WBA - My Dividend Growth Portfolio: Mid-Summer Update

2023-08-04 13:23:26 ET

Summary

- I have been collecting dividends and enjoying all-time highs in my portfolio, but I have not made many new purchases.

- I decided to sell my position in Cardinal Health due to a lack of significant dividend increase and swapped it for Home Depot, ADP, and CME Group.

- I discuss the variable dividend of Blackstone and my decision to hold onto my shares in Johnson & Johnson despite a recent exchange offer.

It's been a couple of months since I have done an update report. Summers are always hectic, so much to do in such a short time. This year has been particularly busy with a few weeks in Iceland and remodeling a rental. But, now things are winding down, and I will have more time to write again.

The upside of not having done an update is that there isn't too much to report. The market has been ripping higher, and as a result, I've been hunkering down, collecting dividends, and happy to get my 5% yield on cash.

While I haven't been doing much buying, I have enjoyed seeing my portfolio hit all-time highs. On July 3, the portfolio eclipsed its previous high set at the end of March 2022. Today, the portfolio sits at 4% above that mark. Even though all my investing goals revolve around growing the income, it's still nice to see the portfolio's overall value growing.

This month's update is in a slightly different format than usual. Mostly this is because I have done minimal buying the last couple of months, nor am I seeing any bargains that excite me much. But, I did eliminate one position, made some replacement purchases, and revised my expectations for Blackstone ( BX ).

Cardinal Health ( CAH )

I make every purchase with the intention of holding forever. Companies with long dividend growth histories tend to have periods of faster dividend growth and times when increases are lean. For this reason, I am patient with meager raises. However, sometimes conditions come together when it just makes sense to move on.

Cardinal Health was a micro-position in the portfolio at less than 0.5%. This automatically puts the company on constant watch as these small positions can often be more time-consuming than they are worth. However, I continued to hold CAH for several reasons; It was significantly undervalued, the opioid lawsuits appeared to be concluding, and increased earnings were just over the horizon.

As the lawsuits and earnings were resolved, I expected the company to reward investors with a more considerable dividend increase. However, instead, investors were given a significant run-up in share price. While I'm happy to have my portfolio increase in value, the pittance of a dividend increase led me to reevaluate my position. With the run-up in price, the yield had fallen to 2.3%, leaving many high-quality dividend growth companies as viable replacements.

While earnings forecasts look promising in the future, comparing Cardinal Health to other options made it clear that swapping for higher-quality dividend growth stocks made sense. Earnings forecasts can and do change; additionally, there is no guarantee that increased earnings will translate to increased dividends.

I opened the position in CAH in 2019 at $48.93 per share. Over the time I held the company, I collected $8.29 per share in dividends. My sales price was $84.75. This sum equates to a total increase of 90% when I held the company, significantly better than the S&P 500's roughly 60% gain over the same period.

The companies I evaluated distributing the funds into are Home Depot ( HD ), Automatic Data Processing ( ADP ), Snap-On ( SNA ), and Broadcom ( AVGO ). Broadcom quickly saw a massive run-up, from $630 to $900, so it was eliminated from consideration as a replacement.

As it stands, I ended up swapping the shares for Home Depot at an average cost of $286.34, ADP at $209.34, and CME Group ( CME ) at $180.34. These were all additions to positions I already held and were made at the end of May and early June.

I didn't consider Cardinal Health particularly overpriced at the time of the sale, and its long-term growth forecasts look fantastic. However, I decided to swap for faster-growing dividends. Had CAH been a more significant position in the portfolio, I may have opted to hang onto it for a couple more years to see if increased earnings translated to faster dividend growth.

Blackstone's Dividend

Blackstone is an anomaly in this portfolio as it is not a dividend growth company in the typical fashion. Not only do they pay a variable quarterly distribution, but the dividend has not grown consistently year over year. However, over time the distribution has increased. In 2013 they paid out $1.16, while this year's payout is projected at $3.61.

While the trend line of dividend growth has been up, it's not without setbacks. In 2015, the payout reached a peak that wasn't eclipsed until 2021! This year's payout is cut by nearly 27% from last year and only slightly higher than in 2021. The lumpiness of the distribution is shown in the table below.

{kind=link}

I entered 2023 with a projected dividend of nearly $4.20 a share on Blackstone. I have cut that to $3.60 today, nearly back to 2021 levels. This cut is creating a massive drag on my income growth for this year, as Blackstone is one of the largest income producers in this portfolio, contributing about 7% of the total. However, I accept this with the position, which, while the distribution is lumpy, still goes up over time.

Next year analysts are projecting record dividends for the company at $5.15 per share. While it's a little early to predict, next year should offer investors a welcome higher payout.

Johnson & Johnson ( JNJ ) Offer

I was surprised when J&J announced the exchange offer for Kenvue shares. The offer is similar to General Electric's ( GE ) offer for Synchrony Financial ( SYF ) in 2015. I only remember that one because I was a shareholder in GE and felt cheated at the time.

If you are a shareholder in a company, it should be the whole company, and Kenvue is part of JNJ. Shareholders should not have to choose whether or not they want to own something that already belongs to them. At least with the GE-SYF deal General Electric made it clear that they planned to retire the shares, that isn't so clear here, although I expect JNJ will.

Either way, I plan to hold my JNJ shares. Consumer product lawsuits have a different tone than just a few years ago. I can't help but imagine how much uglier it would be today for the tobacco companies than in 1998.

Maybe it's just my risk tolerance these days, but I dumped my 3M ( MMM ) shares because of the lawsuits. I think it's ludicrous that a company can use (or attempt) a bankruptcy the way 3M and JNJ are trying to contain liability. However, JNJ will survive this, but I don't want to own any future liabilities with Kenvue's products. I will hang on to the shares if they have to distribute shares, as I always do with a split.

Portfolio Goals

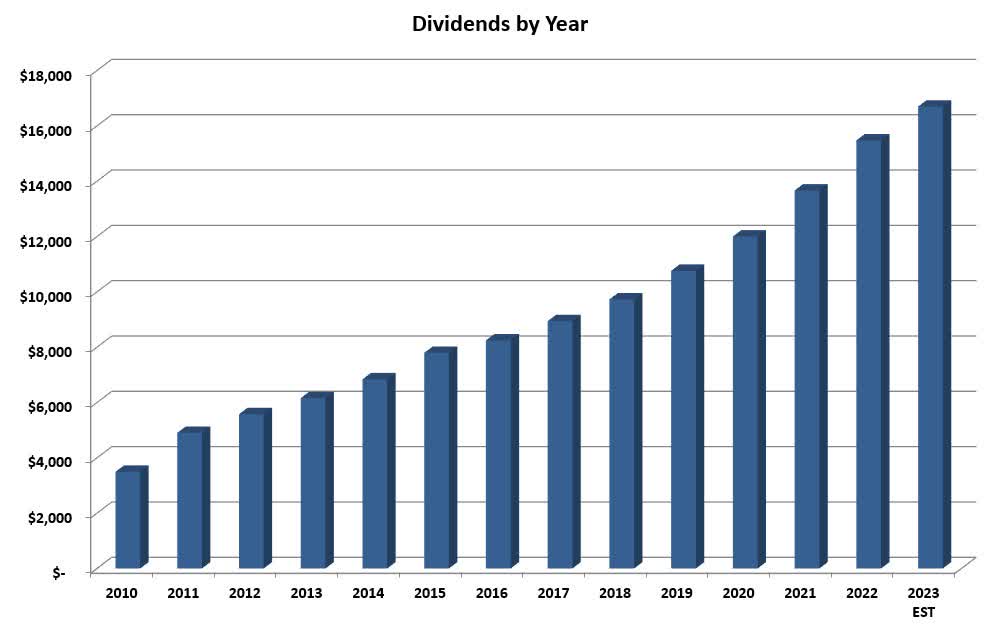

The portfolio goals are simple: Grow the income by 10% annually with dividends reinvested and 7% annually without reinvesting. This goal allows my income to double approximately every seven years while reinvesting and every ten years after I begin withdrawing the dividends. It's important to know that this portfolio has been closed to new capital since 2016. The graph below shows the steady progress of income growth.

{kind=link}

How Am I doing so Far in 2023?

At the end of July, income is projected to be up 7.9% from 2022. This is down slightly from my last report at the end of April. Three factors lead the decline:

- Firstly, I have been accumulating cash rather than buying. As it stands now, the portfolio holds over a year's worth of dividends in cash. At today's nearly 5% yield on cash, I am comfortable staying in cash for two to three years while I wait for the right buys to come my way. But, I am approaching the limit of the amount I want to hold.

- The ongoing reduction in the Blackstone dividend is covered above. At the end of April, I cut my projection to $3.85, and it continues to fall.

- While I use conservative dividend growth projections, the few increases over the summer months have failed to meet my expectations. These included Medtronic ( MDT ), MSA Safety ( MSA ), The J.M. Smucker Company ( SJM ), and Walgreen Boots Alliance ( WBA ). The two that exceeded my expectations, Duke Energy ( DUK ) and NNN Reit ( NNN ), are such low dividend growth that they have no real impact.

At this point, I will miss my 10% goal, as even if I reinvested all the cash now, a single quarter of dividends would likely not get me there. However, as I wrote in my 2023 preview, a down year was possible as income growth was well ahead of historical expectations.

While the portfolio has no goals around the total return, many readers are interested. Even though the portfolio is at all-time highs, it is still trailing the S&P 500 significantly this year, with a Year to date return of 12.2%.

August's Expected Dividend Increases

The only expected dividend increase this month is Altria ( MO ). This raise is important, as Altria is the most significant income contributor at over 11% of the total income.

While I purchased most of my Altria shares in 2009 and even earlier, I added shares in 2019 and 2020. An interesting fact about MO, since 2010, Altria has paid me 152% of my purchase price in dividends, even with the shares added in recent years!

Most people would never guess a company yielding 8% has 5 and 10-yr dividend growth rates of nearly 8%. Of course, the last couple have been sub 5%, and given the JUUL and Cronos ( CRON ) disasters, investors should be ecstatic they were that big.

The smaller increases are likely to be the new normal. I also expect this year to be in the 3-4% range, and I don't foresee raises topping 5% in the near future.

Recent Purchases

None. The market knows only one direction right now. There is nothing I'm excited to add to right now and no bargains that I have enough conviction in to start a new position.

Other Possibilities I am Watching

Since this is a closed portfolio, I can only buy some of the companies that look interesting. This section covers what I purchase and consider in my other portfolios. My other portfolios have different goals and rules, but are also dividend growth portfolios.

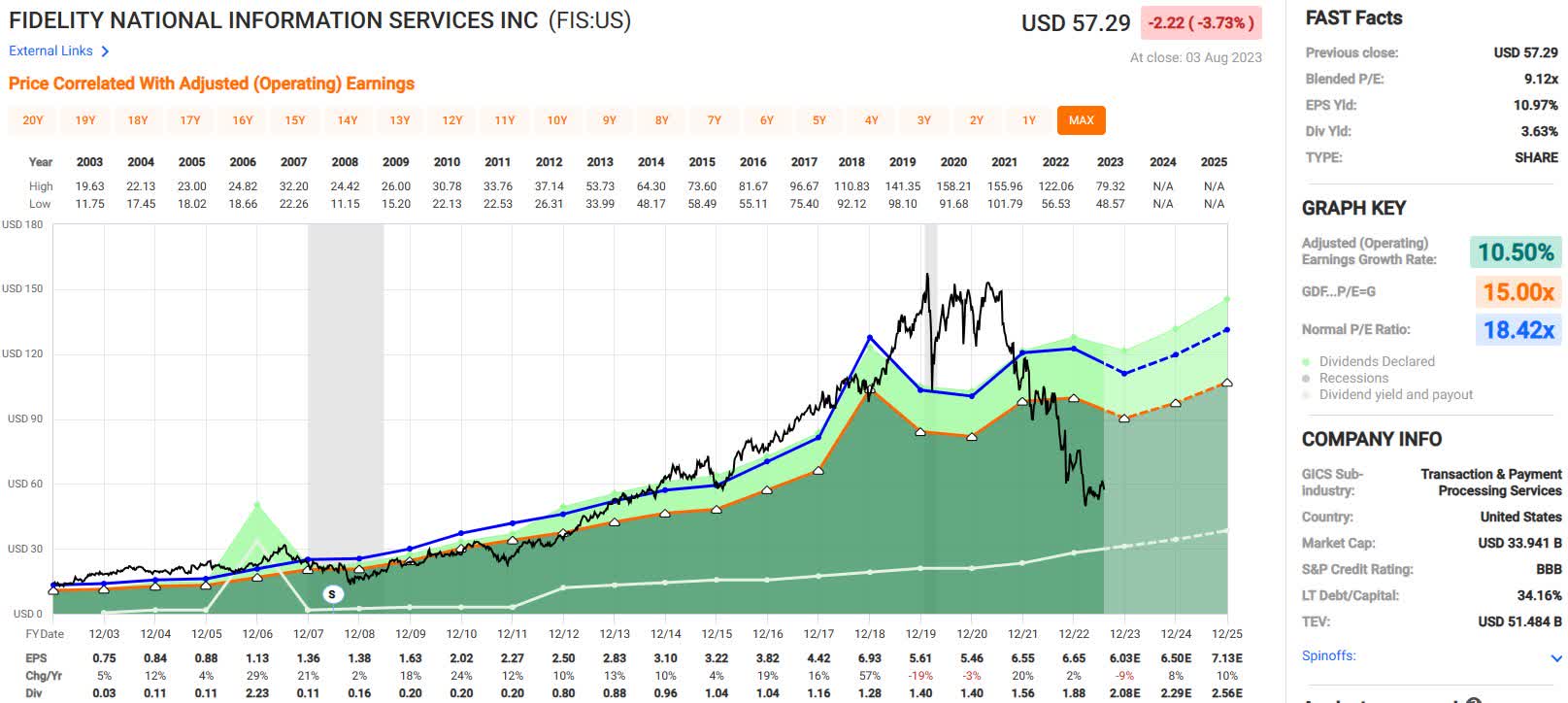

Bargains have been shrinking rapidly in the last few months. I continue to make small daily purchases of Schwab U.S. Equity ETF ( SCHD ), even though the price has started to climb. My only other purchases were adding small amounts of Kroger ( KR ) at around $45 and Fidelity National Information Services ( FIS ). FIS continues to offer a good price. The Fastgraph below shows the relative undervaluation of FIS compared to historical.

{kind=link}

Even though banks are off their lows, they still look attractive here. While I only hold a few big banks, I have been tempted by some smaller regionals. I find myself looking at First Interstate Bank ( FIBK ) often.

When I consider the risks in the market right now, the only two companies I have genuinely considered adding to this portfolio are Nexstar Communications ( NXST ) and United Parcel Service ( UPS ), which continue to look like good deals.

Retailers continue to offer better-than-normal deals, even though they are up significantly. Target ( TGT ) and Tractor Supply ( TSCO ) are the most interesting right now, although Best Buy ( BBY ) maintains the top spot on my bargain watch list. I'm just not convinced retailers are out of the woods yet.

Finally, if I were in the market for a high-yield company, I would look hard at AT&T ( T ) and Verizon ( VZ ). Verizon has rarely offered such a large yield.

Final Thoughts

Next month, I will be back to my regular format, hopefully, with some purchases to report and several upcoming dividend increases.

I have spent much time playing with the numbers to determine how long I want to hang onto cash at today's returns. There are a lot of variables and considerations, so it's a complex decision. With my goal of buying companies with an initial yield of 3% and 10% dividend growth, holding cash for 2-3 years is about the max where it makes sense right now.

I don't know how long the market can continue its run, but there are more headwinds than tailwinds at this point. I see a big test when student loans resume in September, although I'll give it 50/50 that it actually occurs. Best of luck to everyone, and I'd love to hear where everyone is putting money during this market run-up!

For further details see:

My Dividend Growth Portfolio: Mid-Summer Update