WBA - My Dividend Growth Portfolio November Update - Thankful For Dividend Raises

2023-12-01 16:20:12 ET

Summary

- The market has been consistently moving higher, making bargains disappear quickly.

- I am considering selling the position in Walgreens for tax loss harvesting but I'm struggling to find a suitable replacement with a similar yield.

- The portfolio is projecting income growth of near 10% this year but trails the S&P 500 considerably. However, the portfolio is at an all-time high valuation.

What a difference a month makes! The market was down significantly at the end of October, and bargains were popping up everywhere. Only a month later, down days have been few and far between, with the market looking for reasons to keep moving higher. It's been great for watching the portfolio balances, but not so great for bargain hunting.

All in all, it was a quiet month. While October had several exciting events to share, this month was much more subdued. November was a slow month for dividend collection within the portfolio, although it was a big month for dividend increases. As the market moved higher, my excitement about the available bargains waned. Even bond yields were down nearly 12%.

As has been the case for most of the year, I have continued to accumulate cash. While the cash pile did drop some in October after a bond purchase, it began climbing again last month and stands near record highs. I continue reinvesting 25% of stock dividends, allocating 25% to individual bonds, and holding the other 50% as cash for the right buying opportunity. I will stick with this plan as long as cash yields 5% or the right deal comes along.

Still looking for an exit in Walgreens ( WBA )

As I have written before, I will exit my Walgreens position. I am still wanting a better exit price, but this has yet to materialize. Now that the last ex-div date has passed, I am considering dumping it for tax loss harvesting. The sad part is that I sold it at a loss about this time last year and rebought it at a lower price after the wash period. It is one of the worst investing decisions I have made, and I made it twice!

The biggest challenge with selling WBA is finding a replacement. I like to replace sales with equal or better yield and equal or higher quality. With WBA yielding nearly 10%, there are few replacement candidates. The apparent replacement is Altria ( MO ), which would be a no-brainer. However, this portfolio is well overweight MO (accounting for over 11% of the dividends), and I have been actively working to bring that down for several years. I did, however, sell enough WBA this month to buy six shares of MO and bring the holding up to a round lot number.

There are a few other companies that I have considered as replacements. Ares Capital ( ARCC ) and Main Street Capital ( MAIN ) are two that I am leaning toward and was planning to buy at some point. However, I would prefer to add these during a recession as these companies get flattened, and yields jump high enough to offer a comfortable margin of safety. The chart below shows how ARCC behaved in both 2009 and 2020.

Another possibility is accepting the loss of income and rolling the WBA proceeds into my Enterprise Products Partners ( EPD ) position. While there would be a loss of income, there are some offsetting tax benefits going this route. Additionally, EPD looks poised to give better increases for a couple of years.

I will likely do a combination of a BDC company and some EPD to balance risk and yield. However, I may hang onto WBA for a while longer and see what happens. A price rebound is still likely, particularly if the dividend is cut and a clear path forward is articulated; I have yet to lose any income as the dividend is still intact.

Portfolio Goals

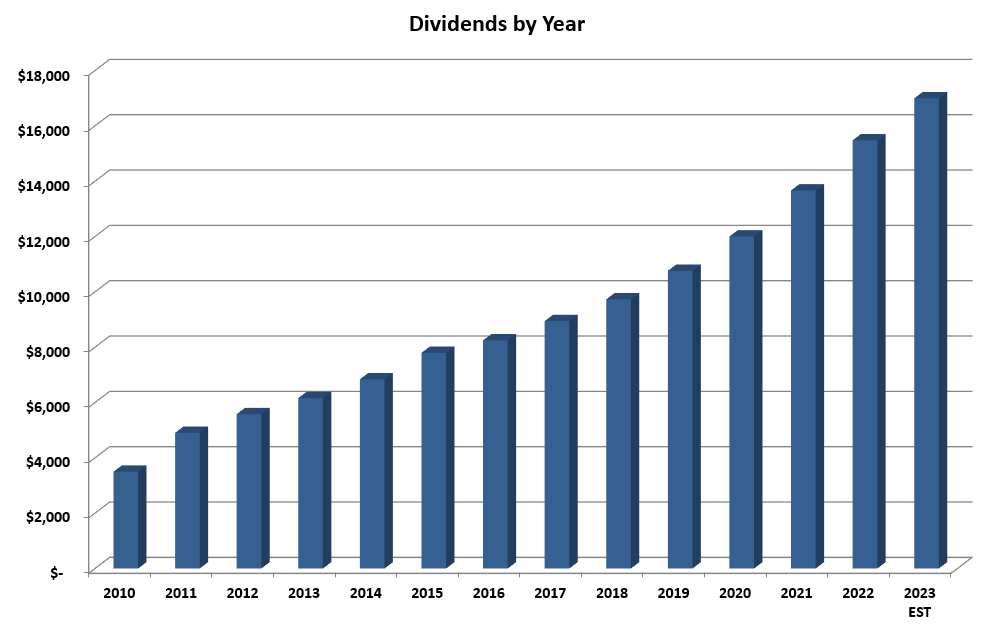

The portfolio goals are simple: Grow the income by 10% annually with dividends reinvested and 7% annually without reinvesting. This goal allows my income to double approximately every seven years while reinvesting and every ten years after I begin withdrawing the dividends. It's important to know that this portfolio has been closed to new capital since 2016. The graph below shows the steady progress of income growth.

{kind=link}

Wyo Investments

Portfolio Guidelines

I use guidelines rather than rules to achieve my goals. Rules imply something hard and fast, whereas guidelines are flexible but give a general direction to follow. I keep these simple, as I have found that complexity adds time without any real benefit. These have evolved over the years, the most recent being the addition of selling covered calls in certain circumstances.

- Invest in companies from the Champions and Contenders list with at least 15 years of dividend growth.

- Look for companies with a 3% starting yield and the potential to maintain a 7% dividend growth for decades. The growth is critical as it's impossible to continue growing income at 7% without reinvesting unless companies raise distributions by at least that amount.

- Replace (or sell covered calls against) significantly overvalued positions if the opportunity exists to reduce risk and increase income. In practice, this usually means higher quality at a higher yield.

- I want to see flat to mild payout ratio creep. A payout ratio growing from 30% to 35% over ten years is acceptable. One that has gone from 30% to 60% is not. I want companies to grow the dividend with earnings, not by increasing the payout ratio.

- Unless it is well-diversified across industries, every sector should account for at most 20% of the income. This burned me in 2016 when several energy companies cut dividends.

Again, these are just guidelines and are flexible to accommodate what makes sense to achieve my overall goals. I follow a few other items but don't see them as integral to my investing. Instead, these tend to be more personal preferences. They include avoiding foreign companies because I don't enjoy accounting for the taxes and FX rates causing fluctuating dividends.

How am I doing so far in 2023?

For this year, I am projecting dividend growth of 6.0%, which is below all of my goals. This is primarily due to the massive reduction in the Blackstone ( BX ) dividend for the year and the limited reinvesting. With interest included, the total income is projected to be up 9.8% for the year. These results are acceptable, if not great, considering the Blackstone dividend, which is lumpy but has increased over the years. Next year's dividend projected for BX by analysts today would add 2.5% immediately.

As many readers are interested in total return, I do track it, although it is not a goal of the portfolio. The portfolio's goal is only income-oriented. While the portfolio trails the S&P 500 significantly this year with a 12.6% gain, it is sitting at all-time highs, something the S&P still has yet to achieve.

November's Dividend Increases

Last month, there were three dividend increases, and they were massive! I was expecting much more conservative numbers, so it was encouraging to see double-digit increases all around.

Automatic Data Processing ( ADP )

With 47 years of dividend increases, ADP is still going strong! The company has 5 and 10-year dividend growth rates of about 12%, and it did it again this year with another 12% raise. The company is trading slightly above my first buy point, and I am considering adding more.

Aflac ( AFL )

Aflac is another company with a long dividend growth history that still churns out significant increases. After 41 years, the company still has a 10-year growth rate of 9% and a five-year growth rate of 13%. Aflac matches earnings growth to dividend growth well, so its raises can be lumpy. Last year's was only 5%, while the year before was 20%. This year's surprised to the upside at a whopping 19%! Aflac is currently trading about 15% above my first buy point.

Snap-On ( SNA )

Last month, Snap-On extended its dividend growth streak of 13 years with another nearly 15% raise, matching its 5 and 10-year dividend growth rates. This one blew away my estimates. EPS Growth is expected to slow over the next couple of years, so I'm expecting the dividend growth rate to slow as well. In the meantime, the raises have been fantastic. SNA is trading about 15% above where I would like to add more, but I have yet to rule it out with the funds I have for reinvestment.

December's Expected Increases

This month's raises will mostly take effect in 2024, with the notable exception of Broadcom ( AVGO ). I have left off Fortune Brands Innovations ( FBIN ) as they reduced the dividend last year when they spun off MasterBrand ( MBC ) and have given no indication of resuming increases. However, I think they may announce an increase this year.

Broadcom

It's been a wild year for AVGO, with the stock up over 70% on the tails of an AI bubble. If only earnings were up 70% to match! Unfortunately, earnings are projected to be flat for the year and up 9% in 2024.

The company has expanded the payout ratios considerably since 2016 and is approaching the point where dividend growth will need to match earnings growth. However, I think they can push out a 7-9% increase this year. Anyone looking at the 28% 5-year growth rate will likely be disappointed.

Broadcom has become the single largest holding of my combined portfolios. It is up five times since I was buying in 2020, on the back of an over 6% yield. As dividend growth investors, we sometimes catch a significant gain by focusing on bargains. Right now, I couldn't consider adding any AVGO as I see it as significantly overvalued based on historical metrics.

CVS Health ( CVS )

CVS has given 10% raises in the last two years after keeping them frozen for several years. While two years is hardly a reason to expect another raise this year, I would be surprised if they didn't.

The company's price has tanked along with WBA, even though CVS is as much an insurer as a retailer. Earnings are flat this year; expecting another 10% dividend increase is asking a lot. I am expecting something in the 5% range.

I show CVS as a good bargain, although I am not in a hurry to add more. The price will be dragged down by its retail segment for the next couple of years, even though this is just a small part of its business. In the long run, this is a profitable company with the potential for good dividend growth.

Abbot Labs ( ABT )

Since spinning out AbbVie ( ABBV ) well over a decade ago, I have nearly wholly ignored this position. It is just a safe, steady company that never seems to have any drama. Additionally, it has been (and continues to be) overpriced for the past decade.

The company's dividend increases have been lumpy over the past decade, ranging from 25% in 2021 to a meager 1.5% in 2017. Putting the 10-year growth rate at 7% and the 5-year growth rate at 12%. I'm not expecting this year to be a big year, and I expect we will see a raise in the 5% range.

CME Group ( CME ) Special Dividend

While I don't try to predict special dividends, CME has announced one every December since 2012, so it is reasonable to expect one again this year. They have a unique dividend policy of paying out nearly all their cash flow. That would conservatively put this year's in the $4.50 range, making the effective yield on the company over 4%.

Sales in November

There were no sales other than the previously mentioned sale of just a couple of shares of WBA.

Purchases in November

There are two types of purchases I make. The first is the reinvestment of dividends. I try to stick with good bargains for these purchases, generally adding to companies I already hold. However, I will start a new position if enough funds are available to open a meaningful one and the right opportunity presents itself. The second type of purchase is the reinvestment from a sale. I focus on replacing the income with a higher overall quality dividend for these.

As mentioned above, I replaced the sold WBA shares with six shares of MO at $40.24/share.

Regular Purchases

November is a slow month for dividends paid, and with me only reinvesting 25% of the dividends collected at this time, purchases were light.

Kroger ( KR ) was the only company I bought as I continue building this position. I was looking to add below $42 but settled for five shares at an average price of $42.50. As this is still a small position in the portfolio, I will continue to look for opportunities to expand it.

What Else Am I watching?

Since this is a closed portfolio, I can only buy some of the companies that look interesting. This section covers what I purchased and considered in my other portfolios and the bargains I am watching. My other portfolios have different goals and rules but are also dividend growth portfolios.

Last month, there wasn't a lot that interested me as everything was moving higher. As I have all year, I continued my small daily purchases of Schwab U.S. Dividend Equity ETF ( SCHD ). But, other than those purchases, I did little buying, adding to my Lowe's (LOW) position early in the month in the low $190s.

Retailers have bounced well off their lows at the beginning of the month, but they still look like bargains on paper. Best Buy ( BBY ) is still the cheapest of the bunch, but Lowe's and Tractor Supply ( TSCO ) are still well in the bargain zone. Home Depot ( HD ) is showing as a slight bargain. However, I'm still cautious about all these names as a whole.

Staples retailers Kroger and Target ( TGT ) are still historically cheap, although Target is far from the deal it was early in the month.

Traditional dividend growth stocks currently offering good value include Texas Instruments ( TXN ) and Johnson & Johnson ( JNJ ). Texas Instruments has increased significantly since the end of October but still offers a historically good yield. I'm still leery of JNJ with the talc-related lawsuits, but lawsuits generally have a way of passing.

Automatic Data Processing ( ADP ) and Cummins ( CMI ) are sitting within 5% of my first buy target, and I may stretch a bit to add to my ADP position.

Final Thoughts

The stock market is partying like it's 1999, or maybe 2021 is more appropriate? Either way, it only seems to be going in one direction. I'm surprised by the number of companies still in my buy ranges on my watchlist, which is currently standing at 30. In 2021, the list bottomed out at less than ten companies as buys. Of course, this is reflective of the Magnificent 7 driving the market returns this year.

As I've been for many months, an income-oriented investor shouldn't be scared of cash right now. There is time to let the right price come to you. This was different in 2021 when there was no return on cash; every day a dollar sat on the sidelines was income lost. Today, with cash yielding 5%, it's a different story. Even when the market seemingly only goes up, the bargains will come to the patient investor.

For further details see:

My Dividend Growth Portfolio November Update - Thankful For Dividend Raises