NSRGY - Nestlé: Pricing Is Driving Growth

Summary

- Nestlé's revenues are not suffering from the current macroeconomic problems.

- I expect Nestlé stock to outperform the S&P500 if inflation remains high.

- Nestlé is focusing heavily on offering new healthy products.

The difficulties of the macroeconomic environment are plaguing more or less all companies, but there are some like Nestlé S.A. ( NSRGF , NSRGY ) that manage to remain almost unscathed. The 9M-2022 found positive results overall, and it is thanks to inelastic demand for the products sold. Nestlé is managing to cope with high inflation by increasing the final price of goods sold, but without impacting consumers' purchasing power too much. Regarding the positive pricing effect, here is what CEO Mark Schneider said :

We delivered strong organic growth as we continued to adjust prices responsibly to reflect inflation. The challenging economic environment is a concern for many people and is impacting their purchasing power. That’s why we aim to keep products affordable and accessible while considering the interests of all our stakeholders. Our real internal growth remained resilient despite a high base of comparison and continued supply chain constraints, with limited demand elasticity.

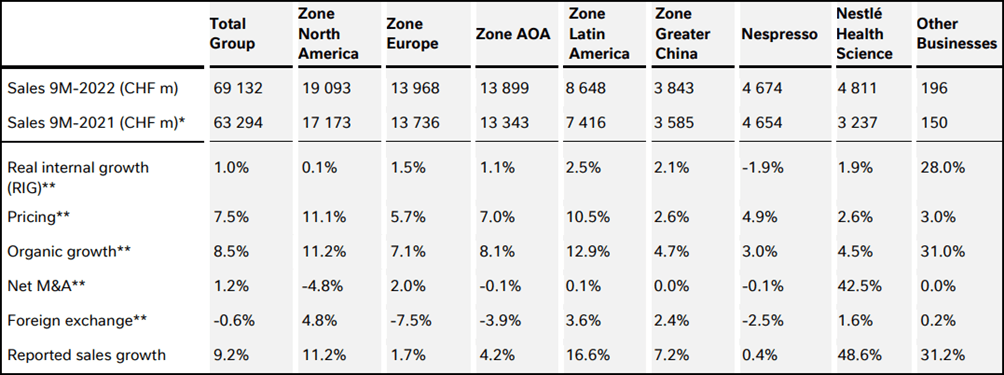

Comparison between 9M-2022 and 9M-2021

{kind=link}

As mentioned earlier, price increases were the biggest factor in this quarterly performance. Total 9M-2022 revenues achieved 9.20% growth, to CHF 69.1 billion versus CHF 63.3 billion in 9M-2021. Organic growth was 8.50%, composed of 7.50% from price growth and 1% from real internal growth. In addition, net acquisitions had a positive impact on revenues of 1.20%, while 0.60% was the loss due to exchange rate.

Zone North America

{kind=link}

North America is the most economically important area, since it is responsible for 27.60% of total revenues. Organic growth was quite high (11.20%) but derived almost exclusively from pricing. With a price increase of 11.10% and real internal growth unchanged, it is clear that demand for the products sold by Nestlé is price inelastic. So, I expect this company's earnings to remain stable even if there are further inflationary spirals in the future. Its earnings capacity has once again proven to be little affected by the macroeconomic environment.

In addition, there was a negative growth impact of 4.80% from the divestment of Nestlé Waters brands and a positive impact of the dollar appreciation against the Swiss franc of 4.80%.

Zone Europe

{kind=link}

In Europe, organic growth (7.10%) was lower than in North America, and the composition is not entirely influenced by pricing (5.70%) but also by real internal growth (1.50%). In terms of total revenues, 9M-2022 achieved 1.70% growth compared to 9M-2021, still registering issues related to an unfavorable exchange rate (-7.50%). The Swiss franc has appreciated significantly against the euro since the beginning of 2022.

Zone Asia, Oceania and Africa

{kind=link}

The AOA zone reported organic growth of 8.10%, of which 7% came from price increases and 1.10% from real internal growth. Sales increased by 4.20% over last year to CHF 13.90 billion, one step away from reaching those from Europe. Once again, the appreciation of the Swiss franc led to a reduction in revenues, about -3.90%.

Zone Latin America

{kind=link}

The Latin America zone experienced a far better result than 9M-2021. Revenue growth was 16.60%, derived from both strong organic growth (12.90%) and a positive exchange rate impact (3.60%). Interestingly, although product prices increased by 10.50%, there was still a real internal growth of 2.50%. In North America, on the other hand, rising prices discouraged consumers from buying more products.

Zone Greater China

{kind=link}

The Greater China zone achieved revenue growth of 7.20%, of which 4.70% was organic. In contrast to the other zones, the pricing effect was limited (only 2.60%) and Covid-19 continues to be a problem due to continuous lockdowns.

Nespresso

{kind=link}

Nespresso achieved rather limited growth, only 0.40%. Although the pricing effect was not very high (4.90%) the real internal growth decreased by 1.90%. Nespresso in the last 9 months has been increasing more and more market share in North America but has reported lower sales in Europe.

Nestlé Health Science

{kind=link}

This segment presented the best growth over 9M-2021, and it was due to the multiple acquisitions made. Nestlé is focusing heavily on offering new healthy products; in fact, three companies were acquired within a few months to revitalize this segment.

- On April 1, 2022, a majority stake was acquired in Orgain, a leader in plant-based nutrition. An option to buy the entire company in 2024 was included in the deal.

- On September 1, 2022, was acquired Puravida, a Brazilian nutrition and health lifestyle brand. This transaction aims to increase revenues from Latin America. On the same date, The Better Health Company was also acquired.

Final Thoughts

Overall, 9M-2022 demonstrated once again how Nestlé is able to generate a steady revenue flow despite the difficulties present in the current economic environment. Its products are essential to millions of consumers, and the company has no difficulty raising prices if inflation rises. Since I consider a global economic recovery unlikely in the short to medium-term given the still-high inflation, I consider Nestlé a buy at least as long as restrictive monetary policy continues to persist.

For further details see:

Nestlé: Pricing Is Driving Growth