NSRGY - Nestle: RIG Growth In 2022 Signals It's Time To Buy

Summary

- Nestle demonstrated real pricing power in 2022, as it's one of very few staple companies that were able to grow sales in terms of mix and volume.

- After years of 'Diworsification', Nestle's management is focused on profitability, ROIC, and risk-adjusted growth.

- The company's portfolio of brands is in a league of its own when it comes to the consumer staples industry.

- It's not a potential ten-bagger, but Nestle should be cornerstone in any long-term dividend investor's portfolio.

Nestle ( NSRGF ) ( NSRGY ) is the best of the best in the consumer staple industry. Its portfolio of diversified brands is unlike any other. After a few years of supply chain issues, unsuccessful acquisitions, and worsening margins, Nestle's management is focused on improving efficiency, portfolio optimization and ROIC. The near-term looks bright with all those initiatives expected to come to fruition and result in top-of-the-industry growth. Yet, Nestle's current dividend yield is 2.69%, which is above its 4-year average of 2.49%. Also, Nestle is trading for a slightly lower P/E ratio than its industry average. I believe Nestle should be trading at a premium, and based on my DCF model, I estimate the fair value of the stock at CHF 119 per share, or $130 per share of the company's ADR. This represents a 9.0% upside compared to its market price at the time of writing, and due to its quality, I rate Nestle as a Buy.

Company Overview

Nestle operates as a nutrition and beverages company worldwide. The company is based in Switzerland and manufactures, sells, and distributes powdered and liquid beverages, water, milk products and ice cream, nutrition and health science products, prepared dishes and cooking aids, confectionary products, and pet food. Nestle's portfolio of brands include Gerber, San Pellegrino, Nesquik, Cheerios, Lion Cereal, KitKat, Toll House, Nescafé, Nespresso, Perrier, Nestea, Häagen-Dazs, Purina and many more. In addition, Nestle owns a 20.1% ownership stake in L'Oréal ( LRLCF ).

Nestle is the largest food & beverages company in the world in terms of sales. In 2022, Nestle sold goods to the amount of $100B, while PepsiCo ( PEP ) and Procter & Gamble ( PG ), the second and third largest companies, reported sales of $86B and $80B, respectively.

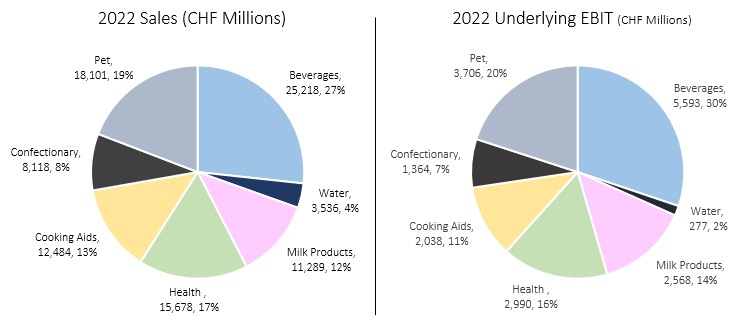

Nestle's product portfolio is diversified, with no product category amounting to more than 30.0% of the company's sales or profits:

Created by author using data from Nestle's financial reports

{kind=link}

The company's growth is broad-based, with every segment seeing organic growth in 2022:

Nestle's 2022 Investor Presentation

It's clear Nestle's business is recession-proof and timeless. The company will most likely still be here to pay dividends to our grandkids.

Investment Thesis - Real Proven Pricing Power

Inflation was the main theme in 2022, and it seems like it's not going anywhere. Markets are fluctuating up and down in response to every small sign of change in trends. Every major consumer staple company have seen its margins shrink due to significant rises in commodities like corn, soybeans, energy, wheat, plastic and more. During times of inflation, companies in the consumer staples category are trying to mitigate the damage with price increases, putting their customers' loyalty to their brands to a test. While many companies in the industry were able to grow their total revenues, most of them have seen volumes and mix go down, meaning their customers are either buying less products or trading down, or both. This is a great natural experiment for investors - which companies really possess pricing power and brand loyalty, and which companies are leaking out customers to competitors.

The way I see it, Nestle have passed the experiment successfully. In 2022, Nestle achieved 8.3% organic sales growth, as a result of an 8.2% price increase and a 0.1% real internal growth (which is a combination of mix and volume). Although it looks small, let's list some very well-known consumer staple companies who weren't able to accomplish the same. Procter & Gamble reported 2.5% revenue growth in CY22, with an average decrease of 4.0% in RIG per quarter. Unilever ( UL ) reported 9.0% underlying sales growth for the year but saw a decrease of 2.1% in volumes. For CY22, General Mills ( GIS ) reported an average organic growth of 8.0% but saw an average decrease in volumes of 7.5%.

So, we can see Nestle's pricing power and quality of brands stand out. This is even more impressive considering the company's growth in recent years, it already being the largest food producer in the world, and the fact that RIG was hurt from China lockdowns and divestitures:

Nestle's 2022 Investor Presentation

Overall, Nestle's 2022 numbers prove to me that Nestle has real pricing power. As the largest consumer staple producer in the world in terms of sales, with more than $100B in revenues in 2022, I find pricing power to be extremely valuable for the company. Investors can be resting assured knowing that even in times of economic pressure, customers are continuing to buy Nestle's products, and the company is able to maintain its huge share in the market. In my opinion, this is a testament for the company's ability to remain a long-term leader.

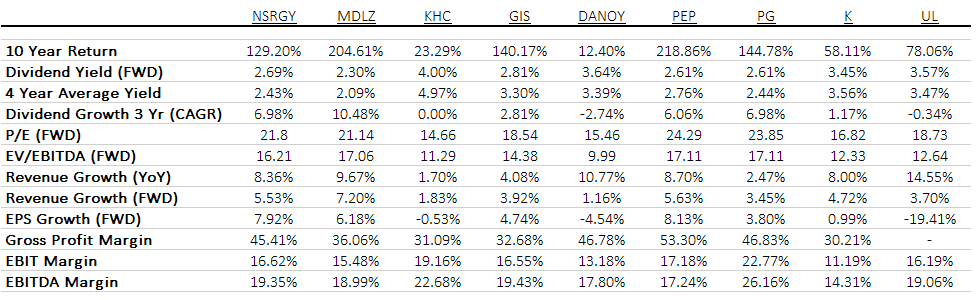

Competitors, Multiples & Dividends

As a mature food & beverages company, Nestle isn't going to provide greedy investors with 10X or 5X returns. However, Nestle can provide long-term dividend investors with constant dividend increases and reliable capital appreciation over time. The company has increased its dividend for 28 consecutive years, and recently announced another 5.0% increase. Looking at Nestle's valuation and results compared to its peers, I find its current price and position to represent a buying opportunity.

Created by author based on data from Seeking Alpha; Data as of February 21st, 2023.

{kind=link}

Nestle is trading at a slightly higher P/E than its peers average, but its expected EPS and revenue growth are at the top tier. Nestle's gross margin reflects the quality of its brand portfolio, and the EBIT & EBITDA margins are showing there's room for better efficiency. Nestle's management set a 2025 target of 17.5%-18.5% trading operating profit margins, which reflects a 3.5 points increase from 2022. If management will achieve this goal, and I believe they will, through portfolio optimization and efficiency initiatives, then we're talking about industry leading margins, industry leading sales and industry leading growth. To me, this all comes for a fair and attractive price.

Valuation

Nestle is no different from its other high quality consumer staple peers in the sense that investors find their valuations at the high range. I find Nestle to be the highest quality in the industry and therefore, I believe it is slightly undervalued. Waiting for a stock like Nestle to go down materially could be a disappointing endeavor, especially because there's a lot of growth opportunities in the near term.

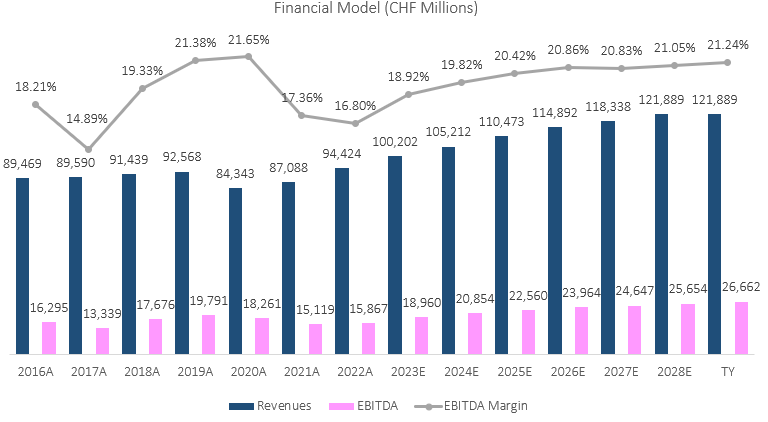

I evaluated Nestle's fair value using the discounted cash flow methodology. I assume Nestle will see revenues grow at a CAGR of 4.35% between 2022 -2028, which is at the low end of the company's long-term guidance for organic growth, which was provided on its latest investor seminar . I believe revenues will grow at this above-industry pace due to Nestle's significant investments to increase capacity, mainly in its PetCare segment.

I project EBITDA margins to increase incrementally up to 21.24%, which is slightly below its 2019 level. This results in an EBITDA CAGR of 8.34% between 2022-2028. This aligns with management's expectations for earnings growth, taking into account that depreciation is expected to increase as a consequence of the company's increased investments. I base my EBITDA projections on the company's portfolio optimization initiatives, targeted price increases and the probable easing of cost inflation.

Created by author based on Nestle's financial reports and author's projections

{kind=link}

An important aspect to take in mind when evaluating Nestle is working capital. Nestle's production chain is one of the best in the industry. Historically, the company's working capital rate is around 2.6%, essentially meaning Nestle's customers are covering the cash payments to its suppliers back-to-back. However, in 2022, the company intentionally decided to stock up inventories, mainly energy and some other commodities in response to the Russian-Ukraine war. Therefore, Nestle's free cash flow in 2023 is expected to benefit from a one-time working capital inflow, after 2022 experienced the opposite.

Taking a WACC of 7.53%, I estimate Nestle's fair value at CHF 119 per share, which equals to $130 per share of the company's ADR. This represents a 9.0% upside compared to its market price at the time of writing. While this does represent an arguably high forward P/E ratio of 23.7, the E in the equation is expected to increase significantly through margin improvements in the near future. Therefore, I believe now is a good time to buy Nestle, and patiently let the growth in earnings and dividends provide a very decent, stable total return.

Near Term Projections

I find it important to provide additional details regarding my near-term financial projections in order to provide both the readers and me the ability to measure the accuracy of the investment thesis. This allows me to easily assess whether an earnings report is good or bad, and what adjustments I have to make in my model.

For the first half of 2023 I forecast Nestle will report CHF 48.4B in sales which is at the mid-point of the organic growth guidance, CHF 22.5B in gross profit, and CHF 6.1B in net income. The consensus numbers are sales of CHF 47.2B, gross profit of CHF 21.9B and CHF 6.3B in net income. As you can see, I'm more bullish than the consensus regarding the sales figure, but more bearish when it comes to the margin improvements. I should say that I project a more significant improvement in the second half, based on what management said during earnings:

[...] We do confirm that this program will have a positive impact on RIG and OG for the full year 2023, but it will have a negative impact in the first part of the year.

--- François Roger, EVP & CFO, Nestle's 2022 Earnings Call

Overall, I expect 2023 to be a great year for Nestle, with more signs of its cost reduction initiatives coming to fruition. However, the material improvement, as well as the contribution of its capacity enhancements, will come in 2024.

Risks

When talking about a company like Nestle, I find it unnecessary to address the general macro-economic risks. Those risks are clear to investors and Nestle is somewhat of a safe haven when it comes to deteriorating macro-economic conditions. Additionally, regarding forex, as I do not see myself as a forex expert, I'll just say Nestle is so geographically diversified, I wouldn't worry about forex when considering investing in the company.

Nestle's growing leverage is a bit more worrisome. The company's net debt increased to CHF 48.2B, compared to CHF 32.9B last year. The increase is a result of cash outflows to pay for share buybacks, dividends, and M&A, and it was offset by lower than usual free cash flows as discussed above. Even though the increase is significant, I wouldn't say it's alarming. Nestle's net debt to EBITDA ratio is still a healthy 2.45X. With EBITDA expected to increase and Nestle's track record, I believe Nestle's leverage is reasonable.

Another cause for concern is Nestle's bad acquisitions in recent years. Management has already admitted buying Palforzia, the peanut allergy treatment, was a mistake. In addition, the company recently shut down its frozen food business in Canada, which was unsuccessful. While ' Diworsification ' is definitely a risk for large mature companies like Nestle, I believe its management learnt from its mistakes and will be very cautious in future M&A.

We were probably at the time, a bit more reluctant to take these hits on volume rig and organic growth. And as a result of that, we were cranking up innovation a lot and had a nice new stream of innovative products coming to market. What got our attention initially was the supply chain constraints. We had to make choices like how do you use limited resources to make either one product or another. But then once we saw the tremendous benefits from that, we saw that there is a significant opportunity here to do more and really played a win as opposed to just play to have another SKU on the shelf and focus profitable growth. That's essentially what we're after. So that will include some further SKU items but that will also include some divestitures over time so that we are even more focused. We will continue as a multi-category diversified food and beverage company, no question. But we believe that the company overall within that broader scope will benefit from even more focus than before.

--- Mark Schneider, CEO, Nestle's 2022 Earnings Call

Similar to bad acquisitions, it is a legitimate worry that Nestle's investments to enhance its production capacity in its PetCare segment will prove to be excessive, resulting in overcapacity. Management addressed that concern:

We are a little bit the victims of our own success here because, as Francois pointed out, this is now the third consecutive year of double-digit growth. And we were even close to capacity limits before COVID and had started to greenlight some of the capacity enhancement programs then came COVID and that huge surge in pet adoption and demand, and this is something that no 1 had on the radar screen. I'm not so concerned about the eventual overcapacity because we've done, as you can imagine, on major CapEx items here [...] lots of projections about how things could turn out. And even if there is a little bit of overcapacity temporarily, it was very clear that with the underlying growth, which is so much intact, you will very quickly grow into it.

--- Mark Schneider, CEO, Nestle's 2022 Earnings Call

Lastly, some investors are worried about Nestle's future growth prospects. While it would be nice to see Nestle growing revenues by double digits, expectations should be reasonable. Taking its size into account, Nestle's growth prospects are quite high compared even to smaller peers. As I laid out above, I believe Nestle's future is bright, and its current price doesn't reflect high expectations for growth acceleration.

Conclusion

Nestle's 2022 RIG growth proves the company's unparalleled quality. While many of its smaller peers saw customers responding to their price increases by trading down or buying less, Nestle was able to keep its RIG positive. Even though 0.1% RIG growth is a small figure, Nestle managed to achieve it despite an 8.2% price increase, supply chain issues, China lockdowns and a few divestitures. Even as the largest consumer staple producer, Nestle is still expected to grow in line with the smaller and faster growing companies in the industry. Based on a multiple comparison and a DCF analysis, I find Nestle to be trading below its fair value, which I estimated at CHF 119 per share (or $130 per ADR). Therefore, I rate Nestle as a buy, and believe long term investors will enjoy a very steady and reliable total return if they add Nestle to their portfolio.

For further details see:

Nestle: RIG Growth In 2022 Signals It's Time To Buy