EMR - National Instruments' M&A Deal: Little Risk And Acceptable Spread

2023-05-25 10:44:23 ET

Summary

- The software offered by NATI offers an advanced approach to create automated test and automated measurement systems.

- Emerson Electric is expected to pay close to $60 per share in cash for National Instruments Corporation.

- If the merger does not close, I would keep the shares. There are other parties who may launch new bids.

- The companies need the approval of shareholders, the expiration of the waiting period under the HSR Act, and some representations and warranties.

National Instruments Corporation ( NATI ) is expected to close an acquisition agreement with Emerson Electric ( EMR ) for $60 per share in cash. Considering the precedent conditions included in the merger, the undervaluation of the target, and the number of interested parties reported in the background of the transaction, I believe that the transaction will likely close. In any case, I would not be worried about a failed merger because NATI delivers substantial FCF and FCF growth, and I believe that it could be worth much more than $60 per share.

Recent Underperformance

For more than 40 years, National Instruments Corporation allowed engineers and scientists around the world to accelerate productivity, innovation, and discovery. The software offered by NATI offers an advanced approach to create automated test and automated measurement systems. Considering the number of years operating in the industry, I believe that the know-how accumulated is substantial. It is worth noting that I hardly believe that the know-how and expertise accumulated could be incorporated in the balance sheet.

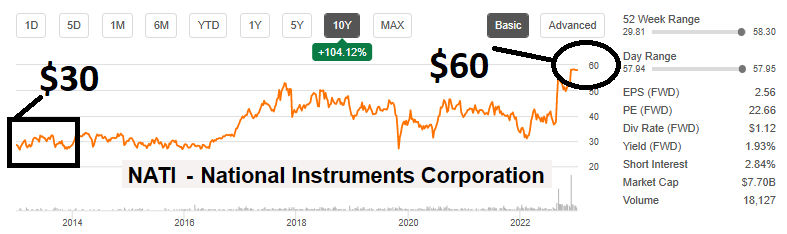

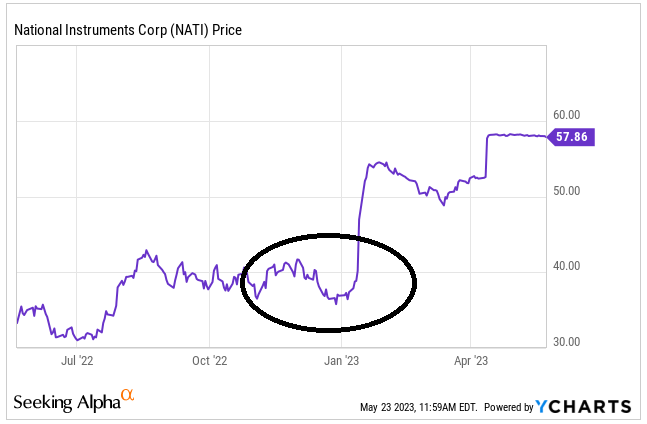

With that about the operations of National Instruments Corporation, in my view, it is fair saying that shareholders could be a bit upset with the recent stock performance. Before the acquisition signed with Emerson Electric, the company was trading at $30-$40 per share, which is close to the level reported close to 9-10 years ago. For understanding why the Board of Directors may have accepted the merger proposal at $60 per share, please see the following stock chart.

{kind=link}

NATI Is Small As Compared To Emerson Electric

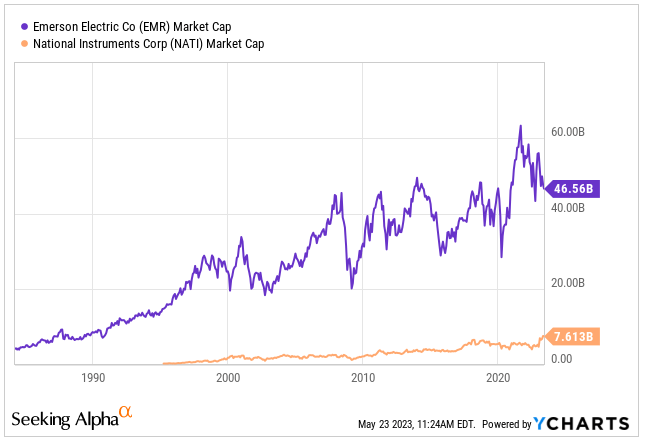

The acquirer, Emerson Electric, reports a market capitalization of more than $44 billion, which I believe is significantly larger than the market capitalization of NATI. In my view, EMR will have sufficient resources to pay and successfully integrate NATI.

{kind=link}

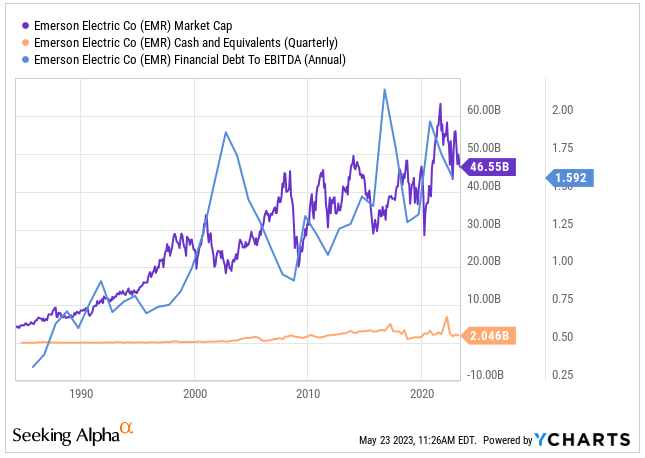

It is also worth noting that EMR reports financial debt/EBITDA of close to 1.59x, which I believe is a small amount of leverage. Besides, the company reports $2 billion in cash, which is close to 24%-25% of the total merger contribution to be paid for NATI.

{kind=link}

Balance Sheet

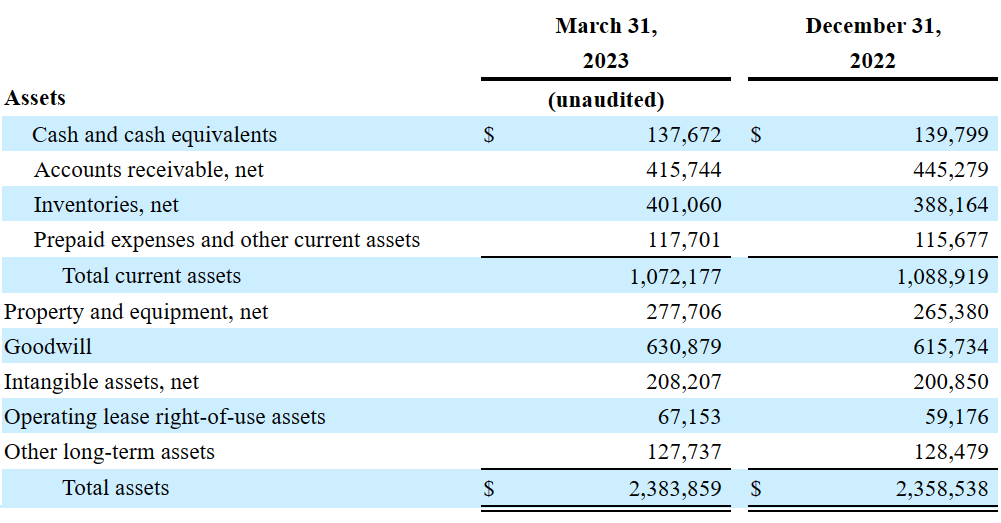

As of March 31, 2023, management reported cash and cash equivalents close to $137 million, accounts receivable of about $415 million, and inventories worth $401 million. Also, with prepaid expenses and other current assets of $117 million, total current assets were equal to $1.072 billion. Considering the current working capital and the total amount of current liabilities, I do not think that National Instruments Corporation suffers from liquidity risks.

The acquirer will likely also receive property and equipment worth $277 million, goodwill close to $630 million, intangible assets of $208 million, and total assets of $2.383 billion. The asset/liability ratio is close to 2x.

{kind=link}

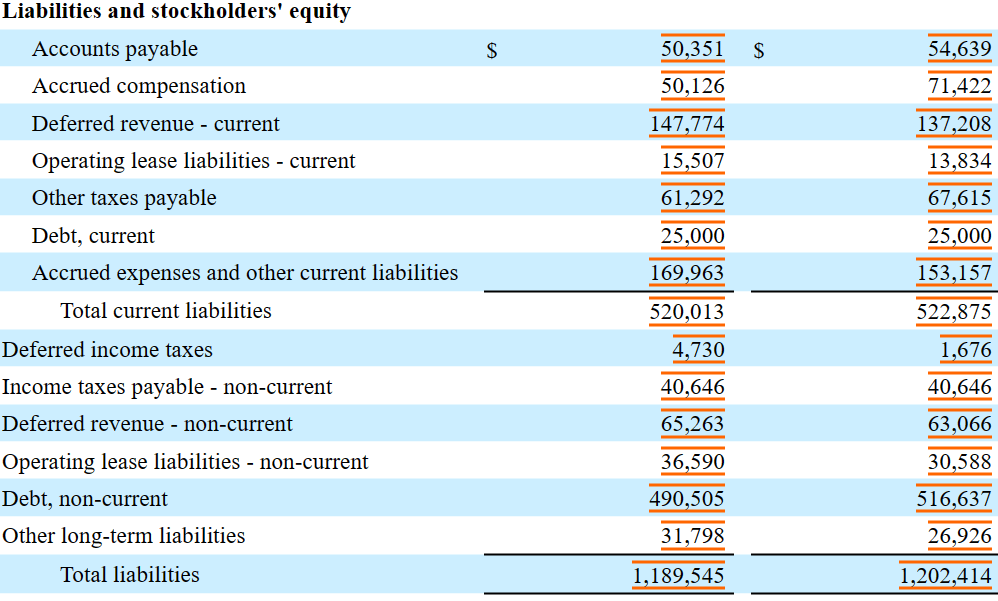

I really do not think that the total amount of debt was a reason to sell the company. Future FCF expectations are sufficient to pay the total amount of debt. Among the liabilities, the acquirer may assume accounts payable worth $50 million, accrued compensation close to $50 million, and current deferred revenue close to $147 million. Besides, current debt would be close to $25 million, with non-current deferred revenue of $65 million, non-current debt of $490 million, and total liabilities of $1.189 billion.

{kind=link}

The Background Of The Merger

I believe that National Instruments Corporation is not a small target, so not many companies out there could bid. From the 8-k, I found that only four parties submitted nonbinding indications of interest: Emerson, Party A, Party B, and Party C. They mostly offered close to $54-$57 per share in February 2023. Below are some excerpts from the 8-K.

Between January 20, 2023 and February 9, 2023, NI executed confidentiality agreements with six parties, including Party A, Party B, and Party C.

On February 23, 2023, four parties submitted nonbinding indications of interest for an acquisition of NI. Party A offered to acquire NI for $54 per share in cash; Party B offered to acquire NI for $57 per share in cash; Party C offered to acquire NI for $55 per share in cash; and Emerson reaffirmed its offer to acquire NI for $53 per share in cash. Additionally, one financial sponsor indicated that it was interested in partnering with a potential buyer in support of an acquisition of NI by providing an equity investment of $500 million to over $2 billion.

The last bidder, Party A, not Emerson, offered $60 per share, but included a significant number of conditions in the merger agreement. National Instruments Corporation preferred the offer from Emerson because the conditions proposed were not as complicated as that of Party A. I believe that the Board of Directors did the right thing. Here are a few other excerpts from the 8-K.

Party A also submitted a draft merger agreement which included a regulatory efforts commitment that imposed significantly lesser obligations than Emerson’s and included several limitations with respect to the level of divestiture and behavioral remedies Party A would commit to undertake in order to secure regulatory approval of an acquisition of NI by Party A.

On the afternoon of April 11, 2023, Emerson and Party A each submitted updated proposals to acquire NI. Emerson offered to acquire NI for $59.50 per share (permitting NI to pay its regular quarterly dividend) and Party A offered to acquire NI for $60.00 per share.

Party A’s proposal also included a reverse termination fee and an 18-month outside date, but continued to have significant limitations with respect to the level of divestiture and behavioral remedies it would commit to undertake in order to obtain regulatory approvals.

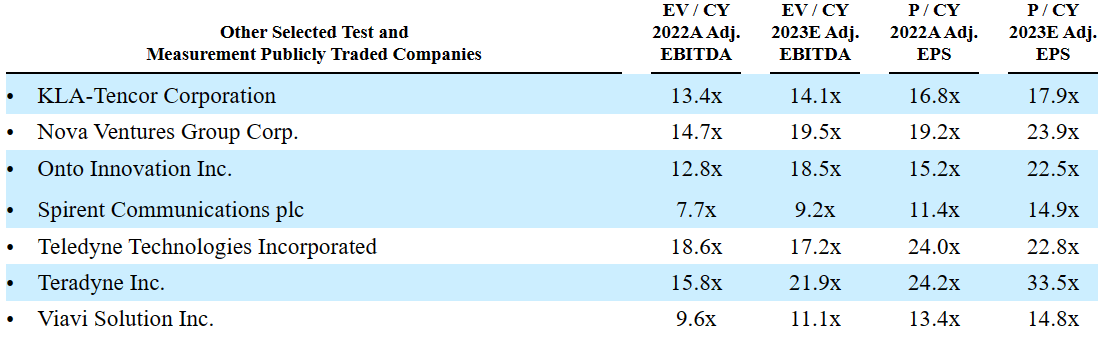

I could also consult the calculations made by the advisor to the merger to reach a valuation of $60 per share. Most peers trade at close to 14x-17x 2023 EBITDA, which implied, according to the financial advisors to the merger, a valuation of close to $53-$71 per share. With these figures in mind, I believe that National Instruments Corporation could be sold at more than $60 per share. I believe that more bidders would most likely have led to a larger valuation.

{kind=link}

{kind=link}

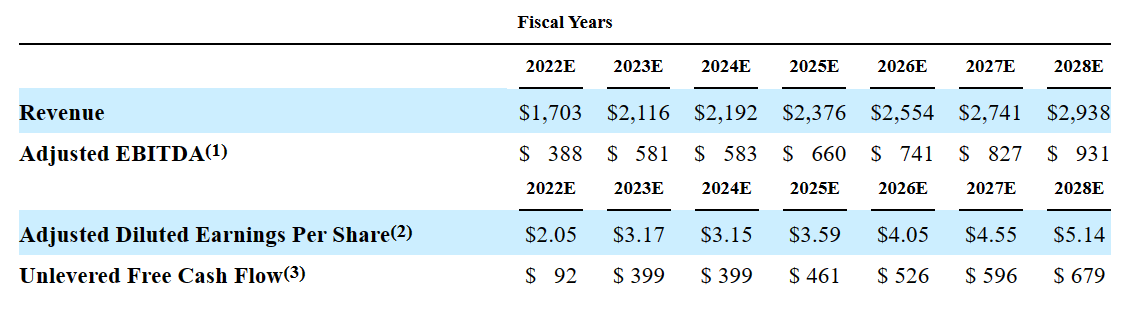

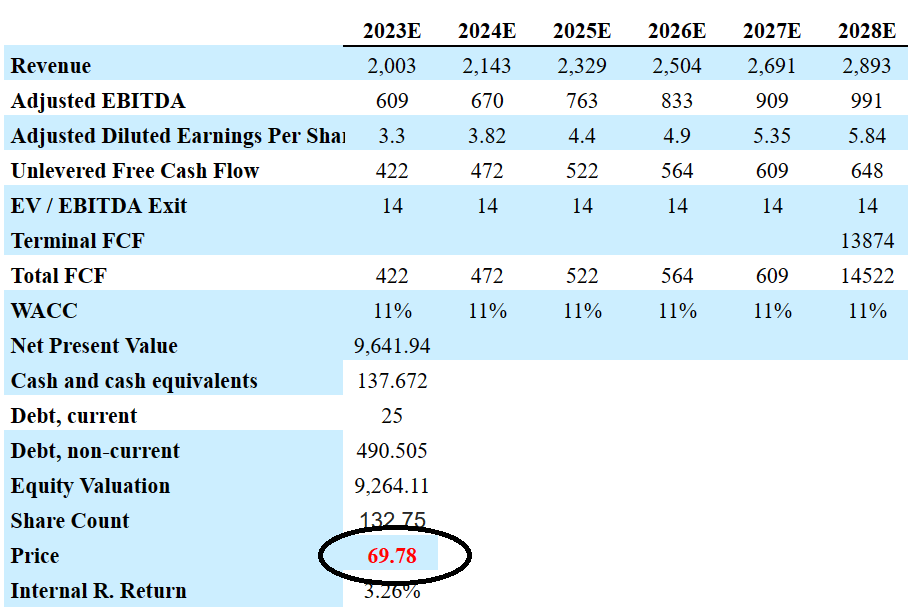

I could also find the expectations of the financial advisor to the merger for the next five years. I used these figures in a simple DCF model, which implied a valuation of $69-$81 per share.

{kind=link}

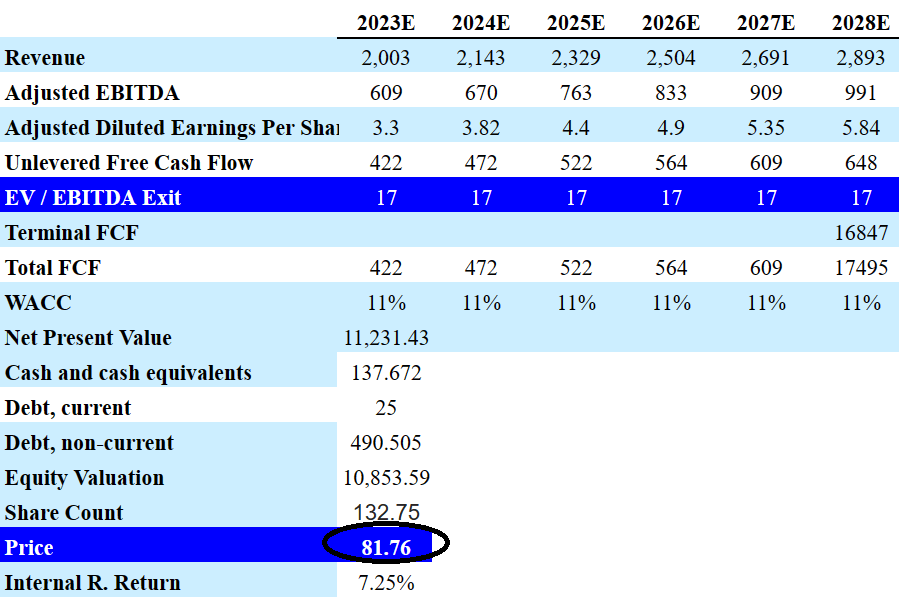

My cash flow model includes 2028 revenue close to $2.893 billion, 2028 Adjusted EBITDA of $991 million, and unlevered free cash flow close to $648 million. If we use an EV/EBITDA exit of close to 17x, the terminal FCF would be close to $16.847 billion. Besides, with a WACC of 11%, the implied enterprise value would be $11.231 billion. Adding cash and cash equivalents of $137.67 million, current debt of $25 million, and non-current debt of $490.5 million, the equity valuation would be $10.853 billion. Finally, the implied price would be close to $81.75 per share.

{kind=link}

If we use an even more conservative EV/EBITDA multiple of 14x, the terminal FCF would be $13.874 billion. Besides, with a WACC of 11%, the EV would be close to $9.641 billion. Adding cash and cash equivalents of $137.672 million and the debt outstanding, the equity valuation would be $9.264 billion, and the fair price would be $69.78 per share.

{kind=link}

In sum, considering that the price being paid is not that expensive, it is quite probable that the acquisition closes. In any case, if we buy, and the transaction does not close, in my view, we are buying a company that could be worth a bit more than $60 per share.

Very Simple Conditions, And I Believe That The Termination Fee Is Not Small

There are other beneficial reasons to have a look at National Instruments Corporation. I believe that the conditions included in the merger agreement are not at all complicated. The companies need the approval of shareholders, the expiration of the waiting period under the HSR Act, and some representations and warranties. Listed below are a few other excerpts from the 8-K.

The adoption of the Merger Agreement by the affirmative vote of the holders of a majority of the outstanding shares of NI common stock.

The expiration or termination of the waiting period applicable to the consummation of the Merger and other transactions contemplated by the Merger Agreement and related transaction documents under the HSR Act and the expiration, termination or waiver of any and all agreements with governmental entities with competent jurisdiction over NI or Parent.

The absence of any injunction or similar order, writ, injunction, award, judgment or decree by any governmental entity with competent jurisdiction over Parent or NI and the absence of any applicable federal, state, local or foreign law, statute, ordinance, rule, regulation, judgment, order, injunction or decree.

The accuracy of the representations and warranties contained in the Merger Agreement.

It is also worth noting that the termination fee does not seem a small amount. It is equal to $310 million, close to 3.7% of the total merger contribution. I believe that both parties will likely think twice before breaking the merger agreement.

Under certain circumstances, NI is required to pay Parent a termination fee equal to $310 million and Parent is required to pay NI a termination fee equal to $310 million. Source: 8-k

There Are Not Many Risks

If the merger fails, which I believe is quite unlikely, investors could lose close to 49% of the investment made. NATI was trading at close to $40-$30 per share before the agreement was reached. With that, I believe that the company is worth close to $69-$81 per share. Perhaps any other parties interested in the company would launch new bids.

{kind=link}

The acquisition could also be quite detrimental for NATI in terms of human resources management. Key team members could leave the organization, which could deteriorate future expected results. If the merger does not close, the company may be worth a bit less than that before the transaction was signed.

Among the operating risks that shareholders could suffer, there are the risks from shortages of certain components, lack of supply, or even increase in the price of certain components. Besides, if NATI cannot receive certain components when it is due, longer lead times could lead to lower production levels and lower FCF margins. The 10-K states the following.

Various factors, including increased demand for certain components are contributing to shortages of certain components used in our products and increased difficulties in our ability to obtain a consistent supply of materials at stable pricing levels. The supply shortages have increased the costs and lead times for certain components. Longer lead times may cause a significant disruption to our production activities, which could have a substantial adverse effect on our financial condition or results of operations.

I also believe that NATI could suffer significantly from new tariffs and trade barriers imposed by the United States as well as other countries. As a result, the company may have to pay too much for certain components, which may bring higher costs and lower EBITDA generation. Management offered a certain explanation in this regard. Here's what the company states in the 10-K.

We are subject to various other risks associated with international operations and foreign economies. Our international sales and operations are subject to inherent risks, including, but not limited to tariffs and other trade barriers impacting China or other countries in which we have significant sales.

My Takeaway

Shareholders of National Instruments Corporation are expected to receive $60 in cash for their shares for about 5-8 months. The transaction is expected to close in the first half of 2024. The spread is close to 3%-4% because the company trades a bit below $60 per share. It means that we are talking about annualized returns of close to 6%-8%, which seems acceptable for the deal. The spread is small, but we may be able to buy shares at better prices in the coming months. I believe that there is little risk because the acquirer is larger than NATI, and reports a lot of cash in hand. I also think that the company could be worth more than $60 per share. Using the FCF expectations delivered by the advisor, I obtained a valuation of close to $69-$81 per share. Hence, if the merger does not close, I would keep the shares. There are other parties, who may launch new bids.

For further details see:

National Instruments' M&A Deal: Little Risk, And Acceptable Spread