PECO - Monthly Mailbox Money: The SWAN Edition

Summary

- Today, I want to leave the ugly ducklings and focus on the SWANs and or the SWAN-a-bees.

- In other words, I want to recap some of the safest “sleep well at night” monthly paying REITs and to recap the fundamentals and valuations for each constituent.

- And just to be clear, not all of these monthly payers are SWANs yet, but they are definitely not "ugly ducklings” which is a reason we added them in this.

I recently wrote an article titled, Fool Me Once, Shame On You, Fool Me Twice, Shame On M e , which highlighted a few REITs that cut the cheese (i.e. the dividend).

The point that was trying to make in that article is that I will never make the same mistake I did with the former net lease REIT, American Realty Capital Properties (formerly ARCP) that was forced to cut its dividend after some accounting shenanigans.

While many investors seek stable and predictable income, it seems that so often these very same investors get sucked into the allure of monthly dividend payments and forget about safety.

I certainly don’t want you to go down that rabbit hole, just like so many of us did with American Realty Capital Properties. That’s why I insist on writing about ugly ducklings like Gladstone Commercial ( GOOD ), Global Net Lease ( GNL ), Necessity Retail ( RTL ), and others.

But today I want to leave the ugly ducklings and focus on the SWANs and or the SWAN-a-bees.

In other words, I want to recap some of the safest “sleep well at night” monthly paying REITs and to recap the fundamentals and valuations for each constituent.

And just to be clear, not all of these monthly payers are SWANs yet, but they are definitely not "ugly ducklings” which is a reason we added them in this article.

Swan-A-Bee: Apple Hospitality REIT ( APLE )

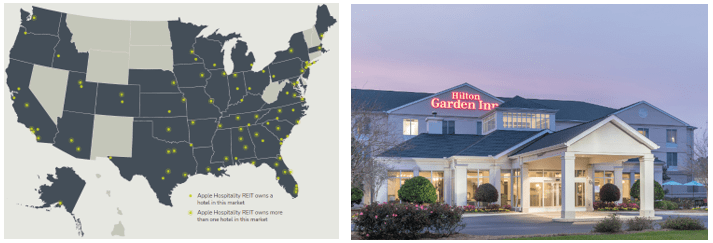

Apple Hospitality is a REIT that owns a diverse portfolio of hotels that are primarily operated under the Marriott and Hilton brands. In all they have 220 hotels with approximately 29,000 rooms that are located in 87 markets throughout 37 states.

Their portfolio consists of 119 Hilton hotels, 96 Marriott hotels, 4 Hyatt hotels, 1 independent hotel and 100% of their properties are operated by third-party property managers. They seek to acquire young assets in markets with strong RevPAR (“revenue per available room”) and focus on select-service hotels operated under leading brands that cater to both businesses and leisure travel.

APLE pays a 5.64% dividend yield and makes monthly distributions. They are a relatively small company with a total market capitalization of 3.89 billion.

{kind=link}

Apple Hospitality and Hotel REITs in general should fare better than average in a high inflationary environment as they can re-rate open rooms on a daily basis. However, the hotel industry as a whole is cyclical and sensitive to economic conditions so if inflation rises to extreme levels, it could limit discretionary spending, including travel for business and to a greater extent for leisure.

Given the current expectations of lingering, but moderate inflation, the hotel industry should be able to maintain their margins even with rising prices so long as it does not materially reduce demand.

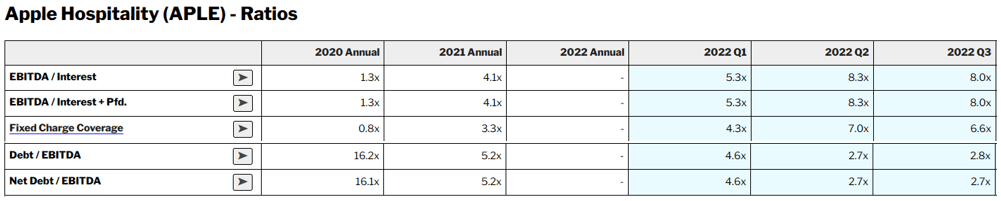

APLE has excellent debt metrics with a Fixed Charge Coverage of 6.6x, a Net Debt to EBITDA of 2.7x, and Net Debt to Total Capitalization of 29%. They have a weighted average interest rate of 3.72% and 87% of their debt is fixed rate as of the third quarter of 2022.

APLE - 3Q22 Form 10-Q

{kind=link}

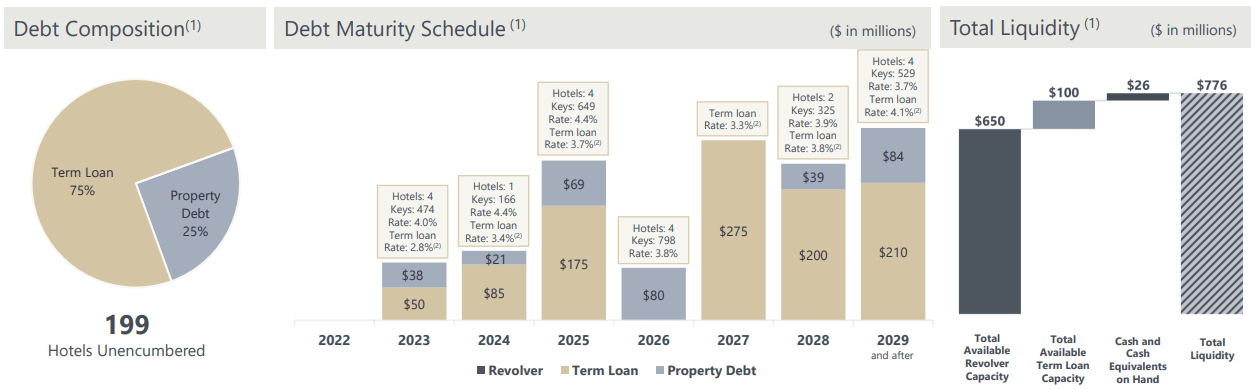

75% of APLE’s debt is from term loans while the remaining 25% is property debt. Out of the 220 hotels APLE owns, 199 are unencumbered. They have a very manageable maturity schedule with $88 million in debt coming due in 2023 with a total liquidity of $776 million available to them.

{kind=link}

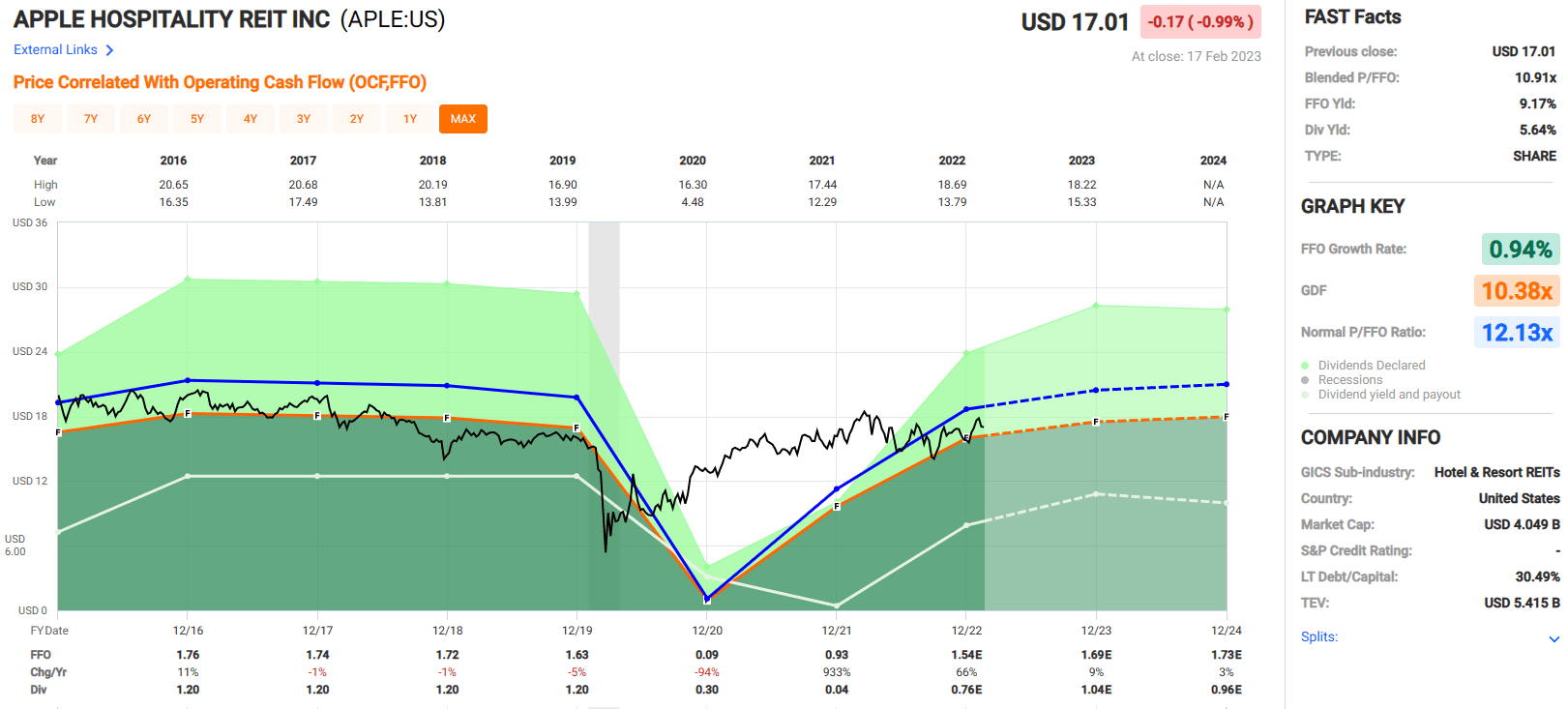

The hotel and travel industry got destroyed during the pandemic and Apple Hospitality was no exception. Their funds from operations went from $1.63 in 2019 to $0.09 per share in 2020 and they were forced to cut their dividend from $1.20 in 2019 to $0.30 in 2020 and then another cut to $0.04 in 2021.

While no one likes it when a REIT has to cut its dividend, I give APLE a pass on this due to the extraordinary circumstances it found itself in that was completely outside of management’s control.

Apple Hospitality’s FFO rebounded from $0.09 to $0.93 per share in 2021 and is expected to come in at $1.54 in 2022. Analysts project FFO of $1.69 per share in 2023 which would get APLE back up to pre-pandemic levels. Similarly, APLE has been repairing its dividend with a raise from its low of $0.04 to $0.76 per share expected in 2023. The 2022 dividend is very well covered with an expected AFFO payout ratio of just 55.88%.

APLE became publicly listed in 2015 and just several years later were forced to deal with the pandemic. It’s hard to get a good read on their long-term growth potential due to their short history and the recent circumstances. Since 2016 they have an average FFO growth rate of 0.94% but that is significantly distorted by the decline they experienced during the pandemic.

Currently APLE is trading at a P/FFO multiple of 10.91x which is a discount to their normal P/FFO of 12.13x. At the current market price they have an FFO yield 9.17% and pay a dividend yield of 5.64% that is very secure. They have a level of built-in protection against inflation with their turnover rate and have exceptional debt metrics. At iREIT we rate Apple Hospitality REIT a Spec BUY.

{kind=link}

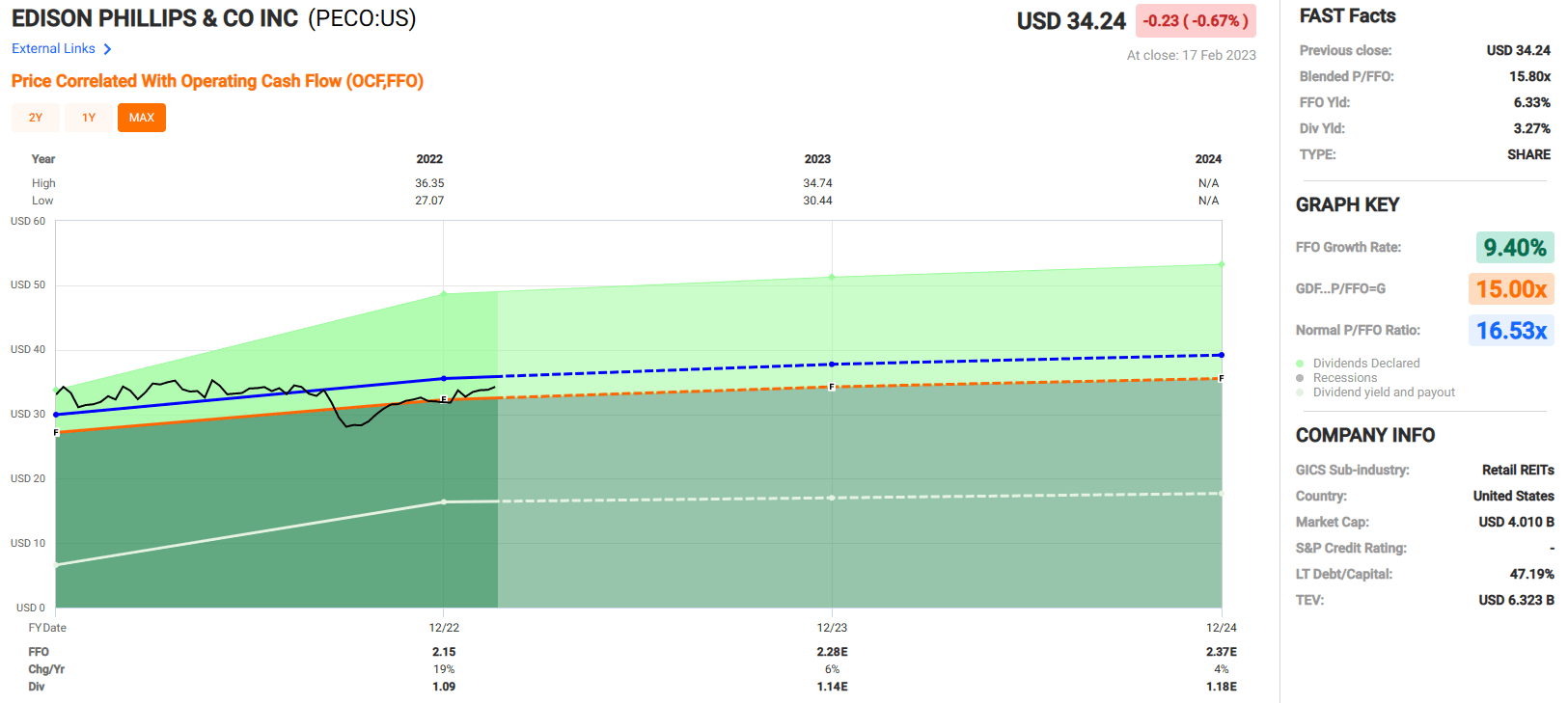

SWAN-a-Bee: Phillips Edison & Co. ( PECO )

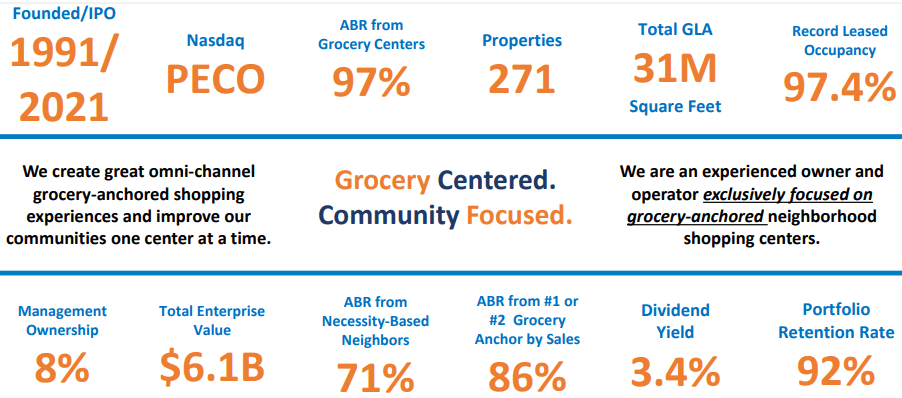

Phillips Edison & Co is an internally managed REIT that specializes in grocery-anchored shopping centers. Their portfolio has both national and regional retailers that sell necessity-based goods and services that are located in areas with attractive demographics. PECO was founded in 1991 and went public in 2021.

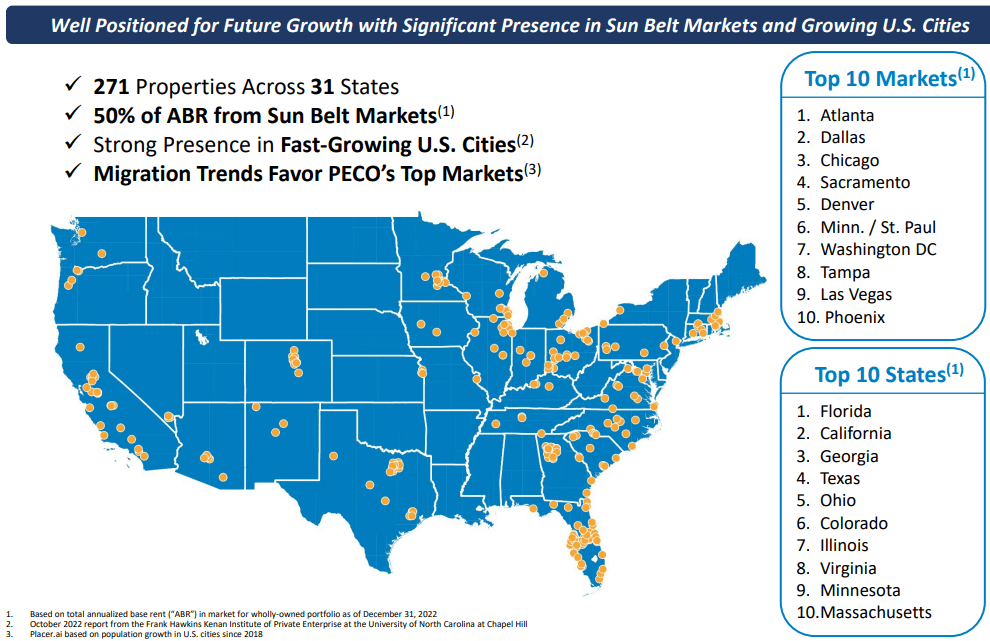

They own 271 properties in 31 states that cover a gross leasable area (“GLA”) of 31 million square feet and have a 97.4% leased occupancy rate.

{kind=link}

Their portfolio is strategically focused on shopping centers that are anchored by a grocery store and necessity-based retailers that are recession-resistant and essential for day-to-day living.

Additionally, they target high growth markets with an emphasis on the Sun Belt region. 97% of PECO’s annual base rent (“ABR”) is generated from omni-channel grocery-anchored shopping centers, 71% of their ABR comes from necessity-based goods and services retailers, while 50% of their ABR comes from Sun Belt Markets. Their top 3 markets are Atlanta, Dallas, and Chicago and their top 3 states are Florida, California, and Georgia.

{kind=link}

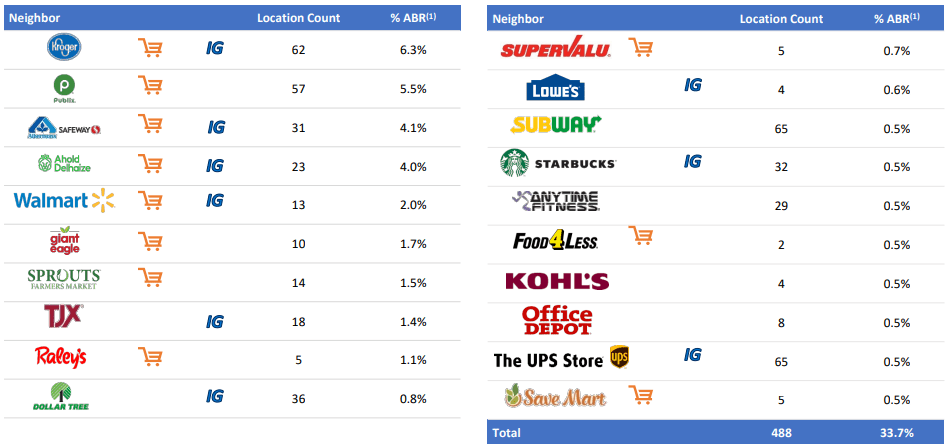

PECO has a strong tenant roster with recognizable names like Kroger, Publix, Walmart, and UPS to name a few. Their top tenant makes up 6.3% of their ABR and their top 20 tenants combined make up 33.7% of their ABR.

Only 9 of their tenants make up more than 1% of their ABR and 4 out of their top 5 tenants are investment grade. PECO has a stable and growing income stream with fixed contractual rent bumps and a weighted average remaining lease term of 31.7 years for their grocery anchors and 8.1 years for their inline stores.

{kind=link}

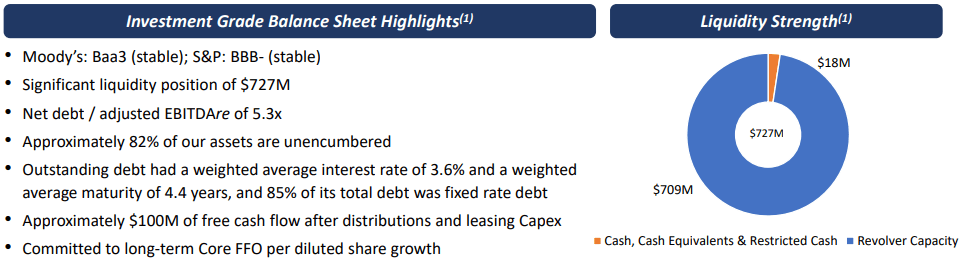

PECO has a strong balance sheet with an investment grade rating of Baa3 and BBB- from Moody’s and S&P respectively. They have a Net Debt to Adjusted EBITDAre of 5.3x and $727 million in liquidity.

Approximately 82% of their assets are unencumbered, 85% of their debt is fixed rate, and they have a 3.6% weighted average interest rate and a weighted average term to maturity of 4.4 years.

{kind=link}

As previously mentioned, PECO is a relatively new public company having filed its initial public offering in 2021. We don’t have much historical information to gauge future growth rates from, but PECO has necessary and reliable tenants with a sound business model and has been in operation since 1991.

Over their short history as a publicly traded company, PECO has a blended average FFO growth rate of 9.40%. They grew FFO by 19% in 2022 but that is expected to normalize to 6% in 2023 and 4% in 2024.

PECO pays a 3.27% dividend yield and makes monthly distributions. The dividend is very secure with a 2022 AFFO payout ratio of just 60.27%.

From the little history we have, PECO has steadily paid its monthly distributions with two increases since 2021. In October 2021 PECO increased its monthly dividend from $0.085 to $0.900 for a 5.88% increase and then in October 2022 increased the monthly payout to $0.933 for a 3.67% increase.

{kind=link}

PECO is relatively new as a public company but shows promise with its concentration in grocery-anchored shopping centers and retailers who are necessity-based.

They have good debt metrics to support ongoing investment and pay a monthly dividend that is very secure with a low AFFO payout ratio of 60.27%. They are currently trading at a P/FFO multiple of 15.80x, which is below their normal P/FFO ratio of 16.53x. At iREIT we rate Phillips Edison & Co. a BUY.

{kind=link}

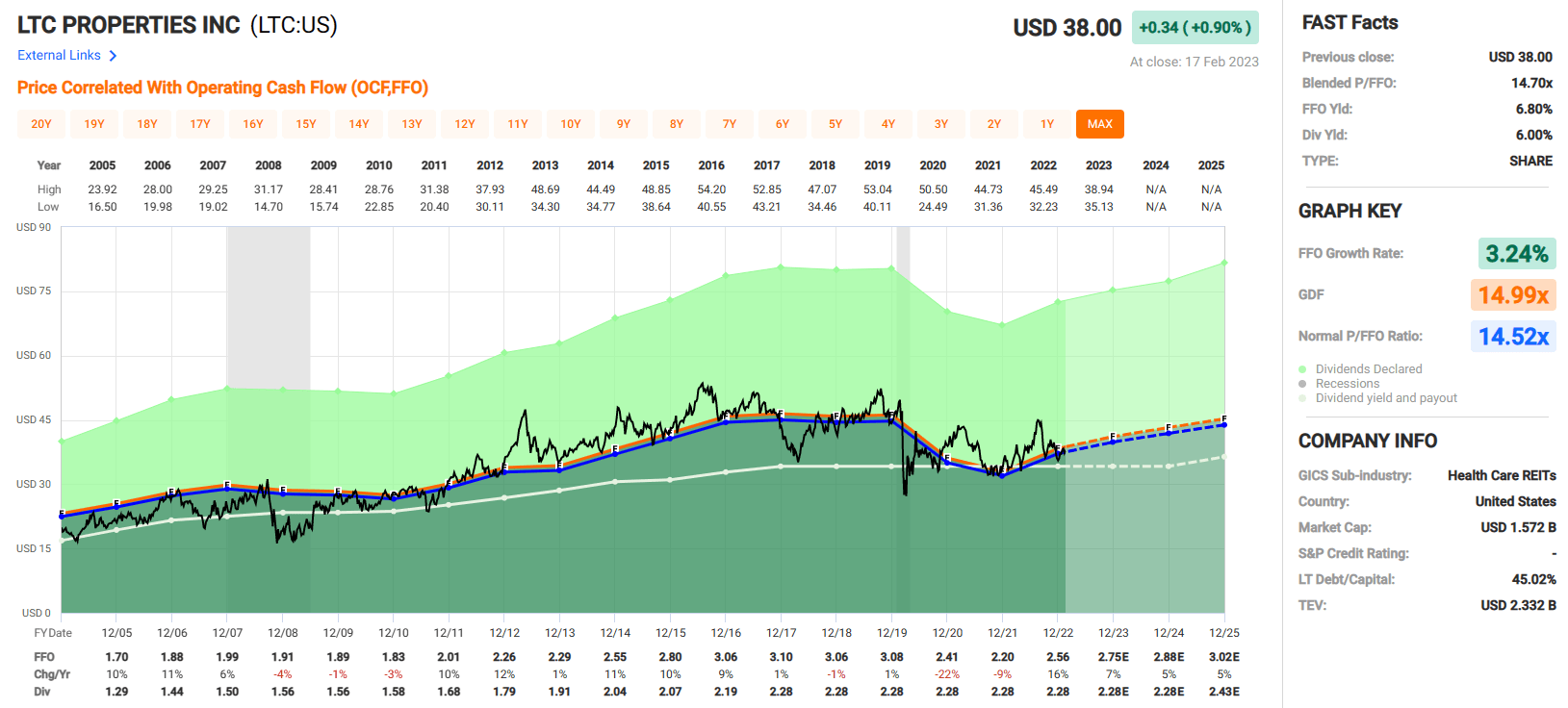

SWAN: LTC Properties ( LTC )

LTC Properties is a REIT in the healthcare sector that invests in Skilled Nursing and Assisted Living facilities. Their investment by property type is almost evenly split with 50.0% in Skilled Nursing and 48.6% in Assisted Living.

LTC has an interest in 78 Skilled Nursing and 125 Assisted Living properties, and one property described as Other, which consists of land and a behavioral health facility. In total, LTC has an interest in 204 properties across 29 states for a total gross investment of $1.95 billion.

LTC - Form 10-K (gross investments in thousands)

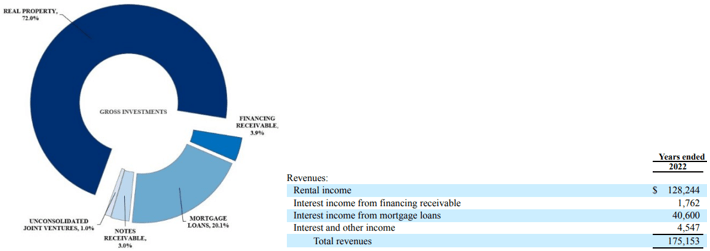

LTC is somewhat of a hybrid between an equity REIT and a mortgage REIT (“mREIT”) as it derives revenue from both rental income and interest income from loans.

While almost all of their investments are in Skilled Nursing and Assisted Living, some of it is in the form of owning the property and leasing it out on a triple-net basis, and some of it is in the form of issuing mortgage debt or other forms of financing for healthcare facilities and collecting interest payments.

By investment type, owned / real property makes up 72.0%, mortgage loans makes up 20.1%, financing receivables makes up 3.9%, and notes receivables makes up 3.0% of their investments. By revenue their two largest categories are rental income which makes up 73.22% of their total revenue and interest from mortgage loans which makes up 23.18% of their total revenue.

{kind=link}

LTC has good debt metrics with a Debt to adjusted EBITDAre of 5.6x, a Fixed Charge Coverage ratio of 4.3x, and a Debt to Gross Asset Value of 37.4%. At 2022 year end, LTC had $10.4 million in cash and cash equivalents and $270 million available to them under their unsecured revolving credit line. Additionally, under their Equity Distribution Agreements they have the ability to raise $130.6 million through the issuance of common stock.

LTC - Form 10-K

LTC does not have an investment grade credit rating from the public debt markets because they don’t issue public debt. Instead, they borrow long term debt through insurance companies and get investment grade pricing because they have an investment grade credit rating from the National Insurance Company Rating agency.

Below is an excerpt from my interview with the management team at LTC. You can find the audio and full transcript at the link below:

iREIT (Pam Kessler, CFO)

Source for interview at iREIT on Alpha

Additionally, LTC has well spaced-out maturities with no major maturity until 2025 and a weighted average interest rate of 4.24%.

LTC - Investor Presentation

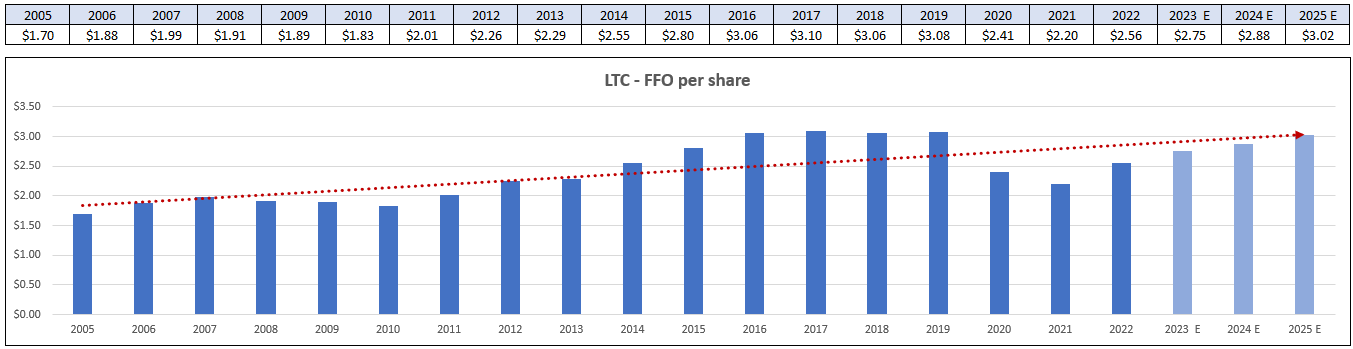

LTC has delivered steady growth in its funds from operations (“FFO”) with an average annual growth rate of 3.24% since 2005. Their average growth rate was severely impacted by the pandemic so when looking at their average FFO growth rate from 2005 to 2019 it comes in at almost 5%. Analysts project FFO growth rates of 7% and 5% in the years 2023 & 2024 respectively.

{kind=link}

LTC pays a monthly dividend and currently pays a 6.00% dividend yield. The dividend is covered with an AFFO (Adjusted FFO) payout ratio of 85.10%. LTC has only had modest growth in its dividend over the last 15 years with an average growth rate of 2.87%.

They have not raised the dividend since 2017 when they raised it to $2.38 which is the same rate they currently distribute. It is of note though that they did not cut the dividend during the crisis brought on by the pandemic.

{kind=link}

Currently LTC is trading at a P/FFO multiple of 14.70 which is in-line with their normal P/FFO multiple. Although dividend growth has been modest, they pay a high current yield at 6.00% that is reasonably covered and make monthly distributions. They have sound credit metrics and are projected to have above average FFO growth over the next several years. At iREIT we rate LTC Properties a Spec BUY.

{kind=link}

SWAN: Realty Income ( O )

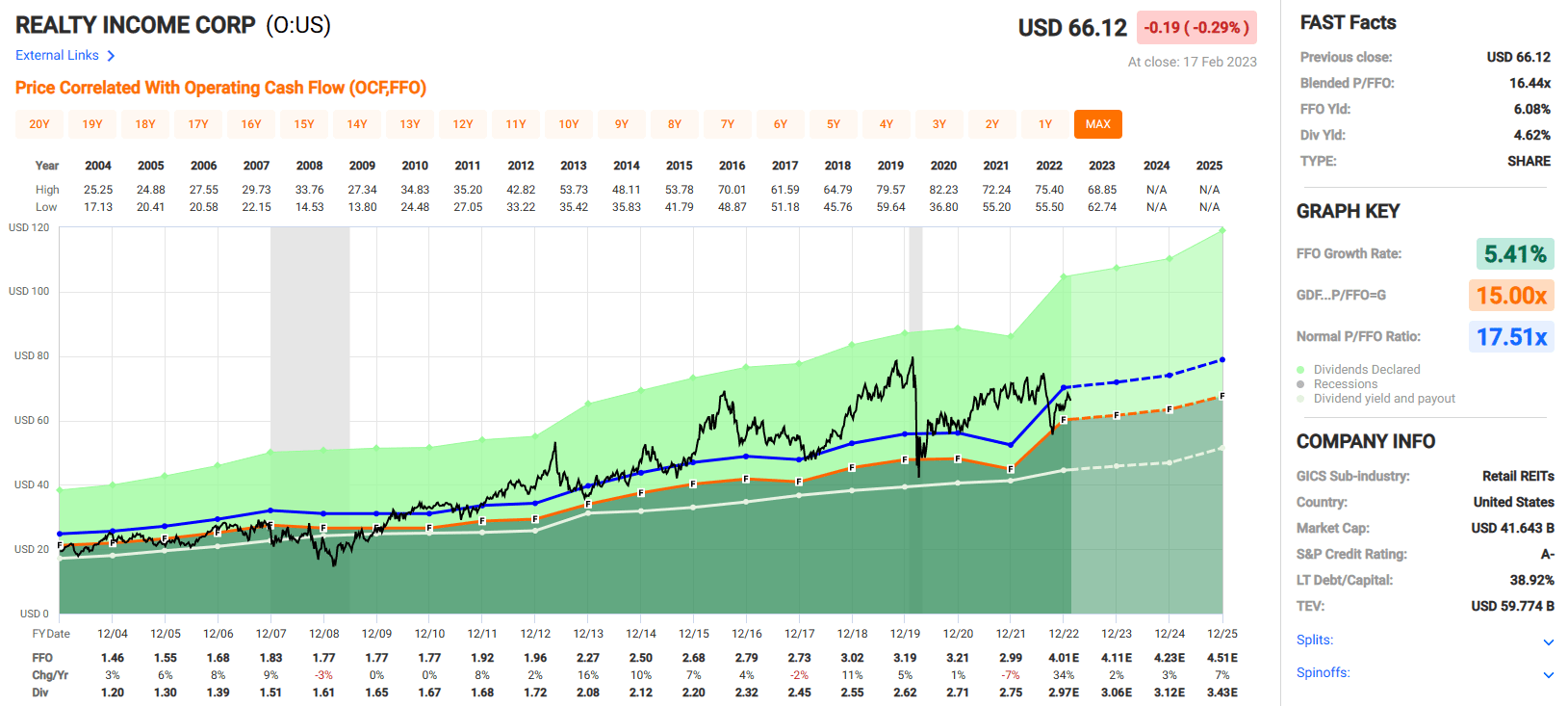

Realty Income was founded in 1969 with a single Taco Bell before going public in 1994. Since its public listing, Realty Income has become the standard bearer for real estate investment trusts (“REIT”) in the triple-net lease space with its portfolio expanding to over 11,700 properties and its revenue growing from $49 million to 1.97 billion in 2021.

Along with its storied history and consistent growth, Realty Income is probably best known for its monthly dividend, so much so that the company trademarked “The Monthly Dividend Company”.

The enthusiasm over their monthly dividend is not without merit as they are one of the few Dividend Aristocrats in the REIT industry with 27 consecutive years of rising dividends. Since 1995 Realty Income’s dividend has a compound annual growth rate of 4.4% with 628 monthly dividends declared and 100 consecutive quarterly increases as of October 2022.

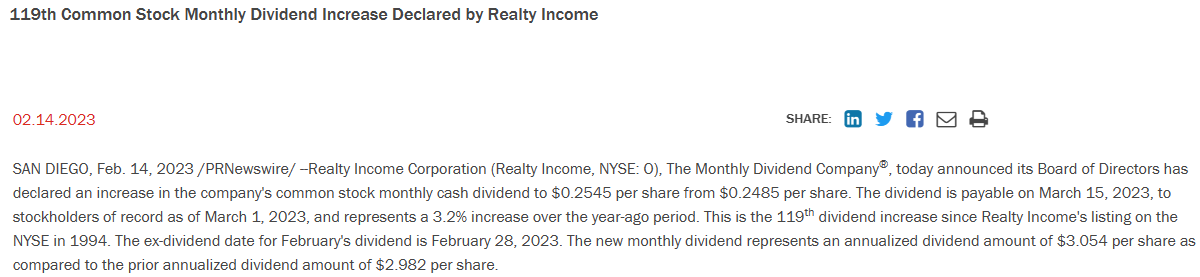

Realty Income - Press Release

On February 14, 2023, Realty Income announced their 119 th dividend increase since 1994. They increased the monthly dividend from $0.2485 to $0.2545 which represents a 3.2% year-over-year increase.

{kind=link}

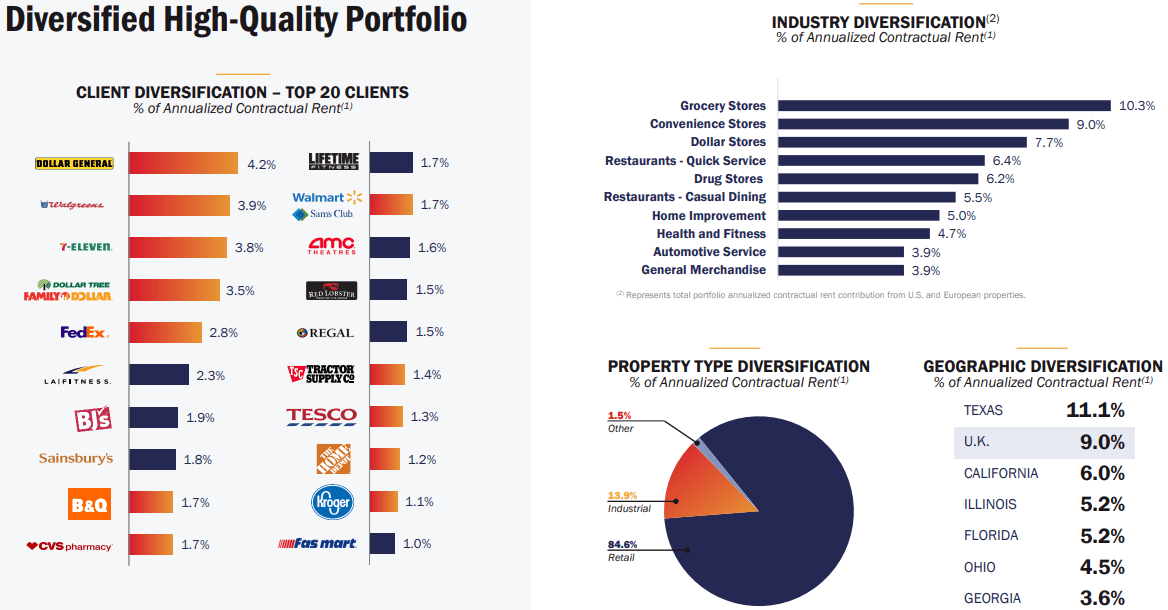

Realty Income is geographically diversified with properties in all 50 states and international properties in the UK and Spain. They are well diversified in the industries they serve with grocery, convenience, and dollar stores making up their largest 3 categories.

Similarly, they are well diversified by client with their top tenant only making up 4.2% of their contractual rent. Their tenants are well known and established businesses including Dollar General, Walgreens, 7-Eleven, FedEx, Kroger, Home Depot to name a few. 43% of their annual rent comes from investment grade tenants.

{kind=link}

Realty Income itself is investment grade with an A-/A3 credit rating from S&P Global and Moody’s respectively. They have strong debt metrics with a 5.2x Net Debt to Adjusted EBITDAre and a 5.5x Fixed Charge Coverage ratio.

95% of their debt is unsecured and 88% of it is at a fixed rate. Additionally, their weighted average term to maturity is 6.3 years and they have approximately $2.5 billion in liquidity as of September 2022.

{kind=link}

Much has been made over the last year about how Realty Income, and REITs in general, will fare under the current inflationary and interest rate environment. From what I’ve seen there are two basic arguments. The first is that with risk-free rates as high as they currently are why invest in a risky asset for a slightly higher (or lower) yield?

Well, this is a valid point and one that comes down to the risk aversion of the investor. If an investor wants to have a risk-free investment at a reasonable yield, then they may prefer treasuries over equity investments. However, if an investor is looking to buy into a company with growth potential in both earnings and yield then investing in equities might be preferred.

I really don’t think comparing the two are “apples to apples”. In one case you are guaranteed a fixed coupon and your principle back. In the other you are buying into a company with all the risks and growth that comes with it.

Generally, over the long-term investing in a basket of equities has outperformed risk free assets so again it comes down to the risk aversion of the investor. Do they want risk-free yield now or yield with the potential to grow and with prospects to deliver more total return in the future?

The second argument I’ve seen is that REITs cost of capital will rise to the point where they cannot make accretive acquisitions with the higher rates we are currently experiencing, which would impact their funds from operations (“FFO”) and ultimately impact their dividend payout. I find this argument to be more flawed than the first.

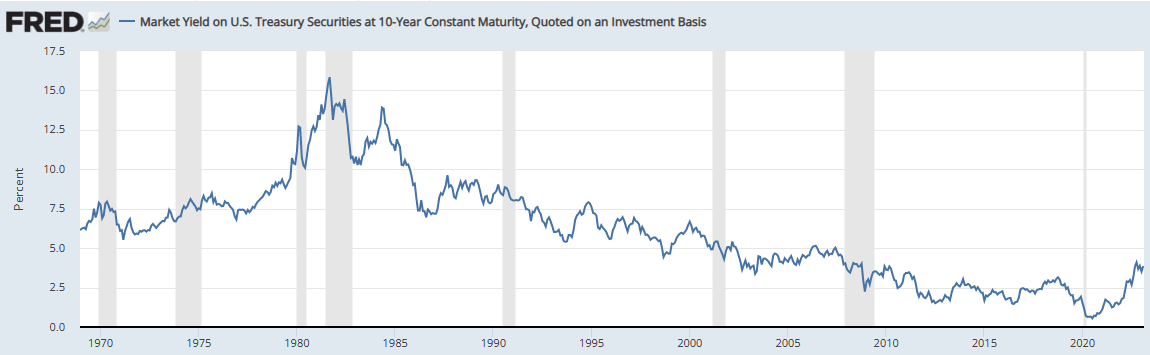

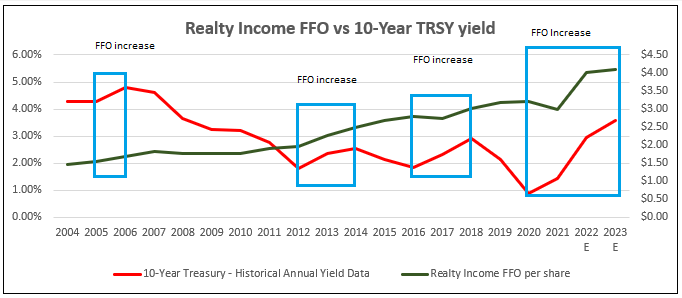

As previously mentioned, Realty Income has been publicly listed since 1994, but they have been in operation since 1969. I pulled the 10-Year Treasury yield since 1969 to illustrate how Realty Income has survived and grown through multiple interest rate environments.

In 1969 the 10-Year Treasury was yielding approximately 6%. That rose to around 15% in the early 1980’s and dropped down to around 6 to 7% in 1994. As of the most recent market close, the 10-Year was yielding 3.817%. The interest rates Realty Income has operated through in the past puts today’s rates in perspective.

{kind=link}

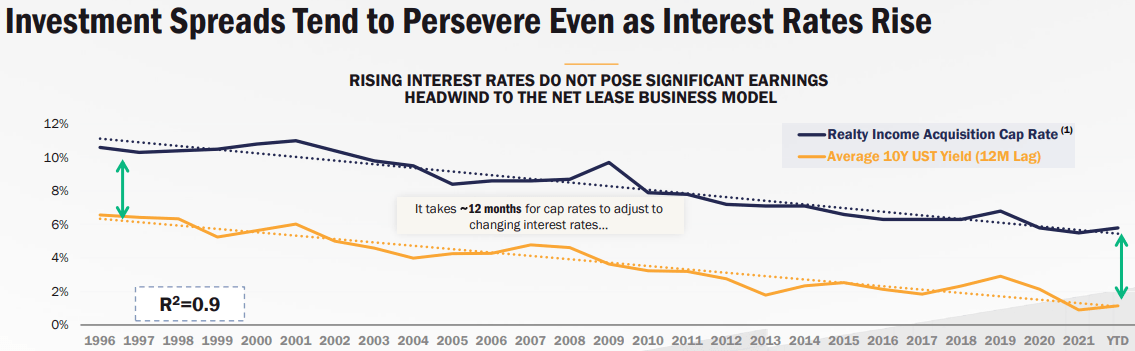

As illustrated in Realty Income’s latest presentation, they are able to maintain their investment spreads even as interest rates rise. They do note that there is roughly a 12-month lag for cap rates to adjust to the changing interest rates, but over the long-term rising interest rates have not materially impacted their investment spreads.

{kind=link}

I put together the chart below to illustrate how rising rates impacts Realty Income’s FFO. The red line represents the 10-Year Treasury’s average yield for the year, while the green line represents Realty Income’s annual FFO per share.

Over this 20-year period rates have declined overall, but there has been several periods where rates rose. I put a box around each period where the 10-Year Treasury’s average yield rose in order to see how Realty Incomes earnings were impacted. In each period Realty Income grew their FFO per share even when rates were rising.

{kind=link}

Realty Income has delivered growth in its FFO and dividend through multiple interest rate and inflationary environments and should be able to continue its performance in the current environment.

Realty Income is a much stronger company today than it was when rates were much higher and has done nothing but grown since it’s public listing in 1994. Realty income pays a 4.62% dividend yield that is well-covered with an AFFO payout ratio of 76.17% and currently trades at a discount to its normal P/FFO multiple. At iREIT we rate Realty Income a BUY.

{kind=link}

One Last SWAN: Agree Realty ( ADC )

Last but certainly least is the monthly payer Agree Realty , a real estate investment trust ("REIT") that acquires and develops retail properties and transacts sale-leasebacks with tenants on a net lease basis.

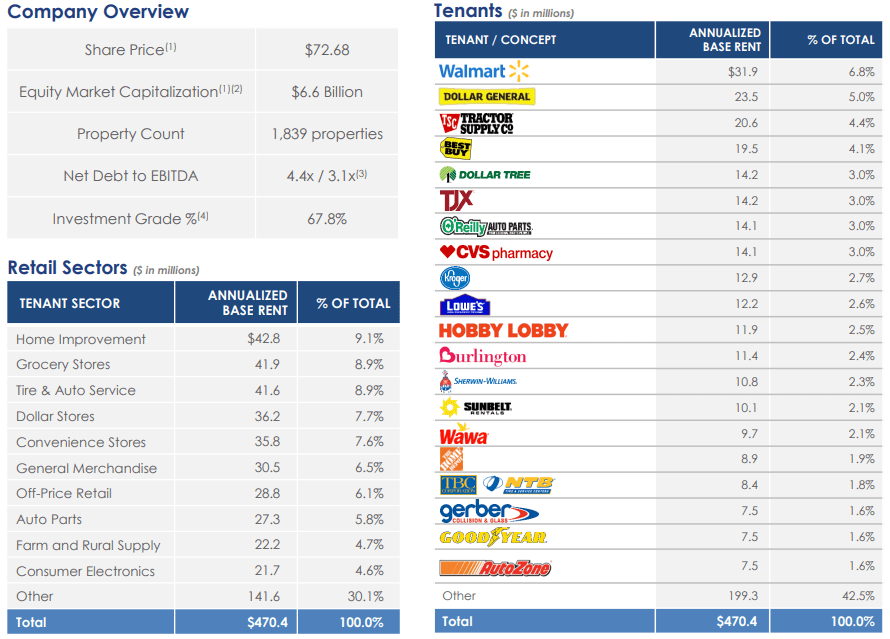

Almost all of ADC’s tenants are subject to net lease agreements which typically makes it the tenant’s responsibility to pay for property taxes, insurance, and maintenance, along with the monthly rent. Agree Realty was founded in 1971, filed its initial public offering in 1994, and currently has a market capitalization of $6.63 billion.

As of December 31, 2022, ADC’s portfolio consisted of 1,839 properties located in 48 states with a Gross Leasable Area (“GLA”) of approximately 38.1 million square feet. Their properties are roughly 99.7% leased with a weighted average remaining lease term around 8.8 years and 68% of their tenants are investment grade.

{kind=link}

On February 14, 2023, Agree Realty reported their fourth quarter and 2022 full year results and highlighted the following:

- Full year Core Funds from Operations (“Core FFO”) per share increased 8.1% to $3.87.

- Full year Adjusted Funds from Operations (“AFFO”) per share increased 9.2% to $3.83.

- Full year dividends declared in 2022 of $2.805 represents a 7.7% year-over-year increase.

- Acquired 465 retail net lease properties in 2022 for a record investment of $1.71 billion.

- Raised roughly $1.3 billion in equity proceeds through two overnight offerings and the company’s At the Market (“ATM”) program.

- Received an upgraded credit rating of Baa1 from Moody’s

- Issued a public bond offering of $300 million of 4.80% senior unsecured notes due 2032 with an effective all-in rate of 3.76%.

- At year end ADC had approximately $1.5 billion in total liquidity that includes revolving credit facility availability, cash on hand, and outstanding forward equity agreements.

(Source: ADC Press Release)

Agree Realty has a strong tenant roster with names like Walmart, Dollar General, Lowe's, Home Depot, and CVS Pharmacy. Their top tenant is Walmart which contributes 6.8% of ADC’s Annual Base Rent (“ABR”) and their top 20 tenants make up 57.5% of their total ABR.

While a fairly large percentage of their ABR comes from their top 20 tenants, the companies in their top 20 are very established and well-known names, and as previously mentioned 68% of their tenants are investment grade. In terms of retail sectors, ADC’s top 5 sectors are Home Improvement (9.1% ABR), Grocery Stores (8.9% ABR), Tire & Auto Service (8.9% ABR), Dollar Stores (7.7% ABR) and Convenience Stores (7.6% ABR).

{kind=link}

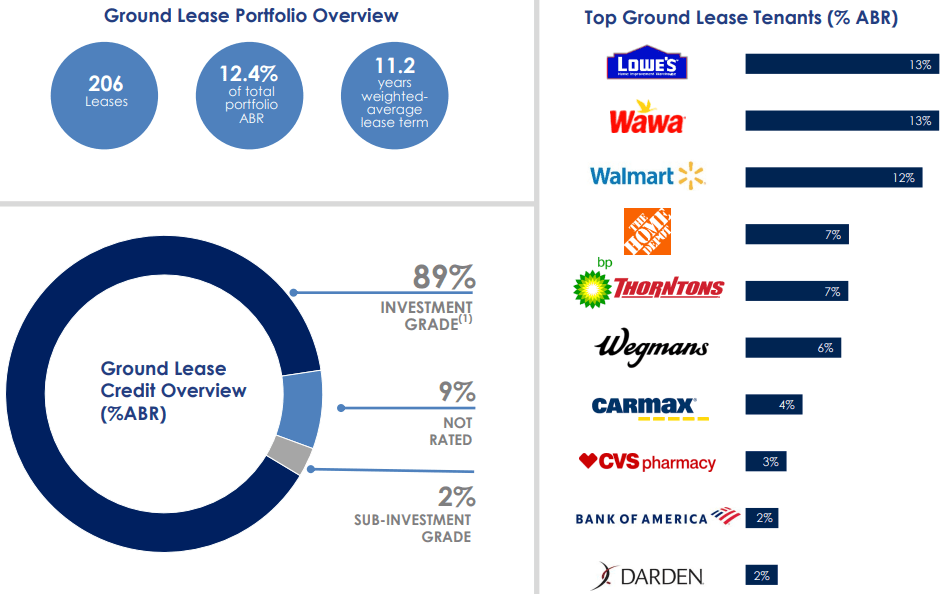

While Agree Realty is primarily known for its net lease retail properties, their portfolio also contains ground leases. They have 206 ground leases that contribute 12.4% of their total ABR with a weighted average lease term of 11.2 years. 89% of their ground lease tenants are investment grade and their top ground lease tenants includes Lowes, Walmart, Home Depot, and Bank of America.

{kind=link}

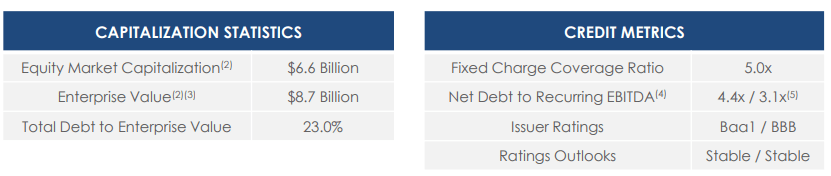

Agree Realty has excellent credit metrics with a Total Debt to Enterprise value of 23.0%, a Net Debt to Recurring EBITDA of 4.4x (3.1x when including the settlement of their forward equity agreement), a Fixed Charge Coverage ratio of 5.0x, and approximately $1.5 billion in liquidity.

{kind=link}

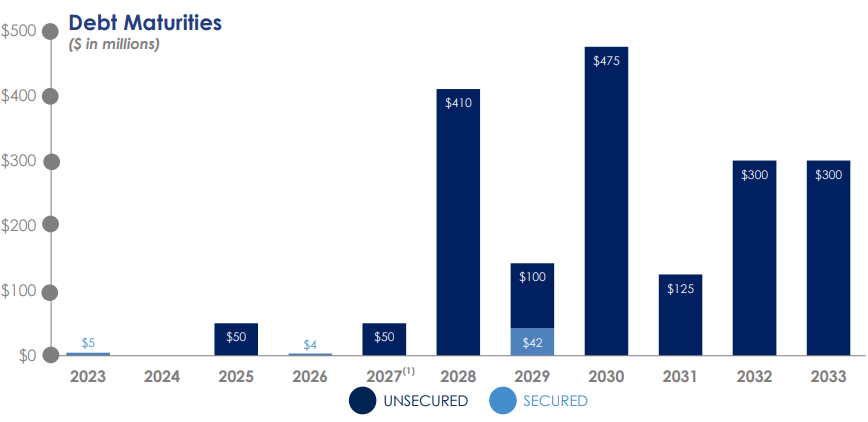

Agree Realty has very few debt maturities over the next several years which should give them flexibility until interest rates normalize. Only $5 million in principle is due in 2023, no principle is due in 2024, and no major maturities occur until 2028. In total ADC has a weighted average debt maturity of approximately 8 years.

{kind=link}

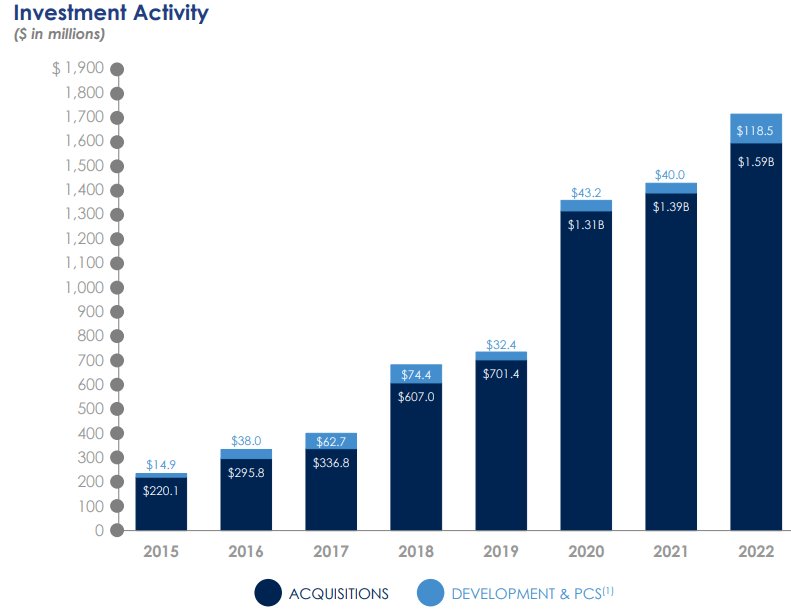

Agree Realty’s investment activity reached a record $1.7 billion in 2022. As shown in the chart below, ADC has been steadily increasing their investments since 2015 with a large increase in years 2020 through 2022. The increased investment activity should result in increased Funds from Operations (“FFO”) which should fuel further dividend growth.

{kind=link}

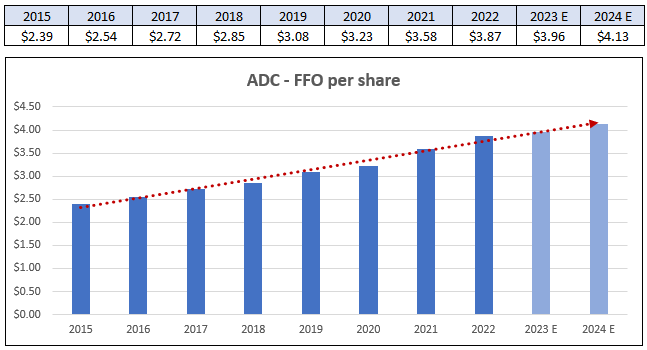

Since 2015 ADC has increased its FFO per share every year and delivered an average FFO growth rate of 6.60%. Analysts project a 2% increase in FFO in 2023 and a 4% increase in 2024. An FFO growth rate of 6.60% is very good. As a point of comparison, Realty Income grew FFO by 5.4%, National Retail Properties had a 4.70% growth rate, and W.P. Carey had an FFO growth rate of 1.69% since 2015.

{kind=link}

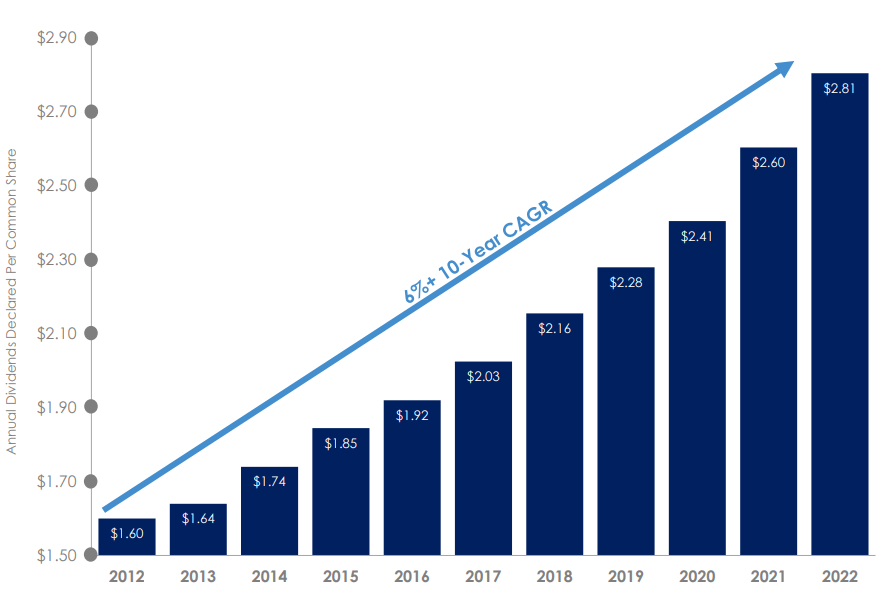

The growth in FFO has enabled Agree Realty to increase its monthly dividend at a 10-year compound annual growth rate of 6%. Currently ADC has a 3.85% annual dividend yield and makes monthly distributions.

They have increased the dividend every year since 2012 and did not make any cuts during the pandemic. The dividend is secure with a 2022 AFFO payout ratio of 73.24%. The low payout ratio insulates the dividend should economic conditions worsen and leaves room for future dividend growth.

{kind=link}

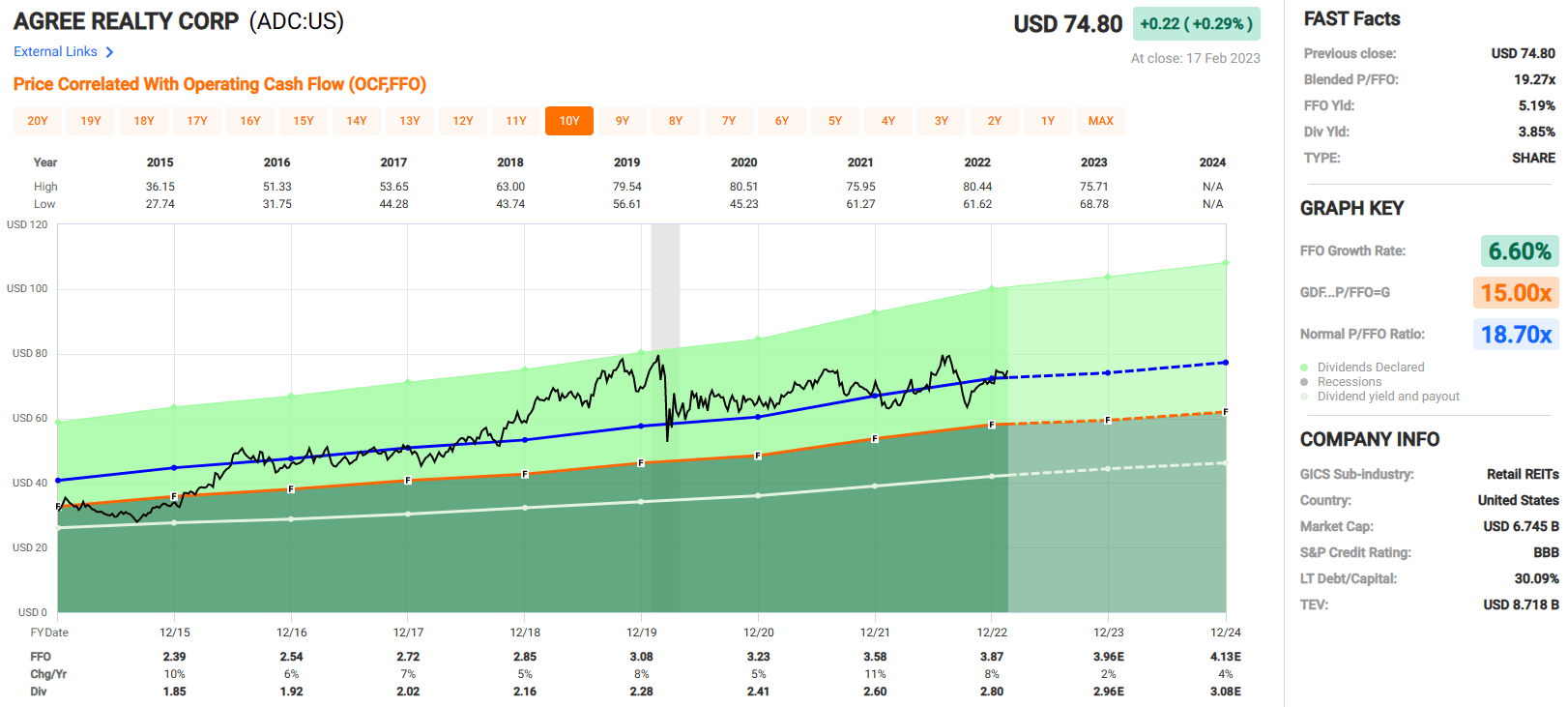

Agree Realty is a blue-chip net lease REIT that is trading at a blended P/FFO of 19.27x, which is a slight premium to its normal P/FFO multiple of 18.70x. They pay an above average dividend yield that is very secure and have delivered high FFO and dividend growth over the past decade.

Their credit and debt metrics are excellent which should allow them to continue to pursue a high level of investment activity that should fuel growth over the years to come. We have a buy-under target of $74.00, which puts ADC slightly outside of our buy range. At iREIT we rate Agree Realty a HOLD.

{kind=link}

I hope you enjoyed the article and I look forward to your comments and/or questions below.

Happy SWAN Investing!

For further details see:

Monthly Mailbox Money: The SWAN Edition