NSRGY - Nestle Is Still Trading With A Slight Premium

Summary

- Nestle is reporting high growth rates, with all categories contributing to organic growth.

- Management is optimistic that Nestle can return to the path of growth, and considering the looming recession, the company might also be a good pick.

- But the stock is still slightly overvalued and not a good investment, in my opinion.

About a year ago, I published my first article on the Swiss food and beverage behemoth Nestle S.A. ( NSRGY ). I called the company the leader in the food and beverage industry, but in my conclusion, I did not consider it being a great investment at that point and finished the article with the following conclusion:

Without much doubt, Nestlé is a solid business, which existed for over 150 years and has a wide economic moat around its business. And although Nestlé is also market leader, there might certainly be better picks right now. The problem: Even if we assume that Nestlé will be able to grow with a high pace in the years to come, the stock is still overvalued. And considering the performance of the past decade, I remain skeptical if Nestlé can grow earnings per share in the high-single-digits in the years to come.

When my last article was published the stock was trading for CHF125. Now it is trading for CHF113, and it is now rather close to the intrinsic value of CHF106 I calculated in my last article. Hence, we might be tempted to could call Nestle more or less fairly valued at this point. In the following article, we take a closer look at the company once again and answer the question if it is a good investment now.

Quarterly Results

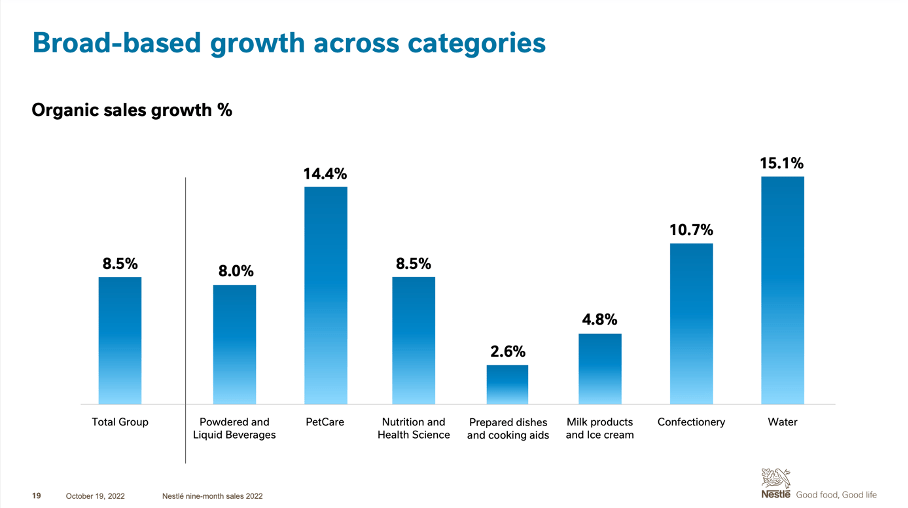

We start by looking at the last results for the company. Nestle - like many other European companies - is only reporting annual and half-annual results and is providing only very limited data for Q1 and Q3 (it usually offers no financial statements). However, Nestle is still reporting some numbers for the first nine months of fiscal 2022. Total reported sales increased 9.2% from CHF63.3 billion to CHF69.1 billion - resulting in a reported growth of 9.2% year-over-year. Organic growth increased 8.5% in the first nine months with pricing contributing 7.5% to that growth. And while all seven categories contributed to organic sales growth, prepared dishes and cooking aids grew only 2.6% while Water increased 15.1% and PetCare also increased 14.4% year-over-year.

{kind=link}

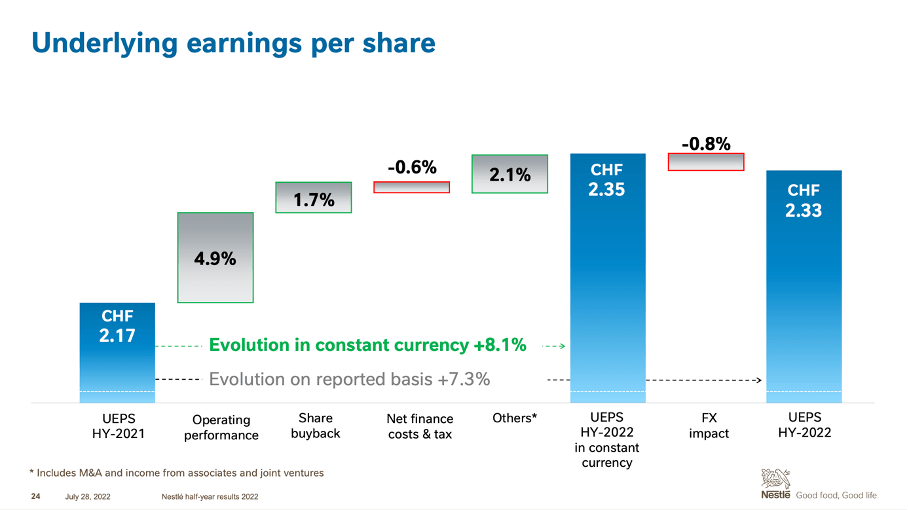

Additionally, we are looking at the half-year results to get a few more information. While sales increased from CHF41,755 million in H1/21 to CHF45,580 million in H2/22 - resulting in 9.2% year-over-year growth - operating profit declined slightly from CHF6,866 million in H1/21 to CHF6,619 million in H1/22. And while operating income declined 3.6% year-over-year, earnings per share declined even 9.4% year-over-year from CHF2.12 to CHF1.92. However, underlying earnings per share increased 7.3% year-over-year from CHF2.17 to CHF2.33.

{kind=link}

For the full year 2022, management is now expecting organic sales growth around 8% and underlying earnings per share in constant currency are expected to increase (but management is not providing any numbers).

Returning On The Path Of Sustainable Growth?

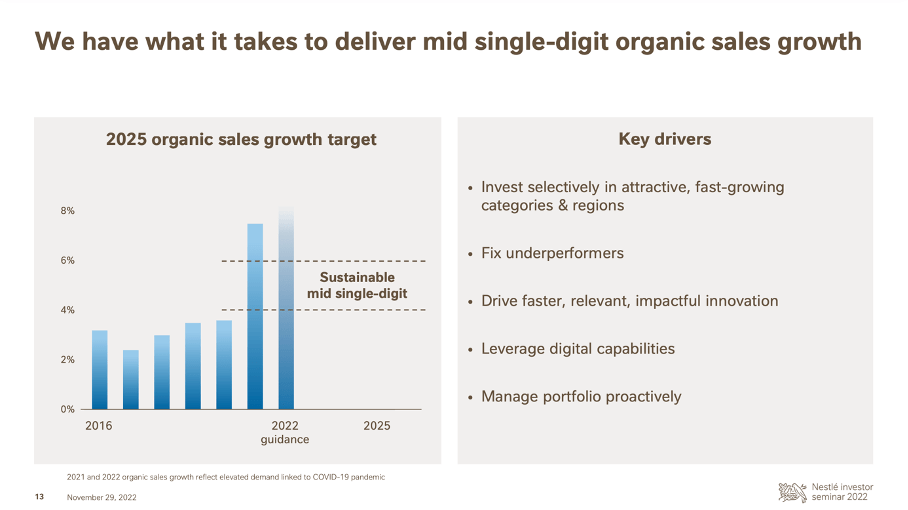

In November 2022, Nestle hosted its Investor Seminar and provided investors with further information on how Nestle is expecting to grow in the years to come. And management seems to be very confident that Nestle has what it takes to grow organic sales in the mid-single digits in the years to come. Not only will the company try to focus on its underperformer and try to improve the performance but it will also focus on faster innovation and try to leverage digital capabilities. And all these strategies combined should lead to solid growth rates.

{kind=link}

And management is not just focusing on driving topline growth but also on increasing efficiency and the company's margins. Key drivers will be the focus on cost efficiencies and actively managing the company's portfolio. But Nestle will also try to premiumize product offerings. And when summing up the different strategies, Nestle is expecting sustainable, organic sales growth in the mid-single digits. In combination with margin improvements for the years to come, Nestle is expecting annual underlying EPS growth to be between 6% and 10% in the next few years.

{kind=link}

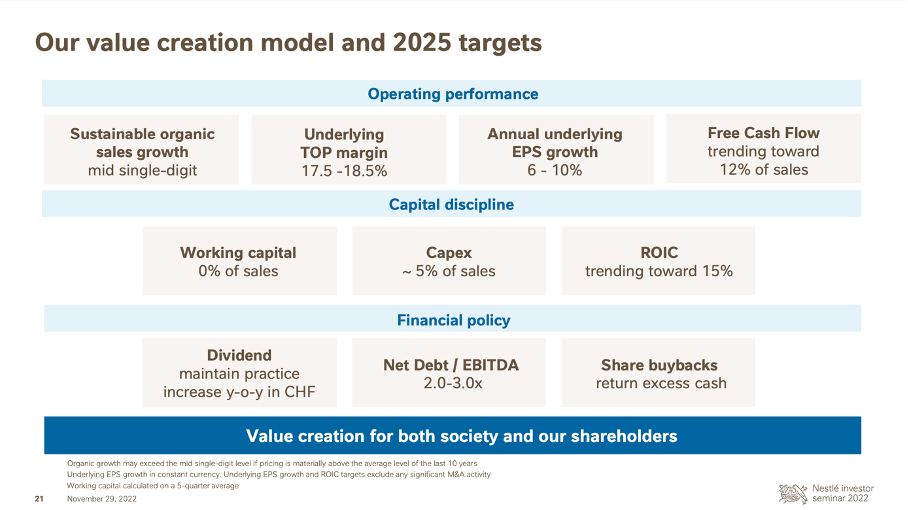

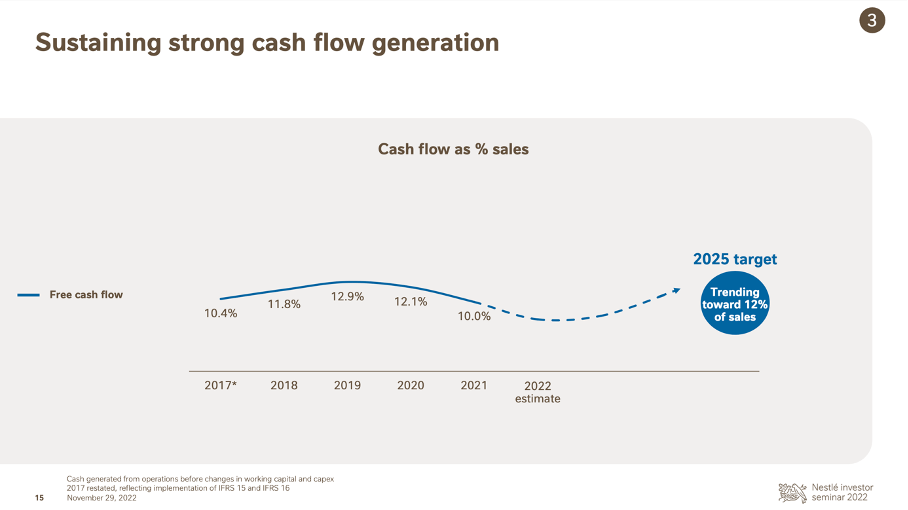

And when looking at free cash flow, the company is expecting strong cash flow generation. The company's 2025 target is to achieve 12% of sales ending up as free cash flow, which is clearly above the numbers in the last few years - but not unrealistic as Nestle could achieve similar rates in previous years.

{kind=link}

Recession Resilient

When you read some of my past articles you know I am one of the investors expecting a recession in 2023 (as several early warning indicators are pointing in that direction). And there is another argument to be made in favor of Nestle. In my last article I did not really focus on Nestle being rather recession-resilient but considering the looming recession it is worth mentioning.

As Nestle is selling food and beverages, we can assume a more or less stable performance in the coming quarters. Even during economic challenging times, people must drink and eat and will continue to purchase these products. One might argue that Nestle is selling branded products (which are more expensive) and in economic challenging times customers might switch to low-cost alternatives. And while this is certainly a risk, I am not so sure how many customers will actually switch. Many of the products Nestle is selling only cost a few dollars (and sometimes even less than a dollar). By switching to low-cost alternatives, customers might save just a few cents, but the taste might be different. I would assume that many customers will rather try to save money in different ways.

And when looking at the performance in previous recessions, it is not like Nestle did not react to economic challenging times. However, the company's performance was quite stable. When looking at the years 2000 till 2003 (following the Dotcom bubble), revenue as well as earnings per share increased almost every year. Only in 2003, we saw declining numbers, but declines were moderate. And during the Great Financial Crisis, revenue declined only in the single digits and I would also argue that earnings per share were rather stable - at least when comparing 2009 to 2007 (the year 2008 was a positive outlier for Nestle). And in 2020 - during the COVID-19 crisis - revenue also declined in the single digits, but earnings per share were kept stable.

All in all, I would argue for Nestle being quite stable during recessions. The company will see some negative impacts but compared to many other businesses we should not really worry about the performance of Nestle during recessions.

Dividend and Share Buybacks

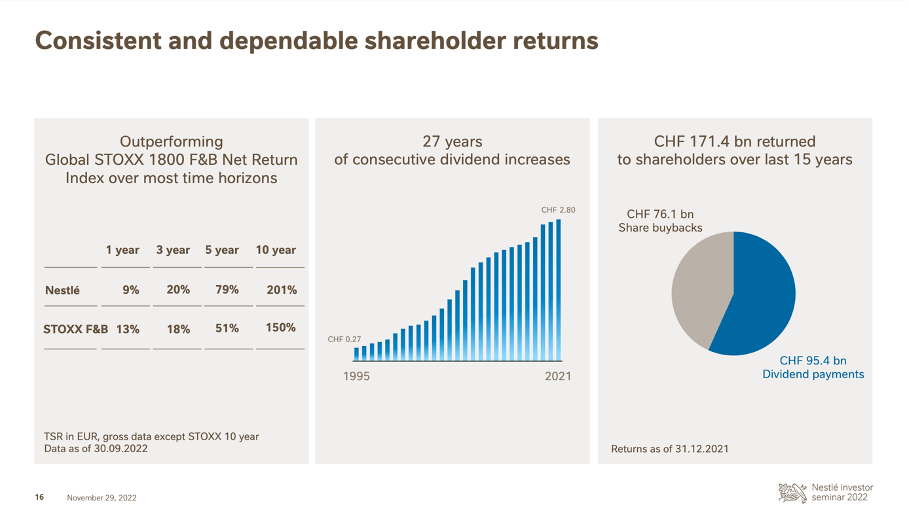

Although Nestle has "only" a dividend yield of 2.5% right now, it is worth mentioning that Nestle is one of the few European dividend aristocrats. Like many major U.S. corporations, European companies also focus on paying dividends but compared to its U.S. peers, European companies don't focus so much on increasing the dividend every single year. And especially during economic crisis, it is not untypical that European companies keep the dividend just stable (or even cut the dividend).

And when keeping that information in mind, Nestle is rather an outlier with 27 years of consecutive dividend increases . Since 1995 Nestle did not only increase the dividend every year but also with a solid CAGR of 9.5%. And while Nestle could not increase the dividend every single year since 1959 it was paying at least a dividend every single year.

{kind=link}

And as I already mentioned in my last article, Nestle announced a share buyback program in December 2021. The share buyback program will have a volume of CHF20 billion and is due to be completed by the end of December 2024. Nestle used share buybacks before and since 2005 it issued several share buyback programs.

Intrinsic Value Calculation

In my last article, I argued that Nestle was still a bit overvalued. Right now, Nestle is trading for a P/E ratio of 18.5 and this is not only one of the lower P/E ratios in the last ten years but also clearly below the average P/E ratio of the last ten years (24.48). And a valuation multiple close to 20 seems neither extremely high nor extremely low and might support the thesis that Nestle is fairly valued at this point.

When looking at the price-free-cash-flow ratio on the other hand we see Nestle currently trading for 43 times free cash flow. And that is not only above the 10-year average (which is 26.53) but it is also an extremely high P/FCF ratio and a multiple that can hardly be justified.

So, we a torn between a reasonable P/E ratio and an extremely high P/FCF ratio. In such a case, a discount cash flow calculation makes sense as it could help us to determine an intrinsic value and make the decision if Nestle is fairly valued or not. And let's be a little bit optimistic and assume Nestle will reach its target of 12% of sales ending up as free cash flow. This leads to about CHF11 billion to CHF11.5 billion in free cash flow as basis for our calculation. And let's assume once again that Nestle can grow 8% annually for the next ten years followed by 6% growth till perpetuity. These are not just the same assumptions as I used in my last article, 8% growth for the next few years is also in line with Nestle's targets for the next few years. And when calculating with a 10% discount rate and 2,750 million outstanding shares we get an intrinsic value between CHF115 and CHF120 and Nestle would be slightly undervalued at this point.

We can argue that 8% growth is the mid-point of Nestle's 2025 targets and must be seen as realistic. However - as I also pointed out in my last article - this growth rate might be a little too optimistic. When looking at past growth rates, Nestle could report a CAGR of 7.43% for earnings per share in the last ten years and therefore I feel a little uneasy when calculating with growth rates of 8% for the next ten years. I would rather calculate with 7% growth or maybe only 6% to be on the safe side. And when calculating only with growth rates of 6% for the next ten years as well as till perpetuity we get an intrinsic value of CHF103.64 and Nestle is still a bit overvalued.

And not only did we calculate with a rather optimistic growth rate for the next ten years, but we also assumed that Nestle will reach its 12% of sales ending up as free cash flow target already in 2022. But we must assume that free cash flow in 2022 and 2023 might be lower - which will also have an impact on the intrinsic value.

Conclusion

Although Nestle seems to be a little cheaper than a year ago, I would still wait for Nestle to fall at least below CHF100 before I would consider the stock being interesting and a potential investment. Right now, the stock is a clear hold (for existing shareholders), but I would not buy the stock or add to an existing position.

For further details see:

Nestle Is Still Trading With A Slight Premium