USOI - My Income Portfolio: The Market Is Us

2023-06-01 17:18:39 ET

Summary

- The market is composed of the intelligence and emotions of its participants, millions of people whose judgments and assessments guide its prices.

- Right now, the market is dominated by the expectation of a recession, and any data is read in its anticipation or confirmation.

- The CEFs and ETFs in my portfolio have on the whole gone down in recent months, and in some cases more than the market average.

- My strategy leads me to accept periods in which the performance of my titles may be negative, and only partly offset by dividend flows.

- In this article, I have decided to analyze the Total Return of my titles for the last ten years, broken down year by year.

Giotto’s Frescoes in Padua

Padua is a beautiful and relaxing city in the Po Valley, just a few kilometers from Venice, crisscrossed by numerous waterways and dotted with porticoes just about everywhere along the streets of the historic center. Porticoes are a common feature of many Po Valley cities and allow people to walk sheltered from the weather while enjoying their artistic and architectural beauty.

Sumptuous pictorial cycles painted by different artists during the 14th century decorate the walls of numerous religious buildings and monumental complexes in Padua, showing a unity of style and content whose model is the Scrovegni Chapel. This chapel is one of the masterpieces of Western art, frescoed by Giotto between 1303 and 1305 with stories from the Old and New Testaments.

There is one panel, in particular, that sums up all the revolutionary features of Giotto’s painting: the “Lamentation over the Dead Christ.” The composition is off-center and the whole scene converges dramatically in the lower left corner, where the body of Christ lies surrounded by a crowd of mourning figures who create, with the volume of their bodies, a credible physical space around him.

The realism of the scene is made even more evident by the presence, in the foreground, of two figures (one imagines female as their heads are covered) crouching with their backs turned, hunched over in pain and weeping. Two anonymous, undefined sculptural masses, but they convey tangible suffering. Nothing else is needed for the painter to engage the viewer and make him become a sharer in the drama: just these two figures seen from behind.

The Silent Majority

Those two characters are us. We, the anonymous spectators intent on observing and sharing what is happening at center stage. We, a mute and indistinct humanity that nevertheless participates in the events of history, makes political choices, determines the course of financial markets. A silent majority animated by the same feelings, expectations, anxieties, fears, desires, hopes or pains reflected in Giotto’s fresco, exactly as in the prices of financial instruments giving substance to stock market fluctuations, sudden collapses and irrational bubbles. Markets are composed of intelligence, emotions and the millions of judgments its participants make. The market is us.

Right now, the market is dominated by the expectation of a recession. Like a self-fulfilling prophecy, any data on output, employment or inflation is read as an anticipation or confirmation of an impending recession. Newspapers do their best to dispense advice on how to prepare one’s portfolio for this scenario, suggesting where to direct one’s investments to better withstand its impact, and the silent majority moves, makes decisions, reacts, in turn directing the market.

Every action is being opposed by an equal and opposite reaction: this is the third principle of dynamics. The silent majority responds to external stimuli and makes decisions, which in turn affect market performance. The prophecy is self-fulfilling.

But what happens if instead of reacting we hold our nerves and refuse to be carried along by the current? Even I, I confess, often wonder what I could do, assuming it makes sense to constantly disassemble and reassemble my portfolio. It would be different if I were completely liquid, but this is not the case, having slowly built up my portfolio (while keeping about 10% cash as a buffer) and currently having numerous loss-making positions, which I think can be seen as normal right now. Now sell to consolidate losses? Is this the spirit in which I devised my dividend-based investment strategy?

Indeed, the cash flow generated by CEFs, ETFs and (a few) individual stocks offers me a not inconsiderable psychological lifesaver in times of crisis, despite persistent fears about possible dividend cuts, especially in the case of equity funds that base part or most of their distributions on capital gains. So, I have decided to hold my nerve and continue to believe in my choices, made in the light of considerations that have not waned over time, even if the performance of some titles has somewhat betrayed my expectations. But such outcomes have to be taken into account.

Waiting For The High Tide

Buying and reselling titles by trying to imagine and anticipate future price movements is not part of my investment philosophy (while a different thing is to lighten one’s positions when prices reach all-time highs). Of course, this approach leads me to endure temporary capital losses, and thus years with negative Total Returns, as 2022 has been for my portfolio and that of other investors like me.

If it’s true, as Warren Buffett says, that “much success can be attributed to inactivity” and that the stock market serves as a “relocation center at which money is moved from the active to the patient,” it’s just a matter of being able to sit back and wait confidently for the high tide, which will lift all boats again. Which is by no means easy, though, bombarded as we are by financial news reports spewing anxiety by the handful.

The Total Return of My Titles

However, I have decided to analyze the Total Return for the last ten years of all my titles, broken down year by year, as reported on the Morningstar website. Some are younger, but Total Return since their launch will be reported in each case.

As you may know, my investments are divided into three different income portfolios: Cupolone, my primary CEF portfolio; Giotto, comprised of ETFs that adopt a covered-call strategy; and Masaccio, my “tactical” portfolio. I briefly summarize the composition of my overall portfolio, in which there are precisely 18 CEFs, 5 ETFs, 1 ETN and 2 stocks:

Closed-End Funds

- BlackRock Science And Technology Trust ( BST )

- Calamos Dynamic Convertible and Income ( CCD )

- Calamos Global Total Return ( CGO )

- Eaton Vance Enhanced Equity Income II ( EOS )

- Eaton Vance Tax-Adv. Global Dividend Opps ( ETO )

- Eaton Vance Tax-Adv. Dividend Income ( EVT )

- Guggenheim Strategic Opp ( GOF )

- John Hancock Tax-Adv. Dividend Income ( HTD )

- Pimco Corporate & Income Strategy ( PCN )

- Pimco Dynamic Income ( PDI )

- John Hancock Premium Dividend ( PDT )

- Pimco Corporate & Income Opportunities ( PTY )

- Cohen & Steers Quality Income Realty ( RQI )

- Royce Value Trust ( RVT )

- Special Opportunities Fund ( SPE )

- Cohen & Steers Infrastructure ( UTF )

- Reaves Utility Income Trust ( UTG )

- XAI Octagon FR & Alt Income Term Trust ( XFLT )

Exchange-Traded Funds

- JPMorgan Equity Premium Income ( JEPI )

- JPMorgan Nasdaq Equity Premium Income ( JEPQ )

- Global X Nasdaq 100 Covered Call ( QYLD )

- Global X Russell 2000 Covered Call ( RYLD )

- Global X S&P 500 Covered Call ( XYLD )

Exchange-Traded Notes

- Credit Suisse X Links Crude Oil Shares Covered Call ETN ( USOI )

Stocks

Below is a list of all 26 of my titles, broken down by financial instrument, as shown above. For completeness, both price and NAV data are given, although, for my analysis, the focus is exclusively on the latter (for the two stocks, the graph of price trend since launch will be given).

Close-End Funds

BST

{kind=link}

Disastrous 2022 after a series of positive years. Important recovery for early 2023. NAV performance is largely positive since launch.

CCD

{kind=link}

Disastrous 2022 after a series of positive years with a slide into negative territory in 2018. Timid recovery for early 2023. NAV negative performance since launch.

CGO

{kind=link}

Disastrous 2022 after a series of positive years with a slide into negative territory in 2018 but excessive year-to-year inconstancy in yields. Good recovery for early 2023. NAV performance quite negative since launch.

EOS

{kind=link}

Disastrous 2022 after a series of positive years, albeit among ups and downs. Important recovery for early 2023. NAV performance barely negative since launch.

ETO

{kind=link}

Quite negative 2022 after a series of positive years with a slide into negative territory in 2018. Good recovery for early 2023. NAV performance quite positive since launch.

EVT

{kind=link}

2022 negative after a series of positive years with a slide into negative territory in 2018. Also barely negative for early 2023 but NAV performance quite positive since launch.

GOF

{kind=link}

2022 negative after a series of positive years but with too much inconstancy in returns. Timid recovery for early 2023. NAV performance largely negative since launch, which does not justify the exaggerated premium requested to buy this stock in my view.

HTD

{kind=link}

2022 just negative after a series of positive years with two slips into negative territory in 2018 and 2020. Also negative for early 2023 but positive NAV performance since launch.

PCN

{kind=link}

2022 negative after a series of all positive years. Timidly positive also for early 2023 but NAV performance quite negative since launch.

PDI

{kind=link}

2022 negative after a series of all positive years. Timidly positive also for early 2023 but NAV performance quite negative since launch.

PDT

{kind=link}

2022 just negative after a series of positive years with two slips into negative territory in 2018 and 2020. Also negative for early 2023 but NAV performance slightly positive since launch.

PTY

{kind=link}

2022 negative after a series of positive years. Timidly positive also for early 2023 but NAV performance quite negative since launch.

RQI

{kind=link}

2022 very negative after a series of positive years with two slips into negative territory in 2018 and 2020. Also barely negative for early 2023 and NAV performance negative since launch.

RVT

{kind=link}

2022 very negative after a series of positive years with three slips into negative territory in 2014, 2015 and especially 2018. Timidly positive for early 2023 and NAV performance largely positive since launch.

SPE

{kind=link}

2022 negative after a series of positive years with three slips into negative territory in 2014, 2015 and 2018. Timid recovery for early 2023 but negative NAV performance since launch.

UTF

{kind=link}

2022 negative after a series of positive years with three slips into negative territory in 2015, 2018 and 2020. Also negative for early 2023 but positive NAV performance since launch.

UTG

{kind=link}

2022 negative after a series of positive years with three slips into negative territory in 2015, 2018 and 2020. Also negative for early 2023 but NAV performance largely positive since launch.

XFLT

{kind=link}

2022 negative after a series of positive years with a slide into negative territory in 2018. Timidly positive for early 2023 but NAV performance quite negative since launch.

Exchange-Traded Funds

JEPI

{kind=link}

2022 slightly negative after a largely positive 2021. Timidly positive for early 2023 and positive NAV performance since launch.

JEPQ

{kind=link}

Very young ETF, shows a decidedly positive 2023 start but NAV performance since launch just negative.

QYLD

{kind=link}

2022 negative after a series of positive years with a slide into negative territory in 2018. Important recovery for early 2023 but NAV performance quite negative since launch.

RYLD

{kind=link}

2022 negative after a positive 2021 and a barely negative 2020. On parity for early 2023 but NAV performance quite negative since launch.

XYLD

{kind=link}

2022 negative after a series of positive years with two slips into negative territory in 2018 and 2020. Positive for early 2023 and NAV performance just positive since launch.

Exchange-Traded Notes

USOI

{kind=link}

2022 positive after a series of up-and-down years with two slips into negative territory in 2018 and 2020. Timidly positive for early 2023 but NAV performance disastrous since launch. The considerations below apply to this ETN’s presence in my portfolio.

Stocks

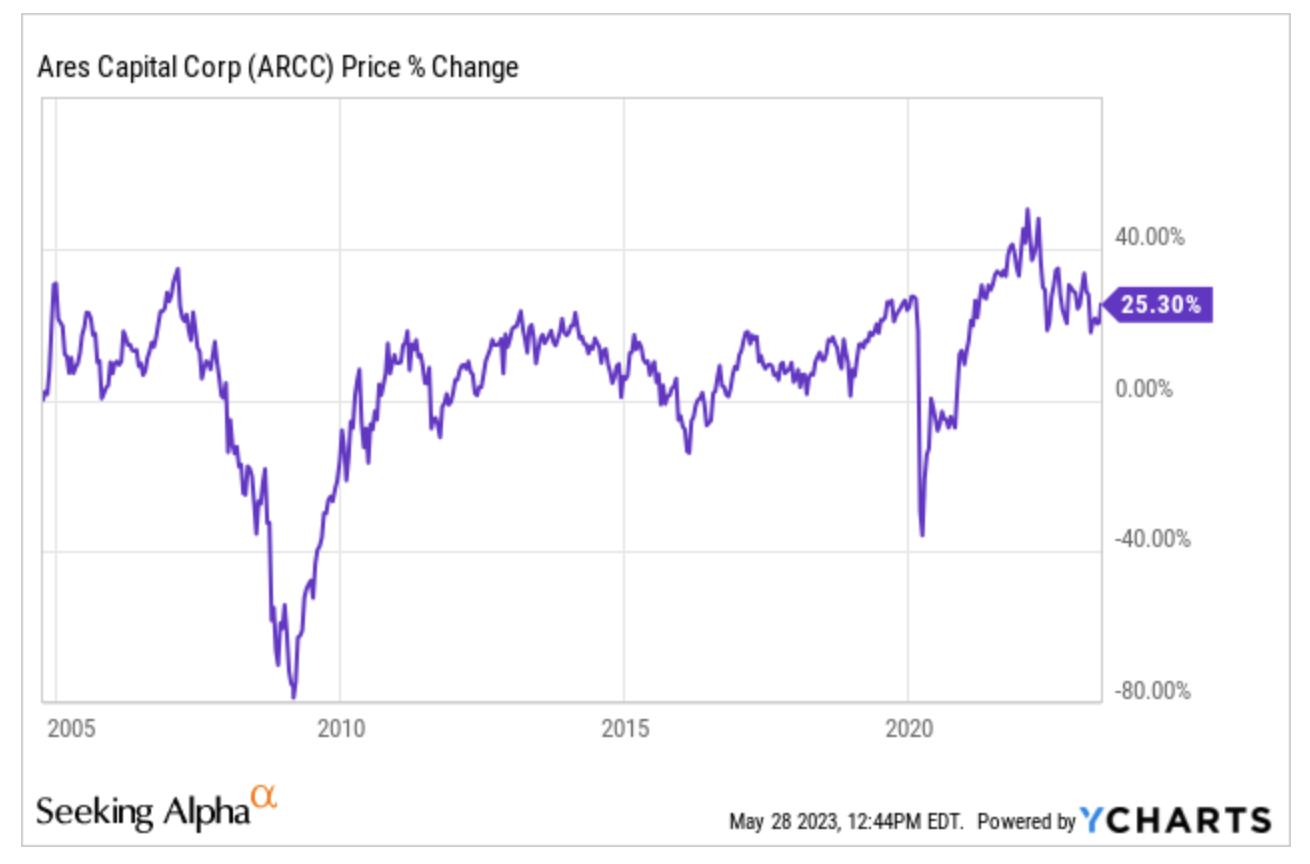

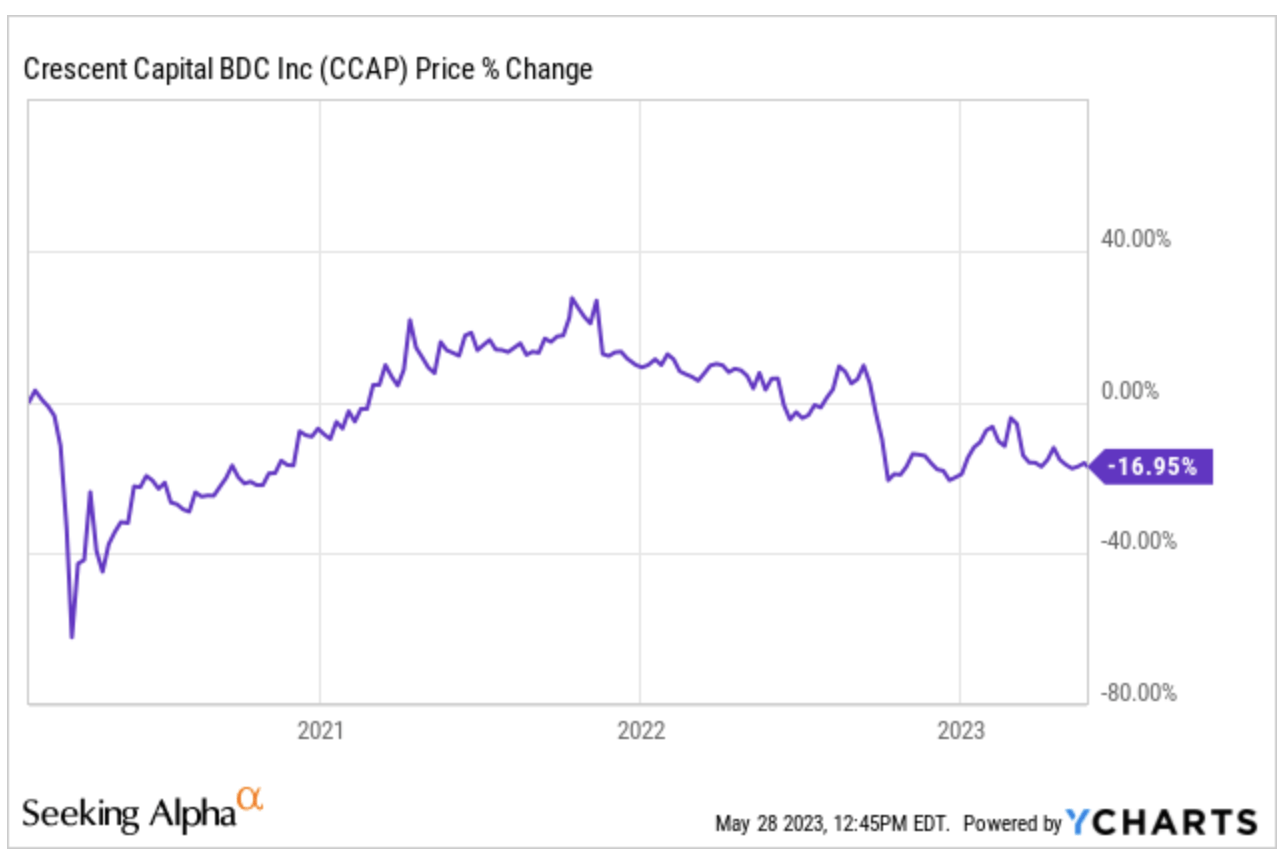

For these two BDCs (Business Development Companies) I simply report the price trend since launch, positive for ARCC and negative for CCAP.

{kind=link}

{kind=link}

Throwing My Heart Over the Hurdle

As can be seen, the Total Return for the last ten years of all my titles, broken down year by year, shows heterogeneous trends. In some cases, an excessive inconsistency of returns even projects their NAV for early 2023 into negative territory.

I like to think that this portfolio balance shows up as negative because of an averagely disastrous market in 2022 overall and not because of the investment strategy. My last article on this subject – from January 2022, before the outbreak of the war in Ukraine and record inflation – shows a completely different situation, and largely positive Total Returns in the portfolio as a whole.

To chase a positive Total Return year after year at all costs would lead me to adapt my portfolio from time to time to changing market conditions, which would make me take on connotations of a trader rather than an investor. As an investor, therefore, I must psychologically cope with bad years such as 2022 and (at least in part) this 2023, trying to resist the temptation of moody moves and “throwing my heart over the hurdle.”

By the way, XFLT has announced a dividend of $0.085 for June, a 16 percent increase over May’s distribution: let’s take this is a sign of hope, a kind of “dove with an olive branch.”

What About USOI? (Take 2)

As I wrote in my previous article , during April I decided to significantly reduce my position in USOI. In early May, the second dividend since UBS took over Credit Suisse was announced, and it was $1.9479, which is much closer to the historical average for this title than the April dividend. It is too early to jump to conclusions, but this apparent return to normalcy gives me hope for the ETN’s survival. At around $72, I bought back a few shares, bringing my position in USOI back to 50% of its previous position and around 1% of my overall portfolio. For now, I have stopped here; it is such a low percentage that I am not worried about keeping it, partly because ETNs are the only securities whose “coupons” – I want to remind here – generate so called “other incomes.” These are the only ones that can allow me, as an Italian, to offset them, month after month, using prior losses.

Under the Starry Sky

Everyone probably agrees that 2022 has been a dark year for financial markets. The CEFs and ETFs in my portfolio also fell, of course, and in some cases more than the market average. I have been buying when I can, opening new positions and trying to average down those already open, from a long-term perspective.

My strategy obviously leads me to accept periods in which the performance of my titles (and therefore their Total Return) may be negative, and only partly mitigated by dividends, which, however, allow me to reinvest at profitable prices, partly offsetting the capital loss of the portfolio.

Thus, for me, the biggest concern is the possible cut in dividends or distributions, from which I have tried to protect myself by diversifying sectors and managers, while I have very few individual stocks for the reasons I have already explained in a previous article .

In the absence of such cash flow, the psychological balance would be unsustainable for me, leaving me at the mercy of the elements. Let’s say that dividends are for me like the reassuring blue sky studded with stars frescoed by Giotto in the inimitable vault of the Scrovegni Chapel.

For further details see:

My Income Portfolio: The Market Is Us