IONQ - My 2023 Christmas Wish List And 2022 Wish List Results

2023-12-11 04:08:05 ET

Summary

- I present my secret Santa list of Christmas wish list stocks for 2023 that I expect to outperform the market in 2024.

- I review my previous Christmas wish list from 2022, which had a success rate of nearly 80% and generated a gain of over 54%.

- My 2023 Christmas wish list includes stocks in the energy sector, BDCs, quantum computing, fintech, EVs, midstream pipelines, and semiconductor companies.

Ho, ho, ho! It's time to get merry and try to predict what is going to happen next year. Whether you believe in the spirit of Christmas or not, (and if not, that is fine with me) you can still enjoy the merriment associated with it. And in that spirit, I would like to unveil my secret Santa list of CHRISTMAS wish list stocks for 2023 that I expect will outperform the market in 2024.

Before I disclose my 2023 secret Santa list of 9 Christmas picks to outperform in 2024 (one for each letter of the word) I would like to review with you my previous Christmas Wish List that I first introduced in December of 2022. The picks were all Growth stocks that I believed would likely outperform over the following year. This is what I wrote at the time:

Some trends that look like tailwinds for 2023 include increasing infrastructure spending on broadband/5G, transportation, clean water, electric utilities, renewable energy, and cost-effective technology solutions.

As it turns out, my picks were nearly 80% accurate and if you had bought equal positions in all 9 of them, you would have made a gain of more than 54% in the one-year period from November 2022 to November 2023, based on a backtest analysis that I performed using Portfolio Visualizer.

{kind=link}

I created a quick spreadsheet to capture the tickers and what the 1-year total price gain was according to Seeking Alpha. The article was published in December so to get a full year I had to start with November 2022 to measure the one-year performance in PV.

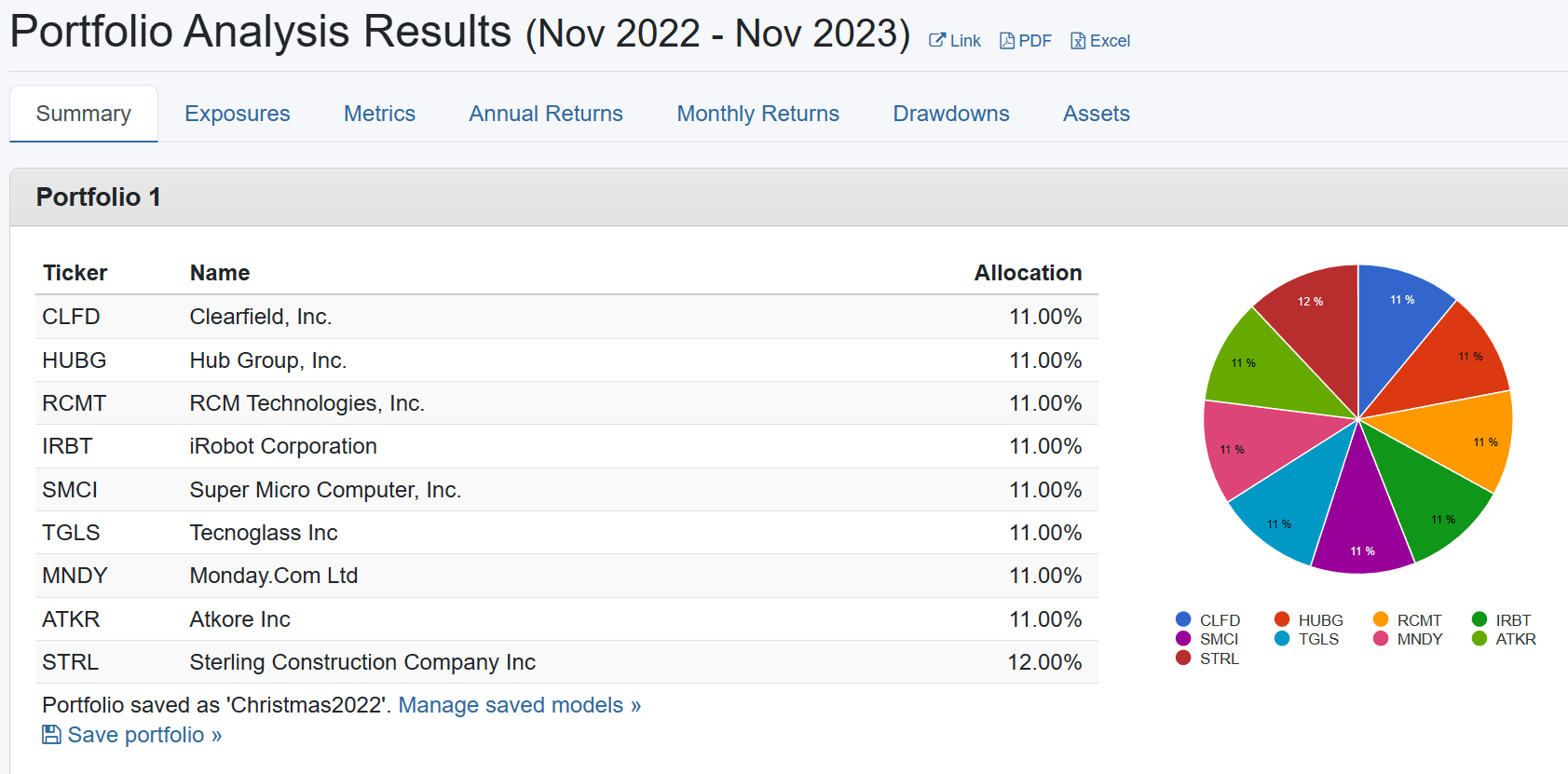

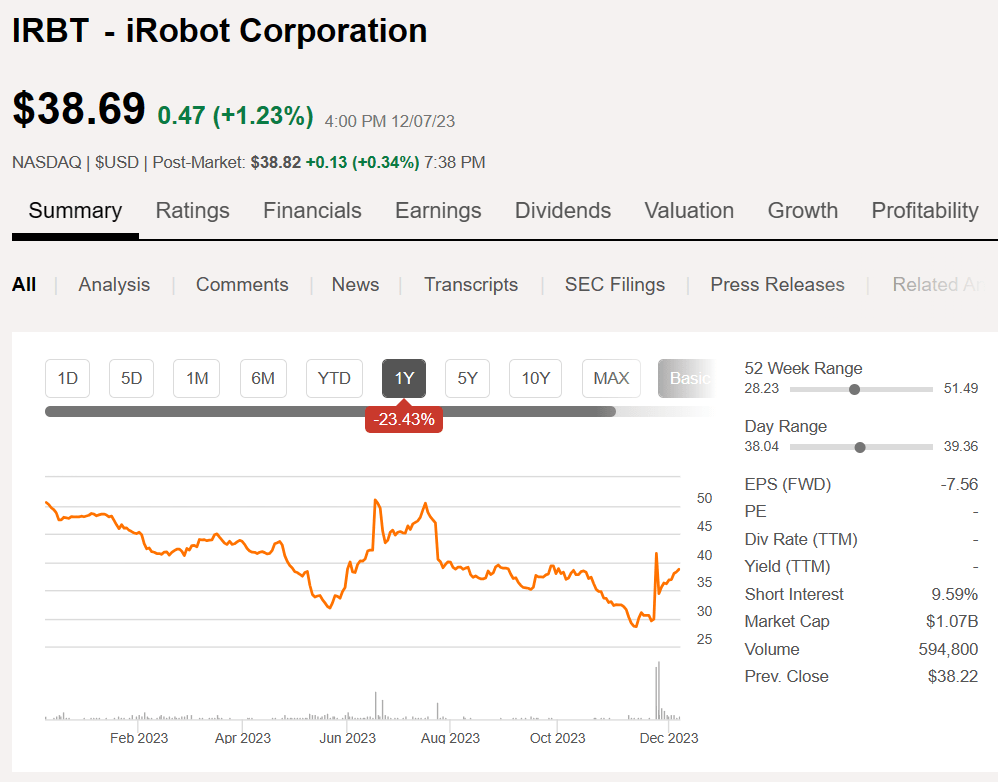

From my spreadsheet you can see that I only had 2 bad picks, [[CLFD]] and [[IRBT]]. Although [[HUBG]] had a positive gain, I would not really call that a good pick but at least it held its value through a tough year. The average gain was 46% with gains as high as nearly 200% for [[SMCI]] and almost 100% for [[RCMT]], with most of that gain in the last month.

author spreadsheet

CLFD was a huge disappointment as all the broadband spending on new fiber construction did not pan out like they hoped it would in 2023. IRBT could still turn out well if the Amazon (AMZN) deal goes through, but recent fears that it will not be approved have caused the price to crash leading to a big loss for 2023.

{kind=link}

The backtest analysis started with 11% allocated to each holding except [[STRL]] which was 12% to get the total to add up to 100. I assumed a $10,000 investment in each of the 9 holdings resulting in an initial balance of $90,000. According to the PV backtest, the ending portfolio balance as of December 2023 would be $144,585 for a 54.9% CAGR.

{kind=link}

Those are rather impressive results and not a bad overall accuracy score in my opinion. I wish that I had listened to my own advice, but alas, I went down a different path this year. As you know if you have followed me at all, I no longer focus on Growth stocks per se, but have turned my focus more towards income generation from high yielding dividend paying stocks and funds. Although all 9 picks last year were growth picks (TGLS pays a small dividend but none of the other 8 do), this year I am including a few "total return" picks in my Christmas wish list.

My 2023 CHRISTMAS Wish List

Without further ado, here is my 2023 CHRISTMAS wish list of picks to outperform in 2024. With respect to trends for 2024, I expect a shift back in favor of the energy sector, which has been out of favor for most of this year. I also feel that utilities and infrastructure such as midstream pipelines, financial companies like BDCs and non-traditional banks like SoFi will also have strong performance next year. Technology continues to evolve, and AI and electric vehicles will continue to drive (pun intended) innovation. Those are the major themes driving my current investment picks.

2023 CHRISTMAS list

author spreadsheet

C: Chevron ( CVX )

While CVX has suffered from the market displeasure surrounding their announcement of a deal to purchase Hess Corp. (HES), the stock is only back down to a level that is still about 56% higher than it was 3 years ago. The correction in CVX stock since late October has created a holiday sale on the stock that now trades at only about 10X forward earnings and pays a dividend yield of a little over 4%.

{kind=link}

While oil prices have retreated, and crude oil prices have breached the $70 mark for the first time in months, the whole energy sector is taking a beating. Even with recent OPEC cuts, multiple wars affecting supply, and increasing demand for US exports, oil prices have been coming down along with inflation. But this is temporary and eventually prices will rise again and after the Hess deal closes (possibly in the first half of 2024) CVX stock will likely recover by Q3-2024 and go on to new all-time highs sometime after that. Of course, that is assuming that the situation in Venezuela does not develop into a more threatening situation than it already is.

There is a risk that the Hess deal won't get approved though so anyone investing in Chevron today should do so knowing that they may not get Hess. Just today as I am composing this article the news came from FTC requesting "more information" on the deal. Normal procedure, I believe.

H: Hercules Capital, Inc. ( HTGC )

In 2023 my personal investment focus shifted from growth to income as I decided to retire from my full-time career in August. As part of my Income Compounder portfolio I have written about in several previous articles such as this most recent update , I invest in several BDCs that offer a high yield distribution. One of those BDCs that I follow is HTGC and I believe it is poised to demonstrate strong performance in 2024 as the US economy remains resilient and BDCs are picking up the pace in lending to startups and providing venture capital while banks are more reluctant to.

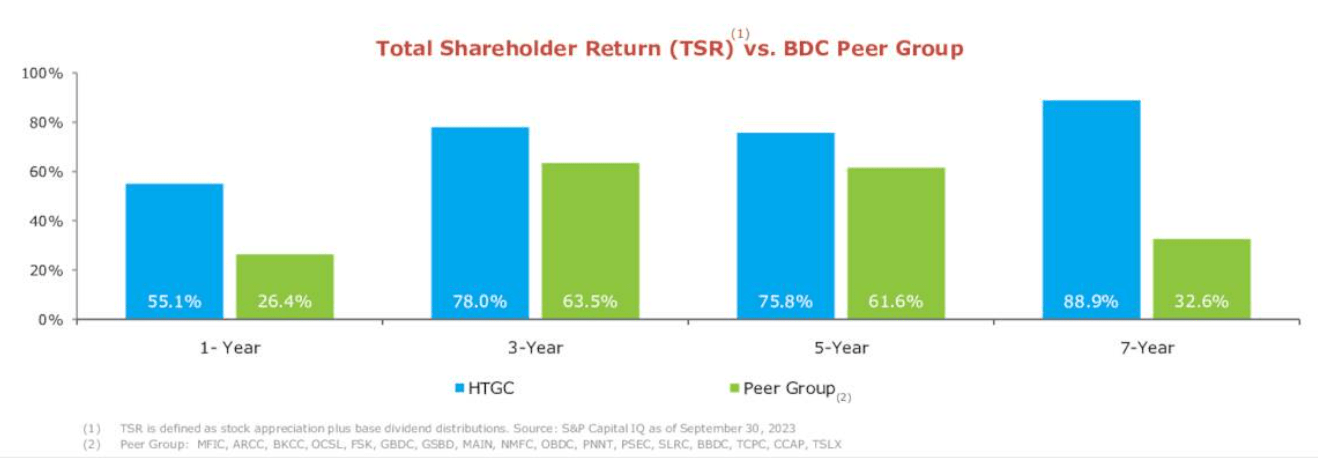

Hercules is a publicly listed, internally managed BDC and RIC (Regulated Investment Company), which requires it to distribute 90% of taxable income as distributions to shareholders. According to the company's Q323 earnings presentation, HTGC has returned far more to shareholders each year than its peer BDCs as illustrated in this chart of 1-year, 3-year, 5-year, and 7-year total returns.

{kind=link}

As a venture stage capital provider, HTGC focuses on specific areas of specialized expertise in Technology, Life Sciences, SaaS financing, Sustainable/Renewable Energy, and Special Situations such as M&A. The company's GAAP effective yield as of Q323 was 15.5%. Unless the economy dips into a severe recession next year, which is looking more unlikely with each new monthly jobs and inflation reports, HTGC is poised to deliver strong total returns over the next year.

R: Runway Growth Finance Corp. ( RWAY )

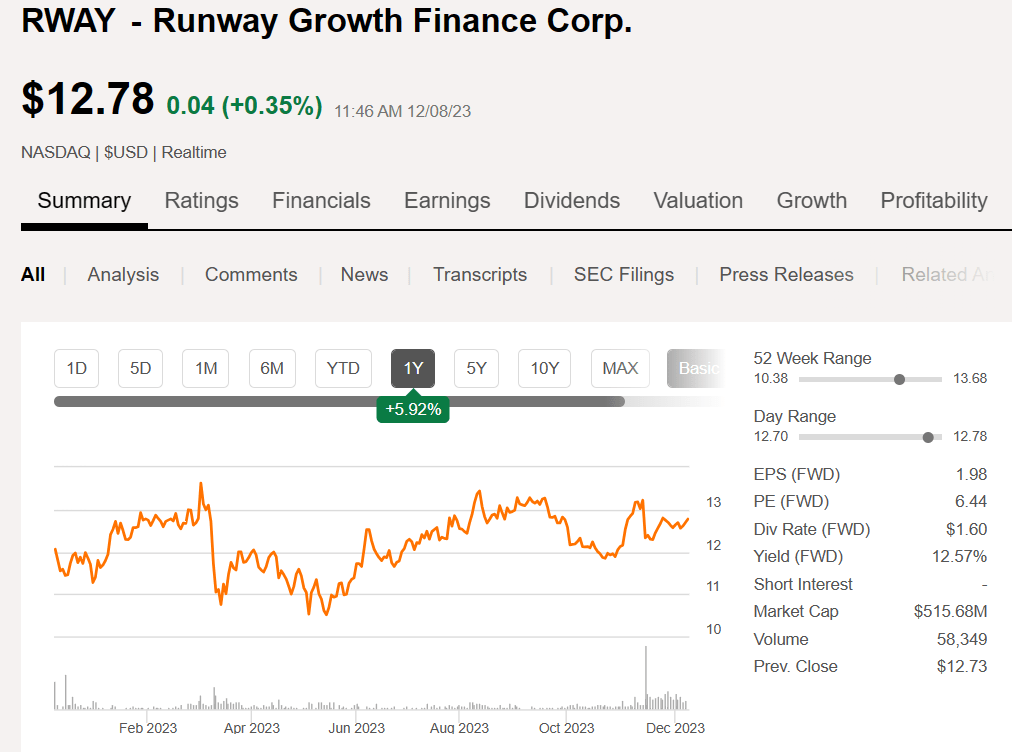

Another BDC that I like and currently own is RWAY. As a relatively young, publicly traded BDC it offers investors a yield of 12.7% and shows promising growth with 60% YOY revenue growth reported in Q323. Like HTGC, RWAY invests in mostly venture stage companies and that business is likely to continue to expand in 2024 as capital markets regain momentum after slowing down in 2023. Unlike HTGC, which trades at a premium to its NAV, RWAY trades at a discount of about -15% and therefore I believe it has more upside potential for price appreciation.

{kind=link}

From the company's Q3 earnings call , Interim CEO Greg Greifeld (acting CEO while David Spreng is out on a medical leave) described the market outlook:

According to recent PitchBook Data, U.S. late-stage venture equity deal value, which we view as a proxy for the venture debt market opportunity, was approximately $57 billion Q3 year-to-date.

While deal value is down from record levels in 2021 and 2022, it remains above the comparable period in 2020 and preceding years. U.S. late-stage venture equity deal value represented 46% of total deal value for 2023 year-to-date and nearly one third of total deal count. This is a continuation of the dynamic we've observed in recent quarters, more late-stage deals but at smaller values.

This snapshot shows that the late-stage VC ecosystem is active. However, our team expects deal volume to accelerate into the middle of next year as companies that raised substantial equity in 2021 and 2022 spend the remainder of those proceeds. As liquidity runs dry, companies will need to raise additional capital to fund growth.

I believe that RWAY is well positioned to take advantage of the expected uptick in late-stage VC financing along with HTGC.

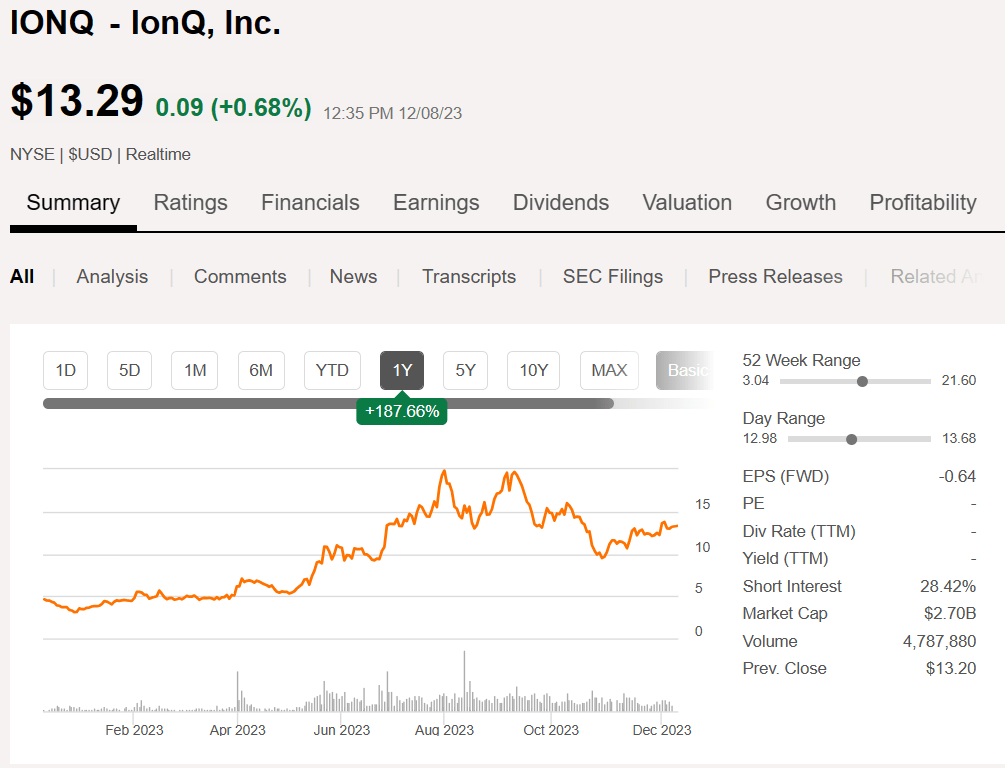

I: IonQ, Inc. ( IONQ )

For a completely different idea in a growth stock opportunity, I am highlighting this quantum computing pick, IonQ. As explained by my fellow SA analyst in his writeup, IonQ Stock: High Risk, High Reward Caution , IONQ is a high risk/high reward opportunity. The company went public through a SPAC merger in 2021. Based in College Park, MD, IONQ has developed a quantum computer called IonQ Forte, which has a capacity of 29 qubits. Qubits are quantum bits for machine learning using quantum circuits.

{kind=link}

As of Q323, the company has booked over $100M in cumulative bookings in its first 3 years of commercialization. According to the latest earnings report on November 8, "full year bookings are now seen to be between $60M to $63M, versus a previous guidance of $49M to $56M." The stock price has risen by more than 187% in the past year.

{kind=link}

In September of this year, IONQ announced an expanded relationship with the US Air Force: IonQ expands its relationship with Air Force Research Lab. That deal, in addition to adding $25.5M in revenues, helps to solidify IONQ's position as a preferred quantum computing provider of choice. This statement from the press release explains the significance of this contract award:

As IonQ's systems approach 64 algorithmic qubits (#AQ 64) and usher in the era of enterprise-grade quantum computing, we are committed to supporting the nation's security interests. This partnership will significantly help advance U.S. defense technologies as quantum computers increasingly become a prevalent centerpiece of national computing stacks," said IonQ CEO Peter Chapman.

IONQ is a speculative pick for those growth investors seeking huge rewards if the technology can deliver on those promises.

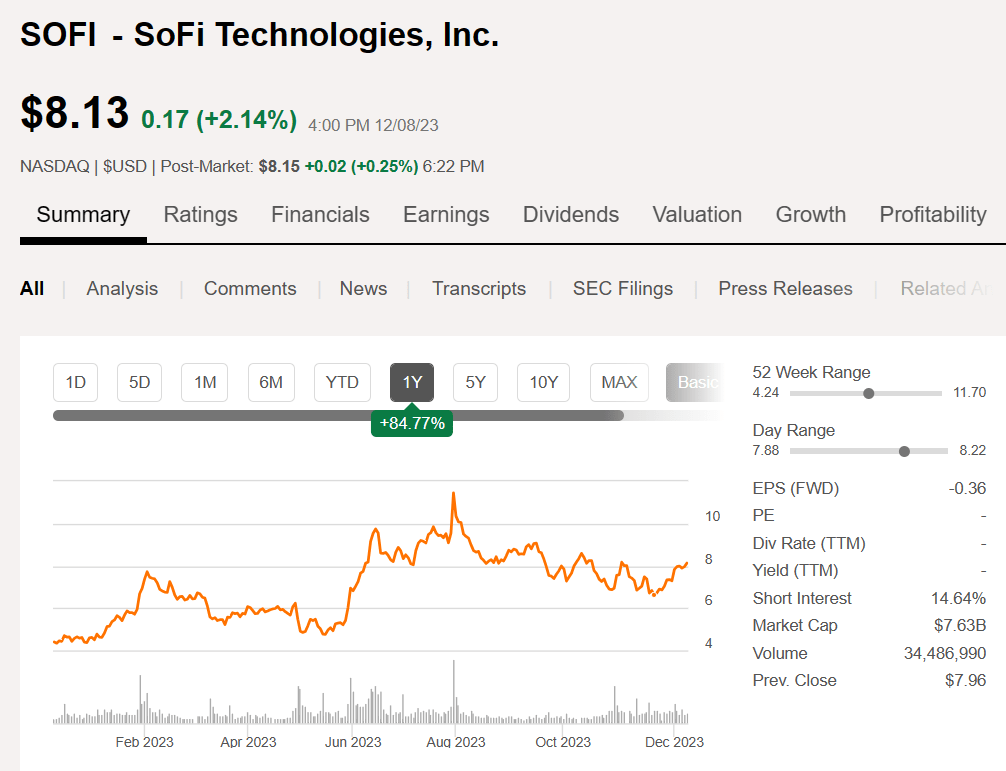

S: SoFi Technologies, Inc. ( SOFI )

Another somewhat speculative growth pick for 2024 is SOFI. Considered a "meme" stock this year, SOFI is not yet profitable but is growing and stealing market share away from traditional banks. SOFI is a financial technology business or fintech company, that is changing the way that people borrow and finance their futures. According to CEO Anthony Noto, SOFI is poised to become profitable by Q4 2023 and by 2024 he expects about 50% of the revenues to come from borrowing and 50% from technology and financial services, with the financial services segment continuing to expand further.

We continue to actively explore ways to leverage the technology platform at SoFi and also to leverage the technology platform resources to develop products and services more broadly for the industry.

The company expects to generate from $300 million to $500 million in tangible book value in 2024. As of Q323 the company reported record EBITDA for the 5th quarter in a row as explained by CFO Chris Lapointe in a December 4 shareholder conference.

In Q3, we ended up delivering $98 million of adjusted EBITDA, our fifth consecutive quarter of record EBITDA. We also grew tangible book value by $68 million in the quarter and $171 million over the last 12 months. This is critically important as every $100 million of incremental growth in tangible book value results in $800 million of organic lending capacity.

Already in the past year, SOFI stock has risen by more than 80%.

{kind=link}

The recent news announcing the end of their involvement in cryptocurrency comes as a bit of a surprise, but I believe it helps the long-term credibility of the business by not "tainting" it with the nasty (in some people's view) crypto tag. It makes sense to me that the company focus should be on the technology side of more traditional, digital banking. Even though crypto is part of the new digital currency and banking movement, there are certain additional risks that dealing with crypto introduces from a regulatory perspective, which would detract from SoFi's other business ventures. Overall, this is a positive decision by SoFi in my opinion and the stock is up about 2% today, so the market seems to agree.

T: Tesla ( TSLA )

As an American consumer who is committed to helping the environment and doing my part to reduce vehicle emissions while still having a nice ride, I am excited to be part of the EV movement. I am now leasing a new Kia EV6, and it is my first EV. Yes, I absolutely love it. I test drove a Tesla Model Y as a rental car in Southern California where I was visiting my mother. I liked the Tesla ok, but it is not nearly as much fun to drive as my Kia. Regardless, I understand the appeal to many drivers who do enjoy the Tesla experience.

author photo

Despite my dislike of Elon Musk as a human being, he is a remarkable, brilliant businessman. He has established Tesla as much more than just a company. The Telsa brand has become like the "Xerox" of the EV movement. Tesla as a company does much more than just sell cars - and now a Cybertruck , which could become the iPhone moment for Tesla in my opinion.

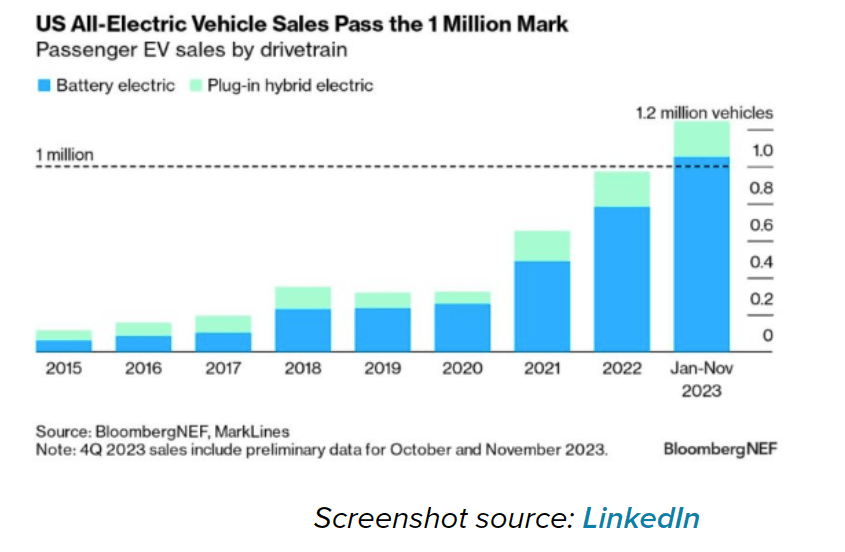

As interest rate fears recede into the distance, there is likely to be renewed buying enthusiasm for EVs along with boating, and RVs as people look to move beyond Covid-19 and get out and enjoy life! And even though I like the Kia, a whole lot more Tesla EVs have been sold this year. In fact, according to this report from Electrek, EV sales in the US are up more than 50% YOY with more than 1 million sales this year.

{kind=link}

Keep in mind that sales of EVs in the US are only part of the Tesla story. According to this source , Tesla is the largest-selling EV car company in the world with far more EVs sold in China than in the US.

Tesla has sold the most electric vehicles in the world. Tesla was the first company to manufacture electric vehicles on a global scale, and it remains the industry leader. Widely, Tesla is seen as a luxury producer of electric vehicles.

Even as other EV makers ramp up production and bring down costs, Tesla is able to compete. Although TSLA stock is seen as overvalued, many good growth picks can look overvalued for years. TSLA has an A+ in Profitability with $12B in Cash Flow from Operations.

Seeking Alpha

Achieving high yield income from growth is another way to play the Tesla stock story by acquiring the YieldMax TSLA Option Income Strategy ETF (TSLY). Formed just over a year ago in November 2022, TSLY generates high yield income from capturing options premiums on Tesla stock. The fund uses a synthetic covered call options strategy to capture income. The TTM yield on TSLY is over 80%. I have a small position that I just started in TSLY to capture the income while the fund is paying it. As long as TSLA continues to increase in value, the options premiums will continue to generate some strong income. I expect that TSLA will continue to outperform in 2024 as EV sales continue to skyrocket worldwide.

M: MPLX LP ( MPLX )

Another energy sector pick for 2024 is this midstream pipeline company. MPLX operates in two major market segments, Logistics and Storage, and Gathering and Processing. As an LP, the stock issues a K-1 at tax time and is best held in a taxable account to take advantage of ROC in the distributions, if you are so inclined. The current distribution amounts to a yield of about 9.5% and is a retirement "dream machine" according to one SA analyst.

Midstream companies have been increasing their steady income streams as they pass along rising interest rates in renewed contracts that lock in those higher rates. In fact, MPLX just increased the distribution by 10% as explained by President and CEO Michael Hennigan on the October 31 Q3 earnings call.

For the second year in a row, based on the strength and continued growth of our cash flows, last week, we announced a 10% increase in the partnership's distribution, which now stands at $3.40 per unit on an annualized basis. We're committed to returning capital to unitholders and expect our distribution to be the primary return of capital tool supplemented with opportunistic repurchases. We are well positioned to optimize return of capital given the strength of the business and our balance sheet.

There is a risk with MPLX that should be considered by potential investors, although I do not believe it is likely that it will happen in the next year. But the parent company, Marathon Petroleum (MPC), could decide to buy out MPLX. From the remarks made by CEO Hennigan on the earnings call it does not sound like that is in the works anytime soon:

And with the recently announced 10% increase to the partnership's base distribution, MPC now receives $2.2 billion annually from MPLX's distributions, illustrating its strategic value as part of MPC's portfolio. As MPLX pursues its growth opportunities, we believe the value of this strategic relationship will continue to be enhanced.

On another positive note, BofA on November 17 came out with ratings of 16 global stocks that have underperformed in 2023 but they are overweight and expect a potential breakout in 2024. MPLX is on that list.

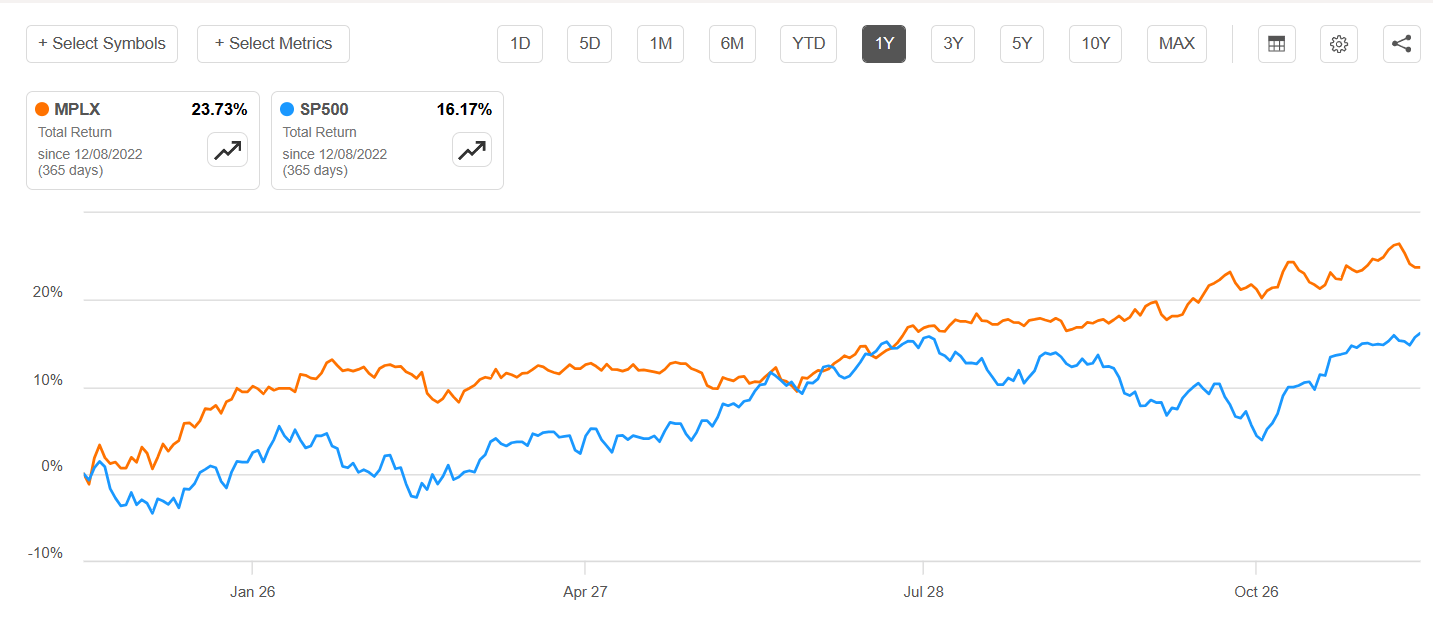

The one-year total return for MPLX was about 23.7%, far outperforming the S&P 500 16% TR as shown in the SA charting tool. I expect this outperformance to continue in 2024 and even improve if oil prices resume their rise back to $90 crude as some predict .

{kind=link}

A: Advanced Micro Devices ( AMD )

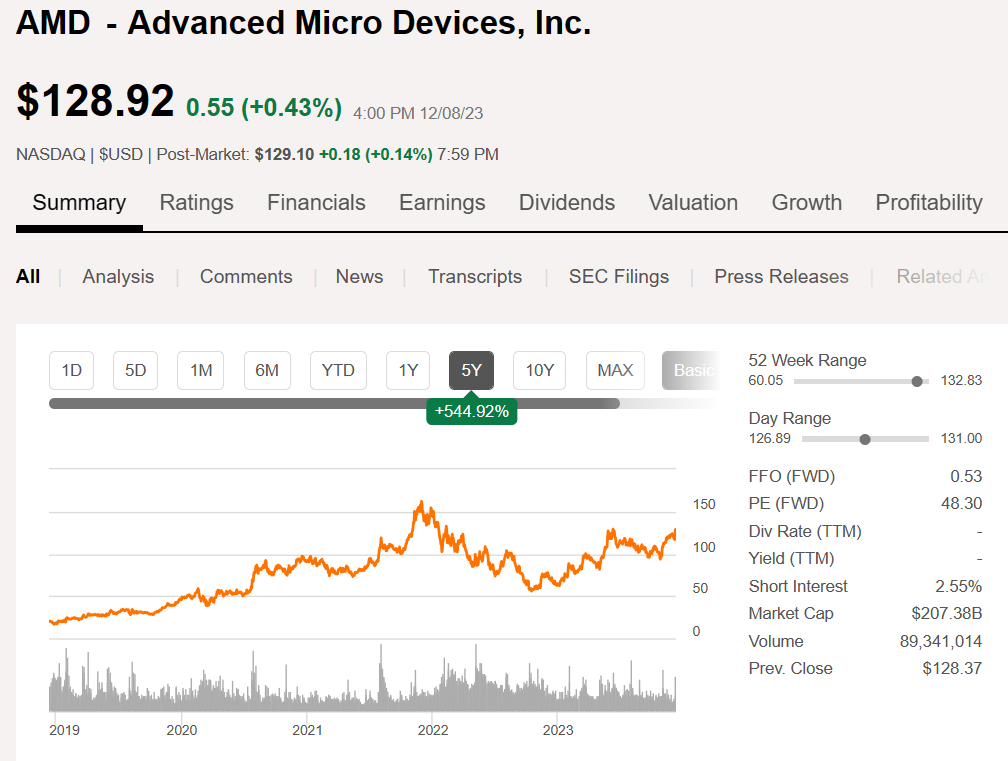

There are a lot of strong opinions on AMD and for those who got in early, those strong opinions are typically positive and optimistic for the future. And why not? After all, AMD stock has achieved a gain of 80% in the past 1 year, 545% in the past 5 years, and a whopping 3,368% gain in the last 10 years.

{kind=link}

Does that mean it will gain another 500% in the next 5 years? Probably not is my guess, but the company is performing well, firing on all cylinders, and leveraging the increasing interest in AI for their chipsets and embedded software technologies. In particular, the reaction to the new MI300x AI accelerator fired up the whole semiconductor industry this week. Helping to fuel the fire was CEO Lisa Su's comments about the increased TAM for AI Accelerators now expected to reach $400B by 2027 compared to an estimated $150B in previous guidance.

While AMD stock floundered a bit since early 2022, it is now in a nice recovery and is approaching the 52-week high of $132. AMD stock has strong Profitability, Growth, and Momentum as shown in the Quant factor grades, but is a bit overvalued currently at nearly 50x forward earnings.

Seeking Alpha

Those earnings revisions are likely to be revised upward shortly in my opinion. For example, during the MI300 unveiling event on December 6, AMD said it expects the MI300 to generate $2B in sales in 2024. The impact of the AI revolution is just starting to be seen. I believe that 2024 will be a significant year of growth for AMD as AI technology evolves and more compute power will be needed to support the growth.

Other SA analysts also like AMD and several have recently given the stock Strong Buy ratings:

Seeking Alpha Seeking Alpha Seeking Alpha

My belief is that the MI300 is a game changer and AMD will stand to benefit for years to come. The stock tends to be somewhat cyclical though, so do not expect a straight path upward. I expect the price to pull back a bit from current levels before setting new all-time highs perhaps as soon as Q3 of 2024. Unless the global economy takes another Covid-like swoon between now and then, I think the forward prospects for AMD growth look very positive.

S: NXG Cushing Midstream Energy Fund ( SRV )

Did I mention that I like the prospects for midstream energy investments right now? There are several ways to invest in midstream assets. One way is by purchasing units of an LP like MPLX mentioned above. Another way is to invest in a CEF that holds midstream assets. I have previously covered SRV twice, both articles published earlier this year. In my first article on SRV, NXG Cushing Midstream Energy Fund: A Fund That Fights Inflation And Yields Over 16%, I discussed how such a fund fights inflation by paying a high yield distribution based on recurring income from midstream assets.

The long-term opportunity in income generation from real assets such as midstream energy infrastructure offers investors a steady flow of cash at lower risk relative to other asset classes, especially as inflation continues to impact pricing.

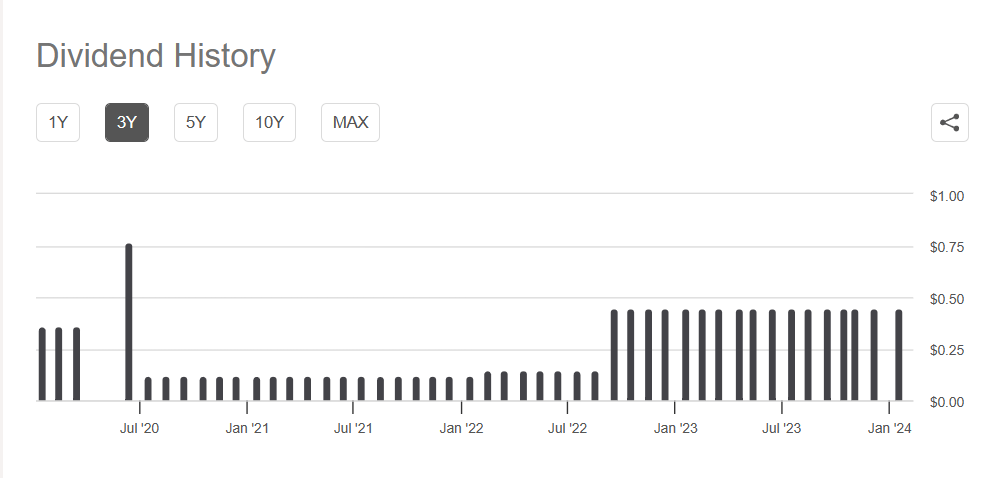

Then in my follow-up article , I talked about how the SRV fund is able to cover the huge 16% distribution and still maintain some NAV growth. Many readers questioned me when the fund managers decided to bump up the monthly distribution back in September 2022 when they tripled the payout. Looking at the 3-year dividend history you can see how the fund went from paying $.12 monthly to $.15 and then jumped up to $.45 monthly in September 2022 and has been paying that amount ever since.

{kind=link}

In April 2023, the fund made a further transition with a name change and changes to its investment strategy including subtle changes to the definition of midstream to include biofuels, carbon sequestration, solar, and wind in addition to more traditional midstream assets like pipelines.

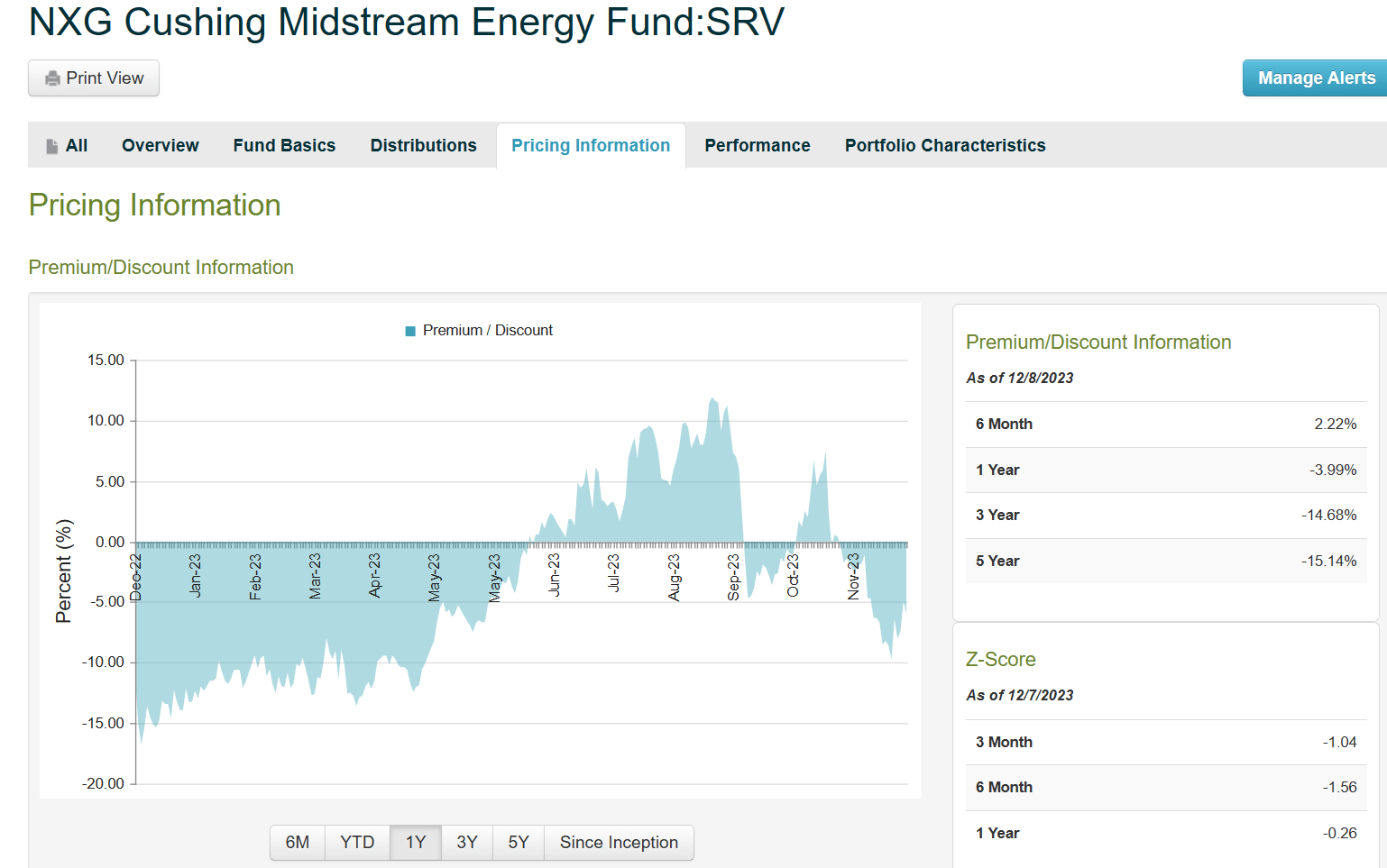

One of the stated reasons for bumping up the distribution was to close the discount on the fund, which historically traded at a very wide discount as shown in this chart from CEFConnect. The 5-year average discount for SRV was around -15% and after the raised distribution the discount closed, and the fund even traded at a nice premium for a few months before retreating back to a discount again.

{kind=link}

Now the latest attempt to close the discount is a 3-for-1 rights offering . As with many ROs there is a potential advantage for shareholders who already own shares to exercise their rights to buy more at discounted prices. But sometimes the market discounts the price even more than the offering price, so it may be better to wait until after the offer expires on December 14 if you wish to purchase new shares at a lower price.

I believe that the SRV fund managers have a good understanding of midstream assets and will continue to deliver a high yield distribution for at least the next year. While the short-term impact on the RO may be a slight reduction in NAV per share, having more shares at a narrower discount should help offset that reduction and improve the total asset value to provide for future investment opportunities.

At the current price of just under $35, I believe that SRV will deliver a strong total return over the next twelve months and deliver monthly distributions that can be reinvested to buy even more shares or used to support purchases of other undervalued holdings as I do in my Income Compounder portfolio.

Time to Put a Bow on it!

That is about all I have time for now. I hope this was a nice gift for your Inbox and you came away with at least one idea that you can use or share. Have a joyful holiday (whichever you prefer) season and I wish you all the best in the new year.

For further details see:

My 2023 Christmas Wish List And 2022 Wish List Results