DLA - Movado Group: Still Attractive Despite Fundamental Deterioration

2023-06-30 00:07:26 ET

Summary

- Movado Group's shares have significantly dropped in recent months, despite the company's solid financial performance in the previous fiscal year.

- The company's financial performance in the first quarter of the 2024 fiscal year has been disappointing. Management expects overall revenue for the fiscal year to decline by 1.9%, and net profits to reduce by 32.8%.

- Despite the negative outlook, I maintain a 'buy' rating for Movado Group. The company has no debt and holds $198.3 million in cash and cash equivalents.

- I believe that MOV stock is cheap on an absolute basis and fairly valued compared to similar firms, making it a potentially good long-term investment.

One of the worst feelings when it comes to investing is going long a stock, only to see shares plummet. Sometimes or to some extent, the decline in price is warranted. But other times, it's not. One case that I could point to where some decline was probably justified, but not to the extent we have seen, involves watch manufacturer Movado Group ( MOV ). Over the past few months, shares of the company have plummeted while the S&P 500 has appreciated. To some extent, a move lower was justified because sales, profits, and cash flows, all took a leg lower. And in all likelihood, that pain will persist throughout this year. Many investors may take this as a cue to sell out of their positions and move on. But I would argue that shares of the company are still cheap enough to warrant attractive upside, even though they might be closer to fairly valued relative to similar firms.

A look at recent pain

Back in the middle of February of this year, I took a rather bullish stance on Movado Group. In the article that I wrote about the business, I acknowledged that the company had done really well from a share price perspective, even though financial data up to that point had been a bit discouraging. From the time I had written about the company previously in June of 2022, shares were up 13% compared to the 8.7% seen by the S&P 500. Even with that move higher, however, I believed that the stock probably offered additional upside from that point. That led me to keep the business rated a 'buy'. Since then, the market has decided to take things in the opposite direction. The S&P 500 has risen another 4.6%. By comparison, Movado Group has seen its share price plummet 17.6%.

{kind=link}

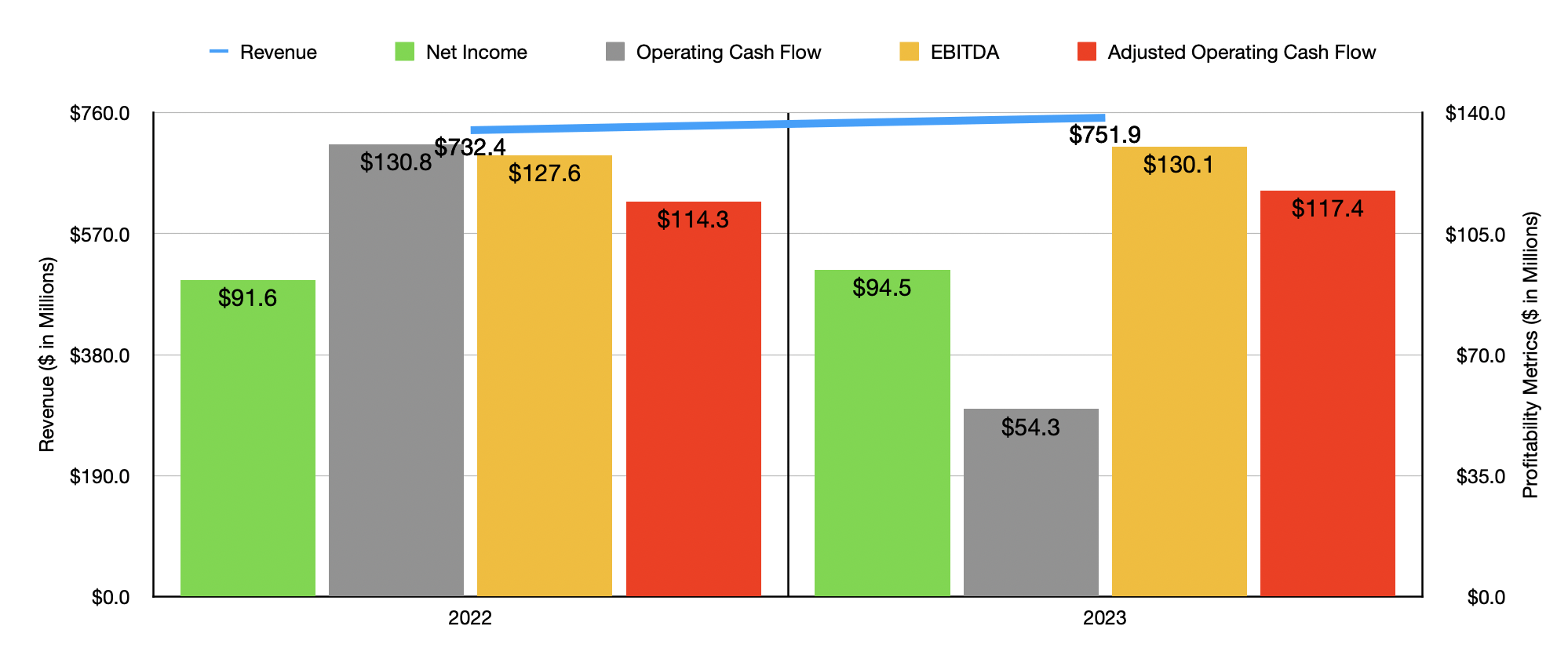

This is rather discouraging when you consider how the company performed during its 2023 fiscal year . Revenue of $751.9 million beat out the $732.4 million the company reported one year earlier. Net profits grew from $91.6 million to $94.5 million. It is true that operating cash flow more than halved from $130.8 million to $54.3 million. But if you adjust for changes in working capital, you would see this number inch up from $114.3 million to $117.4 million. And finally, EBITDA for the company expanded from $127.6 million to $130.1 million.

{kind=link}

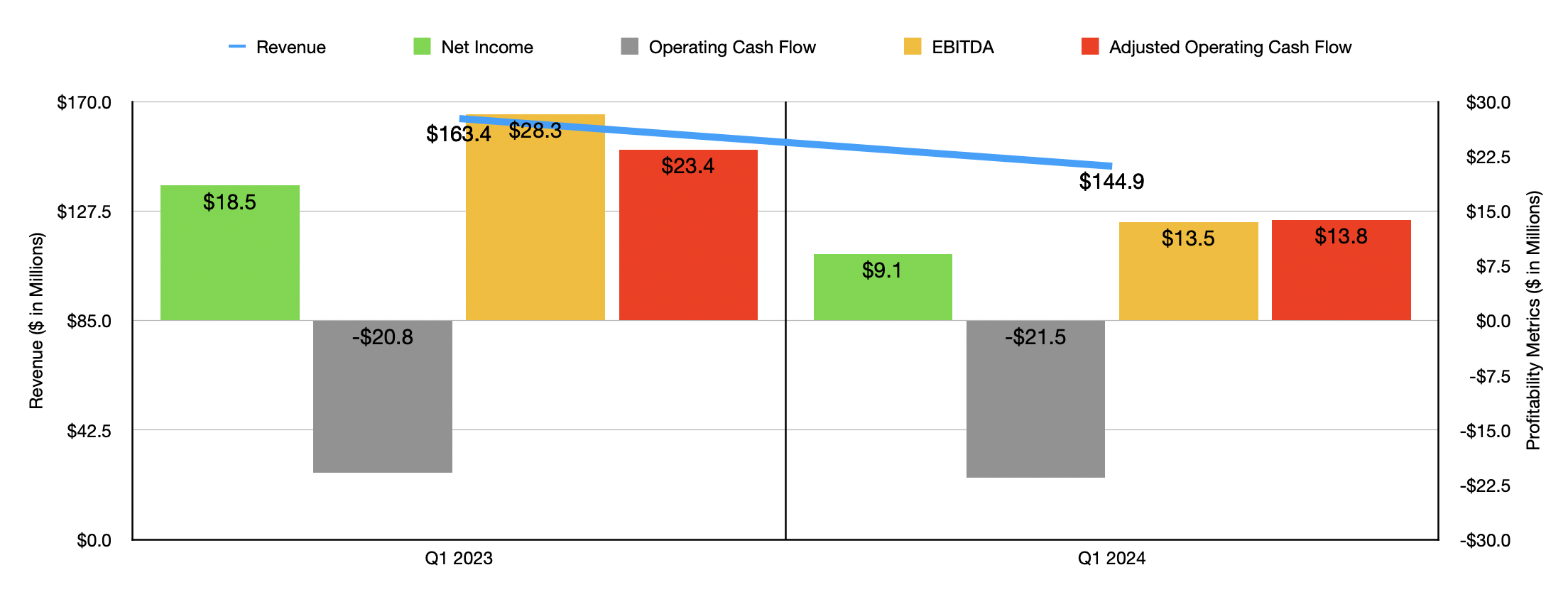

The picture for the company changed, however, once we entered the 2024 fiscal year. Consider revenue. During the first quarter of the year, sales came in at $144.9 million. That's 11.3% lower than the $163.4 million generated the same quarter last year. Really, the company experienced weakness across all of its major sales categories. For instance, revenue associated with its owned brands dropped from $53.2 million to $45.1 million. Sales associated with licensed brands fell from $88.8 million to $80.2 million. After sales services and all other activities reported a decline from $1.4 million to $220,000. For the Watch and Accessory Brands segment as a whole, the decline in sales totaled 12.4%. Management attributed this to decreased volumes resulting from a reduction in demand from the firm's wholesale customers both here at home and abroad. Lower online retail sales, as well as foreign currency fluctuations, also hit the business.

This drop in sales also brought with it a decline in profitability. The company's net profits, for instance, were cut by more than half from $18.5 million to $9.1 million. A decrease in the company's gross profit margin of 260 basis points was driven by an unfavorable change in product mix, foreign currency fluctuations, and decreased leveraging of fixed costs because of the decline in volume. The drop in profits for the company also brought with it a decline in cash flow. Operating cash flow went from negative $20.8 million to negative $21.5 million. If we adjust for changes in working capital, we would see that number fall from $23.4 million to $13.8 million. Meanwhile, EBITDA for the company declined from $28.3 million to $13.5 million.

When it comes to the 2024 fiscal year in its entirety, management has some bearish expectations . They expect overall revenue to come in at between $725 million and $750 million. At the midpoint, that would translate to a year over year decline of only 1.9%. However, earnings per share are expected to come in at between $2.70 and $2.90. At the midpoint, that would translate to net profits of $63.5 million. That's a 32.8% reduction compared to what the company generated in the 2023 fiscal year. No guidance was given when it came to other profitability metrics. But estimates that I created have adjusted operating cash flow coming in at $78.9 million, while EBITDA should come in at about $87.4 million.

{kind=link}

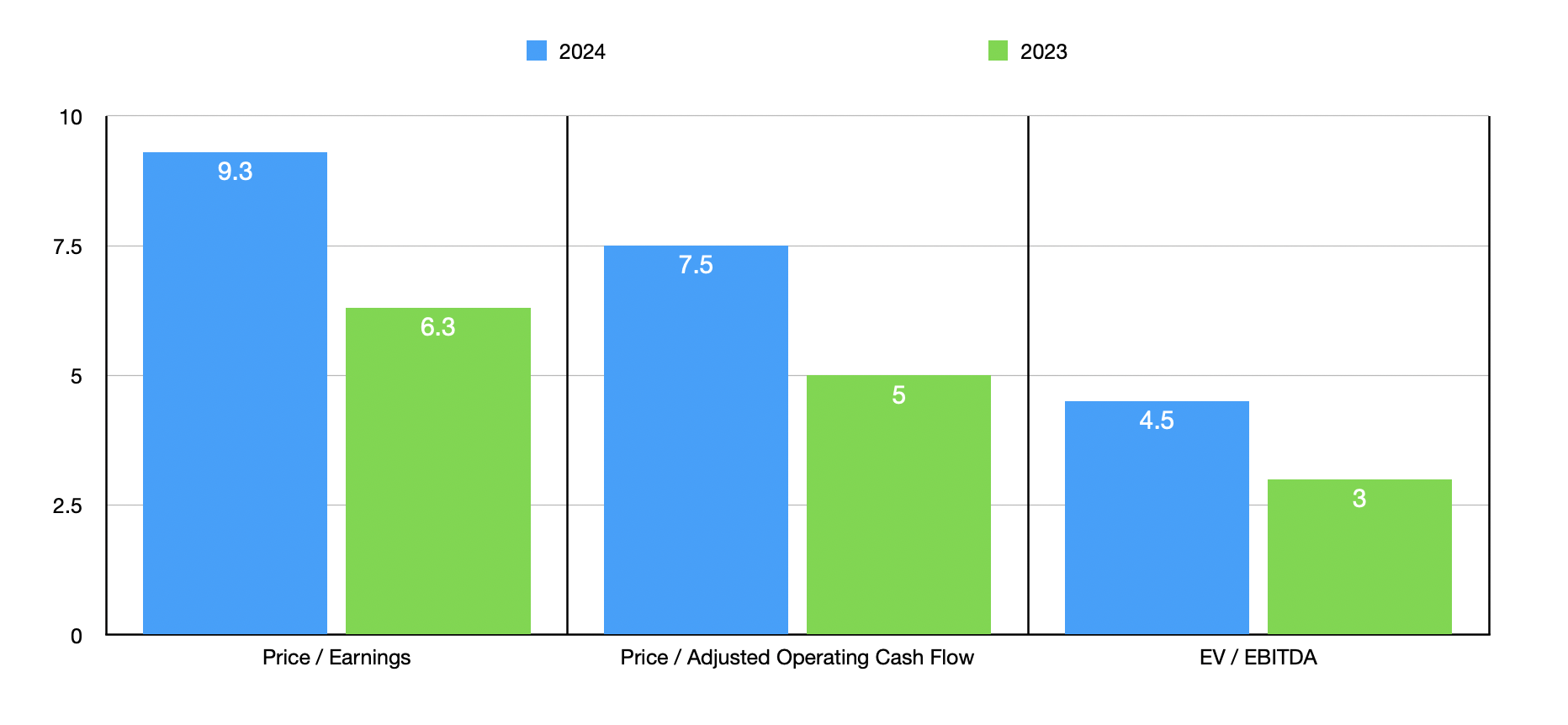

Taking these numbers, it's easy to value the company. The firm is trading at a forward price to earnings multiple of 9.3. That's up from the 6.3 reading we would get using data from last year. The price to adjusted operating cash flow multiple should rise from 5 to 7.5, while the EV to EBITDA multiple should increase from 3 to 4.5. As part of my analysis, I also created the table below. In it, I decided to compare the company with five similar firms. Generally, I would prefer to use the most recent completed fiscal year since the companies I am comparing it to utilize the trailing 12-month data. But given how much the trading multiples of Movado Group are slated to increase, I would prefer to be overly conservative and use the forward estimates for it. On this basis, using all three of the methods, three of the five companies ended up being cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Movado Group |

| 9.3 |

| 7.5 |

| 4.5 |

| G-III Apparel Group ( GIII ) |

| 4.5 |

| 10.8 |

| 4.4 |

| Superior Group of Companies ( SGC ) |

| 11.8 |

| 4.9 |

| 61.9 |

| Delta Apparel ( DLA ) |

| 6.3 |

| 99.2 |

| 13.0 |

| Vera Bradley ( VRA ) |

| 11.3 |

| 3.7 |

| 1.8 |

| Signet Jewelers ( SIG ) |

| 6.2 |

| 6.7 |

| 3.4 |

Takeaway

Fundamentally speaking, Movado Group is a solid business. The firm has no debt and it enjoys $198.3 million of cash and cash equivalents on its books. Even with the stock getting more expensive because of the pressure on its bottom line that's slated to occur this year, the stock is cheap on an absolute basis, while being perhaps fairly valued compared to similar firms. Even though this is less than ideal, the pure cheapness of the company, combined with its cash flow data from last year, makes me feel comfortable about it in the long run. So even though the stock has fallen quite a bit in recent months, I have no problem keeping it rated a 'buy' for now.

For further details see:

Movado Group: Still Attractive Despite Fundamental Deterioration