NCMI - National CineMedia Prepares For Bankruptcy Emergence

2023-08-03 08:18:32 ET

Summary

- National CineMedia is set to emerge from bankruptcy in August or September.

- Common shareholders took part in the bankruptcy recovery as secured claimants.

- NCMI's revenue projections are lower than pre-Covid levels, but the company may still offer an attractive investment opportunity.

National CineMedia ( NCMI ) is set to emerge from bankruptcy in “August or September” after receiving bankruptcy plan approval in court . The situation is unique, as the company repurchased some secured debt at the parent company level last year, not the subsidiary that filed for bankruptcy. As a result, common shareholders took part in the bankruptcy recovery as secured claimants, while unsecured creditors got almost nothing . Shares even has a brief "meme" moment in April . Do common shares represent an attractive investment as the Company exits bankruptcy?

History

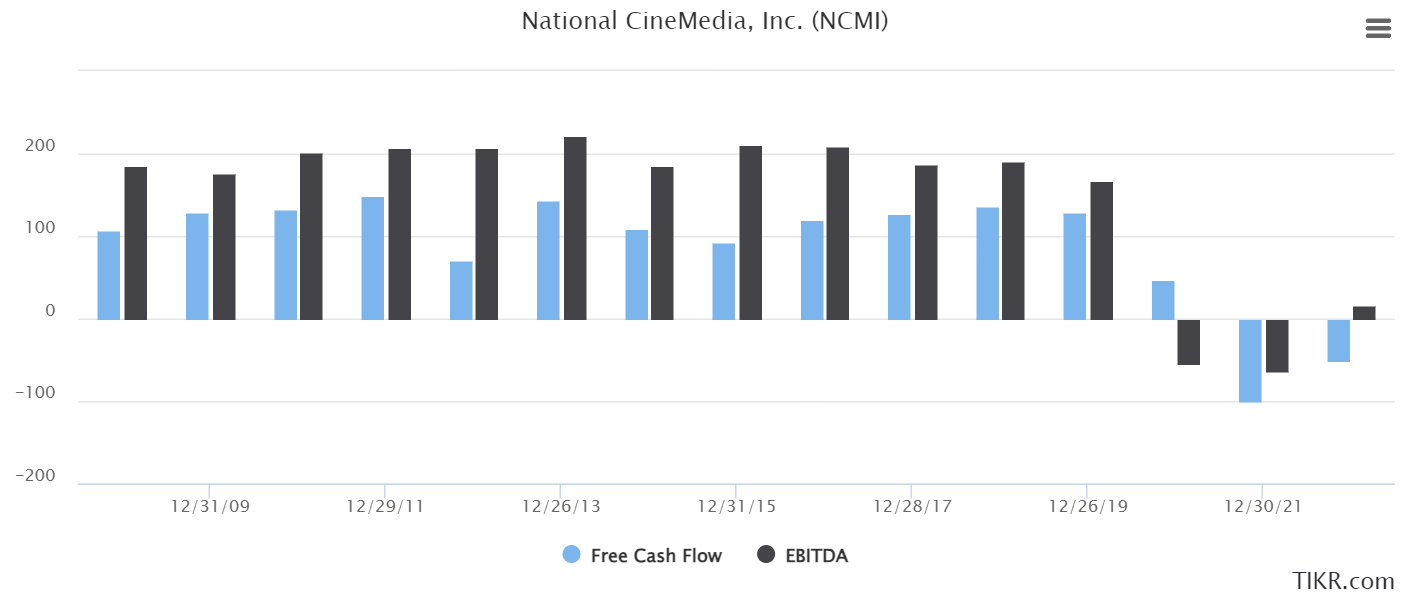

NCMI has an effective monopoly on movie theatre ads in the US, partnered with Regal, AMC, and Cinemark to provide on-screen ads before movies. This lucrative partnership generated impressive, steady cash flows for over a decade prior to Covid decimating the movie theater industry:

{kind=link}

NCMI became a victim of its own capital structure, with $1B of debt unsupported after revenues evaporated. However, thanks to Management’s shrewd debt repurchase, common unit holders retained exposure to the post-bankruptcy entity.

NewCo Earnings Profile

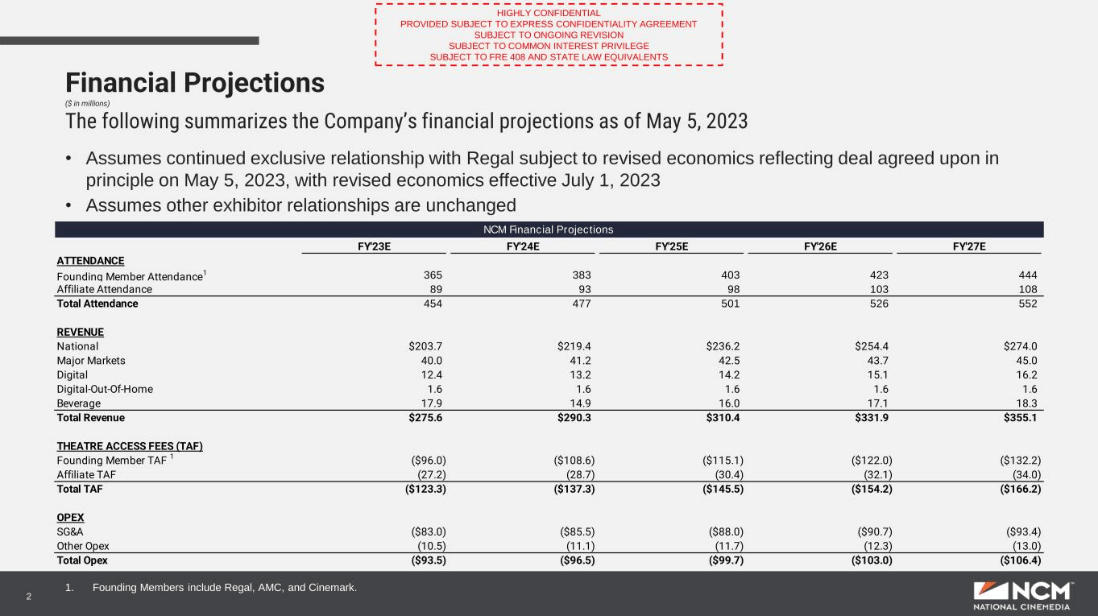

Per financial projections filed in April and revised in May after negotiations with Regal, NCMI is estimating the following “base case” for theatre attendance and financial results going forward:

{kind=link}

As you can see, their revenue projections can’t hold a candle to FY19’s results. This is partially due to lower box office results since Covid, and partially due to a renegotiated deal with Regal after their own bankruptcy experience. NCMI is now suggesting their business is a $50-75m EBITDA business, rather than the ~$200m juggernaut of days gone by.

Conservatism?

Presumably, these projections reflect some conservatism to satisfy creditors that their interests are well-covered, but I wanted to get a bit further in the weeds. Their original assumptions filing showed 651m moviegoers attended NCMI screens in 2019 and 394m in FY22. This compares to 1.2B and 711m tickets sold , respectively, in those years (53% and 55% of total sales). This seems to confirm NCMI has, if anything, improved their market share of theatres since Covid. Year-to-date, theatre receipts are up almost 17% , and NCMI is using a 15% 2023 attendance increase assumption versus FY22. Thenumbers.com suggests this is not due to a change in ticket prices, so their assumptions seem fine.

Unfortunately, Q2 results were filed this week and despite Q2 box office being up significantly Y/Y, actual revenue was down 4% . Perhaps outstanding July results by Barbie Movie and Oppenheimer will help bring new ads into their fold.

Note - if the current strikes in Hollywood continue, it may impact future years substantially.

Valuation

NCMI has disclosed that common shareholders will receive 13.8% of the equity post-bankruptcy emergence. With 174m shares outstanding, at $0.35, this translates to an implied value of $441m. At the estimated $59m EBITDA midpoint for FY23, this is an undemanding 7.5x multiple. I am very curious to see if these estimates end up looking conservative after emergence.

The key question I want to see answered is how capital will be allocated. Historically, parent cash flow was allocated to dividends, which would suggest a nice yield for new NCMI shareholders. If lenders-turned-equity holders are looking for liquidity to exit, NCMI may also offer some level of share buybacks to support their emergence valuation. Especially in the event of the above projections being conservative, this could end up being extremely accretive to remaining shareholders.

I am also curious if they will lever up the business once again to juice returns. If they can borrow under 10% and generate ~15% FCF yield at the parent level, using debt to fuel buybacks would also be accretive. I don’t know what Management’s approach to debt will be so soon after bankruptcy, but this will also be an item to track.

Risks

An investment in NCMI requires some level of belief that the theatre industry can continue to thrive in the face of increased streaming activity. NCMI does disclose some digital revenues in their projections, but it makes up less than 5% of the total. If theatres can recover to pre-pandemic levels, NCMI will likely be a homerun of an investment.

One business risk I’ve seen suggested is the ability to reserve seats in advance may crimp advertising revenue. This will be an important item to watch but is not a particularly new option and is likely already reflected in operating results.

NCMI is working to reverse split their stock to avoid delisting. I assume even a delisting would only be temporary, but this could cause short-term selling if the move fails.

After initially filing for bankruptcy, NCMI senior bonds traded right at the current implied valuation, suggesting one could own the bonds and short the stock above $0.35-0.40 and lock in a nice arbitrage. I expect this dynamic will unwind after emergence and allow for more price discovery, but is likely responsible for the recent narrow price range.

Conclusion

NCMI looks very cheap as they exit bankruptcy, and I’m watching for signs that their projected earnings will end up being conservative. Even if they can merely hit their targets, a 7.5x multiple on FY23 estimates is not a very demanding valuation for an asset-light business with no debt. With effective capital allocation after bankruptcy emergence, NCMI could end up being a winner.

For further details see:

National CineMedia Prepares For Bankruptcy Emergence