DM - Nano Dimension: Interesting Asymmetric Risk/Reward Scenario

2023-06-12 16:17:14 ET

Summary

- Interesting developments are underway at Nano Dimension, with potential about to be unlocked if the events outlined occur.

- We believe there are certain aspects that the markets are not pricing in correctly at the moment, from operational efficiencies to a huge change in interest income.

- The company remains a very interesting asymmetric risk/reward profile, with the downside protected by tangible book value and share repurchases.

Investment Thesis

Nano Dimension ( NNDM ) has had an eventful few months, with a bid for Stratasys, dealing with activist investors and some interesting developments in their fundamentals.

We believe that in the case of Nano Dimension, both the market and investors are likely overlooking certain events and changes in the macroeconomic landscape that are poised to unlock further value for shareholders. As we see it, Nano Dimension's downside is to some extent hugely protected by its tangible book value and management's buyback program. Moreover, we don't think investors are taking into account cost savings in 2023 and interest income, which could move the company closer to cash flow profitability.

We will highlight all these developments, which are arguably not appropriately factored in, and outline what both the downside and upside scenarios look like for the company.

A Special Situation

For a quick refresher on what Nano Dimension does and the very curious situation they currently find themselves in, let's quickly summarize. Nano Dimension is in the 3D printing, or additive manufacturing ((AM)) industry and specializes in 3D printing electronics.

More specifically, the company began as an innovative company with the idea of 3D printing circuit boards, better known as the green circuit boards in computers and virtually all other electronic devices. Recently, however, they started expanding into the general 3D printing industry, following the acquisition of NanoFabrica and Admatec/Formatec. In 2020 and 2021, however, the company gained a lot of appeal from private investors when it became part of the SPAC/ Meme stock era, and was able to go from having a few million on its balance sheet to about $1.5BN through direct offerings.

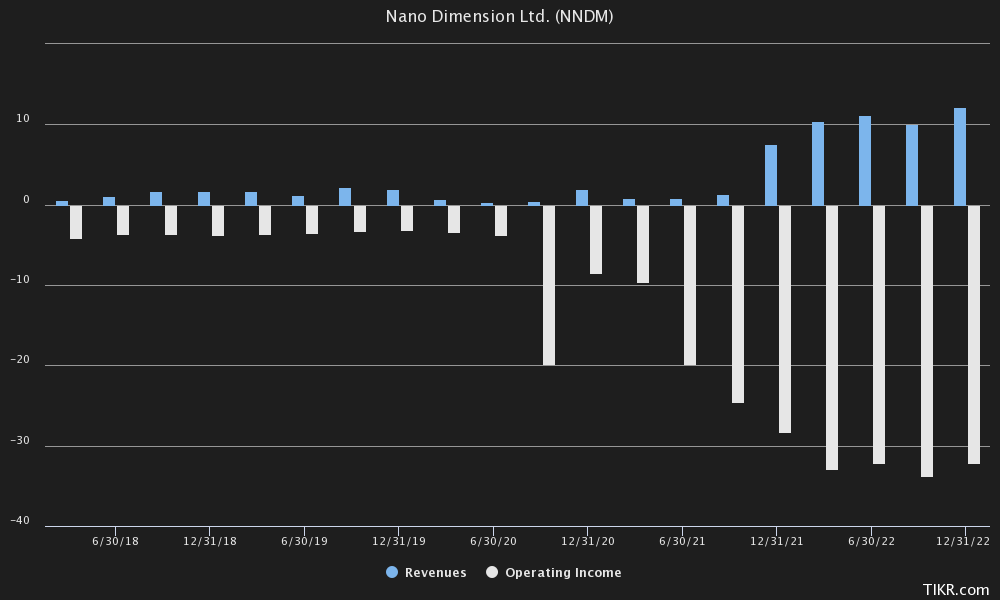

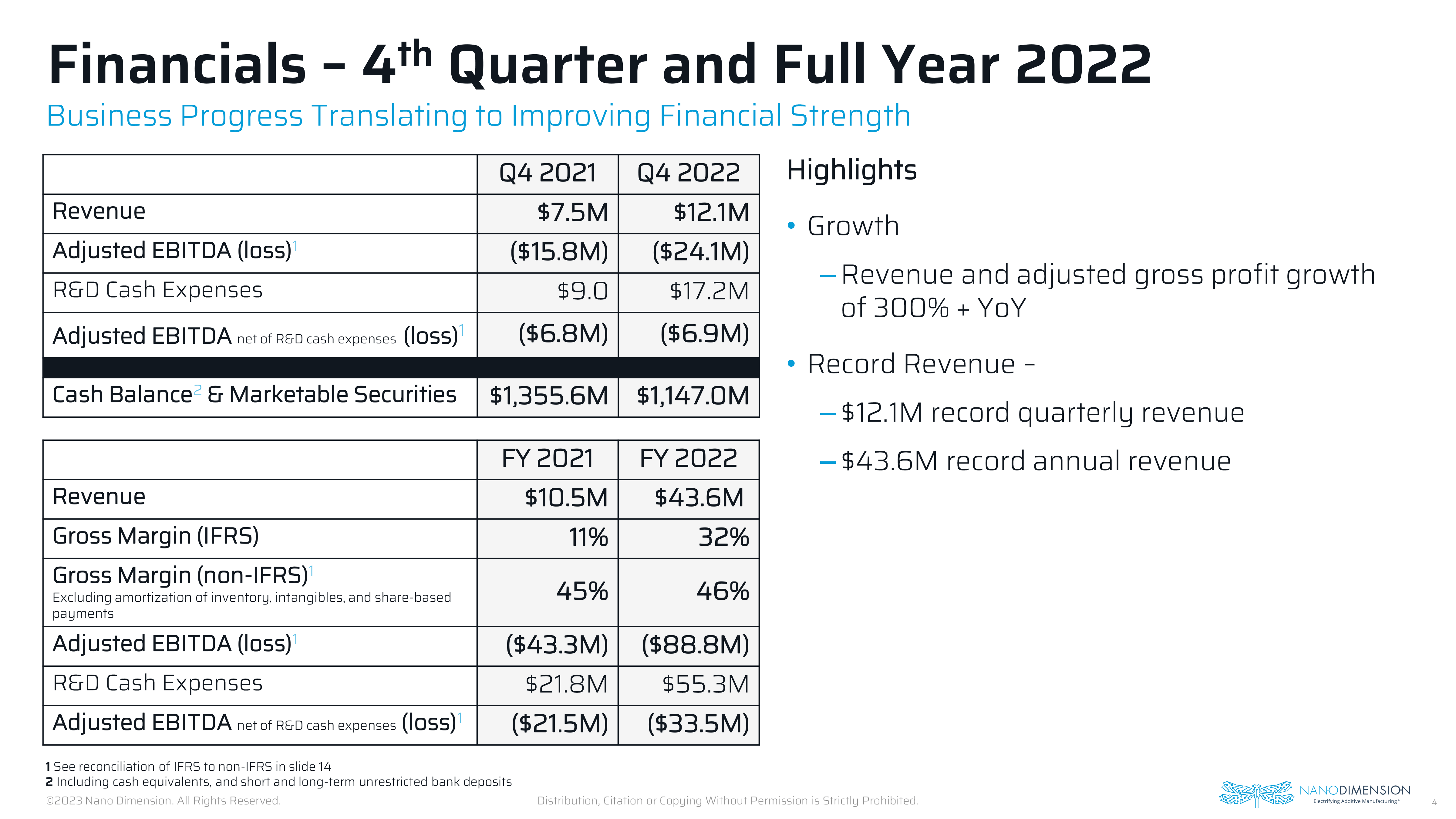

Fast-forward to today and Nano Dimension has grown to $43.63 million in revenues as of fiscal year 2022 , with preliminary first-quarter revenue of $14.6 million or $58.4 million annualized. However, operating income came in at -$131M for fiscal year 2022.

{kind=link}

TIKR Terminal

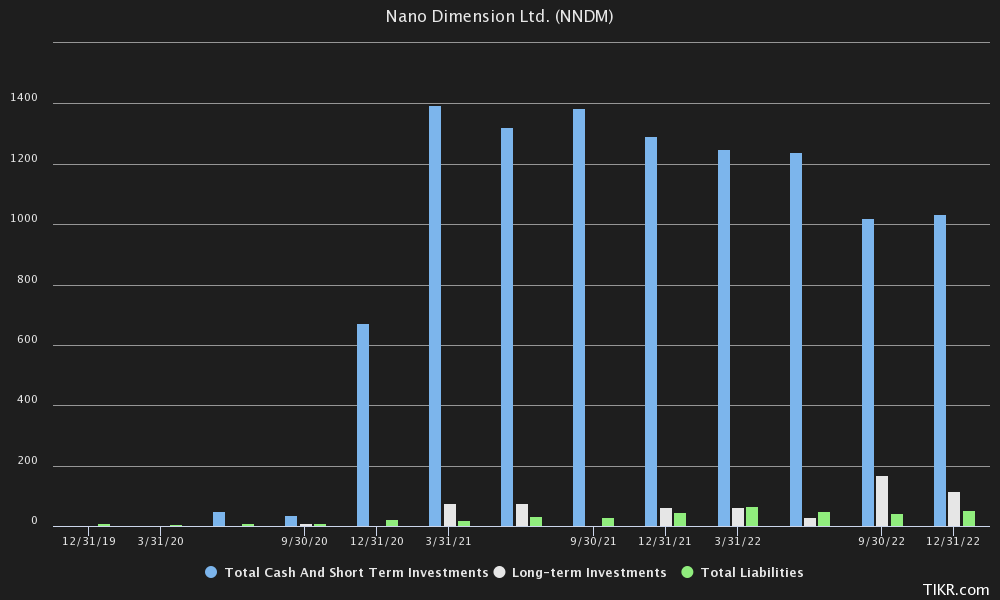

Looking at the balance sheet and going back to the approximately $1.5BN raised through direct offerings, Nano Dimension still has $1.03BN in cash and cash equivalents, along with a 14.1% stake in the other popular Additive Manufacturing company Stratasys ( SSYS ). This interest is worth another $172.48M at the current Stratasys share price, meaning that Nano Dimension has about $1.20BN of liquidity on its balance sheet as of the fourth quarter.

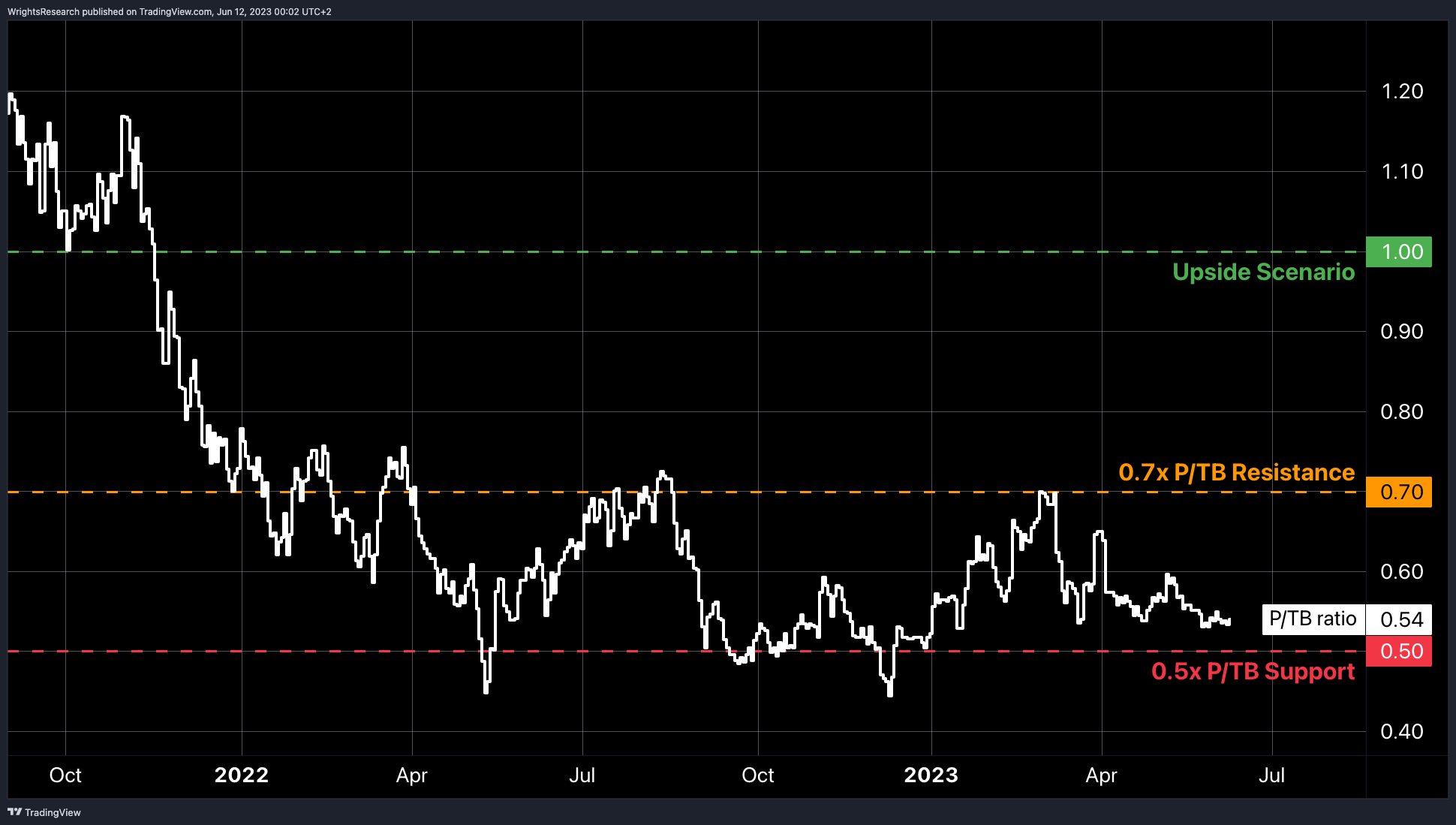

Debt on the other hand is almost non-existent, with total debt in Q4 of $18.32M, which means we believe the company has somewhere north of $1.18BN of tangible book value, taking recent data into account. That's very interesting when you know that Nano Dimension's market cap is currently $607.69M. In other words, that would be a price-to-tangible book value of 0.51x, almost all of which book value is concentrated in cash, short-term investments and public securities.

{kind=link}

TIKR Terminal

But getting back to why the company is probably trading so far below its tangible book value, perhaps it is the negative earnings it is still experiencing. But even at current share prices, we think investors are arguably too pessimistic about the company's future prospects.

As indicated earlier, the company is trading at 0.51x price to tangible book value, or with the latest data by our estimate $596M below tangible book value. Even with operating income of -$131M in 2022, it would still take more than 4.5 years for the company to trade at tangible book value again. But that's where we note some interesting developments that other investors/the market seem to overlook. First, while the company is losing money on the bottom-line, the top-line is still growing 40% year-over-year as of Q1. If we extend Q1 revenue to the full year, they should be able to generate $58.4 million in revenue.

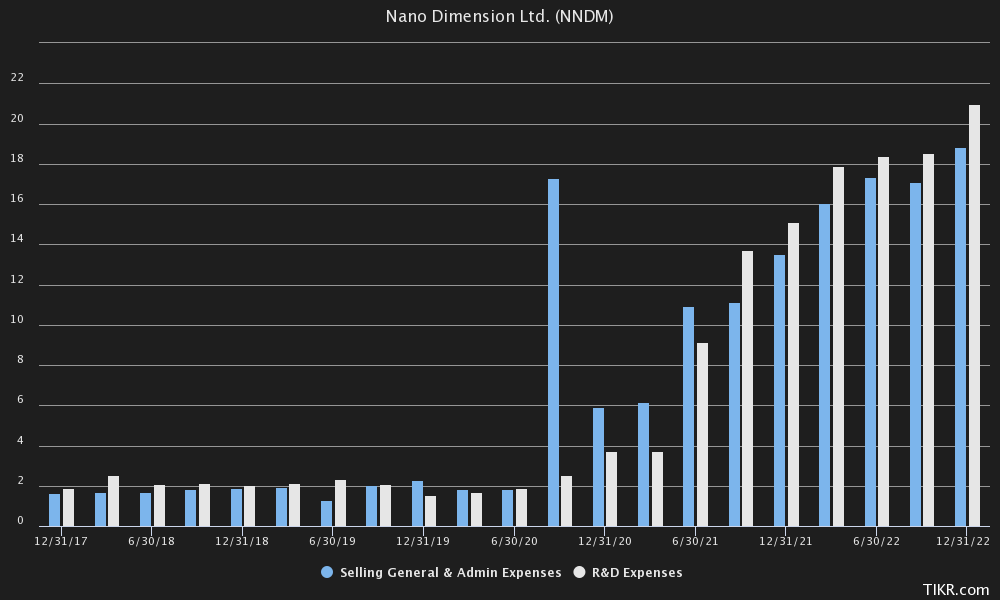

In Q4, they achieved a gross margin of 68.7%, which means that even at a gross margin of 65%, they could theoretically be able to gross up to $37.96 million. However, most of their expenses are operational costs, such as SG&A and R&D. We believe that, especially in R&D, most of these costs consist of engineering salaries, which by accounting rules are charged directly to earnings as they are incurred. Although these costs are charged directly to earnings, they should also provide benefits in the future. Both SG&A and R&D combined amount to nearly $40M per quarter.

{kind=link}

TIKR Terminal

What may not be talked about much is management's plan to perhaps try to keep the OpEx largely flat after building the infrastructure they have now:

But the next stage will be to reducing those percentages even more toward profitability and that comes in two ways: one, increasing revenue without increasing operational expenses because we built an infrastructure guys, we have a run-rate of 50 – last year, $44 million this year, projected to grow dramatically. ( Q4 Earnings Call )

In Nano Dimension's earnings presentation for the fourth quarter, they also highlighted the fact that cash expenses for R&D were a large part of the EBITDA loss for the fourth quarter, and when adjusted for it, adjusted EBITDA only comes down to -$6.9M, which means that if costs are cut when revenue growth slows, the company would actually be in good shape and closer to neutral in terms of cash burn.

{kind=link}

Nano Dimension IR

Even if we go back and take for granted the previously calculated $37.96 million in potential gross annual profit, that does not take into account the interest income the company receives on its gigantic balance sheet, which is also seemingly overlooked. It is only in recent months that interest rates, especially in the United States, have become a major factor in Nano Dimension's performance. As mentioned in the Q4 earnings call:

So in 2022, we had interest revenues of around $18.5 million. Obviously, most of it is towards the second half and very heavily even in the fourth quarter because of the rising interest rates. And in this quarter, the first quarter of 2023, we are at a run rate of more than $11 million a quarter from interest revenue. So, assuming the interest will continue to be as much as they are today, you can multiply it by four and see where we project our interest revenues will be.

At the current 3-month US Treasury bill rate of 5.12%, the company could potentially earn as much as $53 million in interest on its cash balance alone. However, this is a game changer not previously taken into account because interest rates were just going up, and we think the market has not taken it into account. Even if interest income were only $44 million for the full year, added to our generous estimate of gross income, this could total $88.96 million.

So even if operating expenses were $160 million, we expect the cash burn to be only around $71 million. In other words, under such a burn, it would take more than eight years for the company to regain tangible book value. And if, in an extreme scenario, the company decides to drastically reduce OpEx by 50% to $80M per year, the company would theoretically actually start making a profit. The CEO also seems positive about these developments, indicating that cash flow should improve significantly between 2022 and 2023:

We’re going to be profitable very soon. At least by cash flow, I can tell you that the – our cash flow improvement from 2022 to 2023 is going to be huge. We’re going to be much less in cash burn out. And again, the profitability will follow. It depends on the acquisitions as well.

What we are mainly trying to point out is the fact that we think the market is probably overly bearish on the company as it currently sees a deterioration of the bottom line. But 2023 could very well be the turning point, where the cash burn actually decreases. When you combine that with the fact that the company is trading at almost 0.5x tangible book value, we think that could lead to some positive surprises on the upside.

Interesting Developments

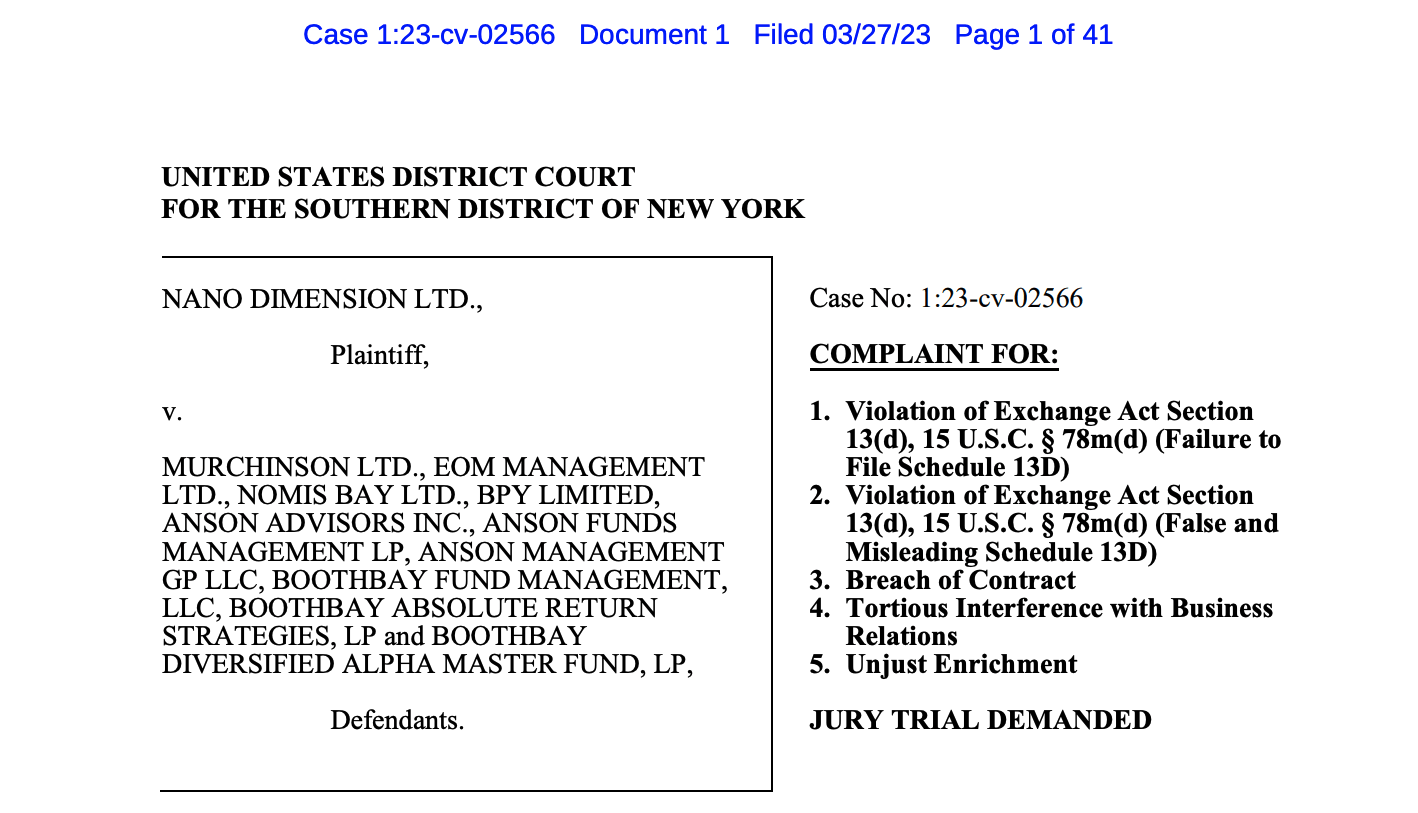

There are also three very interesting developments going on recently that could lead to unlocking more value for shareholders. One has to do with Nano making a bid for Stratasys, the other with activist investors trying to unlock the trapped value in Nano (balance sheet) and the last with the company buying back its own shares.

First, on the subject of activist investors: three activist investors seem to still hold their shares in the company. Anson Funds, Murchinson and Boothbay Fund, together own 17.60% and have bought shares under $3. Recently, however, the situation has become heated, with Nano Dimension suing some entities allegedly accusing them of short selling to buy the shares at a lower price and then trying to dismantle the company.

{kind=link}

Southern District New York Court

It appears that Murchinson et al. also recently filed a counterclaim against Nano Dimension, with securities lawsuits pending in the New York Southern District Court. Although the activist investors were unable to take control of the company by holding their own general meeting, an Israeli court did rule that two observers will be appointed until the next annual meeting to ensure that fiduciary duties to shareholders are met:

The court also decided that, on a temporary basis, until the Company’s next annual meeting or resolution of this matter by the court, two observers will be appointed, subject to signing the Company’ non-disclosure agreements and their obligation to maintain fiduciary duties. Nano Dimension intends to appeal to the Israeli Supreme Court against this decision.

Regardless, we believe there is still an opportunity for shareholders to perhaps unlock value at the next shareholder meeting if these activist investors are able to take control of the company and are able to return the cash in the company to shareholders. Since Nano Dimension is currently trading at nearly 0.5x P/TB, this could essentially result in a near-doubling of the share price if this scenario becomes a reality.

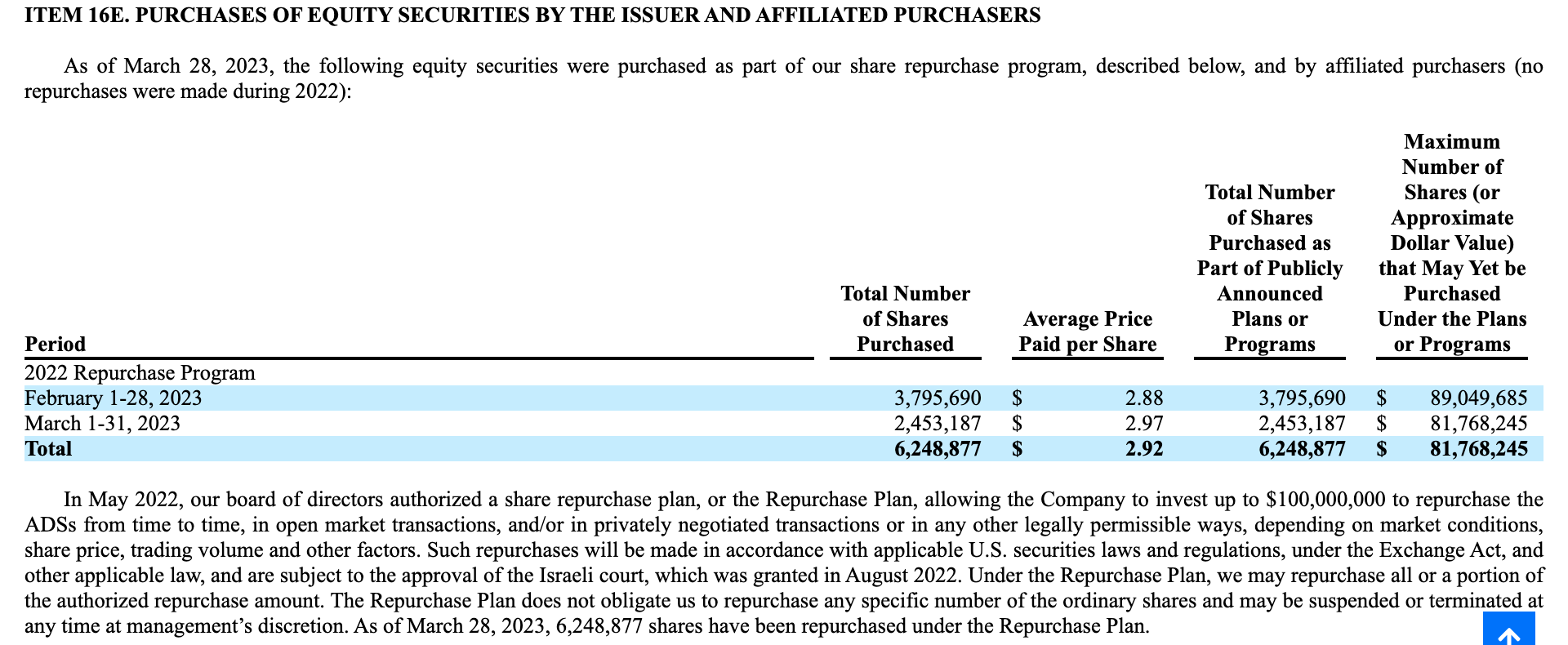

Second, the company still has enormous capacity left from its buyback program: through March 31, it had only repurchased $18.25M worth of shares. That means there is still over $81.75M of capacity left to buy back shares below book value. And especially now, with shares trading cheapest near 0.5x book value, they are basically able to buy back a huge amount of outstanding shares at a discount. The average price paid per share was $2.92, at which point management apparently felt the shares were undervalued. So we see no reason why they wouldn't buy shares now at $2.40.

{kind=link}

SEC, 20-F

With this buyback program, they could essentially put huge support at the 0.5x P/TB level and buy up to $100M worth of shares, when the market cap is only $607M and the underlying is $1.2BN. Anyone selling or shorting the stock at these levels is apparently just swimming against the current.

Finally, there is also a possibility that Nano Dimension could unlock value through mergers and acquisitions. For example, if they were able to buy Stratasys at fair value, then Nano shares should likely move closer to 1x P/TB from the 0.5x P/TB it currently stands at. The situation is very interesting right now, with Stratasys apparently planning to acquire Desktop Metal ( DM ) and merge with the company. Moreover, 3D Systems ( DDD ) has also made an offer for Stratasys, which 3D Systems says will bring a value of $25 per share to Stratasys.

Nano Dimension owns about 14.45% of the outstanding Stratasys shares, which means that even if they are unable to buy more shares, they would still be profiting if Stratasys is able to push the share price to $25 with 3D Systems. After all, the idea of Nano Dimension, a $607 million company buying Stratasys with a market capitalization of $1.21 billion, is actually quite wild, something we've never seen happen. It's certainly a very peculiar position to find yourself in.

Asymmetric Return Profile

Nano Dimension is essentially a classic Benjamin Graham idea of value investing, where you can buy a company below book value to get a wide margin of safety. That said, we will explain where we see the stock going in the future.

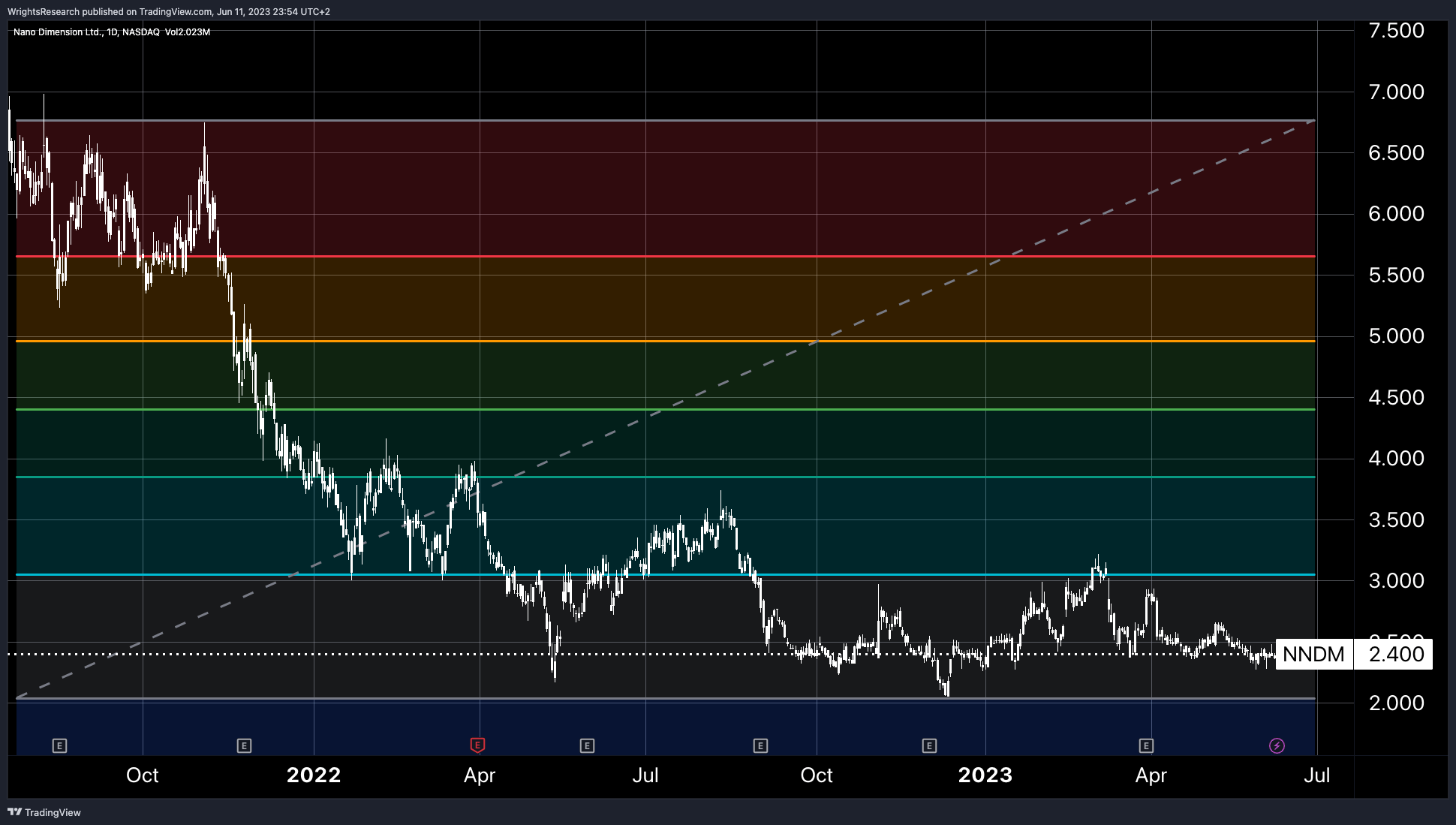

On a technical level, the stock appears to be getting tremendous support at the $2.25 level, with only two times a few days trading slightly below that level. However, it is perhaps important to note that the company has started buying back shares since 2023 and has never traded below the $2.25 level since then. In other words, we think that if the shares were to ever move toward the $2.25 level again, we think the company would likely support the shares by buying back handfuls of shares with the more than $80 million in buyback capacity it still has.

{kind=link}

Wright's Research, Tradingview

In other words, we think the downside move is mostly only -6.25% down, protected by buybacks and tangible book value. Therefore, we would be inclined to buy close to the $2.25 level and start selling when it meets resistance at $3. This should be an easy 33.33% rise from $2.25 to $3.

However, if the value were unlocked and the stock traded closer to its tangible book value, which we believe is closer to $4.80, the rise would exceed 100%, setting us up for a very asymmetric risk-return scenario.

{kind=link}

Wright's Research, Tradingview

In terms of risks, the biggest risk we would see is that management executes mergers and acquisitions at an unfavorable price, which would reduce shareholder equity in excess of 50% over time, at which point the downside scenario could be lower than $2.25. Or perhaps management increases costs and OpEx dramatically, burning up shareholder equity without creating value.

Neither really seems to be the case, since they plan to increase efficiency in 2023 and management's bonus is strongly tied to warrants that require the share price to rise above a certain level by a certain date.

{kind=link}

SEC, 20-F

{kind=link}

SEC, 20-F

The Bottom Line

We believe Nano Dimension represents a very attractive, asymmetric risk/reward proposition, with the downside protected by tangible book value and share repurchases at $2.25, and the upside exceeding 100%, should any of the above events occur.

For further details see:

Nano Dimension: Interesting Asymmetric Risk/Reward Scenario