NSRGY - Nestlé: Too Much Discounted

2024-01-19 09:22:43 ET

Summary

- Nestlé has a track record of 28 consecutive dividend increases and a 2025 value creation model for all the stakeholders.

- Looking ahead, we positively view the company thanks to volume recovery and cost disinflation.

- Nestlé is trading at a discount compared to the EU Staples. This is not justified. We initiate the company with a buy rating target.

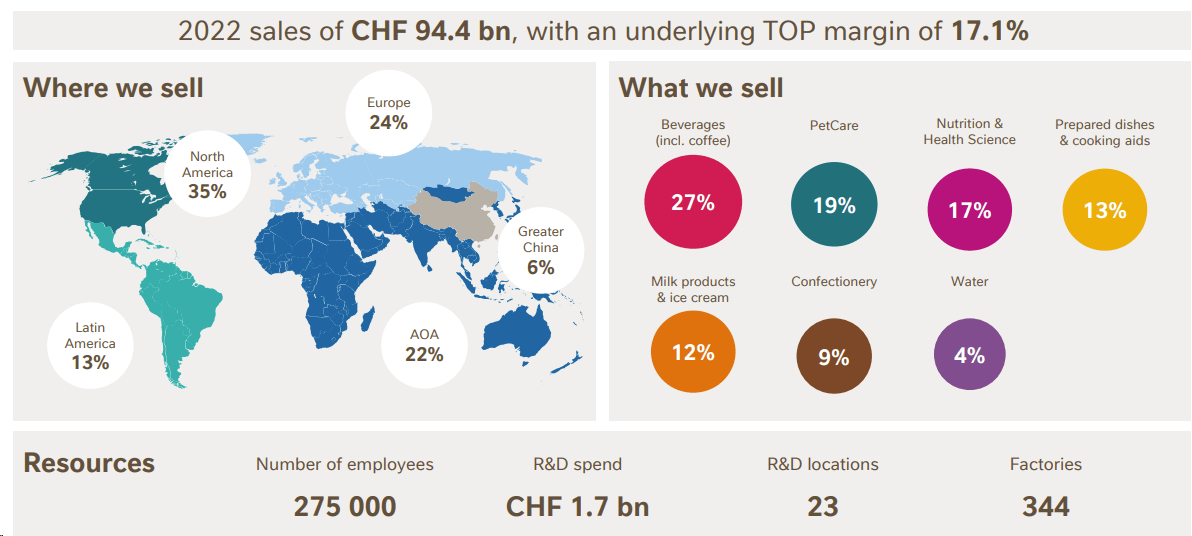

Nestlé ( NSRGY, NSRGF ) is one of the largest global consumer goods companies. Its operations encompass beverages, petcare, nutrition & health science, prepared dishes/cooking aids, milk products and ice cream, confectionery, and waters. Major brands include Nescafé, Nespresso, KitKat, Maggi, and Purina. It operates in approximately 190 countries throughout the world. Beverage and food are core competencies that meet the needs of a modern society looking for high-quality nutrition with an affordable and diversified offering. Nestlé has a track record of 28 years of consecutive dividend increases coupled with CHF 181.3 billion returned to shareholders in the last 15 years, split between buyback (CHF 99.0 billion) and dividend payment (CHF 82.3 billion). Looking back, the company outperformed the Global Stoxx 1800 Food & Beverage Net Return Index by almost 50% in the last ten years and has a 2025 value creation model for all stakeholders. Nestlé's capital allocation priority is set on 1) increasing its dividend per share, 2) maintaining a solid balance sheet, 3) M&A opportunities, and 4) buyback for extra shareholders' remuneration. Supported by a 2025 plan to increase EPS and margins, today, we are looking at Nestlé given the fact that the company trades on 18x 12-month forward P/E (excl l'Oreal) and represents a -15% discount to its 5-year average valuation. Therefore, here at the Lab, we see a favorable entry point for a company that we believe will be a future dividend aristocrat.

{kind=link}

Source: Nestlé’s long-term strategy presentation - Fig 1

{kind=link}

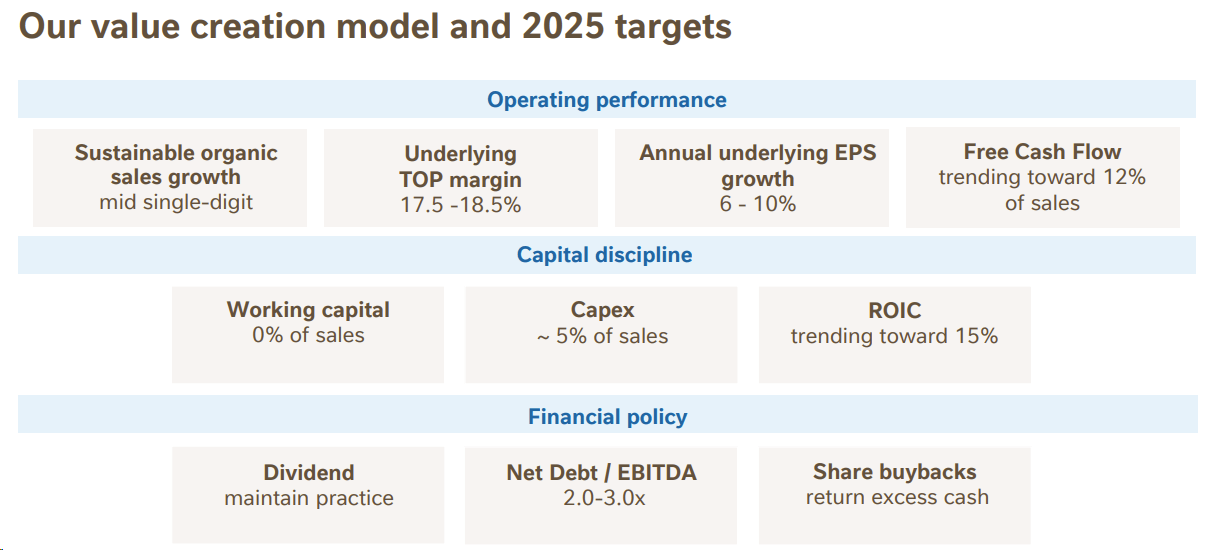

Fig 2

Here at the Lab, our team anticipates organic sales normalization as we anticipate price moderation while we see volumes recover after five quarters of decline. We believe that Wall Street will scrutinize volume trajectory. We also see a solid EBIT margin development, led by the gross margin. These are based on 1) pricing, 2) higher productivity, and 3) savings. We should also start to see an easing in input cost inflation. One of our investment buy thesis is supported by the fact that cost inflation should continue to ease into 2024. That said, the recent spikes in freight rates due to the Red Sea disruption (once again) demonstrate that volatilities remain. Therefore, we prefer companies such as Nestlé with quality margin development, earnings growth projection, and volume sustainability. Here at the Lab, we are also more optimistic about Danone's volume turnaround .

Q4 2023 and FY 2024 Update

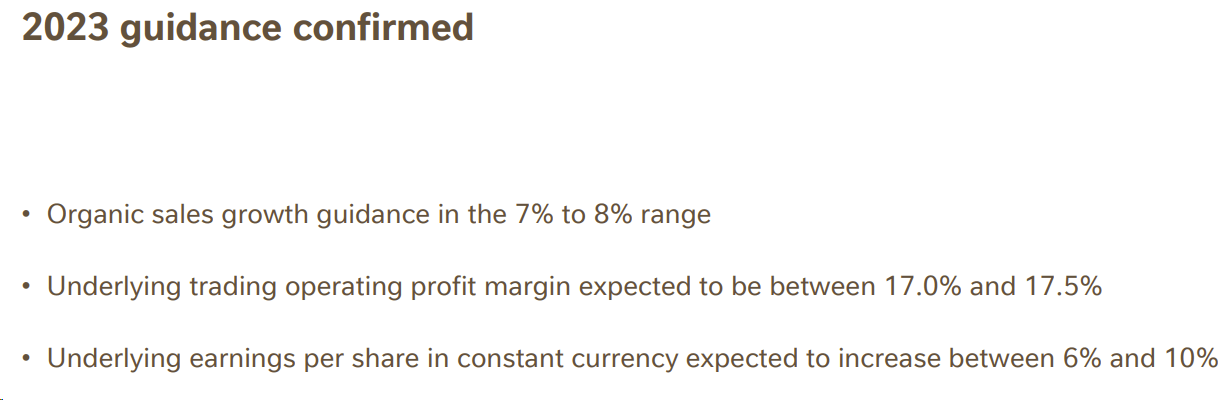

Our team forecast organic sales growth at 6.2%, and we are below Visible Alpha consensus with a +6.8% projection. Our Fiscal Year 2023 sales growth stands at +7.4% and is firmly " within the company's guidance range of +7-8% ".

{kind=link}

Fig 3

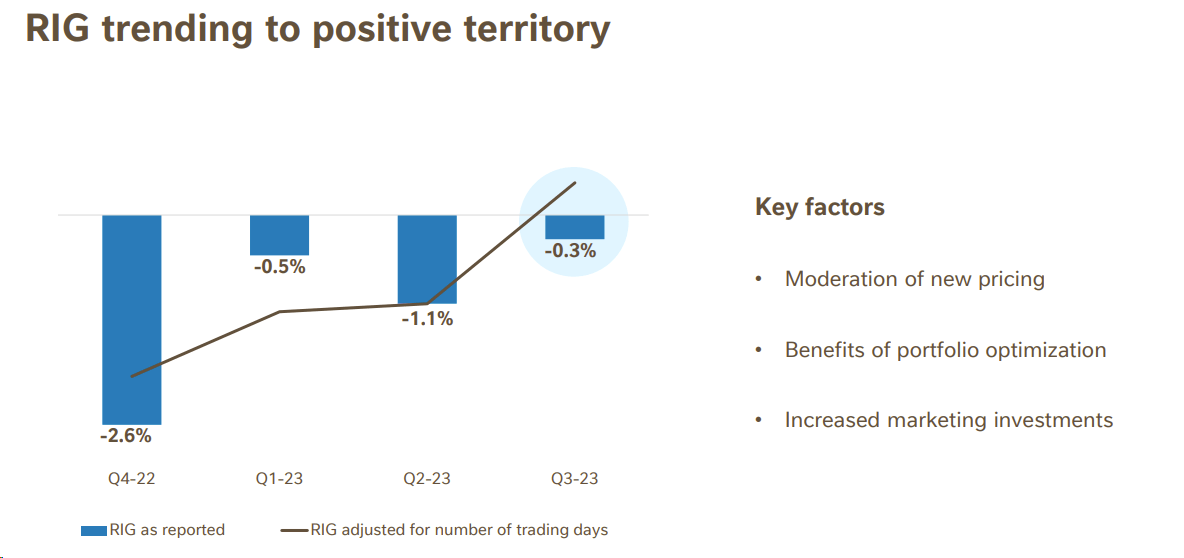

Therefore, Q4 should be an inflection point for the company's real internal growth ((RIG)). At the Lab, we forecast a positive RIG of 1.8% in Q4 after four quarters of decline. At the segment level, we model a negative impact on the Health Science division due to the temporary supply chain constraints.

{kind=link}

Source: Nestlé’s Q3 results presentation - Fig 4

Going down to the P&L, we see an operating margin of 17.5%, higher by 40 basis points compared to last year. This leads to core operating profit at an absolute value of CHF 16.32 billion. In detail, this is supported by an improvement in gross margin in H2 by almost 210 basis points. Our adjusted Fiscal Year 2023 EPS reached CHF 4.94, which is 1% above the Visible Alpha consensus.

Looking ahead, we believe that the company has 2024 optionality:

- Helped by cost disinflation (rather than deflation), Nestlé should benefit from this envelope. Helped by solid pricing power and Petcare expansion, we model organic sales growth of +4.7%. This is made by 2% price and 2.7% RIG. In our estimates, we still expect some pressure from labor costs, cocoa, and sugar. 2024 will be supported by normalization in the price of Arabica coffee beans, and we anticipate resilience in volume in Nestlé's Powdered & Liquid Beverage segment;

- In Q3, there was an IT integration issue in the Health Sciences division. Nestlé's products were out of stock for a couple of weeks. This caused a headwind of 50 basis points of growth. For this reason, we should see a rebound in Q4, and we believe short-term integration implications will cease in early 2024. In our estimates, we project a gradual recovery with an organic sales growth of +6.5% for this year;

- On a high-level consideration, we are cautious of the US consumer while we remain constructive on emerging markets growth. At the moment, the most significant risk is in Europe, with a fragile economy;

-

2023 cost optimization is going to be evident in 2024. By year-end, our team estimated that the company would have cut 25% of their SKUs. In addition, they stepped up their advertising efforts with an extra CHF 500 million budget. These investments heavily focused on their 34 billionaire brands and should begin to show through in Nestlé's product mix;

- Without forecasting acquisition, disposals, and negative one-offs and following the company's target (Fig 2), we arrive at an operation margin forecast of 17.9% in 2024. This is up by 40 basis points and arrive at a core operating profit CHF 16.9 billion. Our Fiscal Year 2024 reached CHF 5.16 and is slightly negatively influenced by the recent update on the currency development.

Conclusion and Valuation

On a downside scenario, the company still has plenty of work to prove in its Health Sciences division. This is set to become a third growth pillar after petcare and coffee. In the company's estimates, this division will likely provide much better returns and margins. Based on our forecast, Nestlé's EPS increases by 4.5% every year while we see the overall market struggle to deliver earnings growth. For this reason, as already reported, we believe this Staples discount is unjustified. On average, the European staples' P/E valuation is approximately 21x. Given its high quality and earnings profile, we believe Nestle should trade at a premium. Even applying the same P/E target multiple, we derive a valuation of CHF 109 per share vs. a current target price of CHF 98. Aside from the Health Sciences division and FX risks already included, we should say that Nestlé’s profitability is derived from consumer variances and is subject to consumer confidence and income. Additional risks include prolonged weakness in the coffee & petcare categories, higher interest rates, and lower-than-expected volume recovery.

For further details see:

Nestlé: Too Much Discounted