PCH - Money Doesn't Grow On Trees Unless It's A Timber REIT

2023-07-02 07:00:00 ET

Summary

- The housing market is a big driver of lumber prices, making timberland REITs another way to invest in the housing sector.

- One of the biggest demand drivers for the timber sector is a growing population, which makes sense because housing is the leading purchaser of lumber.

- When the blue lights start flashing, I may become a buyer of the Timber REITs.

It’s been a while since I looked at Timber REITs, an often-misunderstood sector of the real estate universe that generates income from the production, harvest, and sale of timber.

Some Timber REITs sell the raw timber they produce, while others own mills and sell refined lumber products.

In many cases, these timber REITs also earn income from mineral rights, oil and gas deposits, and leasing their properties to third parties.

What’s unique with this sector is the correlation to the price of commodities, which makes them especially cyclical. The housing market is a big driver of lumber prices, making timberland REITs another way to invest in the housing sector.

However, timber, unlike many other markets, doesn’t require moving commodities quickly because trees can be standing, then harvested at the best times when market demand is high. In addition, there are no associated costs for warehousing or other kinds of storage.

One of the biggest demand drivers for the timber sector is a growing population, which makes sense because housing is the leading purchaser of lumber.

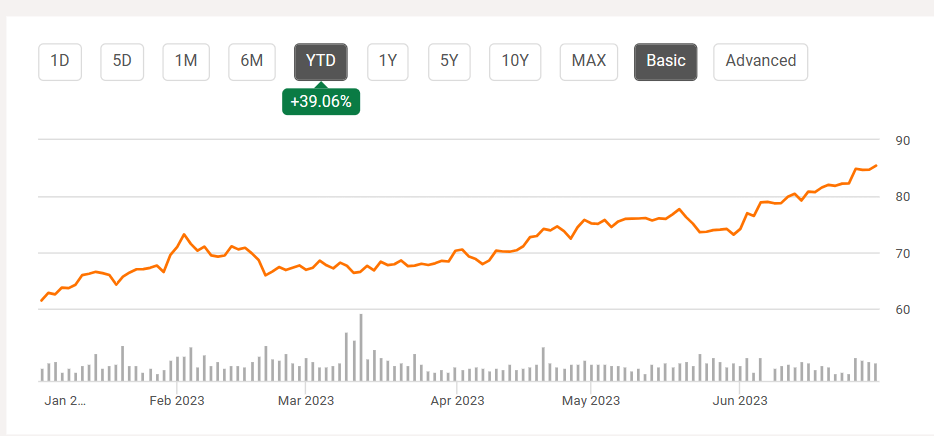

The demand in new housing (and lumber) is a key driver which can be best viewed by looking at the iShares U.S. Home Construction ETF ( ITB ) – up 39.1% YTD.

{kind=link}

ITB is the largest home construction-focused ETF, with around $2 billion in AUM and 67% of its assets are invested in homebuilders. As Leo Nelissen pointed out “ it's not a pure-play homebuilding ETF, but it comes very close .”

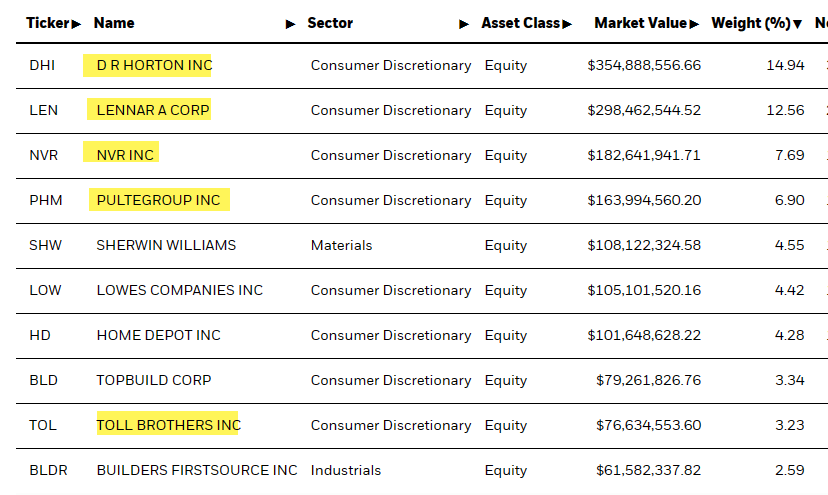

As viewed below, IBD has 5 homebuilders in its “top 10” list including ( DHI ), ( LEN ), ( NVR ), ( PHM ), and ( TOL ) – that’s 45.32% exposure.

{kind=link}

I happen to own Toll Brothers ((TOL)) – up over 71% since purchasing - and is the only homebuilder in my retirement portfolio. In addition, I own Lowe’s ( LOW ) – see my recent article – which is up 28% since I bought shares.

Collectively, my exposure is around 4% (with these two tickers) that have generated an average return of 40%. Alternatively, the three Timber REITs that I’ll be discussing today have returned an average of 8% YTD.

So, with further ado, let’s take a look at the Timber REITs…

PotlatchDeltic Corp ( PCH )

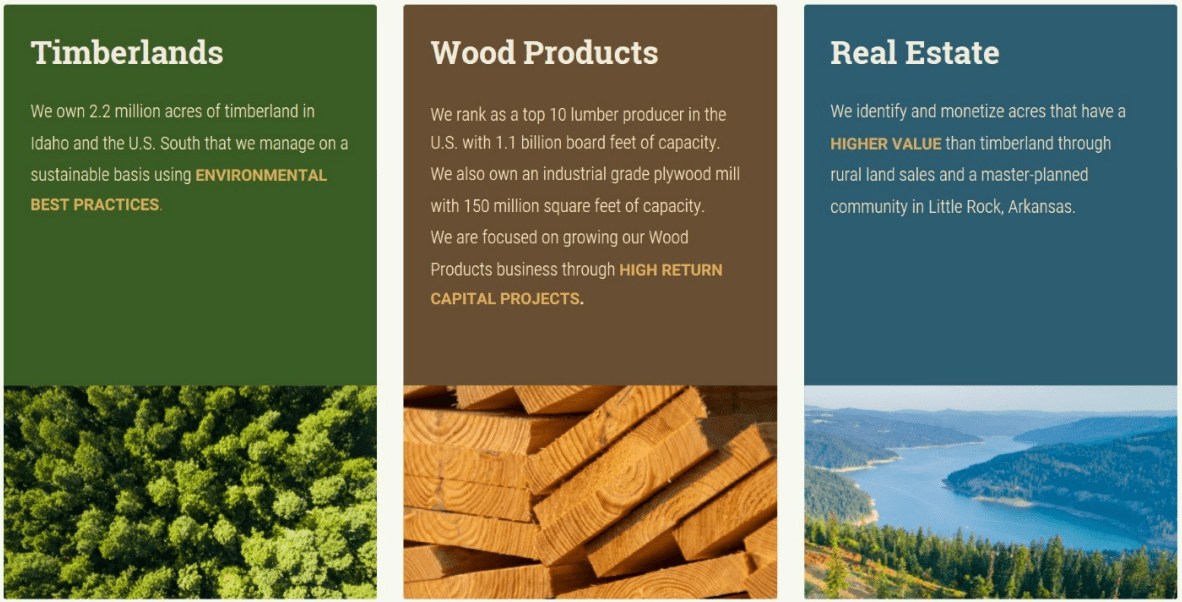

PotlatchDeltic is a timber real estate investment trust (“REIT”) that conducts operations in 9 states and owns approximately 2.2 million acres of timberland in 7 of those states. The timberlands in their portfolio are used to grow and harvest trees which are then converted into wood products and sold to 3 rd parties.

PCH is vertically integrated with 6 sawmills and 1 plywood mill that they use to convert timber into lumber and plywood. Additionally, PCH is a top 10 lumber producer in the U.S. and has 1.1 billion board feet capacity.

In addition to the wood products they sell, PCH also conducts business through their real estate segment which monetizes acres through rural land sales when they deem the land sold for development is worth more than the existing timberland.

The company was formally known as Potlatch Holdings and was incorporated in 2005 as a REIT. In 2018 PCH merged with Deltic Timber Corp and changed its name to PotlatchDeltic Corp.

{kind=link}

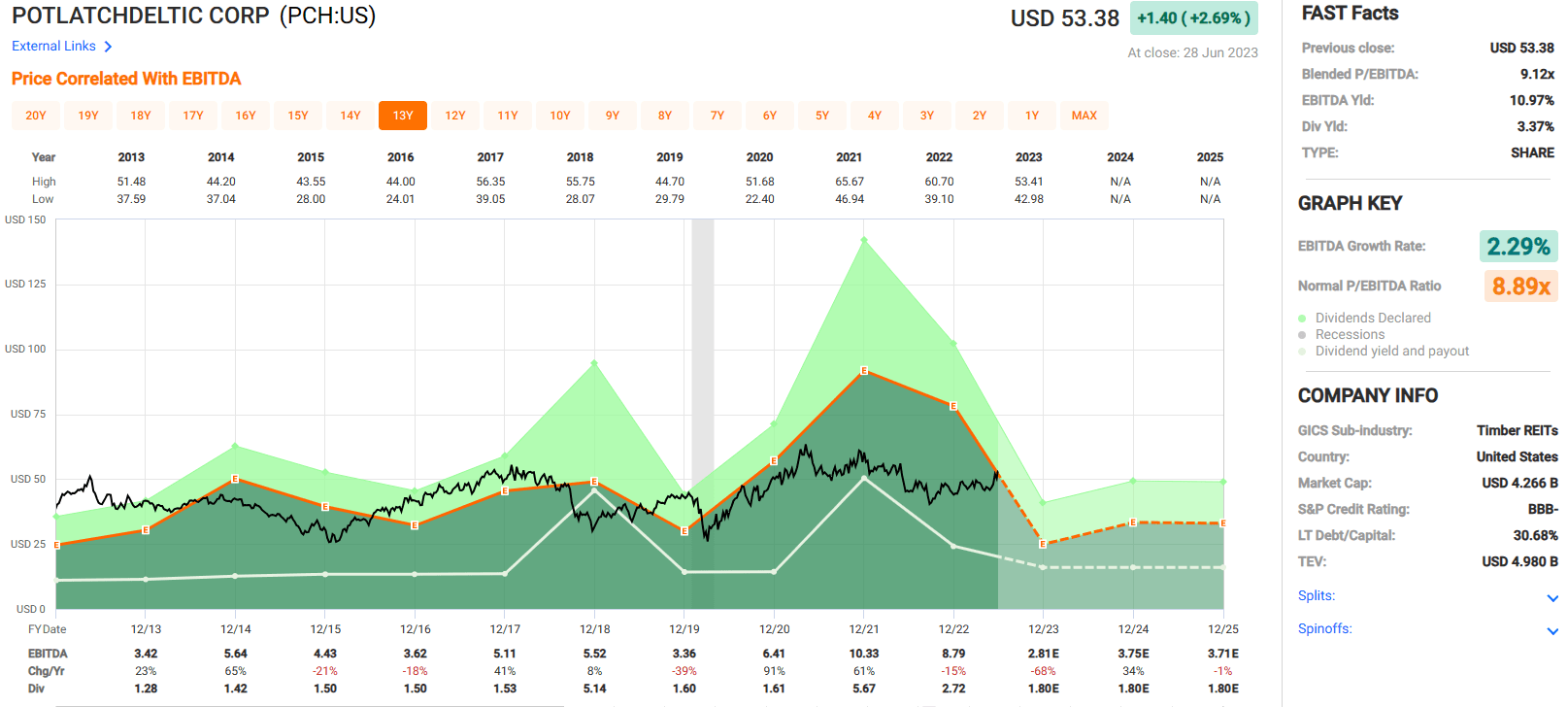

PotlatchDeltic is investment grade with a BBB- credit rating and has strong debt metrics including an adjusted EBITDA leverage ratio of 1.8x, a long-term debt to capital of 30.68%, and a net debt to enterprise value ratio of 15.2%.

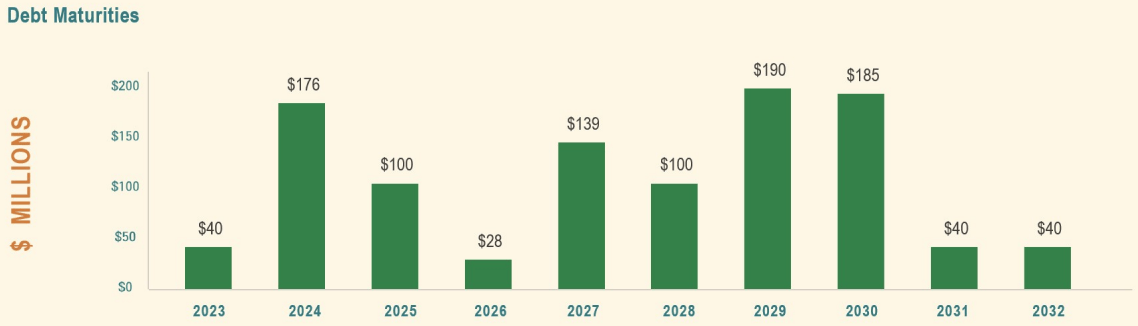

Their debt is 100% fixed rate, and their weighted average cost of debt is 2.4%. Additionally, PCH has $625 million in liquidity with no significant debt maturities until 2024.

{kind=link}

PotlatchDeltic has had earnings before interest, tax, depreciation & amortization (“EBITDA”) growth rate of 2.29% since 2013.

Due in large part to the volatility of lumber prices, PCH’s EBITDA has been very choppy with year-over-year results ranging from a decline of 39% in 2019 to a 91% increase the following year.

In 2022 EBITDA fell by 15% and analysts expect EBITDA to fall by 68% in the current year. Analysts also expect EBITDA to increase by 34% in 2024 and then fall by 1% in 2025.

PCH pays a 3.37% dividend yield and the company has maintained a consistent dividend history (with a few special dividends).

When valuing timber REITs, we look at the strength of the cash flows over time, because this leads to expectations of higher distributions, high values, and higher share prices.

We use EBITDA multiples and as you can see below, the stock currently trades at a Price to EBITDA of 9.12x which is a slight premium to their normal P/EBITDA of 8.89x. Shares have outperformed (+20%) YTD. At iREIT, we rate PotlatchDeltic stock a HOLD.

{kind=link}

Rayonier ( RYN )

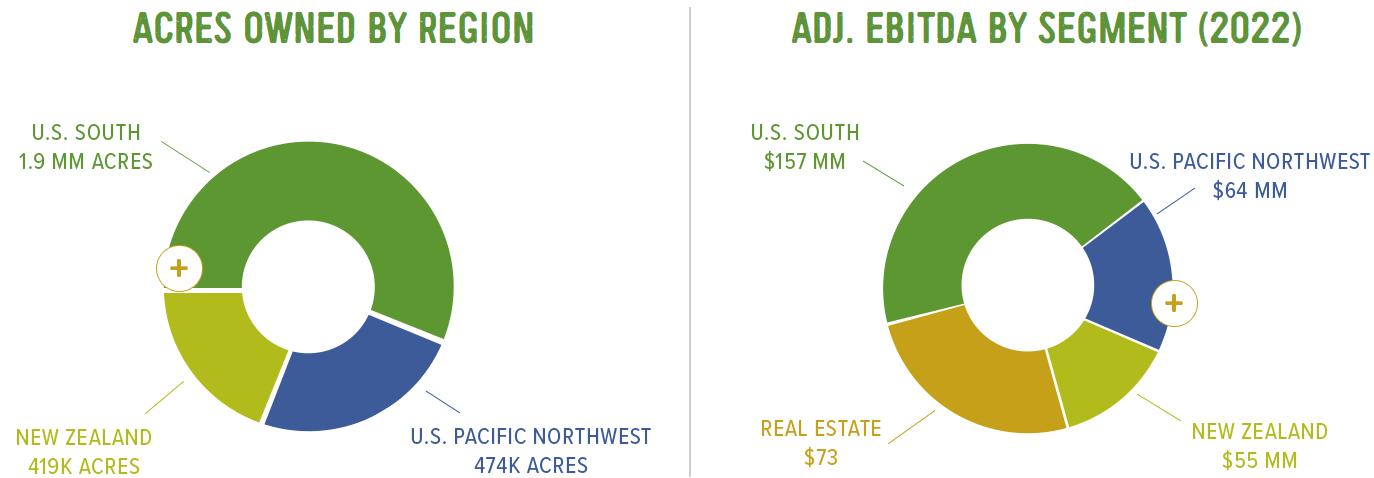

Rayonier is a Timber REIT that owns timberland in the U.S. and New Zealand. They operate through several business segments including Southern Timber, Northwest Timber, New Zealand Timber, Log Trading, and Real Estate.

They own 1.92 million acres of timberland in the U.S. South, 474,000 acres in the U.S. Pacific Northwest, and 419,000 acres in New Zealand. In total their portfolio contains 2.8 million acres of timberland and real estate.

RYN also has a New Zealand export operation in which it engages in trading logs to Pacific Rim markets. Rayonier is a pure-play timberland REIT in that it does not own any manufacturing assets (to convert timber into wood products) and invest exclusively in timberlands. They also monitor and access alternative uses of their timberland in order to monetize land if they feel it is worth more for development than remaining as timberland.

{kind=link}

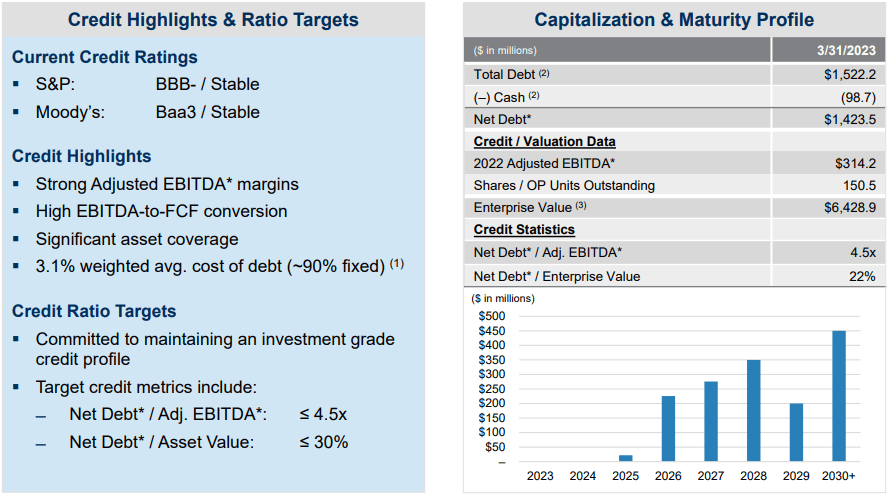

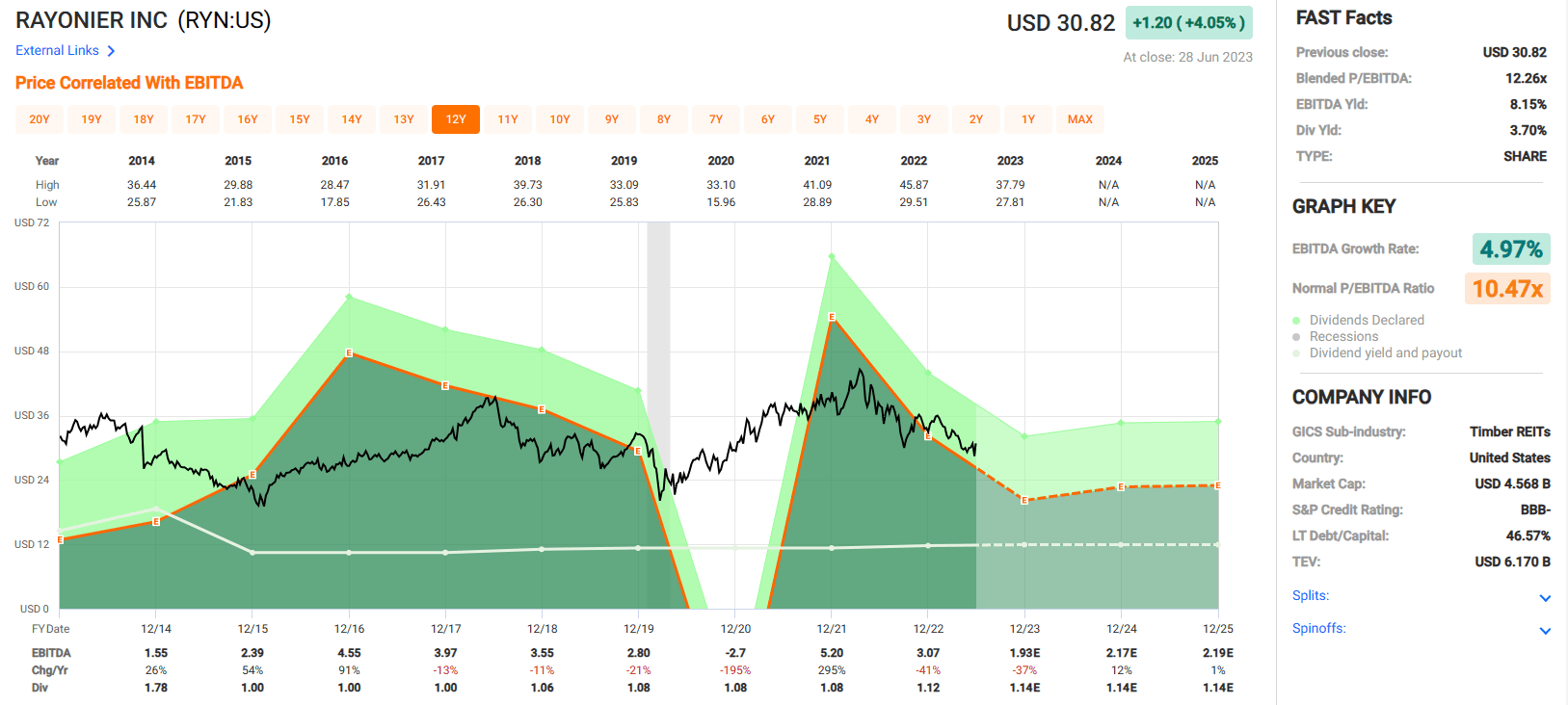

Rayonier has solid debt metrics with a net debt to adjusted EBITDA of 4.5x, a net debt to enterprise value ratio of 22%, and a long-term debt to capital ratio of 46.57%.

Their debt has a weighted average cost of 3.1% and is approximately 90% fixed rate. RYN is investment grade with a BBB- credit rating and has no significant debt maturities until 2026.

{kind=link}

Rayonier’s EBITDA has also been quite volatile with a decrease of 21% and 195% in the years 2019 and 2020, followed by a 295% increase in 2021. EBITDA fell by 41% in 2022 and is expected to fall by 37% in 2023 before rebounding with an expected 12% increase in EBITDA in 2024.

Overall RYN has had an average EBITDA growth rate of 4.97% since 2014. They pay a 3.70% dividend yield that is secure with an EBITDA dividend payout ratio of 36.59% as of the end of 2022.

Currently the stock is trading at a P/EBITDA ratio of 12.26x which is a premium to their normal P/EBITDA of 10.47x. At iREIT, we rate Rayonier stock a HOLD.

{kind=link}

Weyerhaeuser Co ( WY )

Weyerhaeuser is the largest timber REIT with a market capitalization of approximately $24 billion. They own or control 10.6 million acres of timberlands in the United States and manage 14.1 million acres of timberlands in Canada.

In addition to using their land for growing and harvesting timber, they also sell acres of land if they feel it can create more value and also sell royalty agreements for subsurface and surface rights on their land.

Along with being the largest timber REIT, they also operate 35 wood products manufacturing facilities and are one of the largest producers of wood products in North America.

Weyerhaeuser sells wood products that primarily consist of structural lumber, engineered wood products, and oriented strand board to the residential, multifamily and industrial markets.

{kind=link}

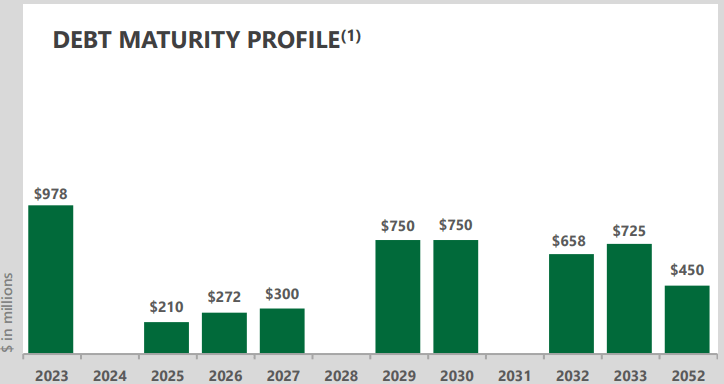

Weyerhaeuser is investment-grade with a BBB credit rating and has excellent debt metrics including a net debt to EBITDA of 1.76x, a long-term debt to capital ratio of 26.92%, and an interest coverage ratio of 9.22%. Their debt is 100% fixed rate and has a weighted average interest rate of 5.4% and a weighted average term to maturity of 8 years.

They do have significant debt maturities in 2023 at $978 million, but they currently have $1.5 billion available to them under their revolving line of credit. There are no debt maturities in 2024 and no other significant maturities until 2029.

{kind=link}

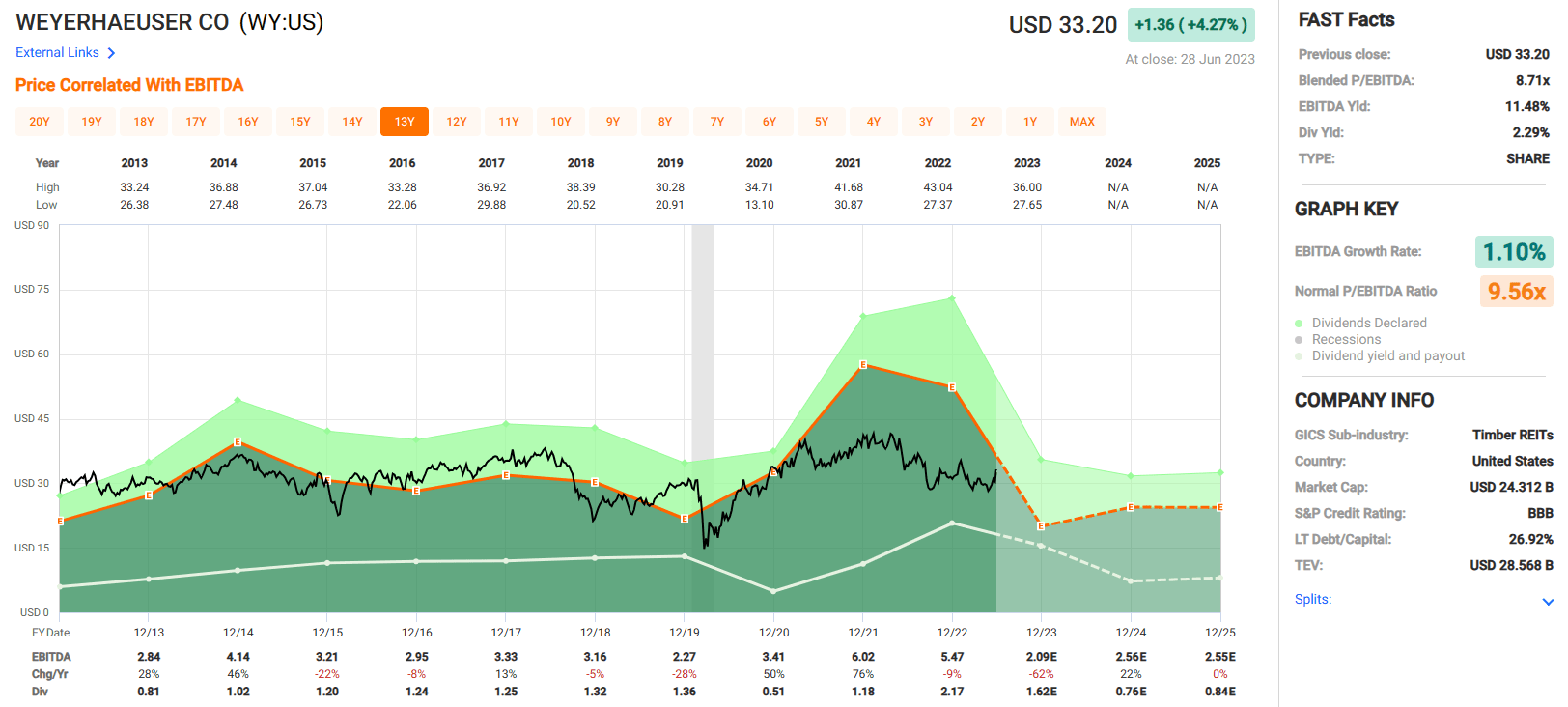

Like the other timber REITs discussed, Weyerhaeuser’s EBITDA has been volatile over the past decade. EBITDA fell by 28% in 2019 but then increased by 50% in 2020 and 76% in 2021. EBITDA fell by 9% in 2022 and is expected to decline by 62% in 2023.

Analysts expect EBITDA to increase by 22% in 2024 and remain flat in 2025. Overall, since 2013 WY has had an average EBITDA annual growth rate of 1.10%. WY pays a 2.29% dividend yield that is well covered with an EBITDA dividend payout ratio of 39.70% as of the end of 2022.

The stock currently trades at a P/EBITDA of 8.71x which is a slight discount to their normal P/EBITDA ratio of 9.56x. At iREIT, we rate Weyerhaeuser stock a HOLD.

{kind=link}

In Closing…

I like the Timber REIT sector, but as a value investor, I see no bargains.

When the blue lights start flashing, I may become a buyer.

{kind=link}

As Leo Nelissen explained,

“If economic growth weakens, unemployment could rise, prompting people to start selling their homes. Once this occurs, the market will be able to correct itself, potentially leading to a significant decline in home prices.

While I won't make a prediction of a Great Financial Crisis-style housing crash in this article, I want to highlight the unfavorable risk/reward of investing in homebuilding stocks and what this could mean for the bigger picture.”

I agree with Leo here, and I prefer to own the other side of that trade, apartment rentals. I will continue to scoop up shares in Mid-America ( MAA ), Camden Property Trust ( CPT ), and Sun Communities ( SUI ).

Another name of loading up on is U-Haul ( UHAL ).

In April I told members at iREIT© on Alpha that this C-Corp. is a high-conviction BUY . Whether folks are moving in new houses or rentals, I like UHAL because it serves every nook and cranny of the residential housing wave…and the company owns or manages around 78 million square of self-storage properties.

Note: UHAL pays no dividend.

In summary, here’s how I’m playing the housing sector…

- Toll Brothers ((TOL))

- Lowe’s ((LOW))

- Mid-America Apartment Communities ((MAA))

- Camden Property Trust ((CPT))

- Essex Property Trust (ESS)

- Sun Communities ((SUI))

- Public Storage ( PSA )

- Extra Space Storage ( EXR )

- National Storage Affiliates Trust ( NSA )

- U-Haul Holding ((UHAL))

I would love to know your picks…

As always, thank you for the opportunity to be of service.

For further details see:

Money Doesn't Grow On Trees, Unless It's A Timber REIT