ELV - Narrowing Down High-Quality Dividend Growth: Elevance Health Is Elemental

2023-07-24 05:16:57 ET

Summary

- A watchlist of high-quality dividend growth companies is evaluated to identify potential bargains in the market through historical and future fair valuation methods.

- Elevance Health appears to be trading at a discount to historical and future fair value, as well as to be attractive based on analyst estimates.

- Lockheed Martin, MarketAxess, Nike, and UnitedHealthcare are attractive based on historical fair value, analyst estimates, and close to fair value based on Future Fair Value.

- Despite potential regulatory and market risks, ELV appears to be a safe dividend growth investment, with a low yield offset by strong dividend growth.

Introduction and Background

The market has been on a role as of late. As such, bargains in the high-quality dividend growth investment space have been harder to find. This is why I find it important to maintain a watchlist of around 100 high quality dividend growth companies that I regularly update. This allows me to identify potential bargains, when inevitably they go on sale, sometimes for very short periods.

I have been slowly trying to allocate a growing store of cash for the past several months. I have found some good opportunities, and yet, I am still on the search for more. For this article, I decided to turn my attention to those companies on my watchlist that have reported earnings recently, to potentially find those companies that the market hasn't quite caught up with late.

This produced the following list:

{kind=link}

{kind=link}

Fair Value Estimation

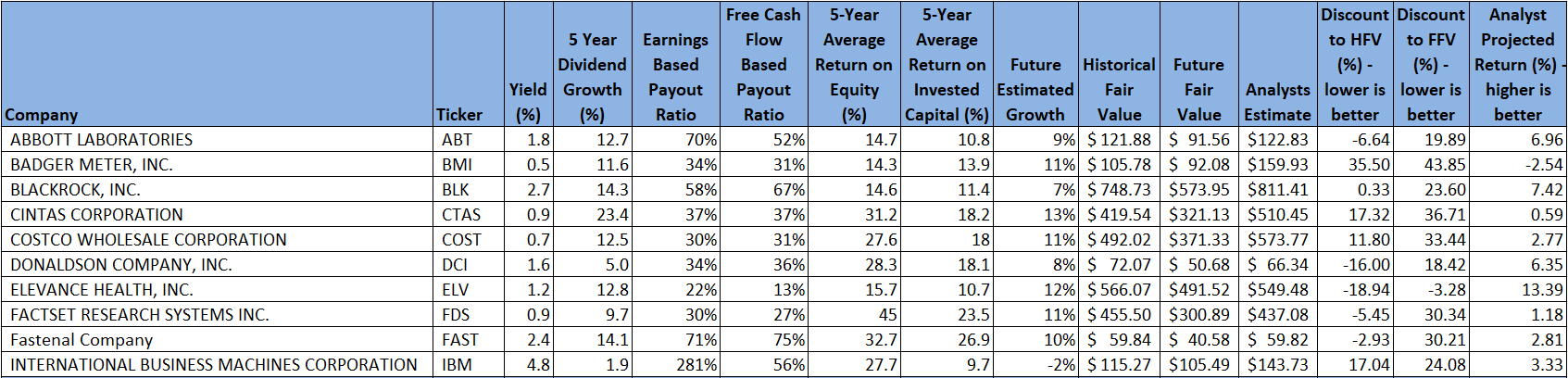

As I've described in previous articles, I like to calculate a fair value in two ways, using a Historical fair value estimation, and a Future fair value estimation. The Historical Fair Value is simply based on historical valuations. I compare 5-year average: dividend yield, P/E ratio, Schiller P/E ratio, P/Book, and P/FCF to the current values and calculate a composite value based on the historical averages. This gives an estimate of the value assuming the stock continues to perform as it has historically. I also want to understand how the stock is likely to perform in the future so utilize the Finbox fair value calculated from their modeling, a Cap10 valuation model, FCF Payback Time valuation model, and 10-year earnings rate of return valuation model to determine a composite Future Fair Value estimate.

I also gather a composite target price from multiple analysts including Reuters, Morningstar, Value Line, Finbox, Morgan Stanley, and Argus. I like to see how the current price compares to analyst estimates as another data point, and as somewhat of a sanity check to my own estimates.

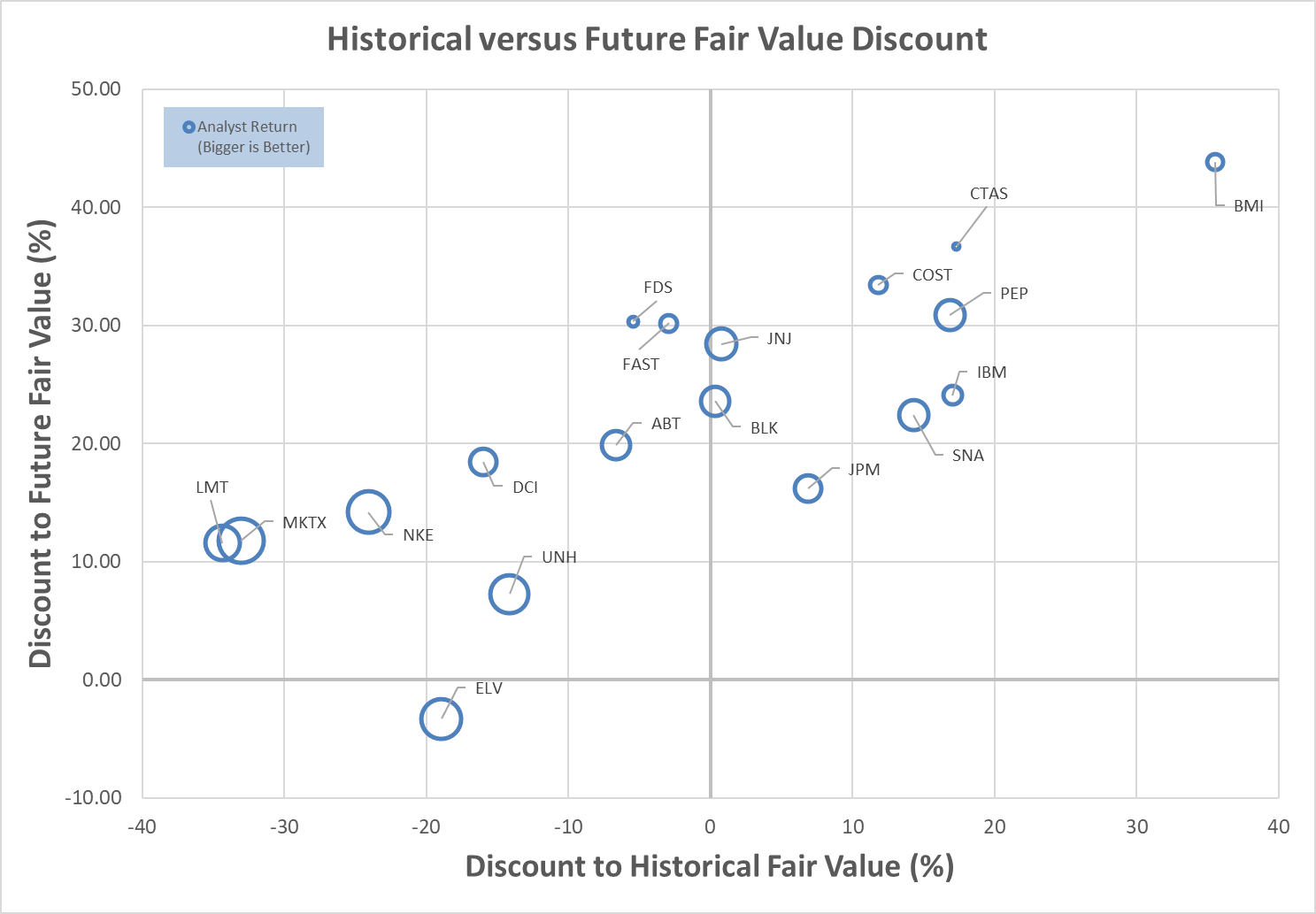

Plotting three variables on one plot is tricky but using a bubble plot allows us to visualize three variables by plotting the Historical fair value versus the Future Fair Value on a standard x-y chart, and then use bubbles to represent the size of discount relative to analyst estimates.

Author calculation of Historical and Future Fair Value, analyst estimates

{kind=link}

This chart is insightful once you understand how to interpret it. What we are looking for are stocks that are trading at a discount to both the Historical Fair Value and the Future Fair Value. So, those stocks that are farther to the left, and farther to the bottom, are potentially the stocks trading at the largest discount to fair value. This would be the bottom left quadrant of the graph. Additionally, those stocks with the biggest bubbles are the stocks that are trading at the largest discount to analyst estimates, so in theory, stocks in the lower left quadrant that also have large bubbles, should be very decent candidates for investment.

Digging into this chart suggests that Elevance Health ( ELV ) is attractively valued from a Historical and Future Fair Value perspective.

I have recently added to my position in this stock, and benefitted from the jump in price it took when earnings were reported.

There are not many other apparent values currently, especially when considering Future Fair Value; however, Lockheed Martin ( LMT ), MarketAxess ( MKTX ), Nike ( NKE ), and UnitedHealth ( UNH ) appear attractive based on Historical Fair Value, while not being terribly over-priced from a Future Fair Value perspective, while also showing upside based on analyst estimates.

Let's dig into Elevance to see if it is a good candidate currently for further investment.

Elevance Health Preliminary Analysis

I like to start simple when analyzing companies. Elevance has a 5-year average Return on Equity of 16% and Return on Invested Capital of 11%. Recent results are in line with the historical averages at 17% and 12% respectively. These are not overly impressive numbers but are above the rule of thumb I personally use of 15% for RoE and 10% for RoIC. I also like to see that RoE is not drastically higher than RoIC, signifying management isn't likely playing games with debt to juice RoE.

Morningstar's Narrow Moat and Standard capital management ratings are ok. This is a competitive segment of health care, with other great companies like UnitedHealthcare and CVS being strong competitors. Elevance is currently 4-star rated at Morningstar, suggesting it could be undervalued.

Now, looking at the dividend, Elevance's 22% Earnings-based payout ratio and 13% Free Cash Flow-based payout ratios suggest the dividend is very comfortably covered and sustainable, with potential for outsized growth. The 5-year dividend growth rate of close to 13% is excellent and helps to offset the low starting yield around 1.2%, for long-term investors. With my estimated growth rate for Elevance being close to the dividend growth rate, I feel this is a good option for the dividend growth investor.

Finally, for our preliminary assessment, let's look at the Seeking Alpha Ratings Summary and Factor Grades.

Seeking Alpha Seeking Alpha

First, from a ratings summary perspective, SA Authors and analysts have are bullish on Elevance. Looking at the factor grades, it seems that the Seeking Alpha algorithms believe Elevance is not very well valued compared to other companies in the health care sector, which is currently beat down, however, the other factors are above average, and even attractive, relative to the sector.

Elevance Health Historical Valuation Analysis

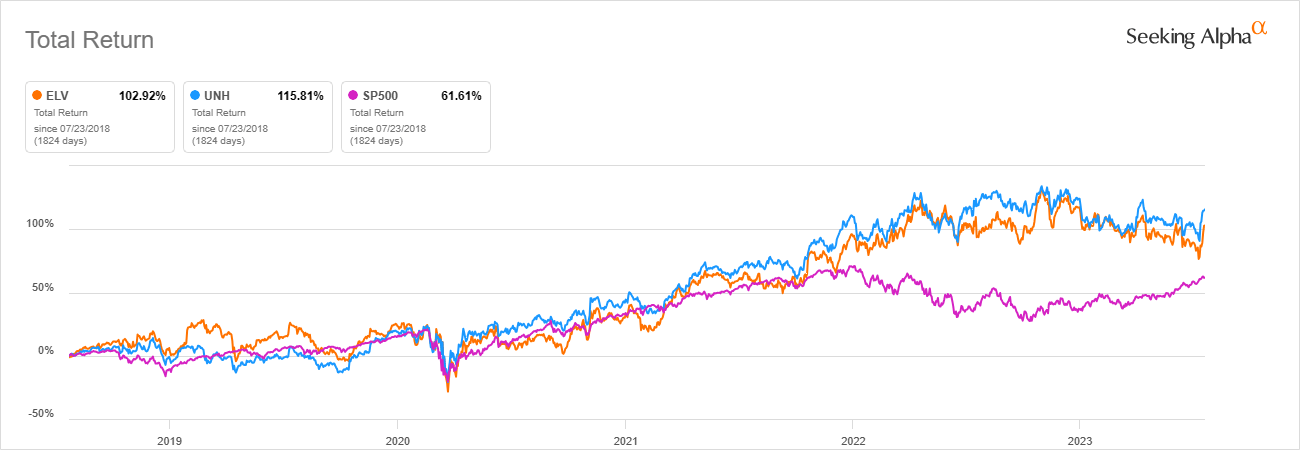

To be honest, my starting point for historical analysis, how Elevance has performed over the past 5 years compared to competitors and the market, isn't really all that useful, but I still like to start with it. In my mind, valuation is more insightful, and we all know past performance is no indicator of future results, but at a minimum, it can provide insight into how volatile the investment is.

{kind=link}

I am only comparing to UnitedHealthcare because it is the only other company from this sector on my watchlist of high-quality dividend growers. It isn't really a competition though, since I own both. They have also performed very similarly over the past five years and have outperformed the S&P 500 significantly.

Outperformance in the past is one thing, but maybe that outperformance was just due to valuation multiples. That's why valuation is important. To know if we should consider investment, we want to be sure we are buying fundamentals, not just exuberance. Two of my favorite initial indicators of valuation are P/E and yield.

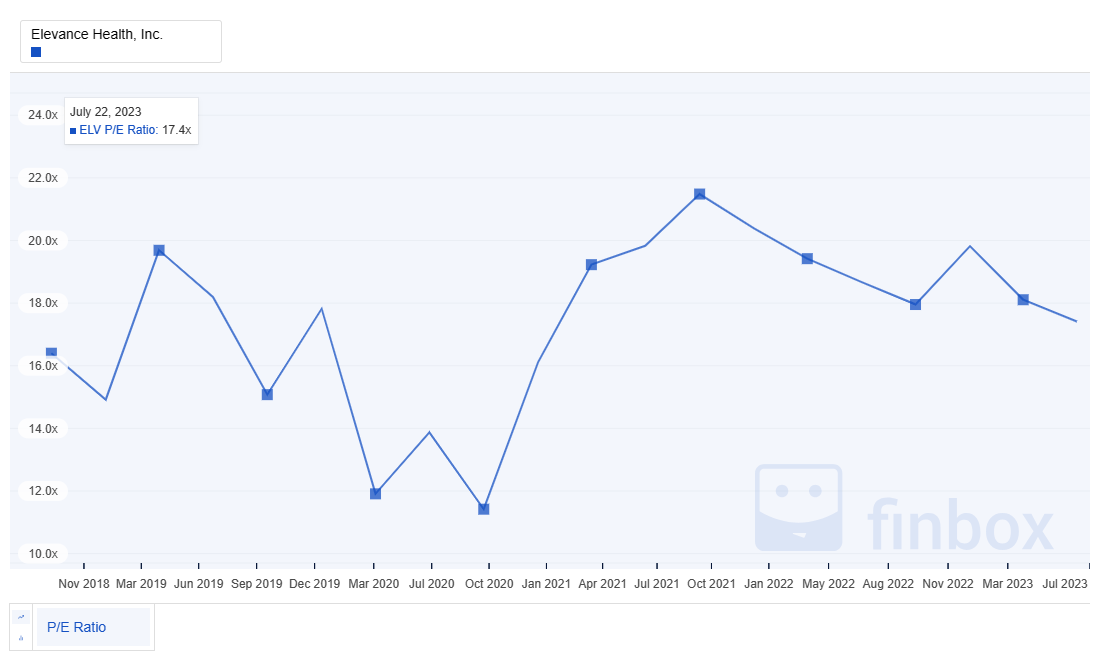

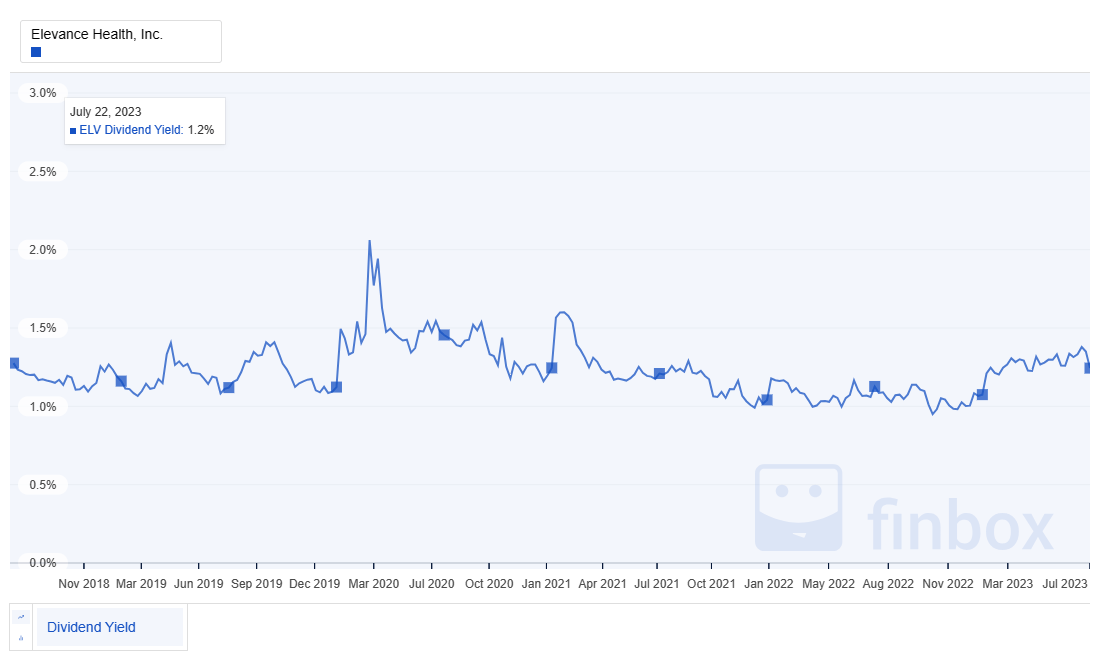

{kind=link}

{kind=link}

Right now Elevance appears fairly valued based on historical comparisons to both metrics. The current P/E of 17.4 is right in line with the 5-year average. The current yield of 1.2% is also right in line with the historical 5-year average yield. Both of these suggest that Elevance may be fairly valued, though likely not a bargain.

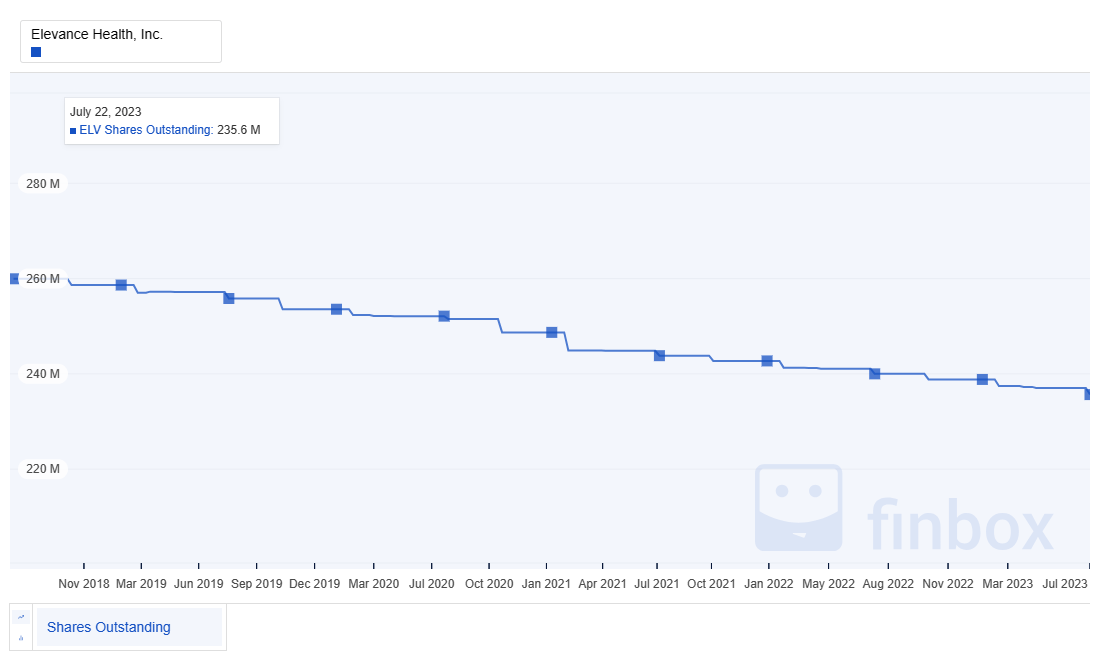

A key part of the Total Shareholder Return includes stock buybacks, which are also important to dividend growth sustainability. Elevance has consistently reduced shares outstanding.

{kind=link}

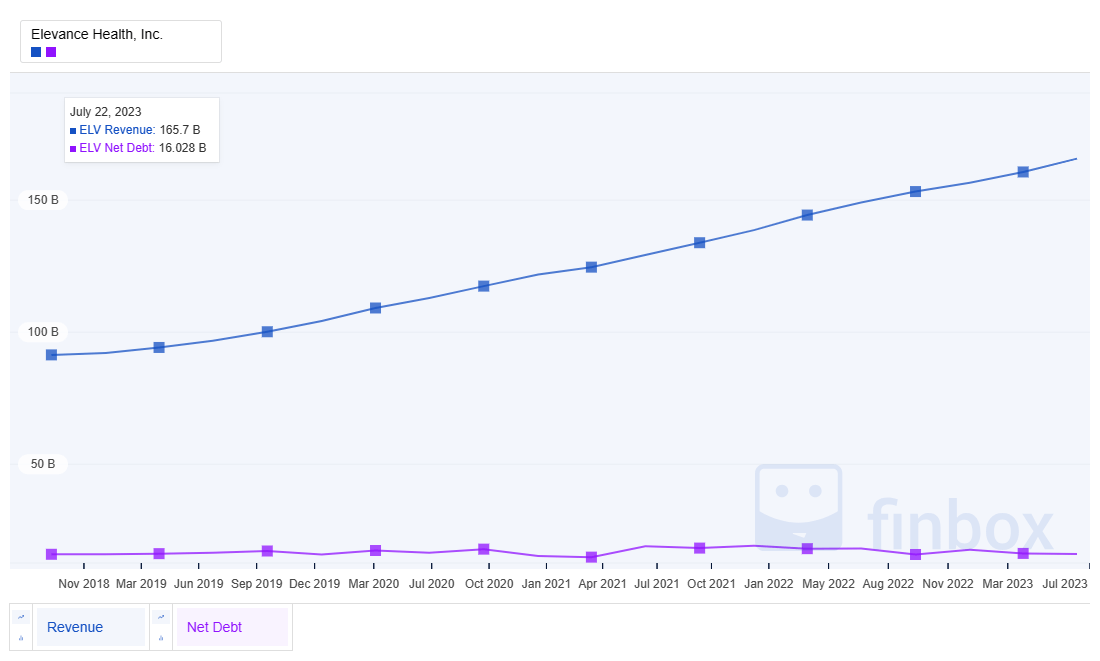

To be confident in dividend stability and growth, it is also important to understand how the revenue compares to net debt. Revenue has grown nicely, and consistently, while net debt has stayed stable. This is a positive sign from my perspective, in that the debt ratio is actually improving over time, giving me high confidence that the dividend will be sustainable.

{kind=link}

Elevance has been paying a growing dividend for over 12 years. The growth has been solid and sustainable. The most recent increase of 15.6% is just above the average 5-year dividend growth of 12.8%, both of which are stellar.

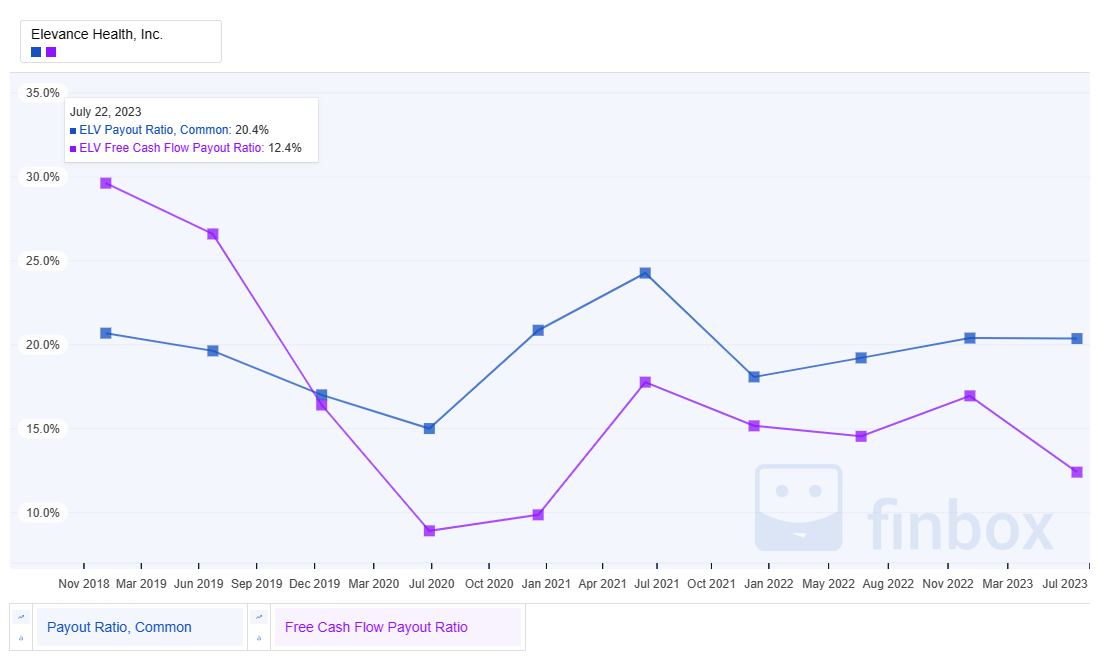

Obviously, dividend growth doesn't do any good if the growth is not sustainable. In this case, Elevance's earnings and free cash flow-based payout ratios have remained relatively consistent and are low. This is another indication that the long-term dividend payout and growth should be sustainable. With payout ratios of 22% based on earnings, and 13% based on free cash flow, there is a lot of margin to protect, and increase the dividend.

{kind=link}

Based on these various indicators of valuation based on historical perspective, Elevance appears to be fairly, if not under-valued, especially considering the potential future growth opportunities.

Elevance Health Future Valuation Analysis

Because we want our dividends to grow in the future, not just the past, we need confidence that the results the company has already achieved will likely continue.

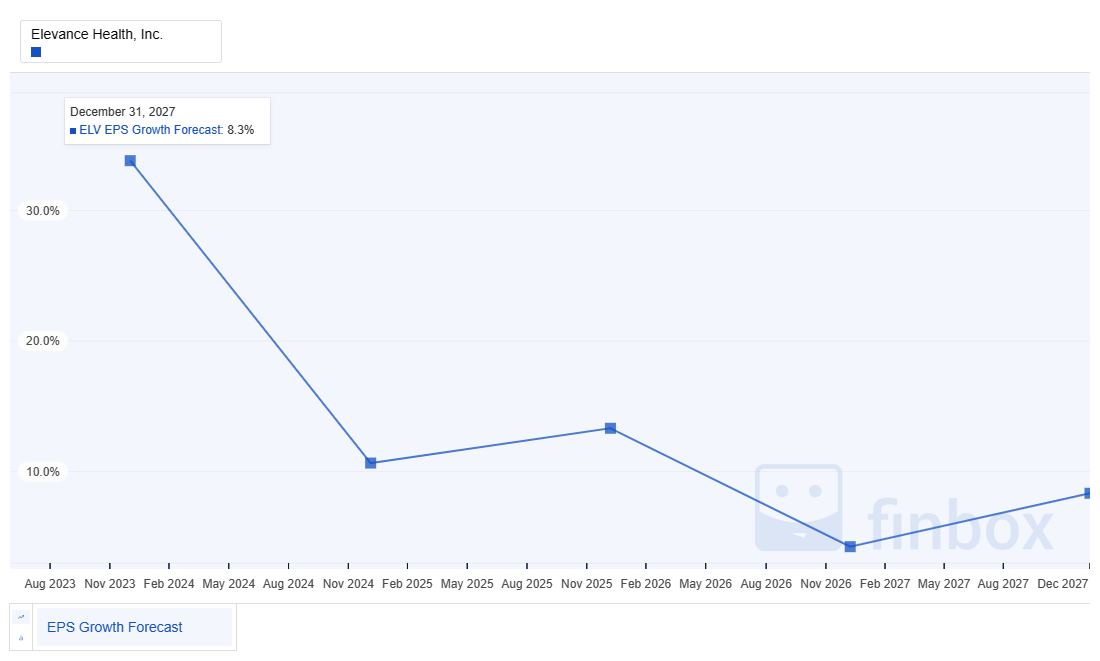

Looking at future Earnings Per Share projections, the future growth looks solid. Shorter term, the growth is projected to be very strong, followed by a period of moderating to lower growth. Just based on Earnings Per Share, an upper-single digit growth looks like a reasonable outcome.

{kind=link}

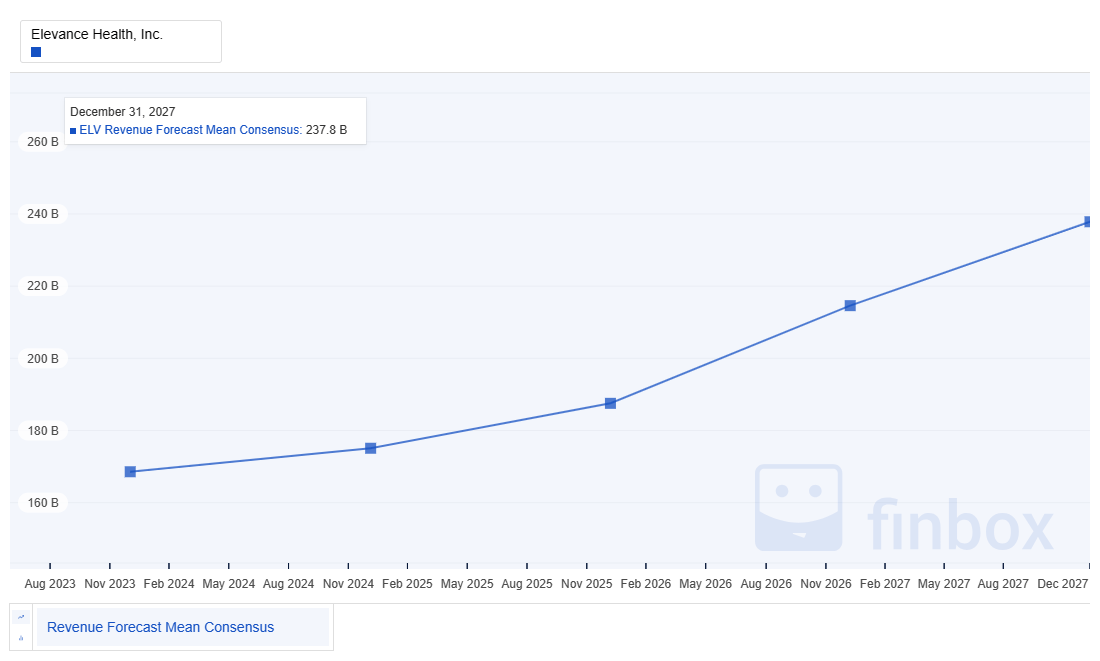

Earnings Per Share can be manipulated, so revenue growth is potentially a more pure indicator of growth health. Revenue growth projections for Elevance look stable, consistent, and admirable.

{kind=link}

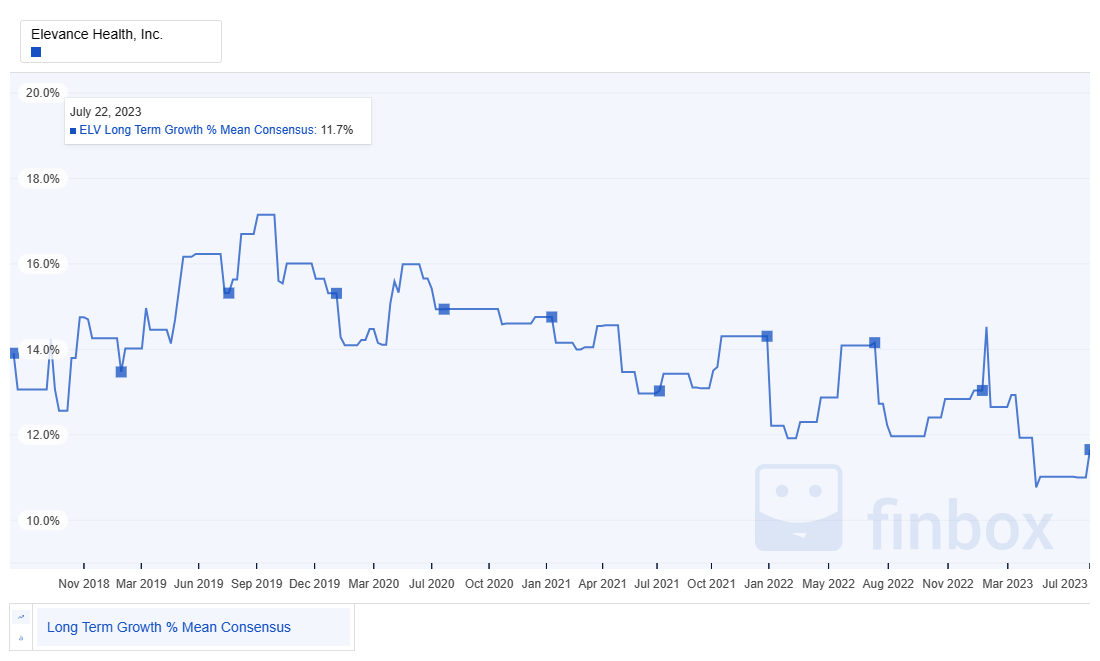

Growth is one of the hardest things to predict in investing, otherwise, investing would be much simpler. As we discussed, future growth for Elevance looks promising. In the case of growth, I do also like to look at historical growth estimates. In this case, generally growth projections have been in a similar range to the future projections shown, which suggest a stable, sustainable business model.

{kind=link}

My own estimate for Elevance's forward growth is around 12%. I derive this from a combination of various growth projections and growth models. This doesn't seem particularly unreasonable and aligns well with strong dividend growth sustainability.

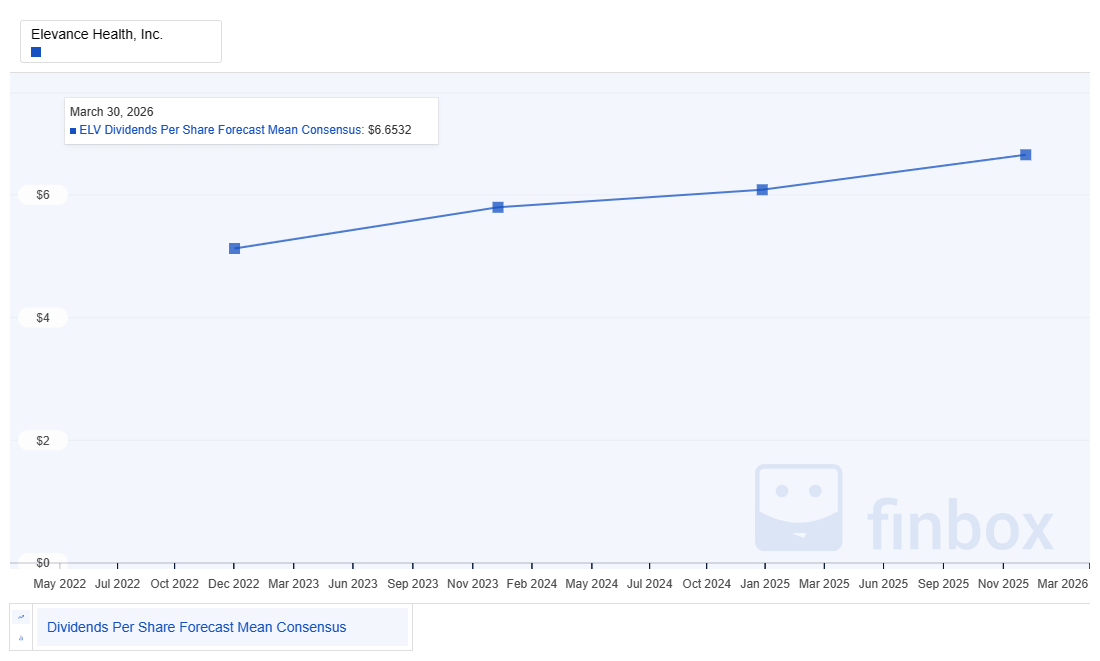

For a dividend growth investor, understanding future dividend growth potential is also important, especially in as much as it is sustainable. Here are the long-term dividend growth projections for Elevance. The forecast growth looks very consistent. At least for the next few years, it seems likely that Elevance will continue solid, dividend growth.

{kind=link}

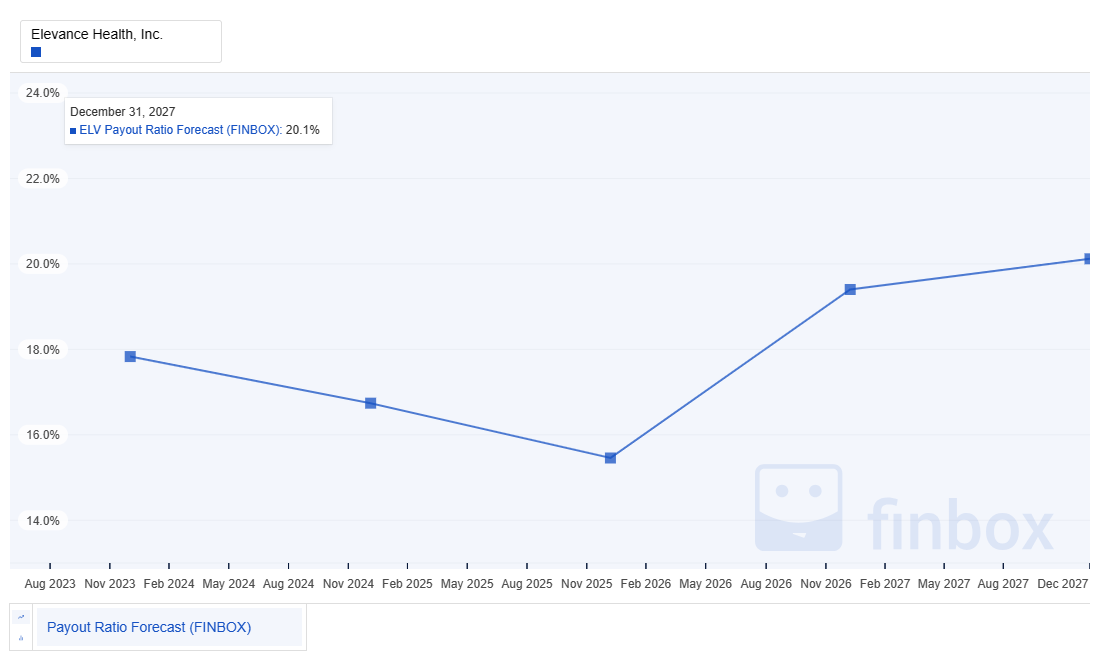

Based on this forecast, and what we've seen already as far as earnings growth and projected dividends, it shouldn't come as a surprise that the earnings payout ratio is also forecast to be well controlled for the near future. The low levels of the payout ratio forecast suggest there will be room for incremental investment back into the business, increased dividend payouts beyond the forecasts, or incremental share buy-backs. All of these are positive for the investor looking for sustained dividend growth.

{kind=link}

Elevance Health Risk

I have very high standards for the companies that make their way onto my high-quality dividend growth watchlist, and into my portfolio, so risk is relative. The S&P credit rating of A and A Value Line Financial Strength rating attest to the quality of this company.

That aside, there are a few risks to discuss. First, healthcare costs are high and therefore the target of increasing regulatory uncertainty. The managed health care sector is by nature, right in the cross hairs of potential regulatory risks. The Inflation Reduction Act specifically targets Medicare costs, which could pressure margins for companies that are part of the profit value stream. For managed health care companies, there will be pressure as input costs increase, while end-customers, including the government, increasingly can't afford to pay more for treatments. Second, there are continued reports that pent up demand for discretionary healthcare due to COVID may result in lower profit and cash flow for managed healthcare companies.

Contrasting these regulatory and market risks, is the natural growth that is projected for healthcare. In a recent Seeking Alpha news article the following was reported:

Annual healthcare expenditure in the U.S. is set to reach $7.2T in 2031, making up about 20% of the total economy, the Office of the Actuary at the Centers for Medicare and Medicaid Services ((CMS)) said in its annual spending report last week.

That is up from $4.4T in 2022, when the U.S. health expenditure accounted for ~17% of the economy, compared to ~18% in 2021 as the economic growth outpaced post-COVID growth in healthcare spending.

However, during 2022 - 2031, the national healthcare expenditure is expected to surpass the economic growth, expanding 5.4% per year on average, despite legislative efforts to contain soaring drug prices.

The Inflation Reduction Act (IRA) passed in 2022, introducing unprecedented changes to Medicare prescription drug pricing, is anticipated to cause a "minor, but noteworthy, influence on Medicare spending trends," according to the CMS.

For the dividend growth investor, Elevance appears very safe. Based on Seeking Alpha's dividend grades, this also appears to be a very safe dividend investment, with the obvious caveat that low yield will need to continue to be offset by strong dividend growth.

Seeking Alpha

I also like to look at short-term risk indicators for any new investments, with Short Interest being one key indicator for me that I might be missing something that others might know.

Seeking Alpha

Based on the very low short interest currently in Elevance, this would not make me hesitate to initiate or add to my position in this quality company and given how few companies appear to be trading with favorable valuations on my watchlist right now, I likely will be adding to my position.

Summary

As I stated at the beginning of the article, I recently put my money where my mouth is and added to my position in Elevance. I am strongly considering adding more after the recent earnings release. I have held Elevance since 2020. It has been a very good investment for me while I've held and added to it multiple times when valuations appear favorable. It has provided relatively good stability, while also having favorable industry trends.

As part of the analysis, Lockheed Martin, MarketAxess, Nike, and UnitedHealthcare appear attractive based on Historical Fair Value, while not being terribly over-priced from a Future Fair Value perspective. They are also potentially favorably valued based on analyst estimates.

For further details see:

Narrowing Down High-Quality Dividend Growth: Elevance Health Is Elemental