SPGI - Moody's: Supreme Business Continuing To Compound

2023-06-15 00:52:40 ET

Summary

- Moody's Corporation is a high-quality business with a high portion of recurring revenue, and its current financial weakness is expected to normalize in the coming year before growth returns in 2024.

- MCO's Moody's Analytics segment is a key growth driver, with strong retention rates and potential for upselling, while the Moody's Investor Services segment faces near-term uncertainty due to macroeconomic conditions and a decline in debt market activity.

- Moody's Analytics is continuing to develop, and we believe the current c.10% ARR growth trajectory should continue as innovation drives the value of analytics.

- Despite its strong financial performance and market positioning, MCO is currently trading at a steep premium, suggesting that the stock may be marginally overvalued.

Investment thesis

Our current investment thesis is:

- MCO is a high-quality business with a high portion of recurring revenue. ARR is growing at c.10% (in the MA division) while the MIS division is essentially a call option of market prosperity.

- The current financial weakness is a reflection of a reduction in activity in the debt market. We expect this to normalize in the current year before growth returns in 2024.

- MCO's impressive margins will fund consistent dividends and buybacks.

Company description

Moody's Corporation ( MCO ) is a global risk assessment firm that operates in two main segments: Moody's Investors Service and Moody's Analytics.

The Moody's Investors Service segment is responsible for publishing credit ratings and providing assessment services for various debt obligations and entities that issue them, including corporate, financial institution, and governmental obligations, as well as structured finance securities.

The Moody's Analytics segment focuses on developing products and services that support risk management activities for institutional participants in financial markets. This includes subscription-based research, data, and analytical products such as credit ratings, credit research, quantitative credit scores, economic research and forecasts, business intelligence, company information products, commercial real estate data and analytical tools, and learning solutions.

Share price

MCO's share price has generated impressive returns across the last decade, as Management has executed an impressive strategy of financial optimization and capital allocation.

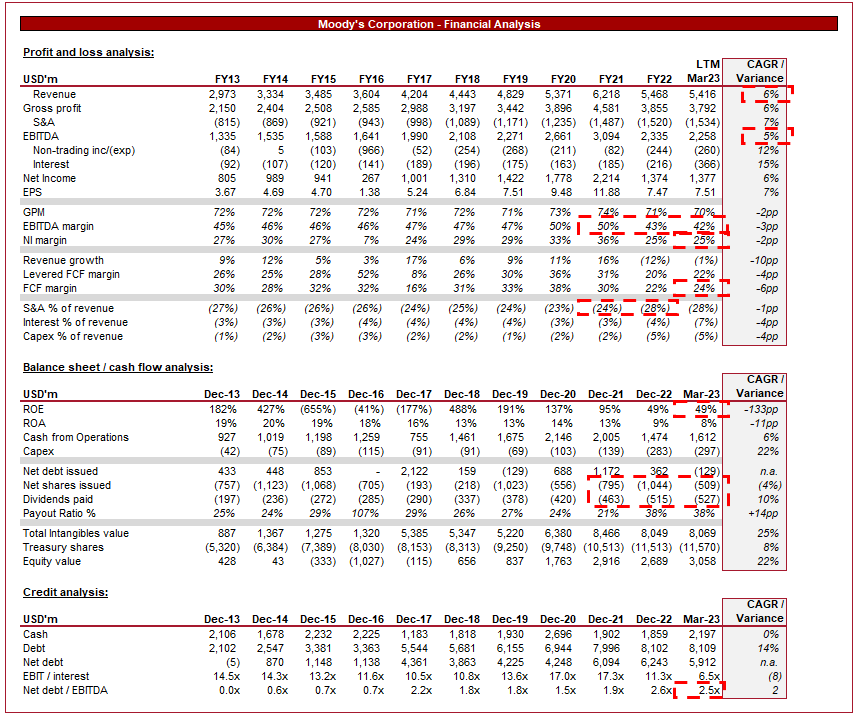

Financial analysis

{kind=link}

Moody's Corporation financial analysis (Tikr Terminal)

Presented above is MCO's financial performance for the last decade.

Revenue & Commercial Factors

MCO's revenue has grown at a CAGR of 6%, with only 2 years with <3% growth. MCO is within a duopoly in the credit rating industry alongside S&P Global ( SPGI ), affording the business impressive scale and pricing economics.

MCO's business is split into two primary divisions. Moody's Analytics is a subscription-based service provided to markets, generating lucrative recurring revenue with low churn. Moody's Investor Services on the other hand is the provision of credit ratings, analysis, etc. For this reason, the segment is volume-driven and thus exposed to factors that can influence changing demand for ratings.

Revenue split (Moody's Corporation)

Moody's Investor Services

The MIS segment of the business has experienced a decline in FY22, contributing to the overall revenue decline for MCO.

The value of issuances has declined by (13)% in Q1'23, continuing the negative trend experienced in FY22. This is driven by macroeconomic conditions, contributing to the current bear market.

MIS issuance (Moody's Corporation)

Inflationary pressures have led to consistent interest rate hikes following a decade of record-low rates. As this occurs, the cost of capital increases, contributing to an increase in the cost of servicing interest payments. This is compounded by the economic effects of higher interest rates, which is generally a softening/decline in economic conditions. This elevates the risk to financers (businesses for example face lower revenues/growth while costs increase, leading to a higher risk of liquidity issues). For this reason, we see debt markets begin to close as the ability to raise debt significantly declines. This is what is happening now, there is no longer the availability of cheap debt.

MIS Revenue (Moody's)

We are most concerned with exotic products such as structured instruments, leveraged debt, and high-yield bonds. These have become problematic as default rates soar. Further, despite MCO seeing healthy demand from infrastructure lenders, we remained concerned due to the cost of financing and the work-from-home trend impacting commercial properties. Finally, weaknesses in the bank sector in recent months have caused near-term uncertainty.

Looking ahead, we expect rates to remain elevated for much of the year, owing to the stubbornness of inflation, which is declining but slowly. Our expectation is for issuances to normalize in the coming quarters, if not improve.

There are several reasons for this. Firstly, uncertainty around the trajectory of inflation has declined. Markets love certainty and so the closer we move toward certainty, the lower the pricing premium associated with risk (higher prices, lower volume). In the UK, for example, mortgage rates are beginning to decline despite the country continuing to lift rates. Further, many businesses face no choice but to refinance their current facilities, with MCO estimating c.$4t is needed in the coming 3 years. This is propelled by the long period of low rates, which encouraged the raising of finances. Finally, S&P Global estimates that global private equity dry powder has reached a record $2t. These funds will need to be invested in the coming years, supported by debt financing.

Moody's Analytics

MA is the crown jewel of the MCO enterprise. The highly recurring (88% of revenue) and sticky revenue (retention rate of 93%) is an investor's dream. Given MCO's scale and deep expertise, markets have little choice but to choose MCO for its data, analytics, and insight. Further, many will have several data sources, significantly increasing the likelihood MCO is one.

The MA and MIS businesses are highly complementary in this regard, as MCO is able to illustrate its expertise to markets through its rating services while developing tangential services.

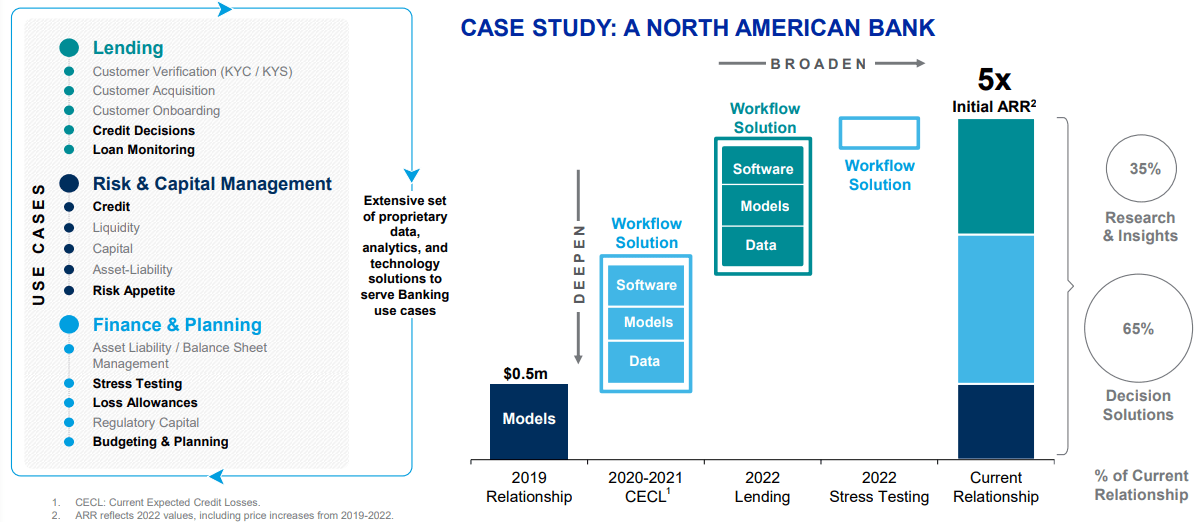

Investment in the development of these data services is critical, as value is achieved through expanding the breadth of expertise and target market. As AI, machine learning, and other factors continue to drive data analysis, the pressure to provide real-time, bespoke, and actionable insight will increase. This represents an opportunity to significantly increase the company's value proposition while also representing a risk if MCO is unable to innovate in line with peers. Management has been developing both the breadth of services provided, as well as the level of insight and analytics provided in order to support decision-making.

Recurring revenue models are judged on their ability to achieve generate growth, achieve strong retention, and have sufficient scope for upselling. Growth has been strong, with ARR continuing to outstrip revenue (double-digit growth). Further, we expect retention to remain at its current level, if not improve, given the lack of alternatives. Finally comes upselling. As mentioned previously, the MCO services suit continues to develop as a means of supporting actionable decision-making for its clients. The following case study illustrates MCO's upselling scope, with breadth providing tangential support while investment in expertise deepens the quality of the service.

{kind=link}

Upselling potential (Moody's Corporation)

Other factors

Environmental, social, and governance ((ESG)) considerations have gained prominence in investment decision-making. Pressures from investors, as well as changing social views and regulation has contributed to increased ESG investing. For this reason, there has been an increase in demand for related services such as data insight, as well as rating services. MCO has invested in the development of its capabilities, in part through acquisitions. We believe this will be a growth area in the coming years.

Expansion of emerging markets will also represent a key opportunity for the business. As we see continued economic expansion in the developing world, markets will follow suite, seeking maturity as a means of attracting external investment. MCO is positioned well to provide its services to this growing list of businesses.

The Regulatory Landscape remains a key risk to the business. Pressures for increased regulatory scrutiny and oversight on credit rating agencies continue following a series of high-profile failures ( SVB had a favorable rating by MCO at the time it collapsed ).

Margins

MCO's margins are fantastic. Across the historical period, the company has consistently achieved an EBITDA-M in excess of 45% and a NIM of c.27%. This is a reflection of the company's superior market positioning and the high barriers to entry. It is almost impossible for new entrants to challenge MCO / S&P, given their expertise and the market's trust in these two.

The slippage in the most recent period is due to the weakness faced due to market conditions, impacting rating activity in higher-margin products. Further, there is a degree of renewal timings on subscription products.

Balance sheet

Management has deftly allocated capital over the historical period, with consistent share buybacks married with a growing dividend. MCO's current debt position is manageable, with an ND/EBITDA ratio of 2.5x.

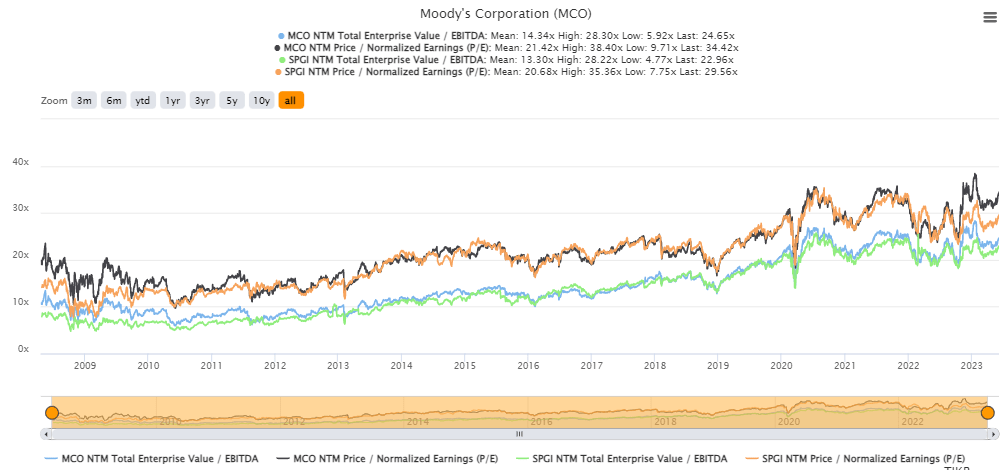

Valuation

{kind=link}

MCO Valuation (Tikr Terminal)

MCO and SPGI have traded in parallel for most of the decade. The companies are trading at the following premiums to historicals currently.

| MCO |

| SPGI |

| NTM EBITDA |

| 72% |

| 73% |

| NTM P/E |

| 61% |

| 43% |

| LTM EBITDA |

| 104% |

| 74% |

| LTM P/E |

| 77% |

| 244% |

As the above suggests, the mean divergence has significantly increased, primarily due to investor confidence remaining alongside a decline in performance.

In our view, the NTM multiples are a better indicator for relative value. In this case, MCO is trading at a steeper premium relative to SPGI. A premium is certainly warranted given the improvement in financial performance, alongside increased recurring revenue. However, a 72%/61% premium appears inflated.

Final thoughts

MCO has been one of the best investments in the last decade. It is favored by a host of value investors including Warren Buffett and Chuck Akre. The company's expansion of its recurring revenue streams has been highly successful and so long as ARR growth remains strong, revenue will follow suit.

The variability of MIS is not ideal but contributes to financial strength during a growing market. Most businesses struggle during a downturn and all things considered, we believe MCO is resilient.

With a high-quality business such as this, getting it at a discount is unrealistic. However, we believe the business to be marginally overvalued. A 72%/61% premium to the historical average looks beyond an appropriate maximum.

For further details see:

Moody's: Supreme Business Continuing To Compound