NATI - National Instruments: Nice Payoff For Long-Term Holders With The Acquisition

2023-10-03 17:09:20 ET

Summary

- National Instruments Corp's financials are mediocre.

- Emerson Electronics is acquiring National Instruments to expand its portfolio and gain a competitive advantage in high-margin products and services.

- National Instruments' financials show below-average performance, but the impending acquisition has rewarded long-term investors.

Investment Thesis

I wanted to take a look at National Instruments Corp’s ( NATI ) financials to see what Emerson Electric ( EMR ) is buying and whether it is a good deal for them. In my opinion, the company's financials are rather mediocre, and I wouldn't buy it, however, Emerson sees it to be beneficial to their operations. There's no point in starting a position here as it is trading at the agreed acquisition price and if you're a current investor, hold on to your shares until the deal is closed later in '24.

Briefly on the Company

NATI is an American multinational company that produces automated test equipment and virtual instrumentation software for engineers and scientists all around the globe. It has a graphical software called NI LabView that helps visualize hardware configurations, measurement data, as well as debugging. The company's TestStand is used for automated tests and measurement applications in the manufacturing area.

The company's products include cables, sensors, power accessories, switch load signal conditioning, instrument control devices, and ethernet interface modules to name a few.

A Little Background

Emerson Electronics is looking to expand its portfolio of offerings and is looking to add NATI’s higher margin end products and services, which will help it achieve a more diversified customer base within highly attractive end markets. The company’s offering $60 a share for the whole company, which at the point of announcement was a 49% premium and that is a nice jump in share price ever since the announcement, which has rewarded long-term investors handsomely.

EMR's previous bid to acquire NATI back in November '22 failed as the two parties did not agree on the price, which was at that time valued at $53 a share. Now that EMR is offering around $60 a share, the two parties are ready to move on and see how this all develops and what kind of synergies this acquisition will help achieve.

I believe this is a great move for Emerson, which looks to expand its portfolio of offerings further with NATI's best-in-class electronic test and measurement products, and other software offerings that Emerson might have lacked in the past. In my opinion, the price is quite steep from where the company traded before all these attempts at a takeover, however, the management of Emerson is going to be playing a long game, which will reward far into the future and make the acquisition bear fruits for a long time, which will be created through efficiencies and higher profitability from higher-margin applications of NATI.

The deal is set to be finalized by the first half of Emerson's fiscal 24.

Financials

As of Q2 ’23 , the company had $139m in cash and equivalents against $564m in long-term debt. The debt figure increased by around $50m since the end of FY22, while cash remained somewhat unchanged. I would like to see the debt figure coming down over time, but it looks like it has been increasing dramatically over the last 3-4 years, which means that the annual interest on debt is going to take away some of the company’s flexibility. So, is this manageable for NATI? Historically, in the last couple of years, the company’s interest coverage ratio stood at around 39x for FY21 and went down to around 10x as of FY22. In the latest quarter, that ratio is now at around 8.5x, which means that EBIT can cover annual interest expense on debt around 8.5 times over. That means it is more than manageable. For reference, many analysts say that 2x is a healthy ratio, while I think it is around 5x. So, it passed both requirements, which means the company is at no risk of insolvency.

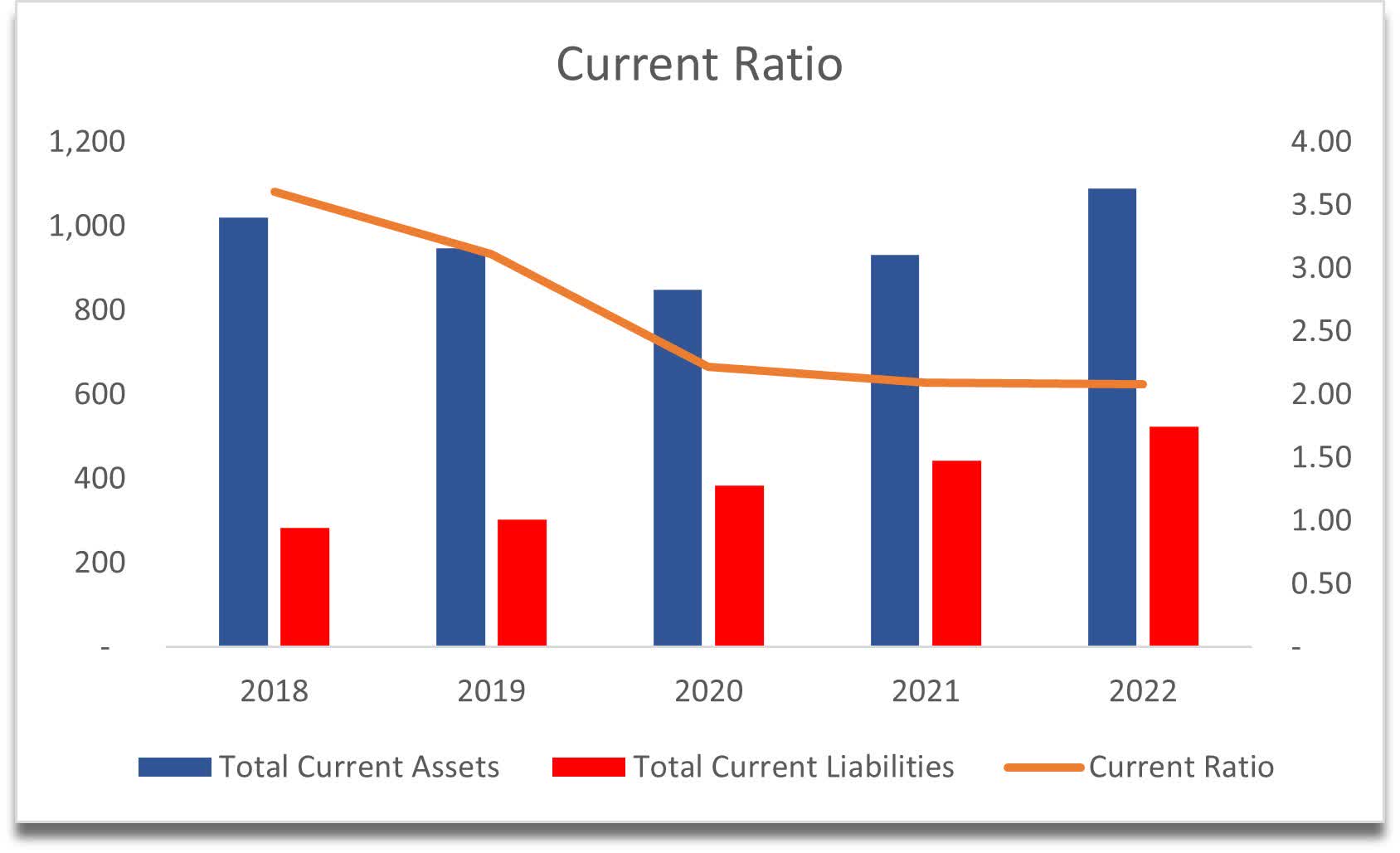

In terms of the company's current ratio, historically, it has been very strong. Strong to the point that it was inefficient in my opinion, as it told me that the company wasn't using its assets very efficiently. However, this ratio has become slightly more efficient each year, which tells me that the management is utilizing its assets like cash to further the company's growth. I would like to see the company’s current ratio to be somewhere in the range of 1.5-2.0, as that strikes a good balance between being able to pay off all short-term obligations and still having enough for growth initiatives.

{kind=link}

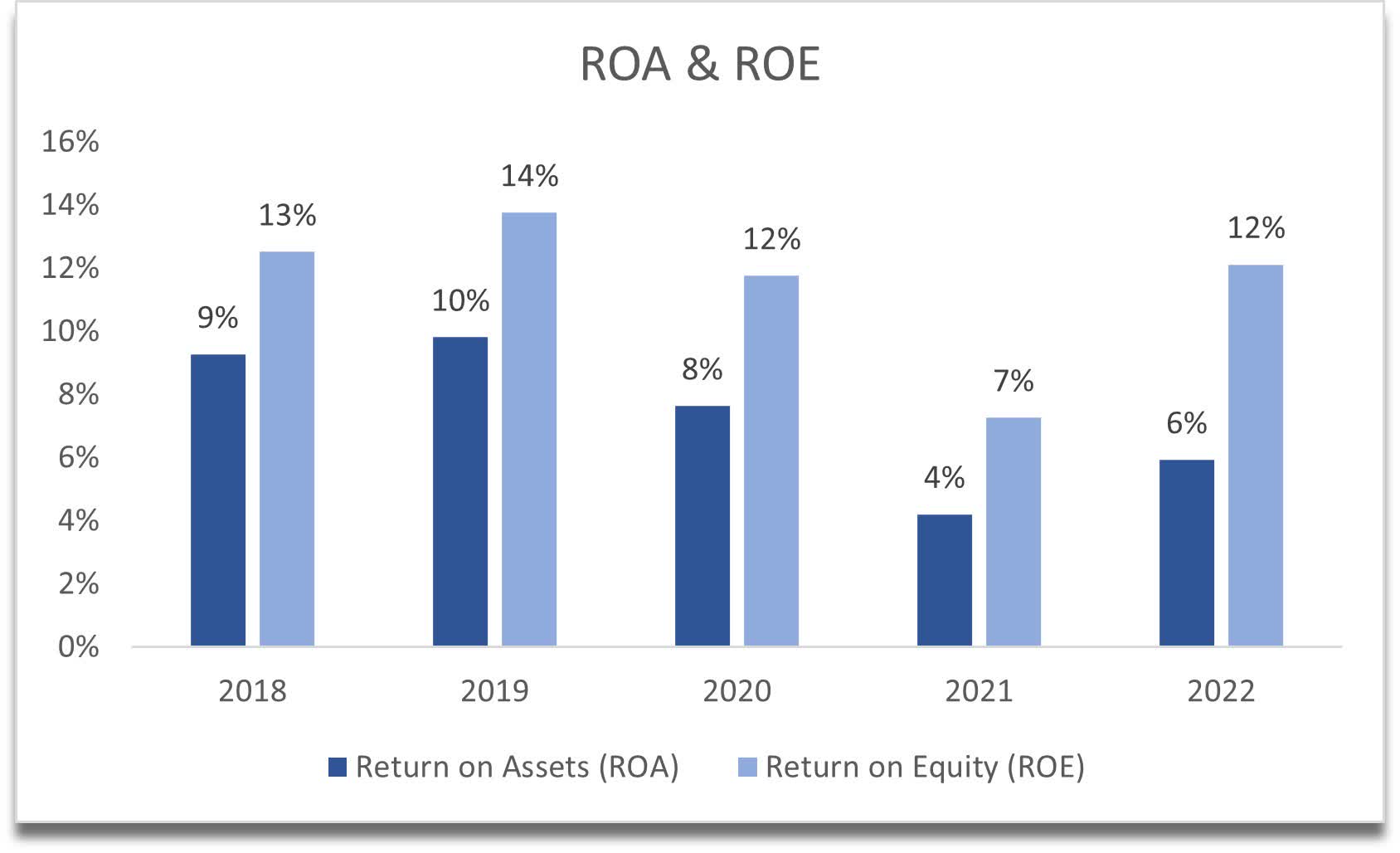

The company's ROA and ROE have seen better days historically, however, these are recovering from the lows of FY21, where the company saw below-average profits that year. These metrics are above my minimum thresholds of 5% for ROA and 10% for ROE. This tells us that the management is quite efficient at utilizing the company's assets and shareholder capital. ROA would have been higher if the company's current ratio had been lower.

{kind=link}

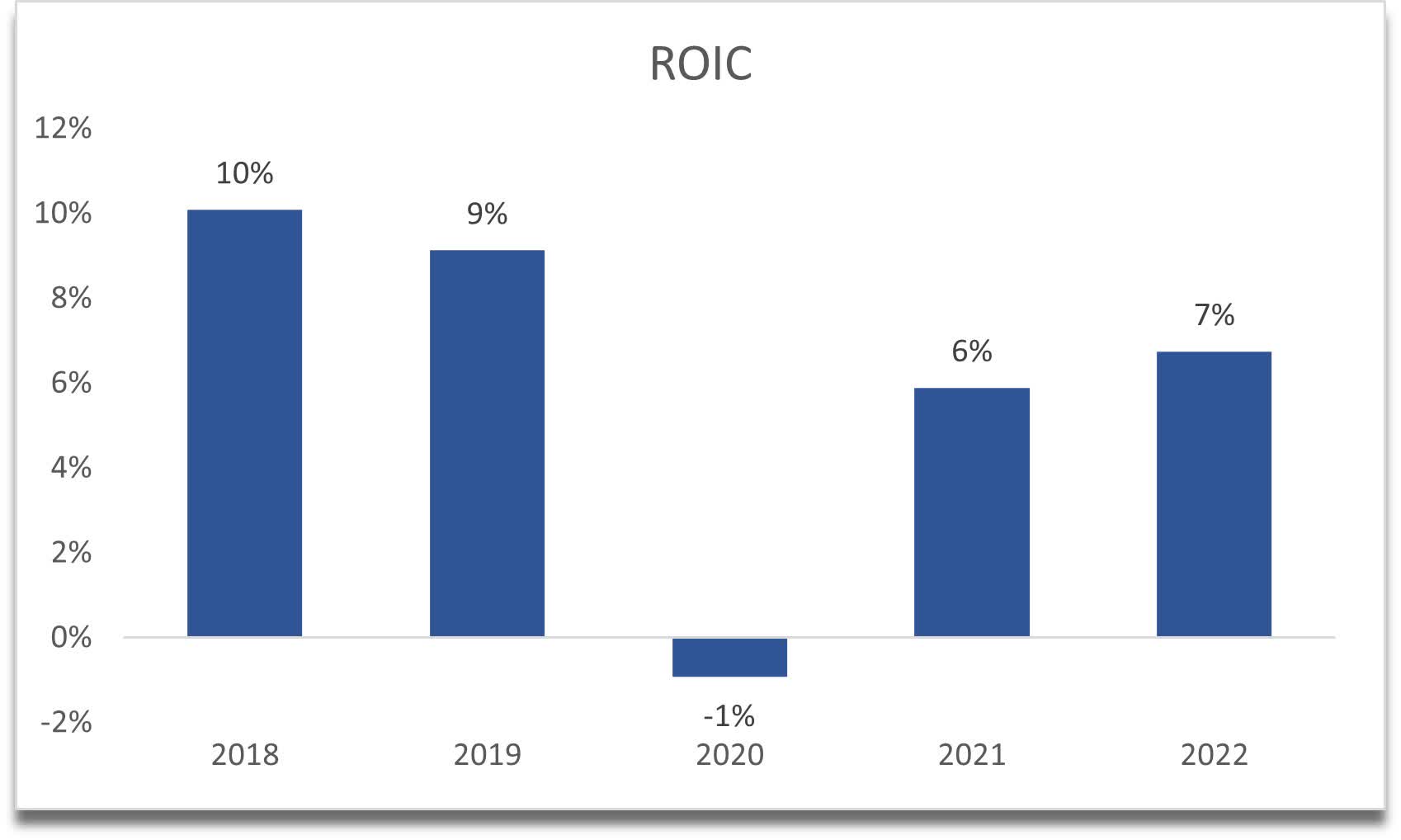

A similar story can be observed in the company’s return on invested capital, or ROIC. In the past, ROIC has been at around 10%, which is the minimum I look for in an investment, however, I do like the fact that it has been going up since the FY20 bottom but hasn’t recovered fully. This tells me that the company might have lost some of its competitive advantage over the years and is trying to regain it, but so far it is still quite a long way to go.

{kind=link}

The company's revenue growth over the last decade has been underwhelming, to say the least. It averaged around 4% over the time while averaging around 13% over FY21 and FY22. I don't think this is sustainable and I am inclined to believe that the company will grow at the company’s 10-year CAGR, but to account for a couple of years of better-than-average growth, I’ll anchor my assumptions a little higher.

{kind=link}

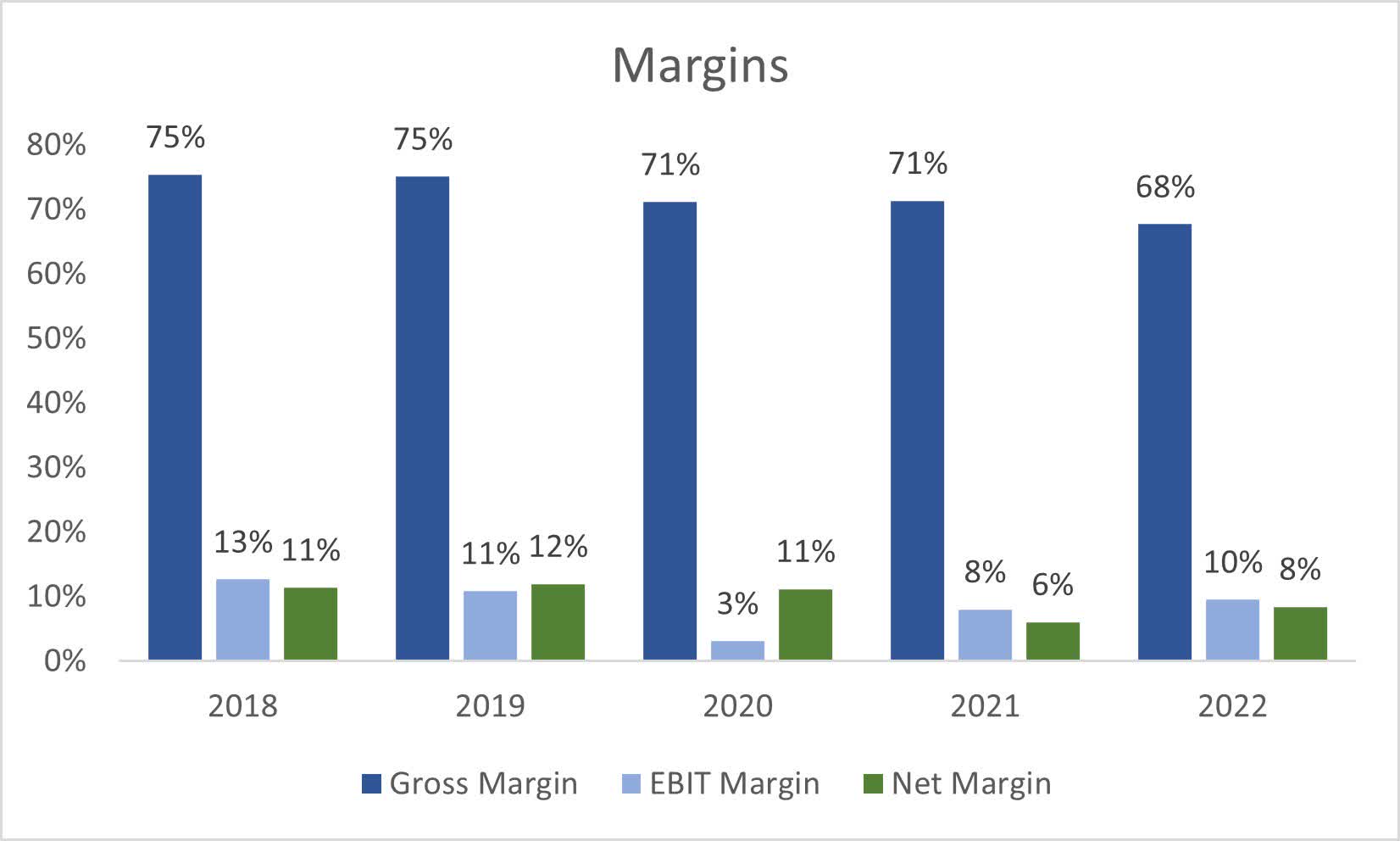

In terms of margins, GAAP margins have slightly deteriorated over the years, which isn’t a good sign. The company became less profitable and efficient, which coincides with the company’s loss of competitive advantage.

{kind=link}

Overall, the company’s financials seem below average, and my requirements aren’t that high. From the financial standpoint, I think that the buyout for NATI was beneficial since the numbers above were deteriorating, and the change of management may be able to turn these numbers back up. If the numbers weren't showing slight dips over the last couple of years, Emerson might have paid even more to own NATI.

Valuation

For the revenue growth for the base case, I decided to be slightly more on the optimistic end, so I went with a 6% CAGR for the next decade. For the optimistic case, I went with an 8% CAGR, while for the conservative case, I went with a 4% CAGR. This way I will get a range of possible outcomes that the company could achieve.

In terms of margins, I decided to use non-GAAP figures as the company seems to be relying on these more than GAAP. Non-GAAP measures exclude the usual culprits like Stock-based compensation, amortization of acquisition-related intangibles and fair value adjustments, acquisition transaction and integration costs, and income tax effects/ adjustment, however, I still do not see a lot of EPS growth over the next decade. I calculate around 8% CAGR of EPS growth for the base case, which isn’t spectacular, around 11% CAGR for the optimistic case, and around 7% CAGR for the conservative case.

The reason I chose to use non-GAAP measures over GAAP is because the company emphasizes these numbers, which in many cases means this is the "true value" of the company. Non-GAAP usually portrays the company in a better light, which can be misleading sometimes, however, seeing what the company excludes it makes sense to use non-GAAP measures. I would prefer to use GAAP measures wherever possible, but if I see that non-GAAP measures do like one-time items, then I will go ahead and use those.

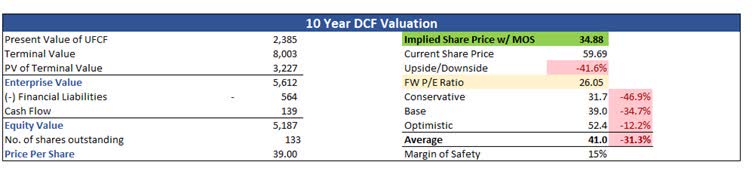

On top of these estimates, I will add a small margin of safety of around 15%, to give myself an extra cushion. With that said, NATI’s intrinsic value is $35 a share, which implies that the company is currently trading at a large premium due to the impending acquisition.

{kind=link}

Closing Comments

It seems that the acquisition is a blessing for all the current investors of NATI because, in my opinion, I wouldn't buy it at $60 a share, but I'm also not buying the whole company to get a better competitive advantage in high-margin products and services.

This deal is more or less in the bag right now for Emerson after the EU and China’s approvals, which is great for the long-term investors of the company. It seems that the company was trading at its fair value before the announcement of the acquisition, which means it’s a win for current investors because if it wasn't for the acquisition, the company would have gone nowhere for a while in my opinion.

I am not recommending to Sell because the deal, as I said previously, is going to go through and current investors of NATI are going to get rewarded quite generously. I am assigning a hold rating because there is no point in anyone starting a new position because the stock price is not going to go anywhere until the deal is done, or for some reason, it doesn't go through (unlikely).

For further details see:

National Instruments: Nice Payoff For Long-Term Holders With The Acquisition