CA - Moon Capital - First Horizon: Balance Sheet Capacity Sets It Apart

2023-07-26 09:00:00 ET

Summary

- Despite the banking industry's struggles, bank profits reached an all-time high of $80 billion in Q1 2021, with earnings up 15% YoY, largely due to the surge in interest rates.

- First Horizon Corporation is viewed as a bank set to perform well in the current rate environment, with robust deposit bases, significant variable rate loans, and a diversified commercial office market exposure.

- First Horizon's uninsured deposits are unlikely to migrate away from the bank, and its balance sheet can withstand a significant increase in funding costs, setting it apart from recently failed banks.

The following segment was excerpted from this fund letter.

First Horizon Corporation ( FHN )

Last quarter, we discussed several banks that fell victim to the Federal Reserve's rapid raising of interest rates. With three banks having been recently put into receivership and many others struggling due to misplaced interest rate bets, it is easy to see why many observers are bearish on the entire banking industry.

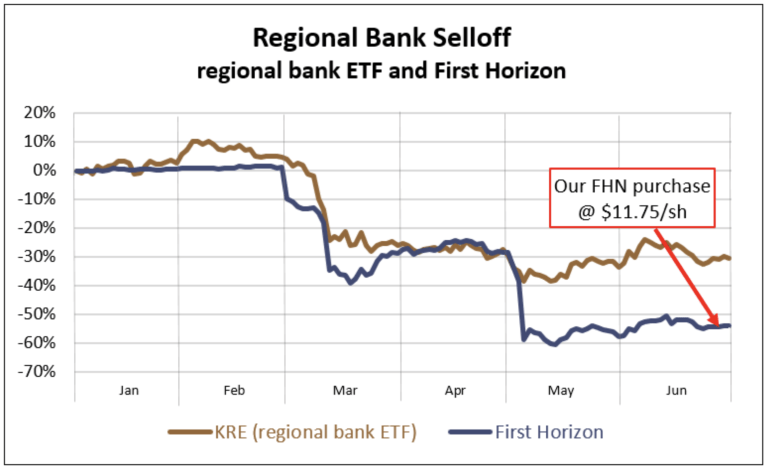

From its high, this February, the S&P Regional Banking ETF ( KRE ) was off 43% at its low in May, its largest drop since the 50% selloff during the 2007-09 Great Financial Crisis. What has been largely absent from the discussion of company-specific banking woes and larger systemic risks such as deposit runs has been the mention of industry profitability as a whole. Given the overall negative news about U.S. banks, few would guess that bank profits reached an all-time high of $80 billion in the first quarter of this year.

Adjusting for one-time gains related to the acquisition of banks in receivership, earnings are up 15% year-over-year. This earnings strength stems from the very factor that has left some banks on life support: the surge in interest rates. While this rise spells catastrophe for banks that loaded their portfolios with long-duration, fixed-rate investments, it benefits banks that were properly positioned, as it allows them to earn higher interest income. As banking analyst Steve Eisman aptly summed up the current situation "We are not having a banking crisis. We are having a crisis with certain banks."

{kind=link}

Historically, most bank failures were caused by credit losses, an issue that was largely absent in the three high-profile bank failures earlier this year. While there are looming concerns about weakness in the commercial office market (an area in which many regional banks are generally overexposed - more on that below), non-performing loans have yet to jump materially, and banks are better capitalized and hold more liquidity than in times preceding prior crises.

Commercial real estate defaults are likely to increase in the coming years, but most banks are well-provisioned for potential increases. Despite the economy having yet to experience any meaningful credit cycle stress, shares of regional banks have largely collapsed, creating a situation that offers some unique opportunities. We took advantage of the indiscriminate selloff in regional bank stocks and purchased shares in First Horizon Corporation ( FHN ) following the termination of its merger agreement with Toronto-Dominion Bank ( TD ).

By our judgment, First Horizon fits squarely in the group of banks set to perform well in the current rate environment - those with robust deposit bases that operate in pro-growth markets and carry significant variable rate loans. We view First Horizon as even further discounted than its cheap peer group, solely due to the uncertainty surrounding the unsuccessful TD merger; we expect that this discount will be resolved over time.

Finally, FHN's exposure to the commercial office market is much smaller and diversified differently than the typical regional bank.

{kind=link}

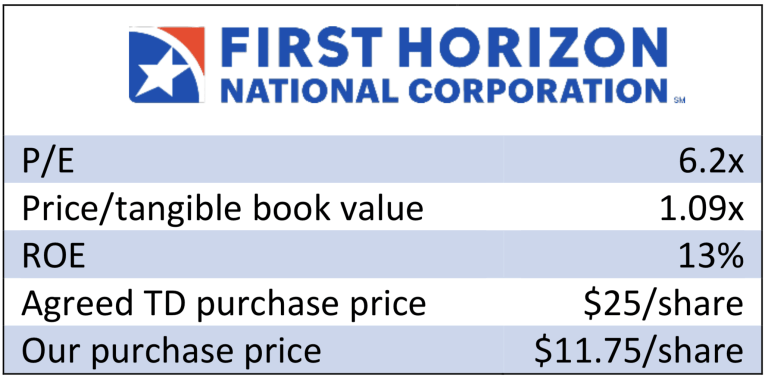

We purchased our shares at prices around First Horizon's tangible book value which, when adjusted for the $225 million fee Toronto Dominion paid to terminate the merger agreement, is roughly $11.70 per share. As a well-run bank that consistently posts returns on equity in the mid-teens, FHN has historically traded well above book value (typically 1.5-2x). For reference, at the time of the merger offer, TD was eager to pay 2.1x tangible books for the company.

When the merger fell through, FHN's price dropped more than 50%, allowing us to buy our shares at approximately tangible book value - and less than half of what TD originally agreed to pay. While both earnings and book value multiples have compressed among regional banks, First Horizon is still positioned to earn well more than $1 billion annually. With a current market capitalization of around $6 billion, this equates to a P/E ratio of six.

Over the past few years, FHN has executed admirably. Instead of extending the duration of its portfolio when yields were near all-time lows, the company parked excess cash at the Fed, which temporarily reduced earnings. Avoiding this reach for yield has paid off, as it has left the bank with minimal "held-to-maturity" losses, which is not the case for many banks. First Horizon has also properly positioned its loan book to benefit from higher rates. In the most recent quarter, the company's net interest margin increased 150 basis points year-over-year, helping it generate a return on equity of 17% (19%, if adjusted for acquisition-related costs).

First Horizon has a valuable deposit franchise with a large base of sticky, noninterest-bearing deposits. In the most recent quarter, the company's total deposit cost was 111 basis points, which allowed it to earn a net interest margin approaching 4%. As a 100-year-old institution, we believe the composition of First Horizon's deposit base is fundamentally different from those of recently failed banks that grew their deposit bases significantly by way of "hot" venture capital money prior to collapse.

First Horizon's top 15 accounts represent just one percent of deposits, a stark contrast to Silicon Valley Bank, which had $13 billion in uninsured deposits from just its top ten depositors. During FHN's recent analyst day, management noted that the company has seen no change in deposit outflows or client relationships since it reported first-quarter results from March. (In addition to deposits and client relationships, First Horizon has also retained its senior-level employees, despite the collapse of the TD acquisition.

From the date of the merger announcement through May 2023, FHN has lost no regional presidents and only 1% of the executives in its top two management tiers.)

A concern among many bank analysts is the effect of work-from-home policies on the overall demand for general office space. Increasingly empty buildings reduce landlords' ability to service the debt used to purchase those buildings. While First Horizon has substantial exposure to the commercial real estate market, only $2.8 billion of its total loan portfolio of $59 billion in office exposure. Of those office loans, roughly half are considered medical office, a market segment that doesn't face the same work-from-home issues challenging general commercial office space tenants and landlords. (It's hard for a surgeon to work from home.) Adjusting for medical loans, FHN's office exposure is well below that of the typical regional bank.

FHN also has a strong market share in pro-growth areas that will likely face fewer commercial real estate issues than some of the larger markets that we expect to be more problematic. (According to a recent Bloomberg study, the Southeast accounted for more than two-thirds of all job growth across the US since 2020 and is now home to 10 of the 15 fastest-growth cities. Additionally, FHN has no exposure in either California or New York.) Moreover, the majority of FHN's loan book consists of floating-rate loans, with 70% of the portfolio expected to reprice within the next year. That is, higher interest rates should provide an earnings boost to FHN.

Additionally, FHN excels in credit evaluation compared to its peers, with an impressively low percentage of non-performing loans, currently standing at only 54 basis points.

One area of concern for FHN has been its relatively large base of uninsured deposits, which represent approximately 41% of its total deposit base. It was a combination of a rapid withdrawal of massive amounts of uninsured deposits and a precipitous drop in the value of its investment portfolio that proved fatal to Silicon Valley Bank. First Horizon doesn't face either of those threats.

While we view FHN's uninsured deposits as unlikely to migrate away from the bank, if it happened the company's substantial interest income provides the ability to easily replace any lost deposits, albeit at a cost. What sets First Horizon apart from recently failed banks is its balance sheet's capacity to withstand a significant increase in funding costs. In contrast, now-defunct banks such as Silicon Valley had locked their balance sheets into low-yielding assets that higher interest rates rendered permanently impaired.

To illustrate a worst-case scenario, let's assume that depositors withdrew 80% of the uninsured deposits at FHN. The company could replace that capital by borrowing from the Federal Reserve at 5% (versus its current 1.7% cost of interest-bearing deposits), resulting in an increased annual interest cost of approximately $600 million - or a temporary hit of less than 50% of the company's net income.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Moon Capital - First Horizon: Balance Sheet Capacity Sets It Apart