BKR - Nabors Industries: Setting Up For Another Buying Opportunity

2023-11-11 03:25:54 ET

Summary

- Nabors made a round-trip from the $80s to almost $140 and back below $90.

- This is all sentiment-driven; despite headwinds for U.S. oilfield services, Nabors is an international player and a premium provider in the U.S.

- Q3 wasn't really that bad.

- Once the shock from $70s oil dissipates, Nabors should move back up again; even a $150-$200 stock price won't imply overvaluation based on 2024 EBITDA.

Investment thesis

Nabors Industries ( NBR ), a major provider of land drilling services in the U.S. and internationally, hasn't had good YTD performance. Much of that hasn't been due to the company's particular results but rather because of "macro" concerns.

I wrote about this before , when I recommended Nabors as a buy at $86 at the end of May:

Nabors started ascending shortly after and almost got to $140, before reversing direction and is now at $88, pretty much back in the same buy zone. It's of course not possible to time exactly the bottoms and tops, so I ended up acquiring NBR at an average cost of $87 and selling at average price of $116, which still made for a 33% gain.

When Nabors got below $90, I started accumulating shares again on essentially the same thesis I laid out in my prior article:

- U.S. headline rig counts are trending down, but internationally rigs aren't falling; Nabors is a global player.

- Even within the U.S., the industry dynamics drive a preference for higher-end equipment where Nabors has an edge.

- Q3 wasn't that bad so the reverse trip from $140 to $88 has again more do with macro perceptions than Nabors specifics. Oil ( CL1:COM ) went up a lot on the Middle East geopolitical premium and then overshot in the opposite direction, now that it looks we won't see further escalation.

Based on current analyst expectations about 2024 EBITDA, we are now at a 4x enterprise value to EBITDA multiple which isn't expensive. The professional analyst targets (summarized by Seeking Alpha) also imply decent upside:

{kind=link}

I think we are quite likely to bounce off the current lows over the next 3-6 months as the "over-correction" reverses. I don't see NBR as a long-term buy and hold until the macro picture stabilizes. For that we need peak long-term yields, the Fed officially moving from tightening into easing, and perhaps even getting past the 2024 elections that may otherwise invite more oil market interventions. However, if you don't mind a shorter trading horizon and are actively monitoring your positions, Nabors may be a bet worth considering.

What is going on with rig counts?

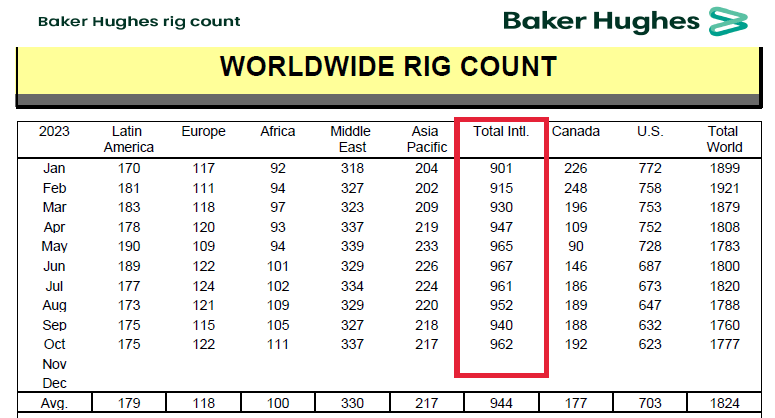

Everyone knows that U.S. rig counts are dropping and that metric is the one most often quoted in the media:

However, international rig counts aren't falling:

{kind=link}

Canadian activity is also good, keeping in mind the stronger seasonality:

This "two-speed" view of the world is also confirmed by the earnings calls of oilfield service majors SLB ( SLB ), Halliburton ( HAL ) and Baker Hughes ( BKR ). All Big 3 have highlighted continued strength in offshore and international markets in parallel to near-term weakness in the U.S.

Why that is the case is a longer story and I have laid out my thoughts in a few of my macro-oriented articles:

Oilfield Services Update: Offshore And International Make Up For North America Weakness

3 Things To Consider Before Buying Oil Stocks

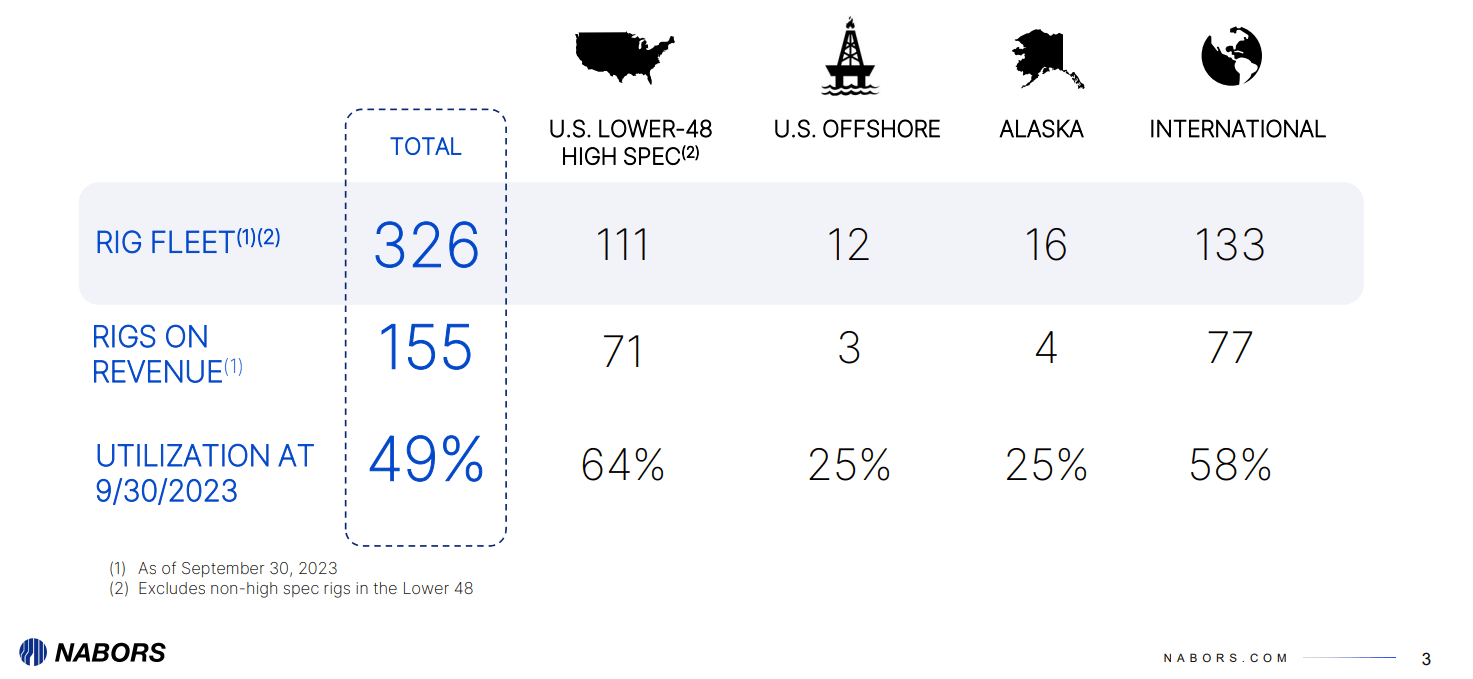

For Nabors' purposes, though, this is simply a fact we need to deal with. The good news (from NBR perspective) is that Nabors isn't a domestic driller; almost half of its exposure is international (working rigs):

{kind=link}

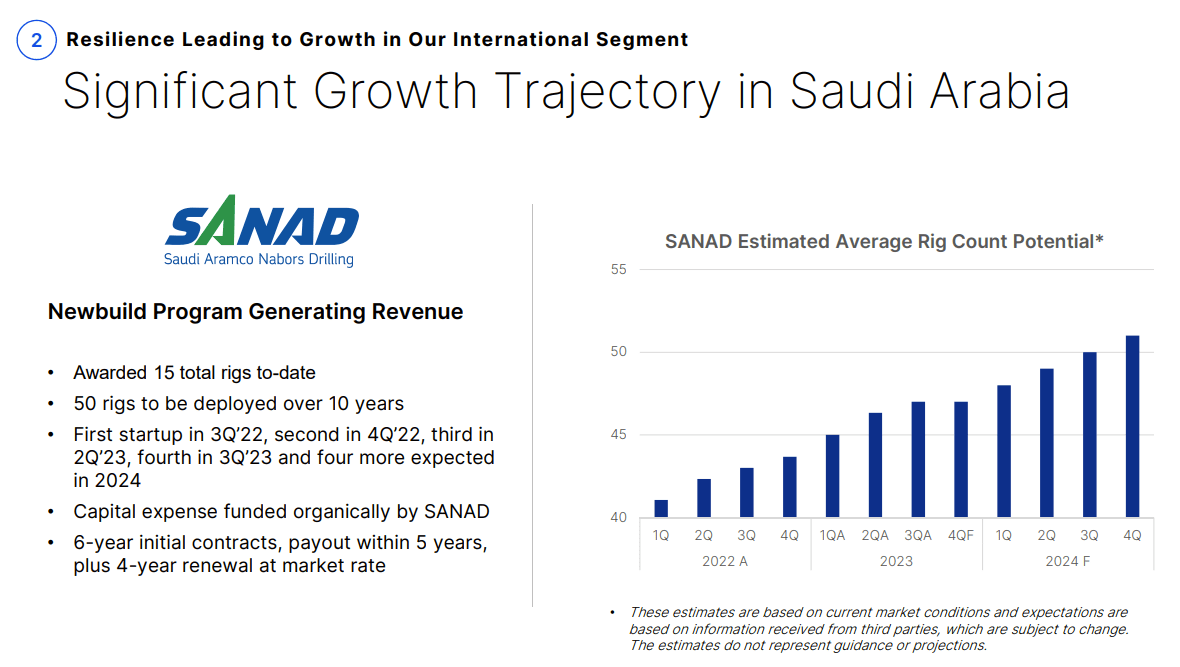

In fact, Nabors is anticipating significant growth from Saudi Arabia, where it has a joint venture with Saudi Aramco; this may add 50 rigs over the next 10 years (compared to 77 working international rigs right now):

{kind=link}

This matters because international activity targets lower cost, lower decline production and is more robust. Compared to U.S. shale, these developmental efforts are longer cycle in nature and will continue even with lower oil prices. Shale is the high marginal cost producer prone to stop-and-go cycles.

So are North American onshore services done?

That's what the market seems to think if you have followed these stocks during 2023. Valuation multiples are still quite low, especially among completion companies that provide pressure pumping services:

{kind=link}

Among this group, I previously made (correct) bullish calls on ProPetro ( PUMP ) and Liberty Energy ( LBRT ), but I am currently more bullish on the Canadian players Calfrac ( CFWFF ) and STEP Energy Services ( STEP:CA ).

Nabor's drilling peer group is a bit less discounted, but still looks like a bargain unless you think drilling will completely collapse:

{kind=link}

Besides Nabors, I also like Precision Drilling ( PD:CA ) and Ensign Energy Services ( ESI:CA ) for their Canadian exposure. Both Canadian drilling and completions companies are emphasizing the positive impact from LNG Canada, the Coastal GasLink and TMX.

For example, STEP Energy says :

STEP will use the moderating of activity in Q4 2023 to complete more intensive maintenance on equipment to prepare it for the extremely intensive utilization anticipated for Q1 2024 ... Activity in 2024 is expected to increase, with multiple clients signaling that their 2024 capital budgets will be higher than 2023 . The discipline in global oil markets and anticipated completion of the Trans Mountain pipeline project and the Coastal Gas Link pipeline/LNG Canada projects are creating an opportunity for Canada to materially increase production in 2024.

What about U.S. shale though? One puzzle right now is that rig counts are falling, but U.S. production is holding up and may have even broken records although HFI Research warns that U.S. production may be overstated due to flaws in the EIA methodology.

Part of the answer may be shale companies drilling longer lateral wells. If you own any shale stocks and follow their calls, you have heard multiple times management talking about how longer their wells keep getting. This brings some efficiency from the operator's perspective as you can get more production out of the same drilling rig:

{kind=link}

Seemingly, this is bad news for Nabors, but that's not the full story as the trend also drives the need for higher specification equipment where NBR has the edge. As explained by management during the earnings call this may help Nabors gain market share from competitors:

You've actually seen some of the big guys talk about that increasing lateral length as much as five miles and that kind of stuff benefits Nabors, because we've pre-invested in that move.

We built the M 1000 rig, which was the successors to the X-ray a couple years ago, has a million-pound hook load that's perfectly designed for these longer lateral lengths. We also introduced to the market a new top drive that has the pious torque available that can actually handle a five-mile lateral. So, the company's positioned itself to capture that moment.

Add to that Harold Hamm's recent comments on shale going after "Generation 3" rock, and it gets clear it's too early to write off onshore services. Rather, what I find more likely is that the increasing technological challenges for shale production will result in the bifurcation of suppliers into high- and low-spec, and those with premium equipment, whether it is drilling or fracking, will be more sought after. So even if the U.S. onshore services ( OIH ) pie shrinks permanently, it doesn't mean Nabors' business will do so too.

Highlights from the Q3 earnings

Revenue and EBITDA in Q3 were down a bit sequentially , but still up year-on-year:

{kind=link}

I don't think this was a bad quarter even if free cash flow only broke even. Management explained:

Free cash flow for the third quarter at just under breakeven fell below our target, mainly due to higher capital expenditures of $33 million, which reflected the accelerated timing of investments in Saudi Arabia and the US..

These sound like timing issues that will reverse in 2024. I didn't see anything particularly negative from Nabors' side, and this confirms my view that the selloff was probably more related to the macro story around oil prices.

Valuation and targets

Right now, most of the professional analysts covering the stock are forecasting close to $1 billion in 2024 EBITDA:

| Analyst |

| 2024 EBITDA |

| Evercore |

| $934 m |

| Benchmark |

| $918 m |

| ATB Capital Markets |

| $931 m |

| Tudor Pickering |

| $952 m |

Source: Refinitiv

Even a 4 to 5x enterprise value to EBITDA ratio can easily take you to a $150-$200 share price given the high leverage.

Risks to consider

NBR isn't a much followed ticker here, so if you're reading this article you're probably already aware of the general risk that oil prices pose for stocks in this sector. So no need to harp on that.

More specific to Nabors, the debt is high, but I am not seeing signs of particular distress yet. The largest outstanding maturities are in 2027 and the spread on those is about 430 bps; it is up from 300 bps in September but I am not concerned so far.

The short interest peaked recently but is still high:

The saying is that short sellers are the smart money, but, according to this article, the most shorted stock in the S&P 500 last month was Exxon ( XOM ), so I am not sure about that any longer either.

Bottom line

Oil prices may be down from the $90 to the $70s, but Nabors' business isn't over. First, the company is half international and the capex cycle there is moving ahead at full speed. Second, even within the maturing U.S shale world, the ongoing trends may end up making Nabors a winner due to its technological edge.

I think the fact that the stock is revisiting its May lows has more to do with macro sentiment and presents another buying opportunity. I wouldn't call it a long-term buy and hold because the seesaw action will likely continue until we achieve more durable macro stability, but I am betting that the next big move is higher.

For further details see:

Nabors Industries: Setting Up For Another Buying Opportunity