WSM - My Dividend Growth Portfolio February Update: Cash Is Not Trash

Summary

- Cash is yielding over 4%, so a dividend growth investor can afford to be patient.

- February marked the first monthly decline in projected income since 2016 due to dividend cuts.

- Healthcare and staples are getting left out of the market rally and are presenting some interesting opportunities.

Last month was a mixed bag. There were some fantastic dividend increases! On the other hand, a couple of dividend cuts negated the gains. As I wrote in my 2023 preview , the portfolio is due for some cuts as the income growth has been significantly exceeding the historical projections in recent years.

The portfolio is still sitting at record-high levels of cash. Patience is a virtue in dividend growth investing, as buying at a bargain price can put income growth years ahead. While I had been getting impatient waiting for bargains to develop in the market, I recently realized that I was looking at this all wrong.

Right now, cash isn't a drag on my portfolios; it's a plus. I realized this towards the end of the month, and it has reframed how I am approaching the market right now and has given me renewed patience. After all, cash is yielding over 4%. My goals focus entirely on income growth; cash can help grow the income now.

Portfolio Goals

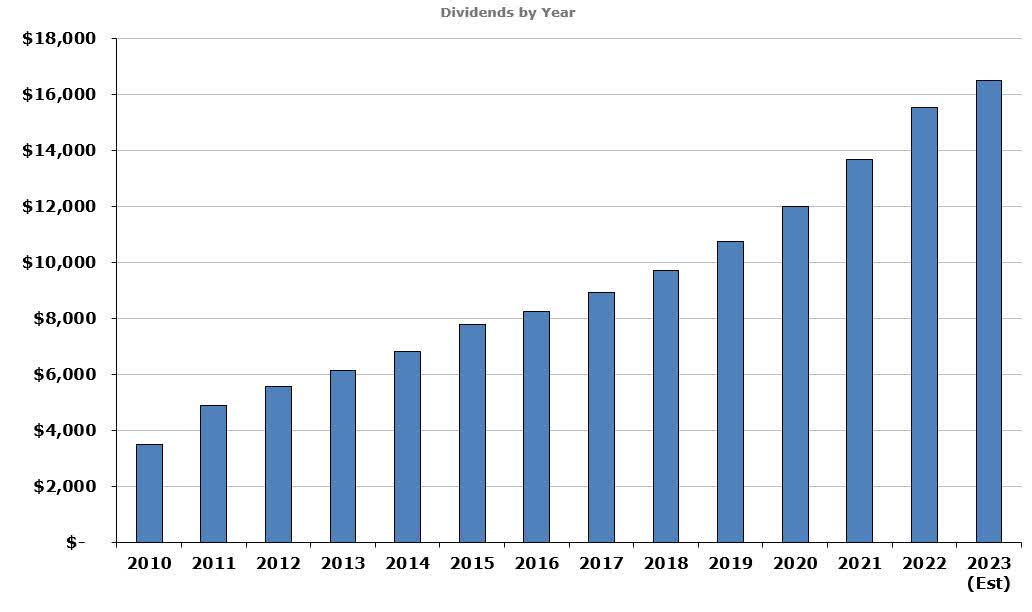

This portfolio's goals are simple: Grow the income at 10% annually with dividends reinvested or 7% without reinvestment. In practice, this means that new purchases need to average a 3% initial yield with a 7% dividend growth rate. The portfolio has hit this goal with remarkable predictability as shown in the chart below.

{kind=link}

In 2016, I closed this portfolio to new capital to better track its performance. Therefore, all income growth has been due to dividend increases and reinvestments, not by adding more funds. My 2022 recap and 2023 look ahead articles describe my full methodology and holdings.

How am I doing so far in 2023?

Last month I reported that income growth was projected at 8.0% for the year, up from 7.9% at the start. However, two dividend cuts have caused the projection to fall to 6.7% at the end of February.

- Blackstone ( BX ) announced a Q1-2023 vs. Q1-2022 dividend reduction of nearly 38%. However, any long-term holder of BX knows the dividend is variable and difficult to estimate. As a result, I further reduced my projection to $4.03/share for the entire year, which is below the analyst average of $4.10.

- Intel ( INTC ) announced a 66% dividend cut. As I wrote about last month, following earnings, I decided to sell my position in INTC. I haven't fully liquified my shares or reinvested the proceeds, disproportionately affecting my projections. The "Sales in February" and "Replacement Purchases" sections cover this more in-depth.

As the portfolio is nearly 3% in cash as dividends pile up, I will begin including interest income in my results but not the projections. Interest income was always negligible in the past as interest rates were too low, and the cash held was insignificant to the results.

The goal of the portfolio is strictly income oriented. However, many readers are interested in the total return. Year to date, the portfolio is up 3.0%, trailing the 4.1% total return of the S&P500.

February's Dividend Increases

Last month brought a slew of raises, many exceeding my expectations. Of course, these were tempered with the cuts mentioned above. Still, I was excited to see three new positions have solid increases. These positions were all replacements for the Apple shares sold last year. These were CME Group ( CME ), Intercontinental Exchange ( ICE ), and Home Depot ( HD ).

CME Group

On February 2nd, CME announced a 10% increase, in line with its past couple of raises and above its ten-year dividend growth rate of 8%. Because CME pays an annual special dividend, evaluating the actual increase is difficult because the company can adjust the special at the end of the year. However, I like this model as it allows the company some freedom and the ability to increase the regular dividend with much less risk.

CME is still a relatively small position in the portfolio at slightly over 1%. The company contributes about 1.5% of the total income, including the special dividend.

Intercontinental Exchange

The same day CME announced its raise, ICE followed up with a 10.5% increase! This exceeded my expectations but was below the last couple of increases of around 15%. ICE makes up slightly over 1% of the portfolio and accounts for just 0.5% of the income.

Pepsi ( PEP )

Pepsi is unusual with its dividend payouts and increase announcements. Firstly, the company doesn't pay a dividend in the fourth quarter but delivers two in the year's first quarter. Secondly, they announce the dividend increase in February, but it doesn't take effect until the June payout.

This year, PEP announced a 10% increase! This was surprising as the company has a very consistent dividend growth rate of 7%. Additionally, Pepsi became a newly minted Dividend King with 50 years of dividend growth!

Home Depot

I've been the holder of Lowe's ( LOW ) in other portfolios since 2020, but I was excited to add Home Depot to this portfolio last year. I had tempered expectations for this year's increase, but the company blew me away with a 10% increase! While this increase lags the 15% increases investors are used to getting, it is welcome in light of the forecasts and falling earnings projections. Next year's raise may be less generous.

Prudential Financial ( PRU )

I added a small position of Prudential as a high-yield moderate-growth position a couple of years back at a plus 5% yield, expecting sustained 5% dividend growth. The company came in broadly in line with my expectations when they announced a 4.3% increase.

Phillips 66 ( PSX )

I acquired PSX shares in the split of ConocoPhillips ( COP ) several years ago. While I have since sold the COP shares, I continue to hold PSX. Dividend raises from the company have been inconsistent since 2020, so I was excited when they announced an 8.2% increase! The company has been lagging other refiners on raises, so this was a welcome increase.

Best Buy ( BBY )

Best Buy announced a 4.5% increase on March 2nd. This aligned with my expectations and will extend their growth streak to 20 years. Aside from Lowe's, this is the longest growth streak of any specialty retailer. Of course, the increase will disappoint many investors who have gotten used to 20% plus raises from Best Buy. For at least a couple of years, smaller increases are likely to be the norm rather than the exception.

March's Expected Increases

After the flurry of increases in the first two months of the year, March is a rare off month. In fact, not only are there no companies in my portfolio with announcements, only one company on my watch list "sometimes" announces in March.

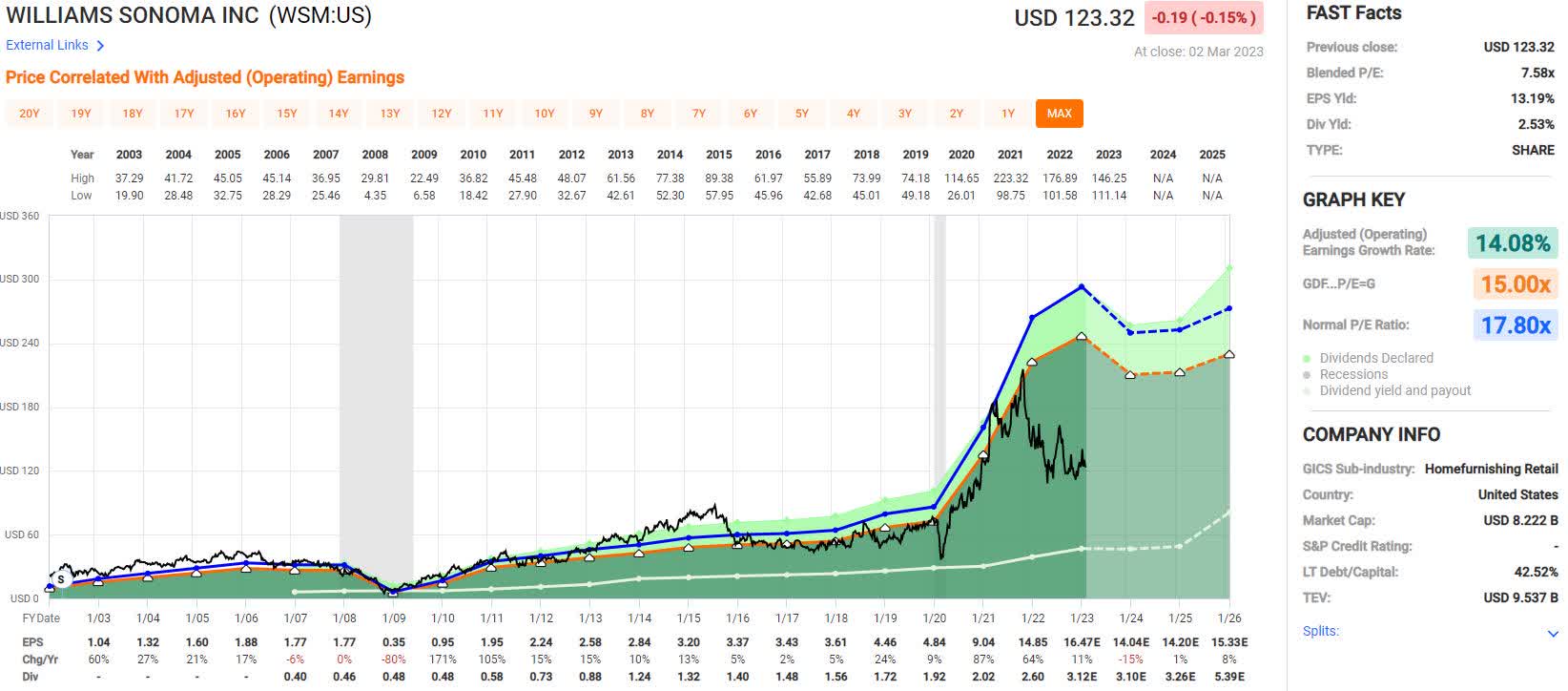

That company is Williams-Sonoma ( WSM ). WSM has been a phenomenal dividend grower with a 10-year dividend growth rate of nearly 14% and a 5-year of 15%. I've been watching retailers closely to see how they handle raises, given most expect reduced earnings. I think we will see earnings forecasts continue to fall for retailers as the year progresses.

As it stands, WSM trades at a PE of only 7.5, although the forward PE is higher with the lower earnings forecasts. Williams-Sonoma might offer a fantastic bargain if we get a general market drop from its current low valuation. The Fastgraph below shows the relative undervaluation of WSM to its average PE ratio.

{kind=link}

Sales in February

I rarely sell companies in this portfolio. Every company is bought with the intention of holding forever. However, I regularly evaluate the positions for significant overvaluation and a change in my thesis. As I wrote about last month, I lost faith in Intel ( INTC ) and began scaling out of my position in February. As of now, I have yet to fully close the position.

I have been an Intel shareholder since 2012, which means I held the company for over a decade and broke even on the price. During this time, I collected about 76% of my purchase price in dividends. Since I don't DRIP, the dividends were reinvested in hopefully more successful stocks.

It's not easy selling companies that are beaten down in price. After all, I am usually looking for bargains. However, nothing about Intel looks like a bargain right now. At a forward P/E of nearly 50 and earnings continuing to fall, there is much room for the price to drop. While earnings are expected to rebound, current estimates place 2025 earnings per share similar to the company's EPS in 2016. As a dividend growth investor, there are plenty of better opportunities.

{kind=link}

Purchases in February

I make two types of purchases: Regular purchases, which are reinvested dividends, and purchases to replace sold shares. I emphasize bargains with reinvested dividends, whereas replacement purchases are more about replacing the income with higher quality and better dividend growth. The portfolio remains at historically high cash levels as I am finding few exciting buys currently.

As I opened with, I like the return on cash at present. Since I am finding no exciting bargains and think that over the next year, opportunities will present themselves, I am content to wait. As a result, there were no regular purchases last month.

Replacement Purchases

As I scaled out of Intel, I began replacing the income by adding to existing positions. As Intel yielded over 5%, replacements will mix high-yield positions and lower-yielding, faster-growing companies. This is because I want to replace the total income that Intel was providing.

Only a tiny portion of the sale proceeds was reinvested in February, and replacement purchases will continue into March. Below is a summary of the investments made and the average price paid. I don't necessarily consider these bargain purchases, but I am trying to balance replacing the income with quality and dividend growth.

- Enterprise Products Partners ( EPD ) 10 shares @ $25.74

- Home Depot 1 share @ $302.54

- CVS 4 shares @ $83.87

What Else Am I Watching?

Since this is a closed portfolio, I can only buy some of the companies that look interesting. I use this section to cover what I purchase and consider in my other portfolios. My other portfolios have different goals and rules but are also dividend growth portfolios.

Some bargains are starting to show up in the market. Nothing has quite reached the point that I am jumping fully in, but I am doing some nibbling. As the market returns to a "risk-on" mode, healthcare and staples are getting left behind. While a few bargains are starting to appear in these areas, many companies are reaching a low enough valuation that should the overall market reverse course, some truly fantastic deals might appear briefly.

The above chart shows the year-to-date underperformance of Johnson & Johnson ( JNJ ), Amgen ( AMGN ), and CVS Corp ( CVS ), three companies I own and track, but the same can be seen in a wide span of healthcare companies.

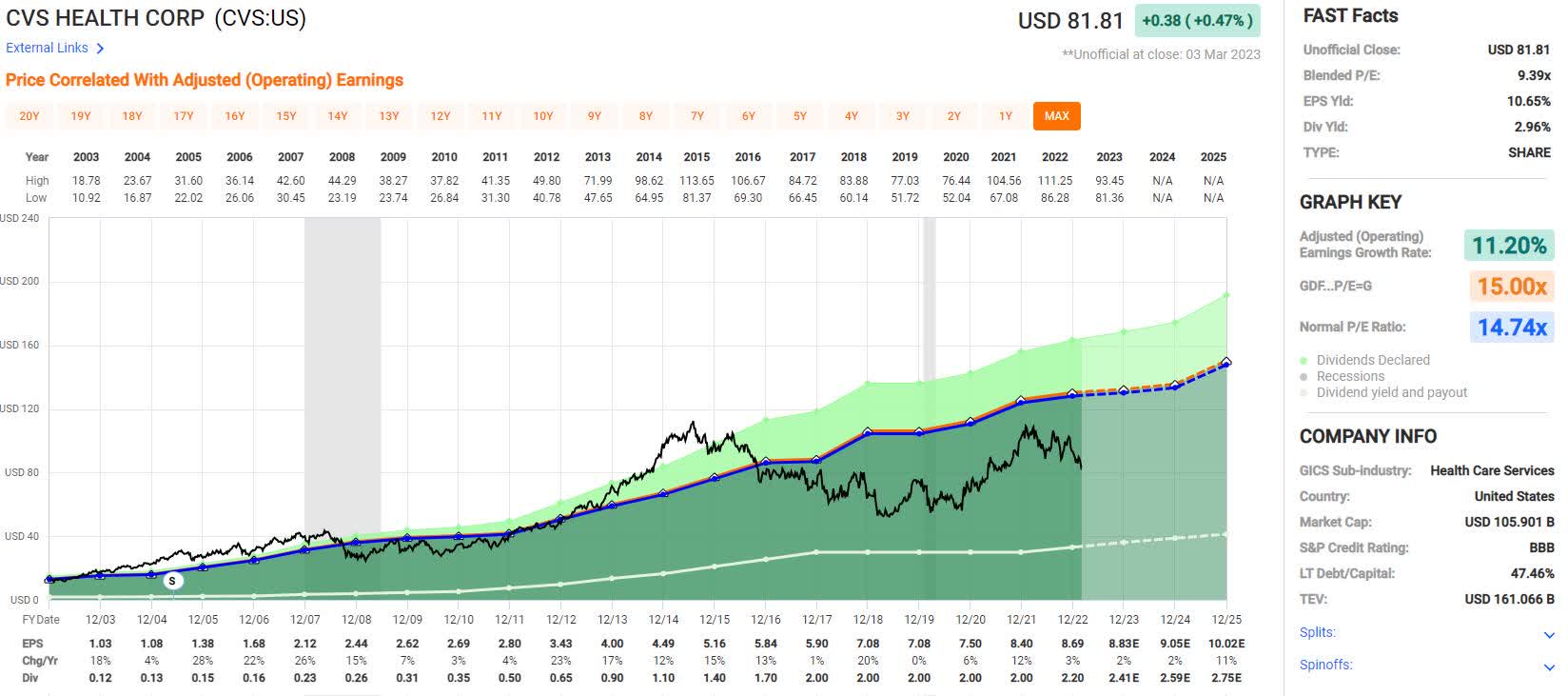

While JNJ rarely offers a 3% yield, as shown below, I am avoiding the company for now. I want to consider the upcoming spin-off more and see more details. More and more companies are using spin-offs to shutter risk and debt, which is understandable, but I'm not sure I want to hold both companies. Instead of JNJ, I am more interested in CVS right now.

CVS has recently begun raising the dividend again, but more importantly, I was impressed with their discipline in freezing the distribution while they paid down debt. Additionally, their transition is putting them more in the realm of UnitedHealth Group ( UNH ) and Cigna ( CI ) rather than Walgreens ( WBA ). As shown in the Fastgraph below, CVS has been undervalued for years but has recently dipped back into the single-digit PEs.

{kind=link}

With Pepsi's recently announced raise, the forward yield on the June dividend is close to 3%. While this isn't a particularly unusual yield for PEP, it's rare for it to get much higher. The table below shows Pepsi's minimum, maximum, and average yields over the past ten years.

Pepsi Dividend Yield History (Seeking Alpha)

{kind=link}

Another staples company I have been watching is Kroger ( KR ). Regardless of what happens with the Albertsons ( ACI ) merger, the company has been a fantastic dividend grower with 17 years of growth and a 5-year dividend growth rate of nearly 15%. I was adding a few shares as it approached $40, but the big pop after earnings means I will be back to watching.

My favorite retailers, Lowe's, Home Depot, Tractor Supply Company ( TSCO ), and Best Buy, are all showing as bargains right now. However, I think it's likely that these companies will retest 2022 lows at some point. But, in a historical context, it's a good time to add these. Incidentally, last month, I reported that Lowe's was a much better deal than Home Depot. This discrepancy has corrected, and now an argument could be made for either being the better buy–both are at historically good yields.

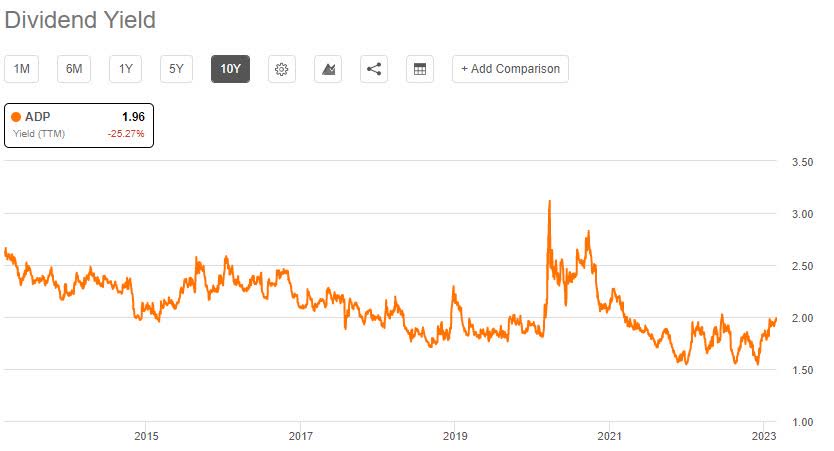

The final company I want to mention this month is Automatic Data Processing ( ADP ). The company has been on a steady slide since the start of the year, down over 6% versus the S&P 500's gain of over 4%. Of course, ADP was well overvalued at the beginning of the year and is now reaching its normal valuation. However, I am watching the trend and will likely add to my position if it hits a 2.5% yield, particularly if the market continues to rise. The chart below shows the dividend yield history for ADP.

{kind=link}

Final Thoughts

For the first time in a long time, investors can get a decent return on cash. It's a good time to be patient with the market. As rates keep going up, the case for cash will only get stronger, putting more pressure on dividend stocks.

This is the first month since 2016 that the portfolio has seen a decrease in projected income over the prior month. Of course, it was primarily due to timing on reinvestments. Over the coming months, this will correct itself as funds from the Intel sale are redeployed, and interest income on the cash held is included in the totals.

Thanks for reading, and as always, I would love to hear everyone's thoughts and investing ideas. The community here helps us all be better investors and uncover overlooked bargains.

For further details see:

My Dividend Growth Portfolio February Update: Cash Is Not Trash