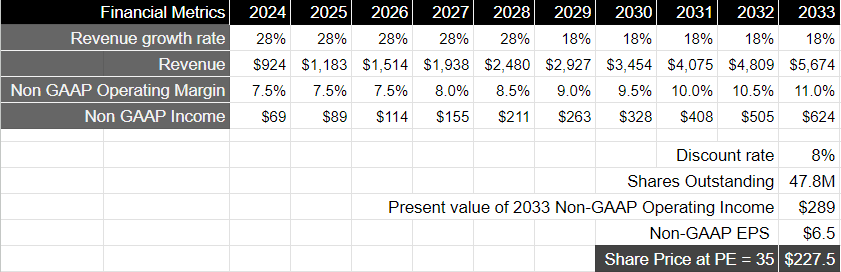

Therefore, looking at a 10-year investment horizon, my expectation is that revenue growth will remain at the mid-20s level for the next 5 years until 2028, after which it will slow to 18% over the following 5 years through 2033. During this period of time, Monday should be producing a total revenue of approximately $5.5B by the end of 2033. I believe that most of the revenue growth will be driven by Monday's robust product innovations, higher penetration in the enterprise customer segment, and a steady net dollar retention rate of 110%. I would also like to point out that while the management expects a non-GAAP operating margin of mid- to high-single-digits into 2026 in its base case, I believe that over a 10-year investment horizon, we will continue to see further margin improvement as the company streamlines its operating expenses to drive higher efficiency.

2023 Investor Day Presentation

{kind=link}

In my valuation model below, I have assumed that the non-GAAP operating margin will grow to 10-11% by the end of 2033. That would mean that Monday produces approximately $650M in non-GAAP operating income by the end of 2033, which would equate to a present value of $315M if discounted at 8%, or adjusted earnings per share of $7.

Taking the above assumptions into consideration, I believe that the price-to-earnings ratio for Monday in 2033 will be around 30-35. I will explain below why I think a price-to-earnings multiple of 30-35 is fair for Monday, using the S&P 500 as a proxy.

If the S&P 500 continues to grow its earnings at an average pace of 8% into 2033, as per its 10-year average, estimated by FactSet , and the US economy grows at a Real GDP of 1.5-1.8% , coupled with inflation normalizing to the Federal Reserve's long term target of 2.2-2.5%, the 10-year US Treasury bond yield should be anchored around 4%. In that case, the price-to-earnings ratio for the S&P 500 will be around 15-18, given historical averages, overall market sentiment, and risk appetite.

Since I expect Monday to grow its earnings at more than twice the rate of the S&P 500 over the next 10 years, Monday should fetch a price-to-earnings multiple that is at least twice that of the S&P 500. Therefore, Monday should be trading at a price-to-earnings multiple of 30-35 in 2033, which would mean that its stock can climb another 21% to reach $230 from its current levels.

{kind=link}

Conclusion

While Monday's valuation may initially look expensive to some investors, I think it is quite the contrary. Given the current price point of the stock, it can continue to climb higher in the coming year(s) as the company executes its long-term vision with a highly robust product portfolio and well-designed growth strategies to expand upmarket and across geographies while maintaining a healthy balance sheet and improving overall profitability. As an investor, I will be watching the overall competitive landscape and monitoring the net dollar retention rate for Monday to see if there has been any shift in the bull narrative. I am impressed so far by the management's execution in a complicated macroeconomic environment and expect it to continue delivering in the coming quarters and years, which would translate to the stock having an upside of 21% from current levels to a price target of $230.

For further details see:

monday.com: Great Upside Driven By Higher Enterprise Adoption And Expanding Margins