CA - New Gold: Another Solid Quarter With Higher Free Cash Flow On Deck

2023-12-25 23:10:19 ET

Summary

- New Gold exceeded production guidance and had positive free cash flow in Q3, a welcome improvement after years of free cash outflows and missed guidance.

- Meanwhile, development at C Zone and Rainy River Underground continues to track in line with schedule, setting up a very strong several years ahead starting in 2025.

- In this update, we'll dig into the Q3 results, recent developments, and where the stock's updated low-risk buy zone lies:

While it was a mixed year operationally for the precious metals sector (GDX) with several companies missing on cost estimates like Jaguar Mining (JAGGF), IAMGOLD (IAG), and Hecla Mining (HL), New Gold (NGD) has been one Tier-1 jurisdiction producer to exceed estimates, tracking to the high end of production guidance and the low end on costs. This is certainly a welcome development after a long stretch of underperformance and struggling to consistently hit guidance, and the solid performance was reflected in its financial results, with ~$100 million in operating cash flow and positive free cash flow for the quarter. In this update we'll dig into the Q3 results, recent developments, and where the stock's updated low-risk buy zone lies:

{kind=link}

Q3 Production & Sales

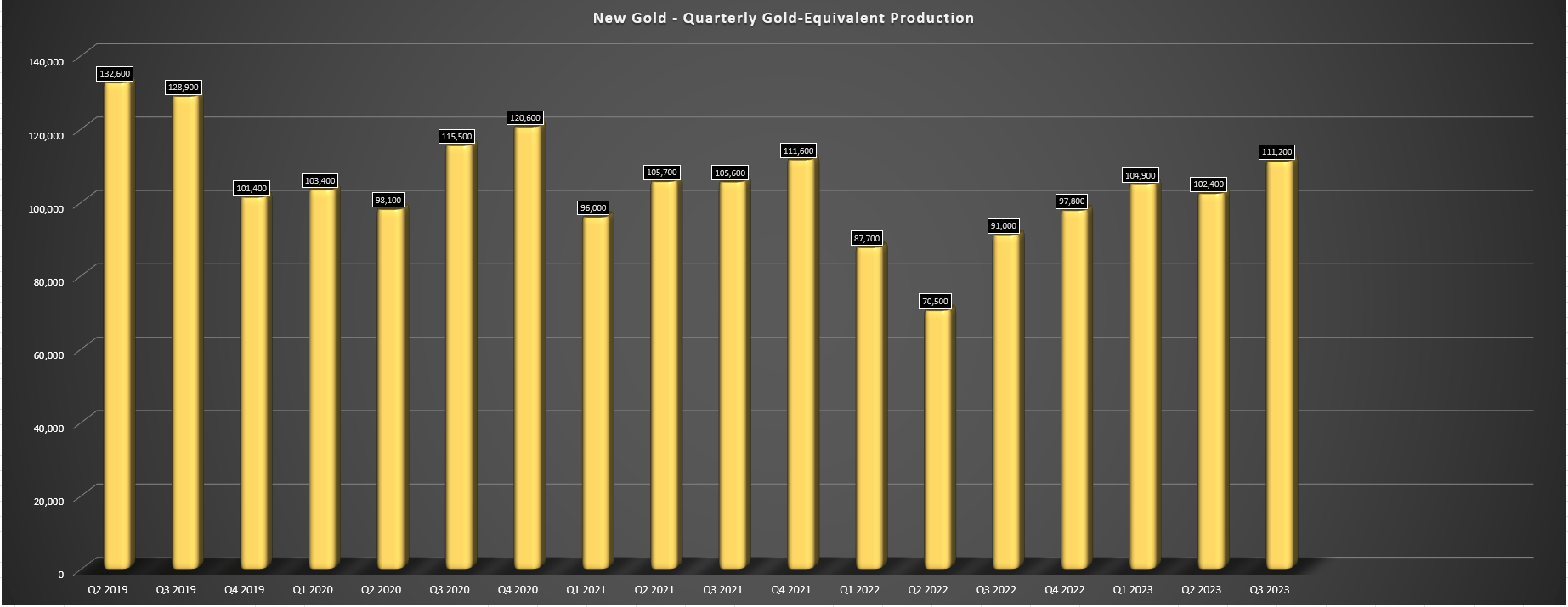

New Gold released its Q3 results in late October, reporting quarterly production of ~111,300 gold-equivalent ounces [GEOs], a 22% increase year-over-year and the company's best production quarter since Q4 2021. The increased production was driven by higher output at both Rainy River (Ontario) and New Afton (British Columbia), with both assets having a solid year and tracking towards the upper end of their respective guidance ranges. In fact, New Gold's year-to-date production is sitting at ~318,400 ounces, sitting at 80.6% of initial guidance, placing it in one of the best positions among its peers regarding year-to-date production levels vs. annual estimates.

New Gold Quarterly GEO Production - Company Filings, Author's Chart

{kind=link}

Digging into the results a little closer, Rainy River's increased production can be attributed to higher throughput and grades, and development continues to progress well with ~560 meters of advance during the quarter. Just as importantly, grades from the smaller Intrepid Zone continue to reconcile well with expectations, with production of 800 to 1,000 tonnes per day, with higher tonnes expected once Main Zone production begins in Q4 2024. During the quarter, Rainy River processed ~25,300 tonnes per day at an average grade of 0.97 grams per tonne of gold (Q3 2022: ~24,400 tonnes at 0.89 grams per tonne of gold), translating to ~66,400 ounces of gold, a 10% increase over the year-ago period.

{kind=link}

Moving to New Afton, production came in at ~44,800 GEOs (+46% year-over-year), benefiting from B3 extraction rates that are exceeding plans that has left the mine on track to deliver well above its guidance midpoint of 145,000 GEOs (~123,100 GEOs year-to-date). The higher production was driven by higher throughput (~8,650 tonnes per day), higher grades (0.72 grams per tonne of gold and 0.80% copper) and higher recovery rates, and we saw a significant improvement in costs with all-in sustaining costs [AISC] dipping to $1,229/oz from $1,769/oz in the year-ago period. Perhaps the most impressive is that New Afton generated $5.1 million in free cash flow during this more capital intensive period as it works to bring the C-Zone online, with over $38.0 million in capex spent in Q3 alone ($109.1 million year-to-date).

{kind=link}

As for progress on the C-Zone, New Gold reported that it advanced ~1,200 meters in the quarter and that the first draw bell at the C-Zone was completed, as was the commissioning of the final two dewatering wells at the New Afton TSF. This is great news in terms of New Gold's transition into a lower-cost miner from a high-cost miner in the past several years given that production during 2024-2030 will average ~230,000 GEOs, ~60% above the FY2023 guidance midpoint, allowing for a significant decline in operating costs at this asset. So, when combined with Rainy River moving into much higher grades (underground contribution) and the completion of waste stripping post-2024, New Gold should see its costs drop materially from the $1,555/oz guidance midpoint this year.

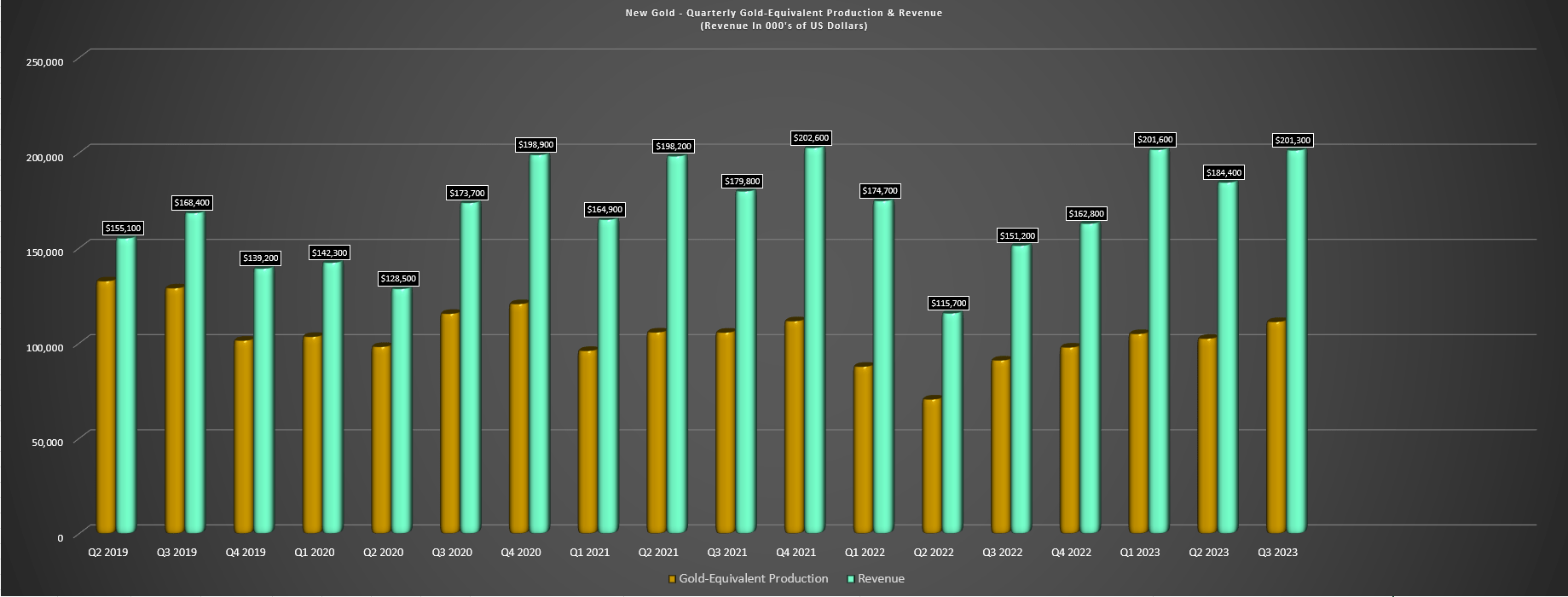

Finally, looking at New Gold's financial results, revenue increased to $201.3 million (Q3 2022: $151.2 million), benefiting from higher metals prices and higher production/sales. And combined with a weaker Canadian Dollar, this helped the company to generate $100.1 million in operating cash flow and over $20 million in free cash flow, a significant improvement from year-ago levels. Notably, this was achieved despite spending $70.6 million on capex or just shy of $300 million annualized. So, once we see a significant decline in capex in 2024 (~$200 million vs. ~$300 million) and a further decline in growth capex in 2025, we should see a material increase in free cash flow starting in H2-2024.

New Gold - Quarterly GEOs Produced & Revenue - Company Filings, Author's Chart

{kind=link}

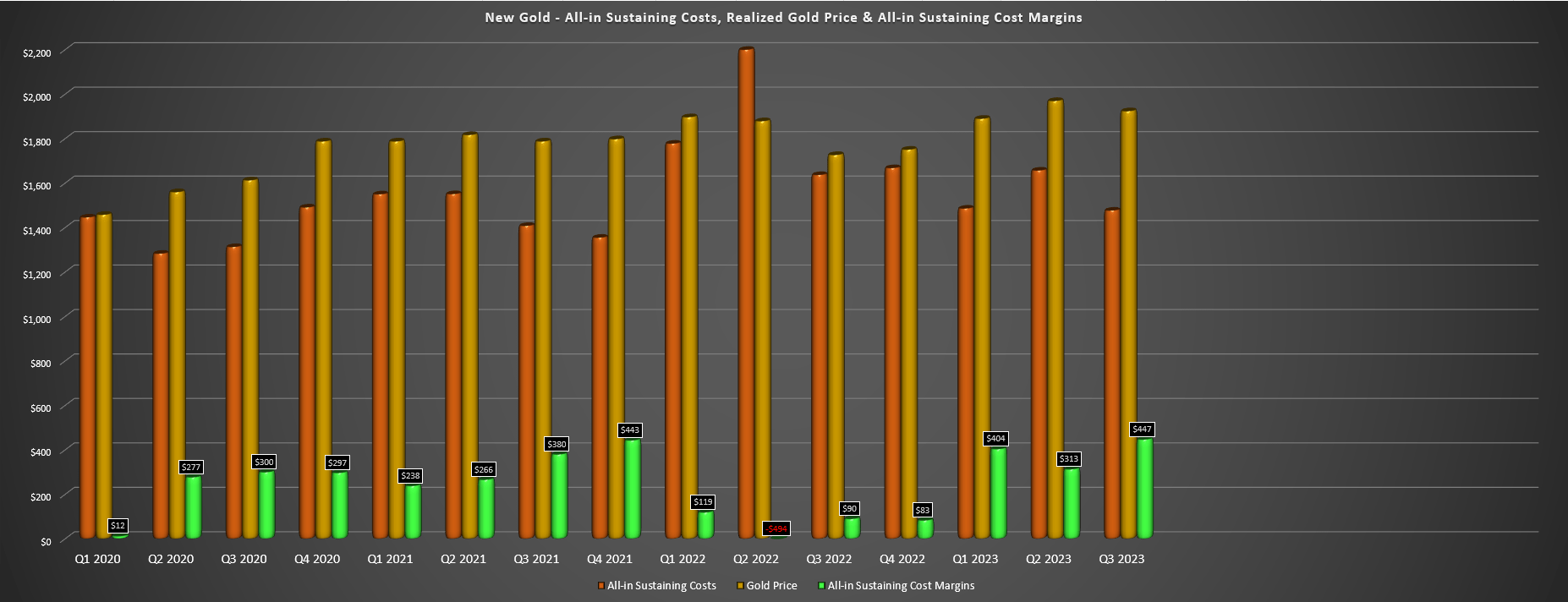

Costs & Margins

Moving over to costs and margins, New Gold reported all-in sustaining costs of $1,477/oz, a 10% decline year-over-year due to lower sustaining capital and higher ounces sold, offset by higher corporate G&A and share-based compensation. This translated to quarterly AISC margins of $447/oz, a massive improvement from the $90/oz reported last year. However, while past spikes higher in AISC margins were short-lived and predominantly driven by gold price strength, the trend appears to have finally changed as New Gold transitions to the best years of its mine lives on deck at New Afton/Rainy River. Hence, I would expect consistent AISC margins above $650/oz starting in 2025 if the gold price can cooperate, allowing New Gold to shed its high-cost producer status and get more respect in the market as a potential investment after years of razor-thin margins and significant margin volatility.

New Gold - AISC, Gold Price & AISC Margins - Company Filings, Author's Chart

{kind=link}

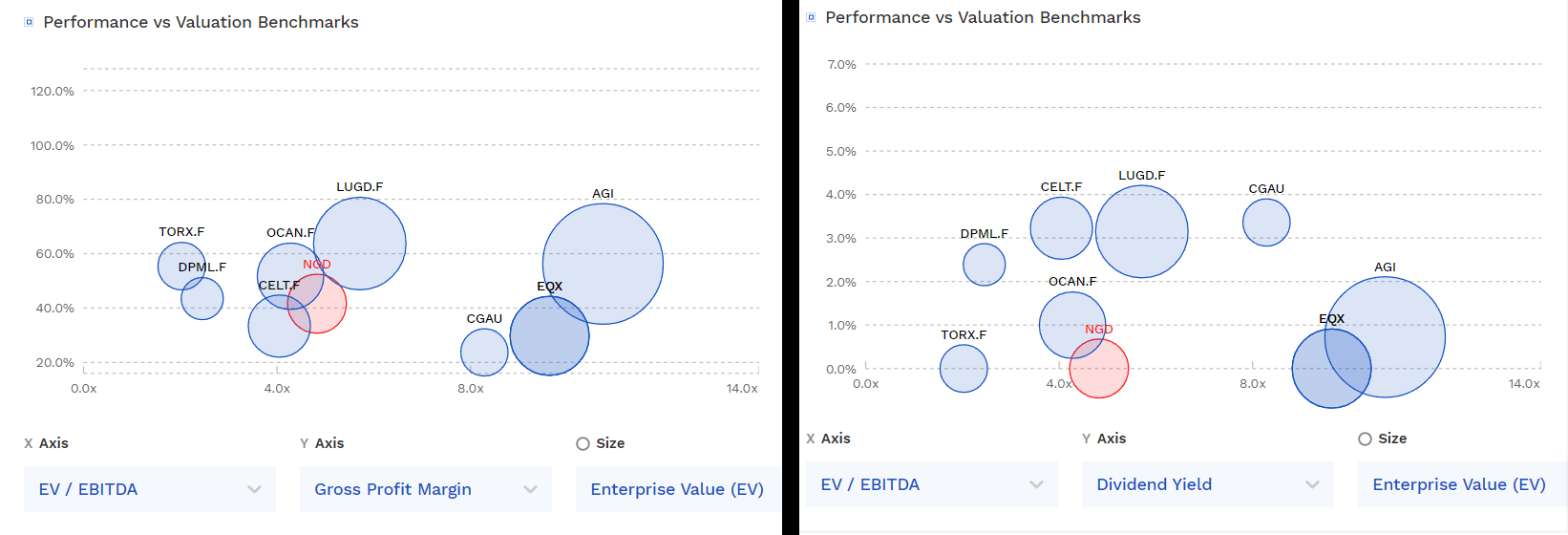

Valuation

Based on ~692 million fully diluted shares and a share price of US$1.56, New Gold trades at a market cap of ~US$1.08 billion and an enterprise value of ~$1.38 billion, leaving it near the middle of the pack for its mid-tier producer peer group. However, while the company has consistently been one of the weakest names from a margin standpoint on a trailing-five-year basis, New Gold will move into the top ranks from a margin standpoint post-2024 with FY2025 AISC likely to come in below $1,250/oz (FY2025 estimated industry average: ~$1,440/oz). And when combined with significant free cash flow generation, this could help to increase its relatively depressed multiple vs. other Tier-1 peers like Wesdome (WDOFF).

Valuations, Enterprise Value & Dividend Yields Peer Group - FinBox

{kind=link}

Using what I believe to be fair multiples of 5.0x FY2024 cash flow estimates and 0.90x P/NAV and a 65/35 weighting (P/NAV vs. P/CF), I see a fair value for NGD of US$1.80. This points to a 14% upside from current levels, and makes NGD one of the least attractive names from a relative value standpoint after its recent outperformance. Plus, I am looking for a minimum 40% discount to fair value when it comes to buying small-cap names, meaning that while NGD was in a low-risk buy zone below US$1.00 earlier this year, it's hard to argue that there's an adequate margin of safety at present with the stock's updated ideal buy zone coming in at US$1.09 or lower. Obviously, there's no guarantee that the stock pulls back by this magnitude and a rising gold price will lift all boats. Still, I prefer to buy at the right price or pass entirely, and I think there are more attractive names elsewhere currently.

Summary

New Gold has had a solid year operationally under new management and the company has flipped from over-promising and under-delivering to performing above expectations this year (production tracking to high end of guidance). Meanwhile, although the company managed to generate free cash flow this year despite significant investments in growth (Rainy River Underground, C-Zone development), 2025 will be a monster year for the year with a full year of Main Zone/C-Zone production and the potential to generate over $200 million in free cash flow (FY2025). That said, while ~6.4x FY2025 EV/FCF estimates is an attractive valuation, I continue to see more attractive bets elsewhere in the sector like Argonaut Gold (ARNGF) at just ~3.8x FY2025 EV/FCF estimates also as a Tier-1 jurisdiction producer (Ontario/Nevada).

To summarize, I remain focused elsewhere on the time being where I see more attractive reward/risk bets, and I would view any rallies above US$1.71 in NGD before February as an opportunity to book some profits.

For further details see:

New Gold: Another Solid Quarter With Higher Free Cash Flow On Deck