MSOS - MSOS: An Industry-Wide Catalyst Approaches

2023-11-11 06:58:56 ET

Summary

- Most of the holdings within the AdvisorShares Pure US Cannabis ETF (MSOS) have improved their cash flow situation over the last two years.

- The Federal government is in the process of rescheduling cannabis to schedule 3.

- When the rescheduling process is finished, I expect the entire industry to rally.

- I currently rate MSOS as a Buy.

Thesis

I have been intentionally avoiding cannabis ETFs and instead chose to only look at investing into individual companies. Mostly, this was done because a majority of the industry was burning cash at an alarming rate. I chose to follow a select list of players which had the most attractive business models and financials. However, many of the holdings within AdvisorShares Pure US Cannabis ETF ( MSOS ) have improved their cash flow situation and are far less terrifying as potential investments, so I have changed my tune.

The removal of the 280e tax obligation will improve the fundamentals of the entire industry. With the cannabis industry currently facing a major catalyst from rescheduling, the situation has changed enough that not only have I stopped ignoring the cannabis ETFs, I currently consider MSOS a Buy.

Fund Background

AdvisorShares Trust - AdvisorShares Pure US Cannabis ETF gains exposure to the cannabis industry by investing both directly, and uses derivatives such as swaps to create its portfolio. The fund was formed on September 1, 2020. It is actively managed and currently charges an annual operating expense of 0.86% and offers a waiver of 0.03%. This brings the net fees down to 0.83% .This non-diversified fund seeks to invest at least 80% of its net assets into companies that derive at least 50% of their net revenue from the United States cannabis industry. With the added goal of focusing at least 25% of its holdings into pharmaceuticals, biotechnology & life sciences.

MSOS Fund Profile (Seeking Alpha)

{kind=link}

Holdings

These values were pulled from their website on November 9th, 2023. With 72.5% of their holdings in just 4 companies and 85.48% of their holdings in just 6 companies, the fundamentals of these few companies are incredibly important.

MSOS Holdings (Advisorshares.com)

{kind=link}

Green Thumb Industries ( OTCQX:GTBIF ) is at 26.80%

Curaleaf Holdings ( OTCPK:CURLF ) is at 18.30%

Verano Holdings ( OTCQX:VRNOF ) is at 15.69%

Trulieve Cannabis ( OTCQX:TCNNF ) is at 11.71%

TerrAscend Corp ( OTCQX:TSNDF ) is at 7.56%

Cresco Labs ( OTCQX:CRLBF ) is at 5.42%

Glass House Brands ( OTC:GLASF ) is at 2.99%

Ayr Wellness ( OTCQX:AYRWF ) is at 2.95%

Cannabist Company ( OTCQX:CBSTF ) is at 2.19%

Jushi Holdings ( OTCQX:JUSHF ) is at 2.18%

Planet 13 Holdings ( OTCQX:PLNH ) is at 1.61%

4Front Ventures ( OTCQX:FFNTF ) is at 1.04%

C21 Investments ( OTCQX:CXXIF ) is at 0.43%

MariMed ( OTCQX:MRMD ) is at 0.23%

Vext Science ( OTCQX:VEXTF ) is at 0.21%

Goodness Growth ( OTCQX:GDNSF ) is at 0.16%

Acreage Holdings ( OTCQX:ACRHF ) is at 0.12%

Gold Flora Corp ( OTCQX:ACRHF ) is at 0.10%

Grown Rogue International ( OTCPK:GRUSF ) is at 0.08%

RIV Capital ( OTCPK:CNPOF ) is at 0.07%

Present Fundamentals

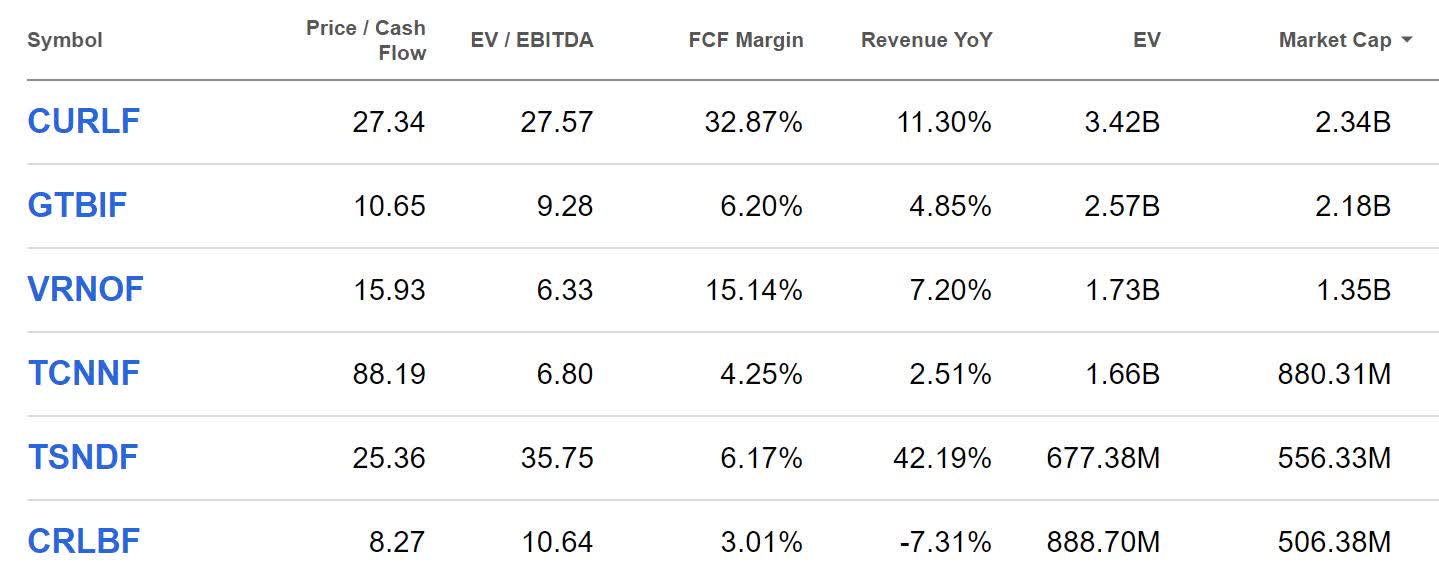

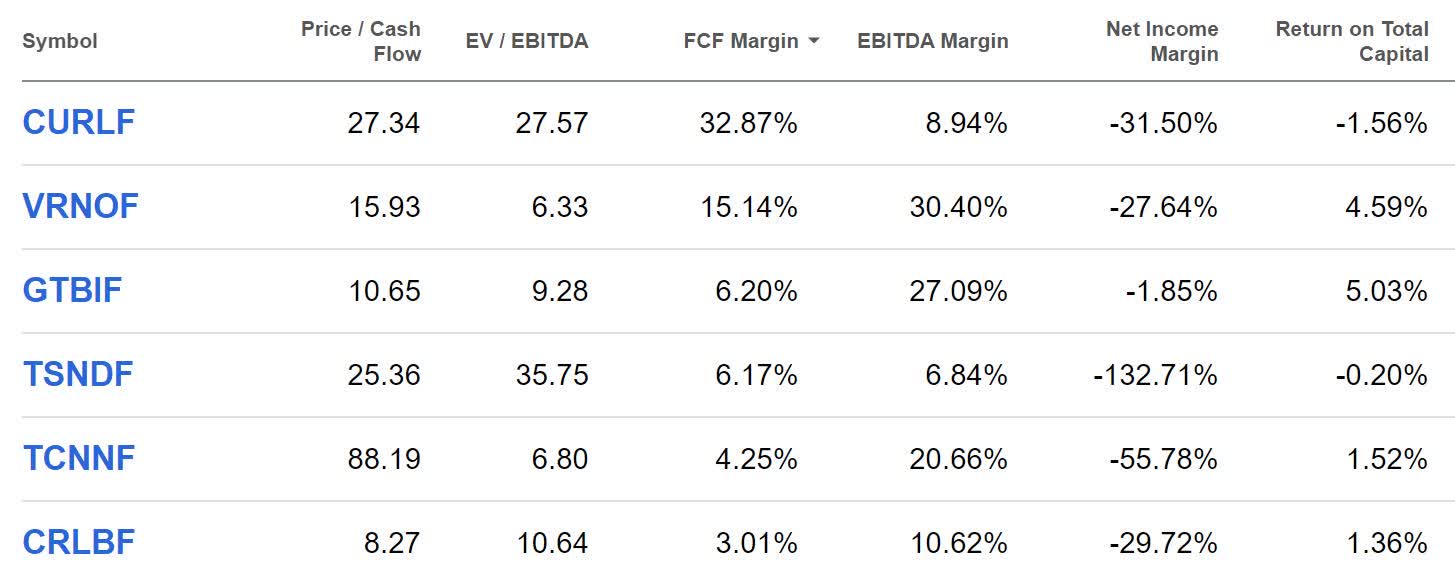

Here are the top 6 holdings sorted by Market Cap.

MSOS Top 6 Holdings Important Metrics (Seeking Alpha)

{kind=link}

A few key takeaways here:

Because of the significant differences between Market Cap and Enterprise Value, its pretty clear that Curaleaf, TerrAscend, and Cresco Labs all have an unappealing amount of debt.

Currently, only Curaleaf and Verano have attractive Free Cash Flow Margins, the others aren't even able to achieve the 10% threshold I look for when searching for attractive compounders.

TerrAscend is the only one to have managed to grow revenue at an attractive rate over the last year.

Green Thumb Industries and Curaleaf are the only ones which currently have Price/Cash Flow ratios which I could consider attractive. When viewing their EV/EBITDA ratios Curaleaf and TerrAscend both appear extremely overvalued .

Post-Rescheduling

In a post-rescheduling environment, all of these U.S. based companies are going to become significantly more attractive. The extremely oppressive 280e tax burden will go away and these companies will be able to take deductions and thus pay taxes like a normal company.

So for example Green Thumb Industries paid $25.8M in income taxes in June of 2023. The removal of 280e would allow them to be able to take deductions and have its tax burden lessened. Since they posted -$18.9M in net income the same quarter, they would have been able to avoid most of the $25.8M income taxes.

GTBIF Income Taxes (Seeking Alpha)

{kind=link}

Curaleaf paid $41.4M in income taxes and yet also posted -$71.2M negative net income that same quarter. Without 280e, they would have been able to avoid income taxes entirely.

CURLF Income Taxes (Seeking Alpha)

{kind=link}

When viewing the net income margins for these same 6 top holdings, it's clear that none of them would be paying as much in income taxes if they weren't operating under 280e.

MSOS Top 6 Holdings Net Income (Seeking Alpha)

{kind=link}

Performance

The entire North American cannabis industry rallied in response to Biden getting elected. Valuations peaked in early 2021. Biden had made several promises about cannabis reform before the election and when he was slow to act on his promises, valuations began sinking.

MSOS 5-Year Performance (Seeking Alpha)

{kind=link}

About a year and a half after the peak, on October 6th, 2022, Biden made an official request for the Department of Health and Human Services and the Attorney General to begin the review process for rescheduling. On August 23, 2022, the DHHS announced their recommendation that cannabis should be rescheduled to schedule 3. The news caused MSOS to rally by about 80% before it began to cool off. The industry is still waiting on the findings of an impact study currently being carried out by the Drug Enforcement Agency before the Federal Government will complete the reclassification process.

MSOS 6-Month Performance (Seeking Alpha)

{kind=link}

Risks

The obvious risk to cite here is that the rescheduling process is somehow halted or takes significantly longer than expected to come to fruition. With Ohio's recent passing of recreational cannabis, and their long history of being a leading indicator for the direction and momentum of the country as whole, it is fair to assume that critical mass has been achieved and that Federal cannabis law will eventually be reformed. Even if the current rescheduling process is abandoned, I believe a new one will be taken up.

Each and every one of the companies within MSOS faces competitive risk from every other player in the cannabis industry. When I first began researching the industry in early 2021, I built a list of over 300 publicly traded companies in North America. Due to a combination of bankruptcy and mergers, the list is now down to about 75 companies. Similar to what happened to the Detroit auto industry in the first half of the 20th century, I expect for consolidation to continue.

If the Federal government ever allows for the importation of Cannabis, then Canadian producers will finally have a market to flood with their ultra-cheap flower and concentrate . They will finally be able to reduce the stress they are under from their ongoing price war . While I doubt this will happen immediately after rescheduling, when or if it happens, I believe the same thing that happened up there will happen here. The more efficient Canadian producers will drive the market price down below the average cost of production, and the less efficient companies will be driven out of business. All of these U.S. based Multi State Operators are used to having significant but not total control over both supply and price. The U.S. MSO's are just as unprepared for a price war now, as the Canadian producers were when they went full rec in 2018. None of them are used to operating in a high competition environment. I believe the coming price war has the potential to drive many of them into bankruptcy.

In addition to sector wide risk from Canadian producers, when rescheduling arrives, all of these U.S. based companies are going to begin to be threatened by Canadian retailers. Part of the reason the price war in Canada has taken so many victims is because several of the more competitive retailers there operate using a discount model . Cannabis consumers are incredibly price sensitive and are willing to drive right past non-discount stores to reach deeper discounts. The only thing preventing these ruthlessly competitive Canadian retailers from entering the United States is the threat of delisting. Once the U.S. Federal government changes their laws, these Canadian retailers will no longer have legal barriers preventing their expansion and they will bring their bankruptcy inducing business models south.

Catalysts

At this point, rescheduling appears imminent. The cannabis industry experienced a massive rally in early 2021 as a result of a mere promise that Biden made during the run up to the 2020 election. I believe it's fair to assume that the rally in response to the laws actually changing will be even larger.

Also, when rescheduling arrives, the brutal tax obligations these companies all operate under will go away and their financials will become far more attractive. The ones with more efficient business models are more likely to survive a price war. The ones which also have a low cost of expansion may even find themselves on my ever evolving list of potential long-term cannabis compounders .

Conclusions

If I didn't believe rescheduling was inevitable, I wouldn't be writing this article. I would still be telling everyone to avoid United States cannabis companies because of 280e. However, I believe rescheduling is inevitable and when it arrives, the fundamentals of the holdings of MSOS will improve significantly. Also, because a large number of retail investors do not have easy access to OTC stocks, and are unable to properly evaluate individual companies, they are more likely to find themselves buying MSOS and some of the other cannabis ETFs to gain exposure to the industry. While I still don't have a super clear picture of when the rescheduling process will finally conclude, I expect that MSOS will experience a truly massive rally as a result.

For further details see:

MSOS: An Industry-Wide Catalyst Approaches