BAYZF - My International Portfolio: Approaching Another Major Milestone And Looking Into Recent Additions

2023-07-27 13:16:21 ET

Summary

- I'm your main street neighbor investor in his mid-30s sharing his brokerage account investment journey pursuing a dividend growth strategy.

- Dividends received YTD totaling $4155 up 18% compared to the same period last year.

- I believe the current market is strained but I keep investing as often as I can to ensure time in the market as opposed to timing the market.

- As my portfolio approaches another milestone, I discuss my investment principles and learnings while introducing new holdings in the portfolio.

Disclosure

Within this article, the company Novo Nordisk A/S ( NVO ) will be mentioned. For the reader, I'd like to disclose that I'm an employee of the company. The nature of my position is an office job that does not concern sales.

The Current Market

My last update is all the way back in October 2022, and a lot has happened since then. At that point in time, the S&P 500 was down more than 25% for the year, and the Nasdaq was down more than 33%. As I’m writing this, the S&P 500 is up 18.6% YTD with the Nasdaq up an incredible 35% YTD. A lot can happen in less than a year, but I’m doing what I’m always doing. Investing as often as I can, taking the bargains I can identify that meet my criteria. I’ve always held dear the famous words of Peter Lynch suggesting that time in the market, beats timing the market. After all, it’s a market of stocks, and there is often something around worth looking into.

I do however don’t agree with the current performance of the market so far this year. The AI hype, where individual stocks can increase their market cap by double digit billions worth of dollars in any given day for an untested marketplace. No thank you, that’s not something I’m willing to bet the farm on. That’s also why I’m severely lagging the markets performance, but I’m okay with that. As another famous investor once said. Rule number one is to never lose money, and rule number two is to never forget rule number one. If you aren’t familiar with what I just paraphrased, then those words belong to Mr. Buffett, and it’s something I hold dear. I came from a low-class upbringing, and it’s instilled in me a need to safeguard my funds, even if it means compounding it at a bit slower rate. It’s who I am, and it’s what I need to sleep well at night. As investors, we need to know our strategy and risk profile, that’s what those reflections address in terms of how I approach the market.

I’m not sufficiently willing to take on risks for someone my age, and I recognize that, which is why I’m also invested in several broad market ETFs to make up for it. With that approach, I’m capturing the Nvidia’s ( NVDA ) and Tesla’s ( TSLA ) of the world. Stocks that I never managed to invest in directly, as I couldn’t justify the valuation when I looked into the cases.

{kind=link}

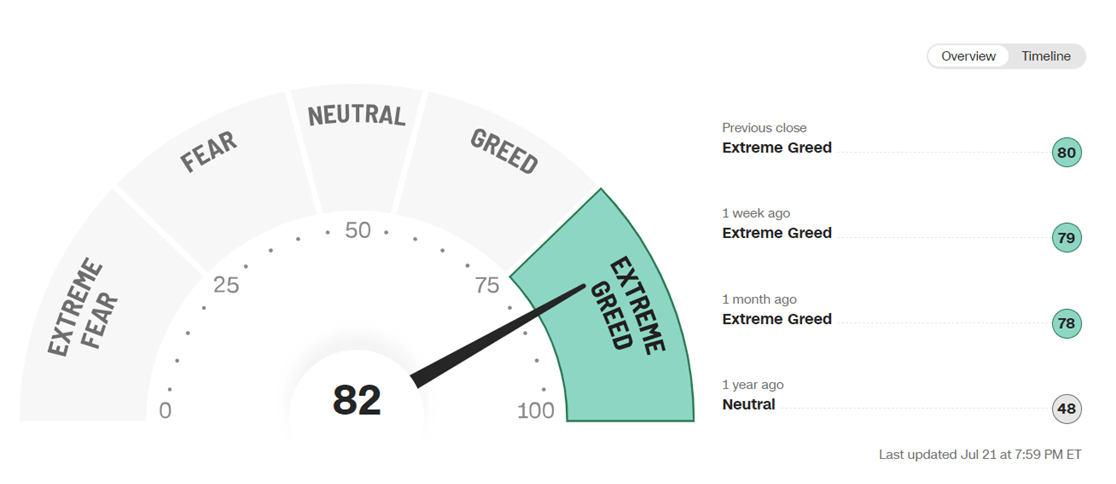

The CNBC fear & greed index is in no way a defining parameter for how I allocate my funds, but I do glance at it from time to time to gauge how investors are considering the temperature of the market. I thought we’d be in a recession by now, but the labor market and economy in general, has proven more robust and resilient than I ever imagined – which is a good thing. Again, that’s why I don’t try to time the market, even though I of course sometimes withhold just a little bit of cash reserves as I see fit.

All I know, is that I’m in this market with a time horizon measured in decades, and that I try to build positions in companies with a substantial moat, healthy market outlook and valuation upside. There are of course positions in my portfolio that don’t immediately scream those exact words, but I’m also willing to invest in cases with mean reversion potential and high yielders.

My Market Activity

As I just mentioned, I haven’t shared an update for my portfolio since October last year. I’ve gotten a new job, welcomed a new family member and lots of other things that’s taken my time and energy. However, I’ve of course invested the funds I could spare in between the chase for baby gear and a larger and family friendly vehicle. Essentially, I had to save cash for redecorating the house and as it often turns out, it costs more than you initially expect.

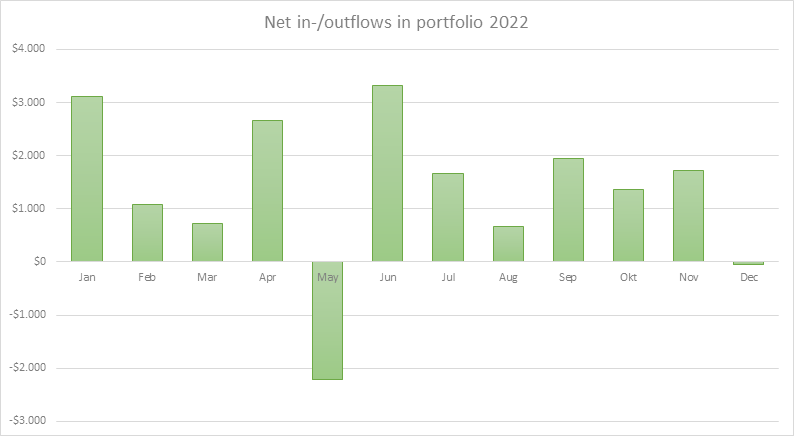

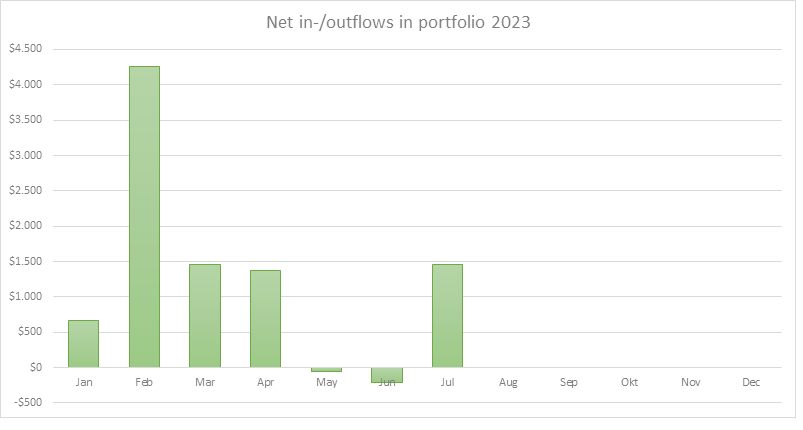

Portfolio flow of funds (Authors Own Creation)

{kind=link}

The graph above exhibits my investment allocation throughout 2022, where I invested an average of roughly $1350 in any given month. This year, as can be see below, I’ve managed much less, especially if you exclude February where I benefitted from a one-off inflow of $4000.

The reason why I have negative outflows, is that I often tax harvest during December, and in May and June this year, I’ve offloaded a few positions where I concluded the valuation exceeded what was reasonable. I immediately put those funds to use, which is why there is a balance close to zero for those two months.

When it comes to the positions I offloaded, Apple ( AAPL ) is an example where I sold half my stake. I’m still up more than 300% for my remaining position, but I concluded there was a limit to how much further the stock could go with respect to the valuation slapped onto the stock. I was also disappointed with the most recent dividend hike out of Apple, which turned out to be a meager 4.3%. I’ve done this once before, so now I only hold one quarter of my original stake. I’ve been fortunate enough to sell at what’s been the previous highs, but looking back in a couple of years, there’s a fair chance that I look like a fool, should the valuation continue to expand due to e.g., new market opportunities for the company that drives additional revenue and earnings.

Another stock I let go was Bayer ( BAYZF ), a conglomerate covering both pharmaceuticals and crop science. A stock I’ve held onto stubbornly for eight years, where the mean reversion never happened, not even when the broader German DAXX index soared. Even including the dividends received during that period, I was left with a 10% loss since 2015. Not my best investment decision.

Portfolio flow of funds (Authors Own Creation)

{kind=link}

On the buyer side, I’ve made numerous moves since October.

- I’ve established a position in Taiwan Semiconductor ( TSM ) with an average price per share of $61.3 meaning I’m up 59%. I published an article at the given time, where I laid out my opinion and why I concluded it was a worthy decision despite the geopolitical risks associated to doing so. I’ve held Broadcom ( AVGO ) and Texas Instruments ( TXN ) for years but wanted to increase my exposure to the industry, and Taiwan Semiconductor is hard to get around given the role it plays within the industry as the leading provider of high-end chips. I finally managed to do so, as I’ve previously never pounced when an opportunity presented itself.

- I’ve established a position in Lam Research Corporation ( LRCX ) with an average price per share of $403.9 meaning I’m up 54%. If you consider the semiconductor industry, then there are companies who design the chips, such as Broadcom, and those that manufacture them such as Taiwan Semiconductor. However, there are also companies who offer equipment and software to the industry operators, such as the well-known ASML (ASML), and in this instance, Lam Research. I looked into a wider array of companies catering to this segment, and Lam Research came at almost half the valuation compared to ASML, making it a very attractive option seen from my vantage point, given that it operates with very attractive unit economics and returns on invested capital, just as ASML. Now, ASML of course demands a particular premium due to its very impressive market position, but Lam Research also operates within a small and exclusive niche of companies and therefore caries a healthy moat.

- I’ve established a position in Union Pacific Corporation ( UNP ) with an average price per share of $194.4 meaning I’m up 12%. Preferably I’d like to add below $180 per share, but I decided to go against that once the stock finally dipped as I accepted to pay a small premium compared to what I considered fair at the time. I believe the company will justify that over time given its impressive moat and business performance throughout time. I’ve wanted exposure to railroads for years but kept missing out. The reason I wanted this exposure is quite simple. The moat is very strong, and the business model is as efficient as it comes when dealing with land-based transport. Once a set of railway tracks have been installed, you don’t establish another set next to them. This creates a sort of monopoly for those operating the rails, and especially in the instance where licenses and tracks have been establishes many years ago and since depreciated. Think for a second, what it would cost to replace UNP today. That’s a form of hidden asset and equity seen from my perspective. Similarly, there is no land transport as efficient as rails when moving heavy goods over long distances, and there is most likely little chance for that to change. I’m pretty sure I’ll broaden my exposure to an additional railroad company somewhere down the line, as to ensure I’m betting on more than one horse.

- I’ve established positions in a couple of REITs also. I’ve held REITs in my retirement account for many years, but never in my brokerage account. Given the pullback we’ve witnessed both during 2022 and now in 2023, I felt the opportunity was ripe to move in. I’m a dividend growth investor, but I’m also seeking exposure to more income related companies. I understand inflation is high, pressuring interest rates and that receiving a dividend of 4% doesn’t compensate, but I don’t believe inflation will stay high for years. With that in mind, I’m happy to lock in those 4%+ yields and absorb the risk associated to real estate, as long as I don’t go overweight within my portfolio. I decided to go with a risky bet, so I established a position in Medical Properties Trust ( MPW ) with an average price of $9.8 per share, meaning I’m up 5% as we speak. I’ve already received two mammoth dividends from the company due to my 11.2% yield on cost, but with the risk associated to it as of today, I’m accepting volatility and the fact that the stock could be back in red tomorrow. There’s also the chance the dividend will be cut, at least that appears to be what the market expects. I paired this with a somewhat safer bet, NNN REIT ( NNN ). It’s a well-diversified company when looking at its revenue distribution inside the US, as well as its sector exposure, making it a solid move as I see it. My average price was $42.4 per share, so I’m currently up 4%.

- Most recently, I’ve also increased my healthcare exposure as I reduced one of my holdings during 2022 and earlier in 2023. So, I’ve added Pfizer ( PFE ) and The Cigna Group ( CI ). Two very different plays, one paying a dividend based on a somewhat high payout ratio, while the other offers more growth opportunity. I’ve added them recently, so my Pfizer position is currently down 2% while my Cigna position is up 10%. I used to only hold three positions with healthcare or pharma exposure, being concentrated within one company in particular. I’m very pleased that I’ve broadened my exposure.

Those were my new positions inside the portfolio, but I also added to existing positions, such as T. Rowe Price Group ( TROW ) which is currently up 1%. I established this position during the summer last year and have been dollar cost averaging my way into it, until the point where it reached a full position for my portfolio. Similarly, I’ve expanded my position in Stanley Black & Decker ( SWK ). This was underwater for most of the past year, but recently creeped into positive territory, being up 13% at this point. SWK is a pure mean reversion play, but unfortunately, I went in too early. Long-term, I believe the stock should be worth $120-130 per share, so I’m holding on while the management team tries to better the situation. It was really a situation of poor decision making on their part that brought the company into the muck, but it’s also a company in possession of many strong and world-renowned brands, and I don’t see why this company, who has been around for 150 years, shouldn’t be here tomorrow. Another favorite of mine, Tyson Foods ( TSN ) has also received a hammering during 2023 as profitability has collapsed, allowing me to expand my position, meaning my average price per share is $65.4 which puts me into red by 19%. Lastly, I’ve also secured a full position in the controversial AT&T ( T ) stock, currently 26% underwater.

Other minor moves including adding to my ETFs as well as adding a couple of shares in Microsoft (MSFT) and Alphabet (GOOGL) (GOOG).

Portfolio Strategy

I’m currently at forty positions in total, including four broad ETFs covering either specific geographies or themes.

I’m a strong believer in diversification, and it’s fair to point out that holding so many positions in a portfolio easily covers that principle. However, at the same time, I only used to have three companies within health care and two within industrials. Having added Pfizer and Cigna, I now hold five healthcare related companies and within industrials I’ve added Cummins ( CMI ), SWK and Union Pacific within the last year, resulting in a total of five different industrial companies. It’s my opinion that was a requirement to broaden my exposure, and I don’t believe I’m done adding new companies to either of those sectors. As you can guess from what I’m writing here, I also prefer diversification within my individual sectors.

Naturally, it’s difficult to track all those companies every quarter, but I’m also of the opinion that one doesn’t need to track all their positions on a quarterly basis. If you are investing and not speculating, then you would consider yourself as an owner of the business and owners don’t monitor their assets to determine if they should sell every quarter, do they?

I for one don’t believe so at least, and therefore I disagree with the notion that a portfolio can’t consist of a multitude of holdings. Even if that means carrying more holdings than one can monitor every quarter.

Sector Allocation (Authors Own Creation)

So where do I go from here?

I’d like to add another REIT before the current window of opportunity closes as well as expand my existing positions. At the same time, I don’t believe that window is about to close before end of the year, so I’m staying patient.

I’ve loaded up substantially within the industrial sector, but two of those holdings, Lockheed Martin ( LMT ) and General Dynamics ( GD ) are pseudo industrials as they cater to very specific defense niches as opposed to broader industrial segments. Therefore, I’d also like to add one additional company here. I’ve wanted to add Deere ( DE ) or Caterpillar ( CAT ) for years, and perhaps this time I might succeed in doing so.

One of my holdings have also fallen out of bed recently, UGI (UGI), so I’m considering the opportunity of adding to my position to lock in the 5.5% dividend. It doesn’t remain a priority for now however, as I have limited funds at my disposal due to the changing priorities and needs in my private life.

Investing Principles

Having managed to build a portfolio of forty holdings with changing perspectives related to sector distribution, is a consequence of many learnings along the way. I’ve made numerous errors, while these errors having shaped and sharpened my attitude towards how I invest.

First of all, I settled on a dividend growth portfolio a long time ago. I’ve discussed this numerous times within these articles, but it originates from one thing in particular.

Paying a dividend requires real cash flows, not accounting numbers. We often observe payout ratios, who are devised based upon EPS numbers. However, those numbers stem from accounting principles and are to some extent arbitrary. Therefore, I always consider the payout ratio compared to the cash flow. Point being, that recurrent dividends are a source of discipline for corporate leadership. You can’t squander cash on empire building to the same extent and it’s my belief that it also aligns leadership with their shareholders. After all, the leadership team is there to service the shareholders – we don’t invest in businesses for the fun of it. We do so to make a healthy return and I’m of the opinion that a management team that is committed to its dividend, is on the same page as its shareholders. There are of course exceptions to any principle, and I’ve deviated from the principles below for some of my holdings.

I try to invest according to the following principles:

- Companies who hold a competitive advantage that justifies strong margins relative to its peers (sector leaders).

- Companies who deliver strong returns on invested capital ('ROIC'). This metric helps one understand leadership’s ability to allocate capital efficiently leading to profitability.

- Companies who have a proven track record in terms of performance compared to the broader index.

- Strong leadership teams (e.g. Glassdoor ratings, prior returns of the stock, competencies amongst the board of directors).

- Companies, products and services I understand, limiting the likelihood of loss of capital. This means, that I for instance avoid cryptocurrencies as a form of investment. Similarly, I for instance avoid investing directly in companies where governance is unclear such as Alibaba (BABA). Instead, I take the path of investing via ETFs to spread my exposure but at the same time obtain exposure.

Take three of my holdings as an example.

Visa, Taiwan Semiconductor and Lam Research all deliver strong returns on the invested capital, hold incredible market positions within their areas of operations, which drive strong margins, and have a leadership team that is recognized amongst the employees in general. You may ask why I’m then invested in for instance AT&T, who have a leadership team that, in my opinion, should have been shown the door a while ago. I do so, as it’s attractive from a valuation and mean reversal perspective. I take these chances, something I think an investor can do, as long as the exposure as a percentage of the portfolio remains within a reasonable threshold.

These are the principles I follow, and what I adhere by when I design my list of potential investment candidates such as Caterpillar and Deere, whom I mentioned earlier. They are manufacturing companies and therefore have higher costs of goods sold, but still deliver strong operating margins and possess the leading brands within their niches.

The Portfolio

Part of the joy associated to tracking one’s portfolio closely, is to watch the compounding do its wonders. Albeit slowly, the changes become very apparent even when considering a short time span of just a couple of years. After all, I do this to one day be able to set myself free. Here I’m talking about the ability to retire at my own time, and not according to the government mandated 70 years of age. At that point in time, I hope I’ll be spending a significant portion of my time trekking the wonderful natural parks of Utah.

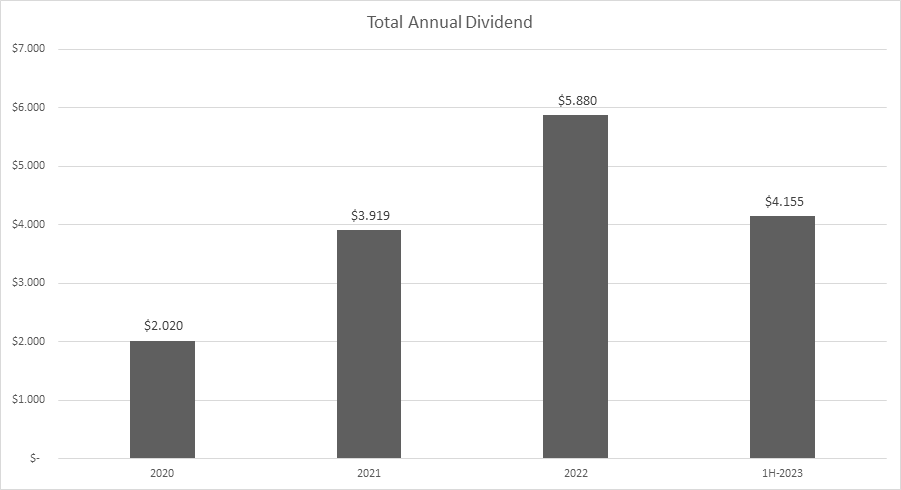

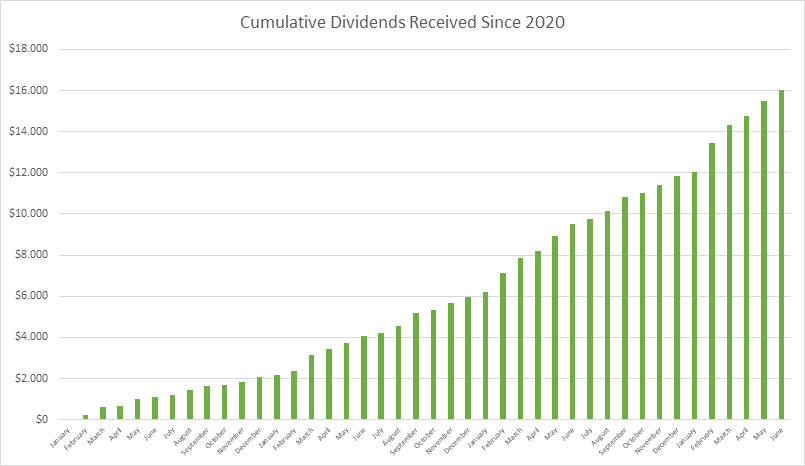

Anyway! Take for instance the total amount of dividends received in a given year and how that has developed. I’ve received $4155 during the first half of this year, which is twice as much as what I received for the entire 2020 and also more than what I received in 2021. Watching that development is incredibly motivating!

Total Annual Dividend (Authors Own Creation)

{kind=link}

The total amount received in the form of dividends also continues growing.

Cumulative Dividends Received (Authors Own Creation)

{kind=link}

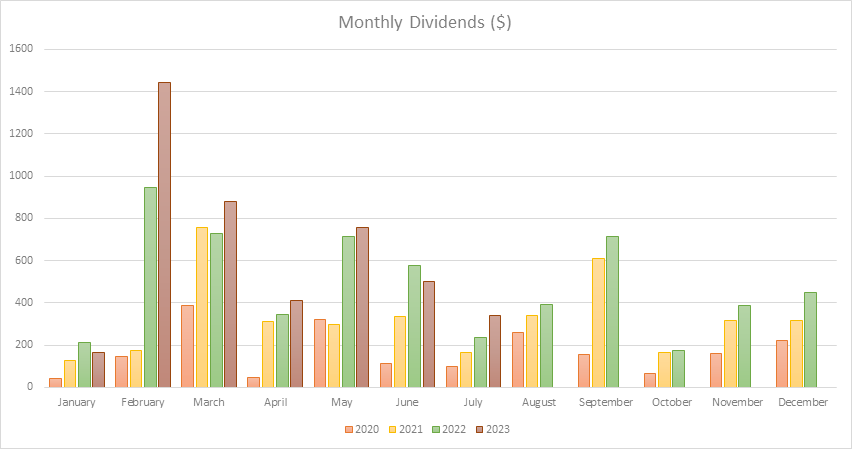

If you look closely, you’ll see that the cumulative graph jumps every February. That’s because I’ve been building my ETF positions, which pay an annual dividend at that time of year. That’s also giving a false impression when looking at my 1H-2023, as it would be a fallacy to simply extrapolate under the expectation that I’d then receive around $8000+ for the full year. That’s not the case, and you can see why in the graph below, where I’ve mapped the monthly dividends.

Monthly Dividends (Authors Own Creation)

{kind=link}

Here the February bump becomes very apparent. Interestingly, the primary dividend paying ETF only paid half of what it did in 2022, but my position has grown substantially since, therefore still pushing it way ahead of last year's result. As you could see in my portfolio weight table, I’m planning on reaching a point where those ETFs make up 15% of my portfolio, and as they only make up 8% today, I expect to continue adding capital. It’s not a priority right now, as I have positions, I want to expand, but as we get closer to end of the year, I expect to prioritize adding to the ETFs once more.

Looking at the monthly dividend distribution, and you can see how it’s mostly ticking upwards across the years, but also that some months suddenly spike. That’s because some of my holdings have been paying extraordinary dividends, such as LyondellBasell ( LYB ) did last year or this year where Mercedes ( MBGAF ) reinstated their dividend, which was slashed during the Covid-19 years.

At the end of the day, this is one of my favorite visualizations of all the hard work and increasing value I get out of it. On a forward basis, I expect my portfolio to pay out somewhere between $7000-$8000 in dividends before tax, and I can’t wait for that number to double. Already today, that amount can fuel a substantial part of my private economy.

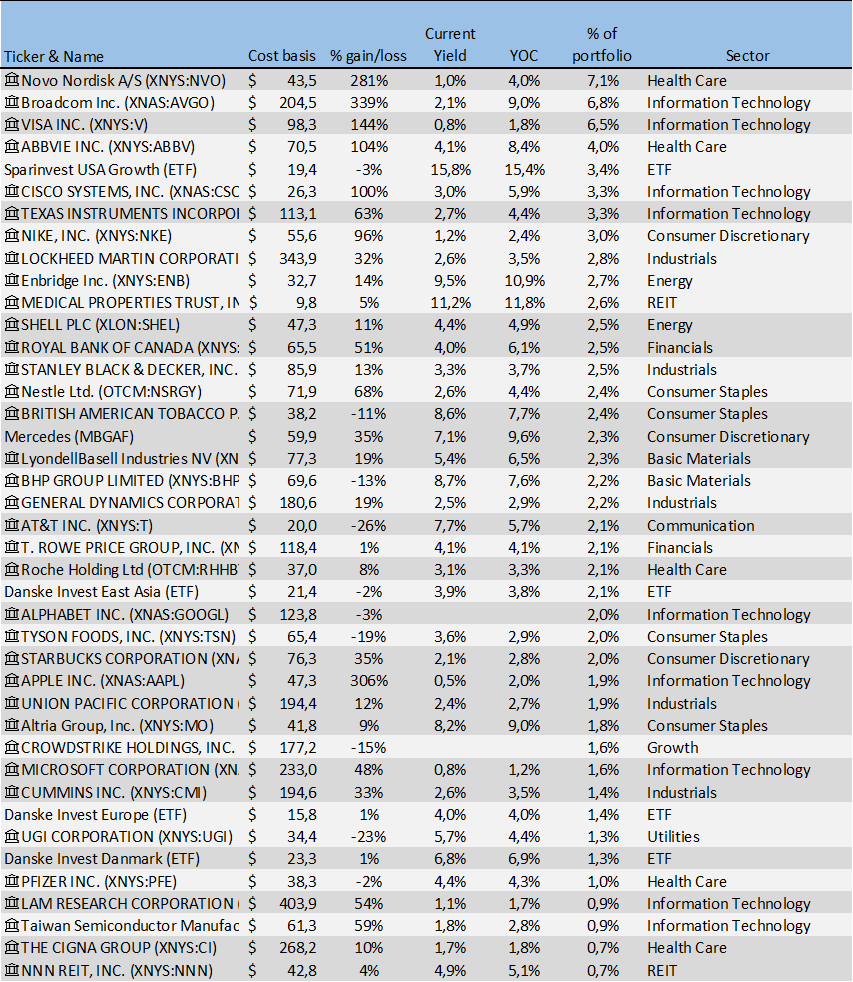

Let’s get to it… here follow’s the whole portfolio, ranked according to portfolio weight. You can ask why I choose to include the yield on cost. The answer is simple. I do so, as it motivates me to witness how a growing dividend, results in me as an investor receiving a growing amount of my principal on an annual basis. You’d never be able to pick up Broadcom at a 9% yield, but I locked in my position many years ago, and therefore I’m reaching a very strong YOC in any given year. Same for Visa ( V ) or Nike (NKE), it was never going to be its initial yield that would drive the decision to invest, but hold on long enough, and that growing dividend starts turning into something real. I’m hoping for another 10% dividend increase later this year, so that my YOC will creep closer to 2%.

My Dividend Portfolio (Authors Own Creation)

{kind=link}

One year ago, my portfolio stood at $160,000 and today it comes in at $197,000. I was close to breaking the two-hundred-mark last spring, so I’ve been down a lot, but I’m hoping it will come sometime during this year. Time will tell.

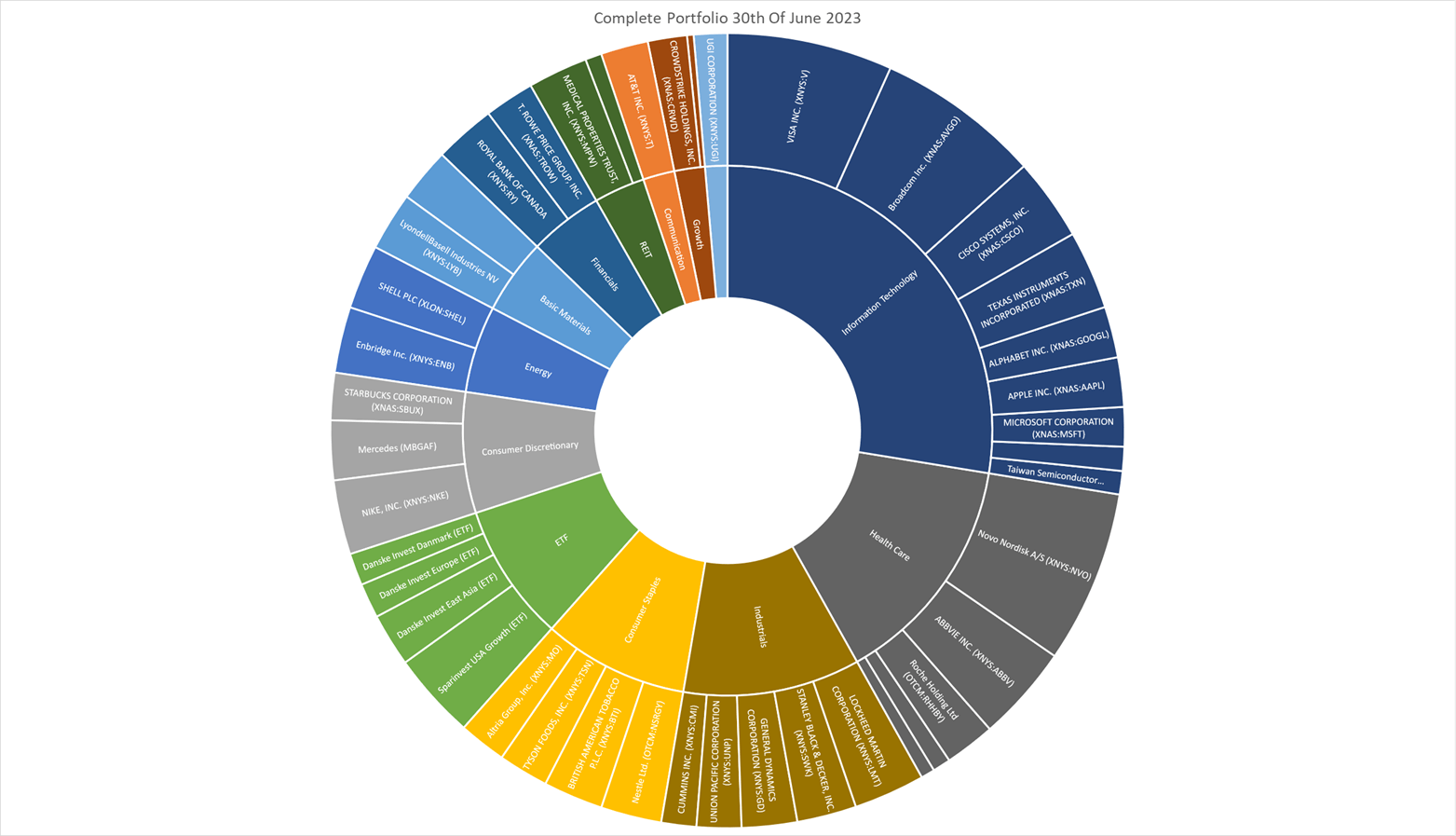

The last illustration I want to include, is also a favorite of mine, the pie chart distribution of my portfolio.

Complete Portfolio Pie Chart (Authors Own Creation)

{kind=link}

This illustration gives a nice and clean overview of how my holdings are distributed and what makes up the portfolio.

Wrapping Up

Time flies but the portfolio never stops developing. For each month going by, it’s another step closer to making myself somewhat financially free. My portfolio is closing in on reaching the next big round numbers, and for every round number, the portfolio and myself stand on top of new learnings and lessons that improves my ability to navigate the markets and stay true to my risk profile.

I’ve shared my perspectives associated to what makes a given company an interesting investment opportunity for me, and as such, also some of the companies I have in mind as relevant opportunities. I’d be very curious to hear your investment principles for when you have to conclude as to whether a given company is of interest?

I'd like to thank you for reading this piece concentrated on updating my portfolio overview. I believe in transparency and sharing what I'm doing myself.

If there is anything else you would like for me to add to these updates or discard, please say so in the comments section and I'll consider adding or removing it for future posts.

For further details see:

My International Portfolio: Approaching Another Major Milestone And Looking Into Recent Additions