SBNY - New York Community: Great Performance And Undervalued

2023-04-29 08:00:00 ET

Summary

- New York Community's Signature asset acquisition looks great.

- The company is performing well operationally.

- The bank is not expensive and offers a sizeable dividend yield.

Article Thesis

New York Community Bancorp, Inc. (NYCB) has reported strong quarterly results. It looks like its takeover of Signature assets has worked well for the company and its shareholders. With an attractive dividend yield and an undemanding valuation, New York Community looks like a good bank investment, I believe.

The Signature Asset Deal Is Paying Off

New York Community Bancorp is not among the largest banks in the nation, but its financial position has been strong enough for it to make a bid on a large portion of the assets that failed Signature Bank (SBNY) owned. Via its Flagstar Bank unit, New York Community bought these assets, such as Signature's deposits and some of its loans, well below face value, and it looks like this deal will be highly accretive for the company's per-share value on a tangible book value basis.

Seeking Alpha reported [emphasis by author]:

The deal included the purchase of about $38.4 billion of Signature Bridge Bank North American assets, including loans of $12.9 billion purchased at a discount of $2.7 billion . Approximately $60 billion in loans will remain in the receivership for later disposition by the FDIC. In addition, the FDIC received equity appreciation rights in New York Community Bancorp, Inc., common stock with a potential value of up to $300 million.

Buying $12.9 billion worth of loans for $10.2 billion sounds like a great deal, especially for a bank that is valued at just $7 billion itself -- this deal, at a little less than 80% of face value, added equity [what NYCB paid versus the face value of the loans] equal to almost 40% of NYCB's market capitalization. Not surprisingly, the market reacted very positively to the deal announcement, and NYCB received several analyst upgrades in the wake of the deal announcement.

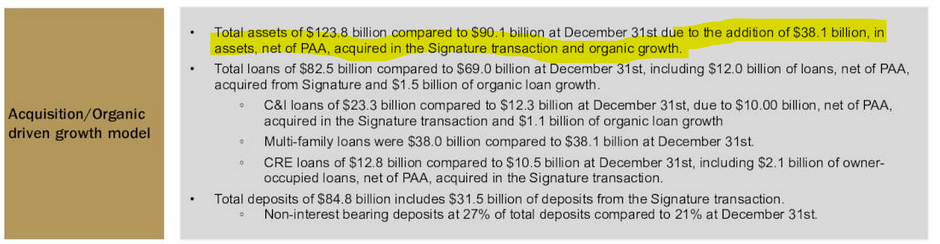

New York Community Bank reports the following in its Q1 earnings slides :

{kind=link}

Assets grew by more than one-third during the first quarter alone, which included the impact of the Signature asset acquisition as well as the growth that NYCB experienced in its existing operations, e.g. due to its customers doing more business with the bank, or by adding new customers at existing branches.

Importantly, New York Community Bank also notes the following:

{kind=link}

While some investors and some management teams believe that acquisitions for the sake of growth are a good idea, many others will argue that acquisitions and other growth investments only make sense when they drive up the value of the acquirer's existing shares. This happens when earnings per share and book value per share rise following a transaction, despite the potential issuance of new shares. This has been the case here, as New York Community's earnings per share and its tangible per-share book value, a metric often used to value bank stocks, have benefited from the Signature deal.

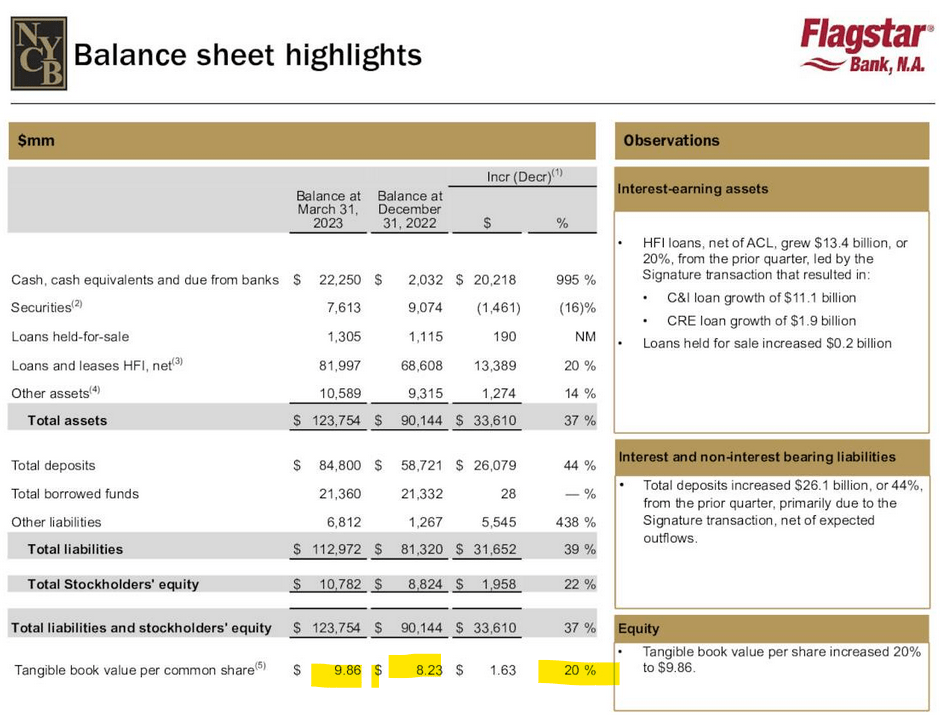

It is important to note that this deal is already accretive despite the fact that New York Community added a large amount of cash via this acquisition -- the bank's cash position grew from $2 billion at the end of Q4 to $22 billion at the end of the first quarter, which makes for a 1,000% increase. Once New York Community has utilized all of this cash in an accretive manner, e.g. by loaning it to its customers, the company should experience a profitability jump, and its earnings per share should go up further from what we have seen during the first quarter.

While New York Community's share count is up on a year-over-year basis, its tangible book value grew a lot faster than its share count, which is why tangible book value rose drastically even on a per-share basis:

{kind=link}

A 20% tangible book value increase during a single quarter is pretty rare and indicates that management's bold move to acquire the Signature assets was a great decision.

New York Community Had A Strong Quarter

While the Signature deal overshadows many other things, New York Community did also perform well on an operational basis during the first quarter. This is, for example, showcased by the bank's strong net interest margin performance during the period.

From a solid level of 2.28% during the fourth quarter of 2022, New York Community's net interest margin rose to 2.60% in the first quarter. This represents a hefty increase that has had a major impact on the bank's revenue performance. If New York Community is able to keep its net interest margin high, or potentially even grow it further, its revenue generation will be on a higher level going forward, even backing out the Signature deal.

Some banks have experienced bank runs or major deposit outflows in recent months, with smaller banks being impacted more compared to the mega banks that are, by many, seen as safer due to their too-big-to-fail status. New York Community has experienced some outflows on an operational basis, but not at a drastic level at all. During the first three months of the year, NYCB's deposit decline was in the single digits, while the addition of the deposits from Signature has resulted in a big overall deposit boost on a net basis. The majority of the deposit outflows had nothing to do with the bank panic that we have seen during late Q1, instead, there were other factors at play. NYCB saw outflows due to crypto company Circle Internet Financial withdrawing more than $2 billion from its reserve account, for example. This happened before the liquidity event and was unrelated to fears about smaller banks. I thus do not believe that there is a large risk of a bank run here -- instead, NYCB looks pretty low-risk from that perspective. Not only does it have a hefty cash balance, but it is also quite profitable and there are no rumors or fears about major risks in its loan portfolio.

Most of said loan portfolio is related to multifamily loans, which is a rather low-risk asset class, as people will always need a place to live, and since residential real estate prices have been surprisingly resilient during the steep interest rate increases we have seen over the last year.

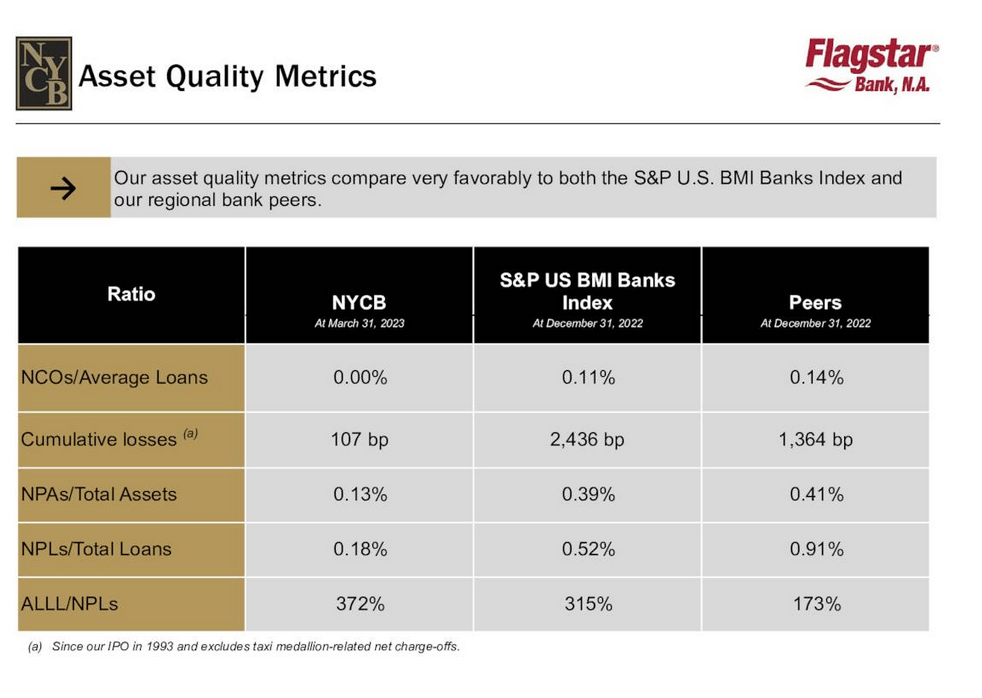

Risks across NYCB's portfolio look low, both in absolute terms and compared to the bank's peer group:

{kind=link}

We see that the ratio of non-performing loans isn't high across the entire US banking industry, but it's especially low at NYCB, at less than 0.2%. Even if all those loans were to end up as 100% losses, that would not have a dramatic impact on New York Community. Cumulative losses since the early 1990s are also pretty low, suggesting that NYCB has strong risk management and great underwriting standards. A bank like that is poised to weather a recession or other macro event better than most of its peers, which is encouraging for investors in the current uncertain macro environment.

A Nice Yield And A Low Valuation

With a tangible book value of slightly less than $10 per share, New York Community is currently trading at a little less than 1.1x tangible book value. For a strong bank with improving profitability and below-average risks, that's not a very high valuation.

Looking at the historic valuation norm for New York Community Bank, we see that the current valuation is pretty cheap:

Over the last three and five years, NYCB traded around 25% higher than today, looking at the bank's tangible book value multiple. Over the last ten years, the valuation was even higher, although I do not expect that NYCB's tangible book value multiple will rise above 1.5 any time soon. But even a reversal to the normal valuation in the recent past would result in a sizeable 20%+ share price gain, before any growth in the bank's book value.

Add a very appealing dividend yield of 6.6%, and NYCB has a good chance of delivering attractive total returns, I believe. The fact that NYCB has maintained the dividend despite the many things going on in Q1, with the banking worries and the Signature deal, makes it likely that the dividend will be safe in the future, too, I believe.

Takeaway

New York Community looks like an appealing bank to invest in right now. The valuation is far from high, the dividend yield is strong, and the company should continue to reap benefits from the great Signature asset deal. While NYCB was an even better buy a couple of weeks ago when its shares traded well below $10, they seem attractive here as well.

For further details see:

New York Community: Great Performance And Undervalued