SPGI - Moody's: It's Time To Rate This Ratings Agency

2023-11-25 02:21:53 ET

Summary

- Moody's is a market leader in credit and debt ratings existing as one of the key players in what is a natural oligopoly.

- The company had a slow start in FY23 but showed strong performance in Q3 and has a relatively healthy outlook for full year 2023.

- Moody's wide economic moat, strong financial performance and incredibly well managed balance sheets make it an attractive long-term buy-and-hold, in my opinion.

- Shares are fairly valued at best given current prices.

- Buy rating issued.

Investment Thesis

Moody's ( MCO ) is the market leader when it comes to credit and debt ratings as well as risk analytics. The company has built a commanding position within both industries through their Analytics and Investor Service businesses and enjoys a wide economic moat built upon their reputation, industry knowhow and massive scale.

FY23 saw Moody's get-off to a slow start but with their most recent Q3 earnings reports showing strong fiscal performance and a relatively healthy full-year 2023 outlook.

While a recessionary environment could place real pressure on earnings growth, Moody's unique set of business and market leading position makes it an attractive long-term buy-and-hold pick.

Still, I believe a fair valuation is present in shares at best with a slightly overvaluation existing should a bearish macroeconomic environment develop for 2024.

I therefore rate Moody's a Buy at present.

Company Background

Moody's FY23 Q3 Press Release

Moody’s is a global integrated risk assessment firm that provides organizations and investors with credit rating opinions and information along with a raft of financial analytics tools. The firm has been in business over 100 years and has emerged as the main credit rating agency having consistently beaten rivals S&P both in terms of market share and profitability.

The agency has spent the last 15 years expanding their portfolio of products and services in order to offer its clients a more holistic toolkit of financial services. This diversification has mainly consisted of the establishment of Moody’s Analytics, a risk assessment franchise serving primarily banks and insurance companies.

Since its inception, Moody’s has enjoyed an enviable position within the market thanks to the oligopolistic nature of the ratings business. The last two decades have seen Moody’s consistently grow their revenues, profits and margins as more and more businesses required their credit rating and analytics services.

Rob Fauber is the current president and CEO of Moody’s having taken over at the start of 2021. Fauber has an extensive history with Moody’s having joined back in 2005 and held multiple leadership positions prior to his election by the board of directors for promotion to CEO.

Given Fauber’s history with the firm, absolute desire for operational excellence and significant experience within the investment banking, corporate strategy and commercial banking businesses, I see little reason to question his ability to continue leading Moody’s forward into the 2020s and beyond.

Economic Moat - In Depth Analysis

Moody’s enjoys a wide economic moat which is primarily built upon their market leading reputation within the ratings and analytics market along with some network effects arising from the integrations between their ratings and analytics service provisions.

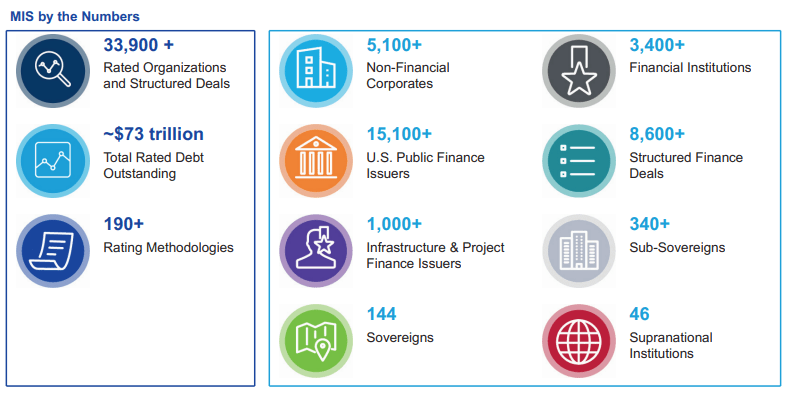

Thanks to Moody’s historic presence, reliable ratings and continued innovation within the industry, the firm has managed to build an incredibly reputable image for the firm’s “Moody’s Investor Service” ((MIS)) business segment.

Many investors, banks and corporate institutions rely on ratings by agencies such as Moody’s, S&P ( SPGI ) or Fitch when conducting business thanks to the more reliable information provided by these firms.

{kind=link}

The majority of revenues extracted by Moody’s MIS segment depend on bond issuance rates which makes the MIS business ultimately quite cyclical and tied to the overall health of the U.S. and global economies.

The expansion of Moody’s MIS operation into a huge number of foreign countries and jurisdictions has greatly increased the attractiveness of Moody’s ratings thanks to the ability for investors to easily compare both U.S. domestic entities and foreign ones.

The provision of international credit ratings has made Moody’s an integral part of financial markets across the globe with the firm acting as an essential source of information and data. Without Moody’s (or S&P and Fitch for that matter), the rating of credit for companies, jurisdictions, countries and financial entities would be an incredibly complex and unreliable objective.

Moody’s also benefits from their historic presence within the ratings business which has allowed the firm to generate a huge wealth of data that underpins their ratings processes. The extensive information present at the firm regarding default rates, credit delinquencies and bond quality benefits Moody’s tangibly especially when compared to a potentially new entrant emerging into the market.

While this advantage is largely shared by both Fitch and S&P, I believe Moody’s emergence over the last 50 years as the leader in the ratings business means assuming the firm has the ultimate amount of data and information is fair.

Fundamentally, it is Moody’s massive presence within the credit rating industry, their extensive data and industry knowledge and international reach that generates the majority of the firm’s wide economic moat. Quite simply, it would be incredibly difficult for key competitors S&P and Fitch to outperform Moody’s given their smaller sizes and slightly less advanced product offerings.

To further bolster their revenue streams through reducing their reliance on the more cyclical nature of the ratings business, Moody’s has rapidly developed their Analytics business to closely complement their core ratings agency.

{kind=link}

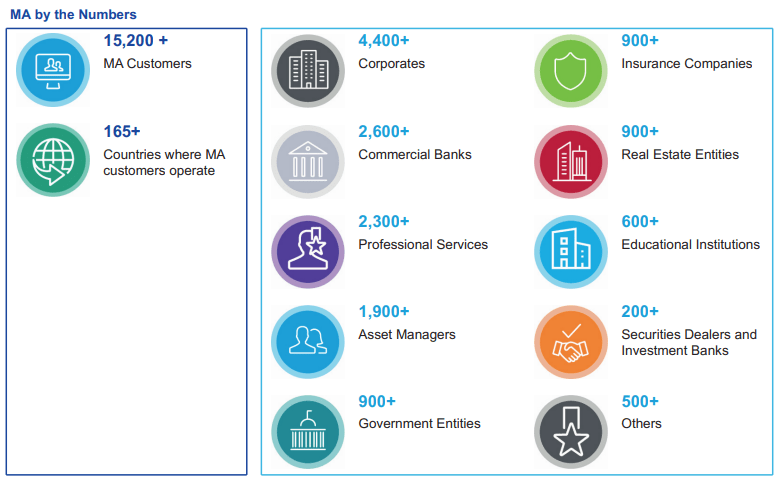

Moody’s Analytics ((MA)) provides mainly business clients with a vast plethora of quantitative tools that allow these organizations to gain a better understanding of their customers, internal data and corporate risk.

The MA business has grown to become an important component to Moody’s overall business with the research and analytics services provided by the segment proving to be very popular among both private and enterprise level clients.

The massive breadth in services offered within the MA segment (ranging from banking, insurance, Know Your Customer (KYC), Data and Information, Decision Solutions, Structure Finance and research and insight services) should allow Moody’s to effectively compete with alternative services moving forwards.

While the credit research element of the MA business relies on data already being implemented and generated by the core MIS business, I believe the real moatiness of the MA business comes from the networking effects it creates in tandem with their ratings operations.

Fundamentally, the provision of a high quality quantitative and research analytics service alongside their already proven credit rating business provides clients with a holistic method of analyzing markets, equities, jurisdictions and countries.

I believe Moody’s is able to engage in significant cross selling of their services thanks to the existence of the MA business which ultimately further acts to promote the core ratings business even further.

Overall, I believe Moody’s wide and robust economic moat is built upon the quality and breadth of their core credit rating business. Their MIS segment is market-leading both in terms of the quantity of information available and the reliability of said data. The international span present within the MIS segment further increases the attractiveness of Moody’s service compared to those presented by competitors.

Additionally, the MA business has proven to be an important element of Moody’s operations as a whole while simultaneously enabling the firm to benefit from tangible networking effects that drive further sales of their MIS product.

Therefore, I rate Moody’s as having a wide economic moat that will aid the firm in continuing their form of earning outsized returns on their invested capital.

Financial Situation

From an operating performance perspective, Moody’s is an absolute profitability powerhouse that on average generates massive returns and margins from their business operations.

The firm has 5Y average (as measured from FY22-FY18) gross, operating and net margins of 71.99%, 42.41% and 30.48% respectively. These margins are truly exceptional for any business and illustrate just how profitable of an enterprise Moody’s is.

The massive gross margin in particular suggests that Moody’s core MIS and MA business segments are lucrative operations that provide the firm with tangible pricing power and the ability to earn revenues far in excess of their COGS.

Interestingly, Moody’s key public competitor S&P has 5Y average gross, operating and net margins for the same period of 71.17%, 45.78% and 31.52% respectively.

The essentially identical gross margins support my earlier hypothesis that a natural oligopoly exists within the market with these two key players relatively evenly sharing market demand.

Moody’s also has 5Y (FY22-FY18) average ROA, ROE and ROIC of 14.01%, 287.49% and 22.35% respectively. The firm’s ROIC is truly excellent on even an absolute scale with very few businesses in existence coming close to such massive returns on invested capital.

The firm has also managed massive ROE in recent years which is a great indicator of the relatively limited number of shares available for purchase thanks to consistent buybacks by management.

Even by just examining these fundamental operational efficiency metrics it is clear to see that Moody’s is an absolute profitability powerhouse with their core business model generating massive returns and margins for the firm.

Moody’s has had a solid FY23 so far with slightly weaker than expected Q1 results being more than made up for with robust Q2 results and some pretty stellar earnings that were reported in their most recent Q3 results.

Examining Moody’s most recent Q3 earnings reports, it is clear to see that the firm is benefitting from the relatively strong demand witnessed across world's economies and particularly the resilience by the U.S. to avoid a recession in 2023.

{kind=link}

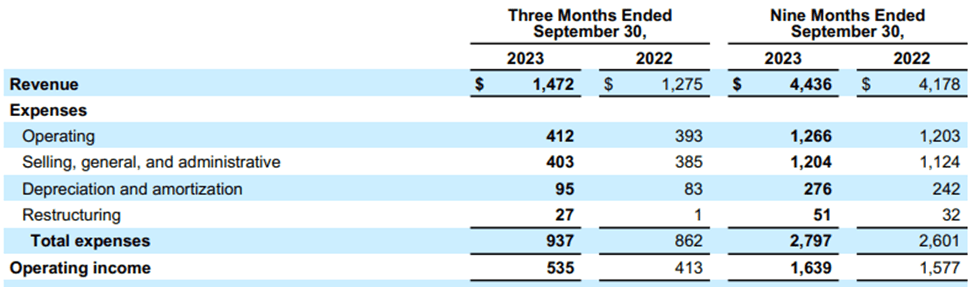

Q3 saw Moody’s grow their revenue YoY by over 15% thanks to strong performance in the MA segment along with outstanding growth being witnessed in their MIS segment thanks to a favorable mix of leveraged finance and infrequent banking issuer activity.

While the infrequent activity may decline in future quarters, the core strength of both the MA and MIS business is encouraging and suggests Moody’s is continuing to accurately meet the expectations and demands of customers within these business segments.

Moody's FY23 Q3 Press Release

The MA segment has continued to grow over recent years and now accounts for approximately 53% of total revenues for the firm. I believe the subscription model offered in the MA business segment has proven to work well given the wide breadth and continuously updated services provided by Moody’s.

Moody's FY23 Q3 Press Release

The strong growth witnessed in the MA business came thanks to strong revenue growth in essentially all of the services offered to customers. I believe this illustrates the high-quality nature of Moody’s MA service offerings and suggests that the business is well placed to compete with alternative products moving forwards.

While it may be difficult for Moody’s to replicate such earnings growth QoQ, I do foresee the MA segment continuing to grow ultimately becoming a dominant player within the analytics industry just like their credit business as in the ratings market.

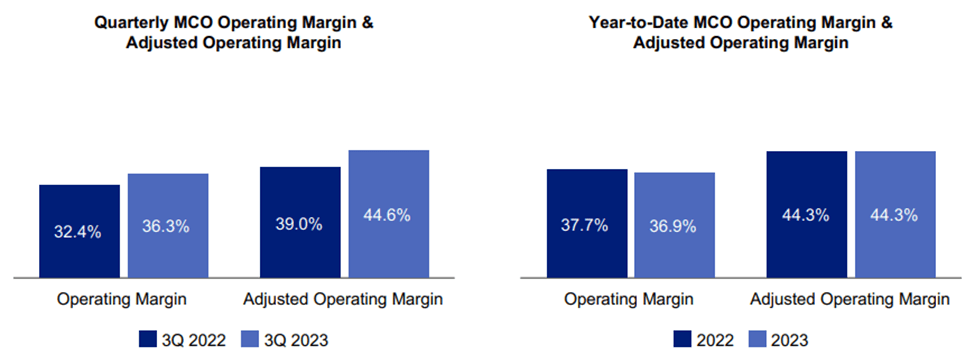

Moody’s has also managed their expenses well ensuring that total operating expenses only increased 8.7% while revenues grew 15%.

{kind=link}

This allowed the firm to increase their adjusted operating margins YoY by over 5% to 44.6% while YTD adjusted operating margins have been flat. Considering their weaker Q1 quarter and the inflationary macroeconomic environment, such cost control is truly wonderful to see.

Net income also increased by 28% as a result of the expanded operating margins and the strong growth in revenues to $389M, up from just $303M in Q3 FY22.

The solid Q3 performance combined with a slightly more optimistic economic outlook has resulted in Moody’s management team finally issuing some concrete guidance for the firm’s full year 2023 results.

Full year revenues are expected to increase in the high-single-digit percentage range while operating margins (unadjusted) are estimated to be around 37%. The firm also estimates full-year FCF or around $1.8B along with adjusted diluted EPS of between $9.75 and $10.25.

This mostly positive guidance suggests Moody’s (who has a reasonable understanding of the health of the overall U.S. economy) is not particularly bearish with regards to the overall direction the economy will be taking as we move into 2024.

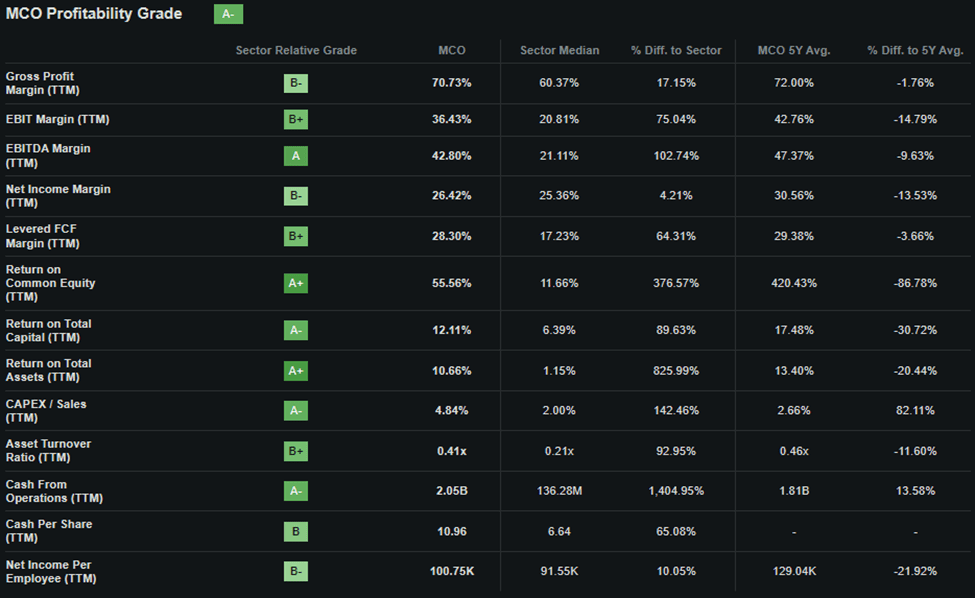

Seeking Alpha | MCO | Profitability

{kind=link}

Seeking Alpha’s Quant calculates an “ A- ” profitability rating for Moody’s which I believe to be a mostly accurate representation of the firm’s ability to generate profits. However, I must admit that I do believe an A+ rating would be more representative given the firm’s outstanding margins, returns and overall FCF.

When considering Moody’s balance sheets, it is clear that the firm is incredibly well run with conservative asset allocation leading to a fiscally robust firm.

The firm has $4.03B in total current assets while total current liabilities amount to just $2.27B. This excellent short-term liquidity leaves Moody’s with a superb quick ratio of 1.61x and a current ratio of 1.78x.

These liquidity metrics are particularly impressive when compared to S&P’s quick and current ratios of just 0.80z and 0.92x respectively which highlights just how well managed Moody’s is as a firm.

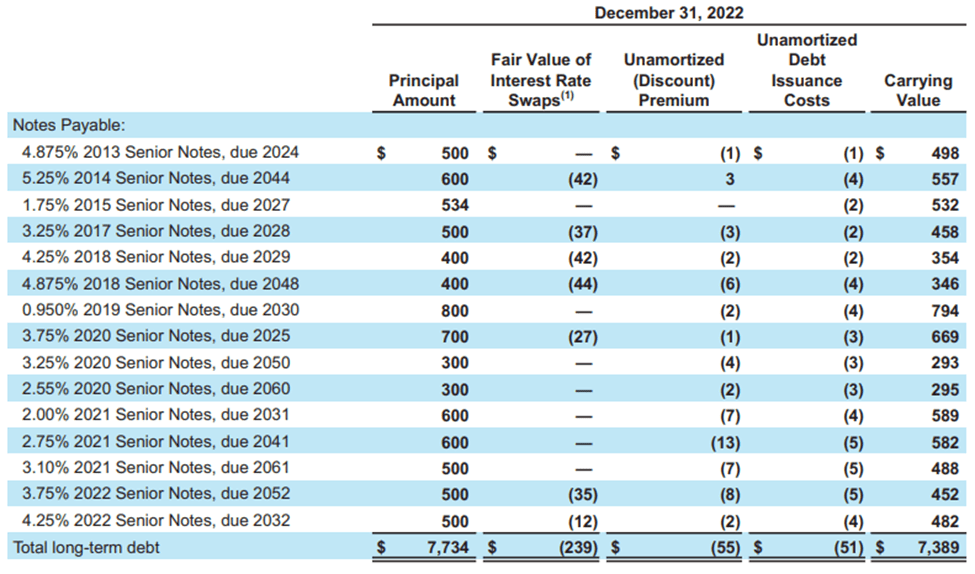

Moody’s total assets amount to $14.2B with total liabilities just $10.84B of which $7.1B is long-term debt. The firm has just $3.35B in total shareholders’ equity. This leaves the firm with a debt/equity ratio of 2.28x which traditionally speaking, would be quite an elevated figure.

{kind=link}

The majority of Moody’s long-term debt has been taken on through the 2017 acquisition of Bureau van Dijk , a European private company data issuer. This acquisition was largely accomplished to bolster the breadth of services present in Moody’s MA business segment.

While their total long-term debt is relatively large, almost all of the firm’s debentures are on fixed-rates which significantly protect the firm from a higher-for-longer interest rate environment.

Furthermore, the table above illustrates just how well staggered their debt profile is with a majority of notes maturing well after 2027. Given how well managed Moody’s debt is, I am not concerned about their elevated debt equity ratio.

Seeking Alpha | MCO | Dividend

{kind=link}

Moody’s also pays a healthy dividend to its investors. The firm has continued growing their dividend for 14 years with a dividend yield FWD of 0.84% and an annual payout FWD of $3.08.

While the 11.84% 5Y growth rate is outstanding, the overall yield is still quite low. Furthermore, an acute economic downturn would almost certainly lead to Moody’s pausing or decreasing their dividend.

I eagerly await the Q4 earnings report which will significantly expand the ability for investors to understand how well Moody’s has managed to navigate a tough difficult macroeconomic environment along with some more guidance hopefully being issued for the coming fiscal year.

Valuation

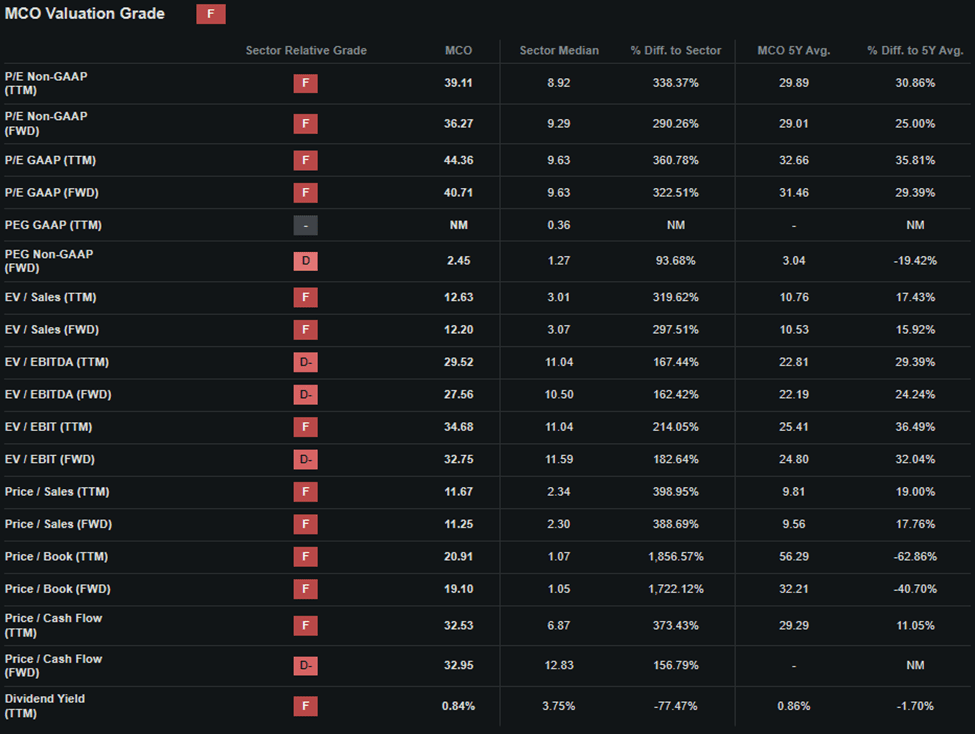

Seeking Alpha | MCO | Valuation

{kind=link}

Seeking Alpha’s Quant assigns Moody’s with an “ F ” Valuation grade. I believe that while the quant’s relative grade may be slightly pessimistic, it is undeniable that by analyzing Moody’s valuation metrics the firm certainly doesn’t seem to be a deep-value opportunity at present.

The firm currently trades at a P/E GAAP FWD ratio of 40.71x. This represents a 29% increase in the firm’s P/E ratio compared to their running 5Y average.

Moody’s P/CF TTM of 32.95 is also quite elevated currently around 11% above the 5Y running average. Their FWD EV/EBITDA FWD of 27.56x is also quite high indeed resting around 25% above the 5y average. The firm’s Price/Sales FWD of 11.25x is also a little high for my liking.

Considering these basic valuation metrics alone it would appear as though Moody’s is slightly overvalued relative to the firm’s peers and historic metric scores.

Seeking Alpha | MCO | Advanced Chart

{kind=link}

From an absolute perspective, Moody’s shares are trading at a slight discount relative to previous valuations with current share prices of around $364.55 representing a slight drop from mid-2022 highs.

When compared to the 73% growth seen in the S&P 500 tracking SPY index over the past five years, Moody’s has outperformed the U.S. market index as a whole by over 70%.

While the relative valuation provided by simple metrics and ratios along with the absolute comparison allow for a basic understanding of the value present in Moody’s shares to be obtained, a quantitative approach to valuing the stock is essential.

The Value Corner

By utilizing The Value Corner’s specially formulated Intrinsic Valuation Calculation, we can better understand what value exists in the company from a more objective perspective.

Using the firm’s current share price of $213.10, an estimated 2024 EPS of $11.15 , a realistic “r” value of 0.16 (16%) and the current Moody’s Seasoned AAA Corporate Bond Yield ratio of 5.61x, I derive a base-case IV of $353.00. This represents what is almost precisely a fair valuation in the firm.

When using a more pessimistic CAGR value for r of 0.14 (14%) to reflect a scenario where a globally spanning recession causes Moody’s MIS revenue growth to drop, shares are valued at around $318.10 representing a 15% overvaluation in shares.

Considering the valuation metrics, absolute valuation and intrinsic value calculation, I believe that Moody’s is currently trading somewhere between a fair valuation and a modest overvaluation.

In the short term (3-12 months), I find it difficult to say exactly what may happen to the firm’s valuation. As 2023 winds to a close, the uncertainty around a recession occurring in 2024 along with how hard such a macroeconomic environment may bite the economy means forecasting a short-term direction for the stock is incredibly difficult.

Given that Moody’s MIS revenues in particular can be quite cyclical, an economic downturn could lead to negative revenue growth or flatline results at best.

In the long-term (2-10 years), I believe Moody’s will continue to be an unavoidable element of the global financial industry. Their services are truly a necessary component of the daily lives of most investors and financial institutions which makes future growth almost guaranteed for the firm.

Furthermore, their continued expansion further into the analytics industry should allow the firm to generate more stable incomes while simultaneously growing their business reach even more.

Risks Facing Moody’s

Moody’s faces some tangible threats with exposure to a cyclical market environment and governance concerns generating the most risk for the firm.

The company’s MIS segment’s revenues in particular are highly reliant on the issuance of bonds and the subsequent need for ratings on these bonds in order for them to be sold to investors. The cyclical nature of bond issuance means that declining bond issuance rates may have a negative impact on the overall profitability of the MIS segment.

While the MA segment helps protect Moody’s from being entirely exposed to the cyclicality of the market environment, the overall drop in productivity levels associated with recessionary or bearish macroeconomic environments still suggests revenues may fall across the board during such market conditions.

Of course, while these threats are not particular to Moody’s and exist for essentially every single business operating in the financial sector, they must still be considered when analyzing the investability of the firm.

I also believe Moody’s faces some acute threats from an ESG perspective with minor governance concerns generating the most risk.

The 2008 financial crisis exposed ratings agencies in a manner never before seen where it became clear to investors that these companies were essentially providing excessively optimistic credit ratings in the hopes of attracting more business.

Such unethical behavior is regrettable to see and difficult to analyze from an external perspective. While changes have been made since 2008, the same unique information and data required to accurately issue credit ratings also make it difficult to see if Moody’s is accurately rating the equities presented to them.

{kind=link}

Moody's ESG information does highlight that the firm is committed to generating positive impacts on society and governance issues from their business operations and suggests that the firm has taken a much more responsible approach to business over the last 15 years.

The overall lack of any major current environmental, societal or governance concerns suggest to me that Moody’s may be a good choice for the more ESG conscious investor.

Of course, opinions may vary with regards to ESG material, and I implore you to conduct your own ESG and sustainability research before investing in Moody’s if these matters are of concern to you.

Summary

Moody’s is a truly unique business that has not only cemented their position in a lucrative segment of the financial market but continues to innovate and develop new auxiliary products to expand the overall service offering may made to customers.

Their ratings and analytics businesses work well together and present Moody’s with a great opportunity to benefit from tangible networking effects and a real opportunity for cross selling of services.

The firm has consistently generated great returns on their invested capital and continues to run the business well leading to massive gross, operating and net margins. When combined with excellent capital allocation strategies and a robust balance sheet, it is clear that Moody’s is an exceptionally well operated business.

Despite a difficult 2023 from a macroeconomic perspective, Moody’s has managed to generate solid earnings and is set to see overall single-digit-percentage growth in revenues.

From a valuation perspective, it is impossible to argue that any real value opportunity exists in Moody’s shares. At best, I believe the firm is fairly valued.

Still, I absolutely believe that purchasing a wonderful company at a fair price will always beat buying into a fair company at a wonderful price. Considering this underpinning investment thesis, I believe Moody’s makes for a pretty decent buying opportunity even at current prices.

Therefore, I rate this ratings business a Buy at present with a Strong Buy rating being initiated once the intrinsic value calculation suggests a tangible (around 10%) undervaluation exists in shares.

For further details see:

Moody's: It's Time To Rate This Ratings Agency