CA - Newcrest: A Solid Year Despite Slight Miss On Guidance At Midpoint

2023-07-26 18:31:08 ET

Summary

- Newcrest reported lower than expected production in fiscal Q4 after extreme weather at Lihir, impacting its FY2023 results.

- However, despite headwinds during the year and a weaker average realized copper price, Newcrest's costs were well below the industry average.

- And while FY2023 might have been a softer year than planned, we should see a much better FY2024 with higher grades at Brucejack and Lihir.

- That said, with an offer that values Newcrest at ~11x cash flow and 40% above the peer group average for million-ounce producers (~7x cash flow), voting in favor of NEM deal looks like the best move as no other offer is likely.

It's been a mixed start to the CY-Q2 Earnings Season for the Gold Miners Index ( GDX ), with Newmont ( NEM ) and Evolution Mining ( CAHPF ) both reporting results below expectations, though out of their control with a strike at Penasquito (Newmont) and severe flooding at Ernest Henry (Evolution). Unfortunately, Newcrest Mining ( NCMGF ) fared little better than its intermediate and senior producer peers that have reported to date, with gold production at the low end of guidance and copper output below the low end of guidance in FY2023. However, like Newmont and Evolution, one of its most productive operations was impacted by severe weather, with Lihir coming up short of FY2023 guidance (720,000 to 840,000 ounces) with gold production of ~670,000 ounces. That said, even with lower than planned output at Lihir and Brucejack due to one-time events and a lower average realized copper price, Newcrest still reported a very solid year. Let's take a closer look below:

{kind=link}

While North American gold producers recently released their Q2 2023 results, the Australian producers released their fiscal Q4 2023 results, which are the same as calendar year Q2 2023 results, to avoid confusion. All figures are in United States Dollars unless otherwise noted.

Q4 & FY2022 Production

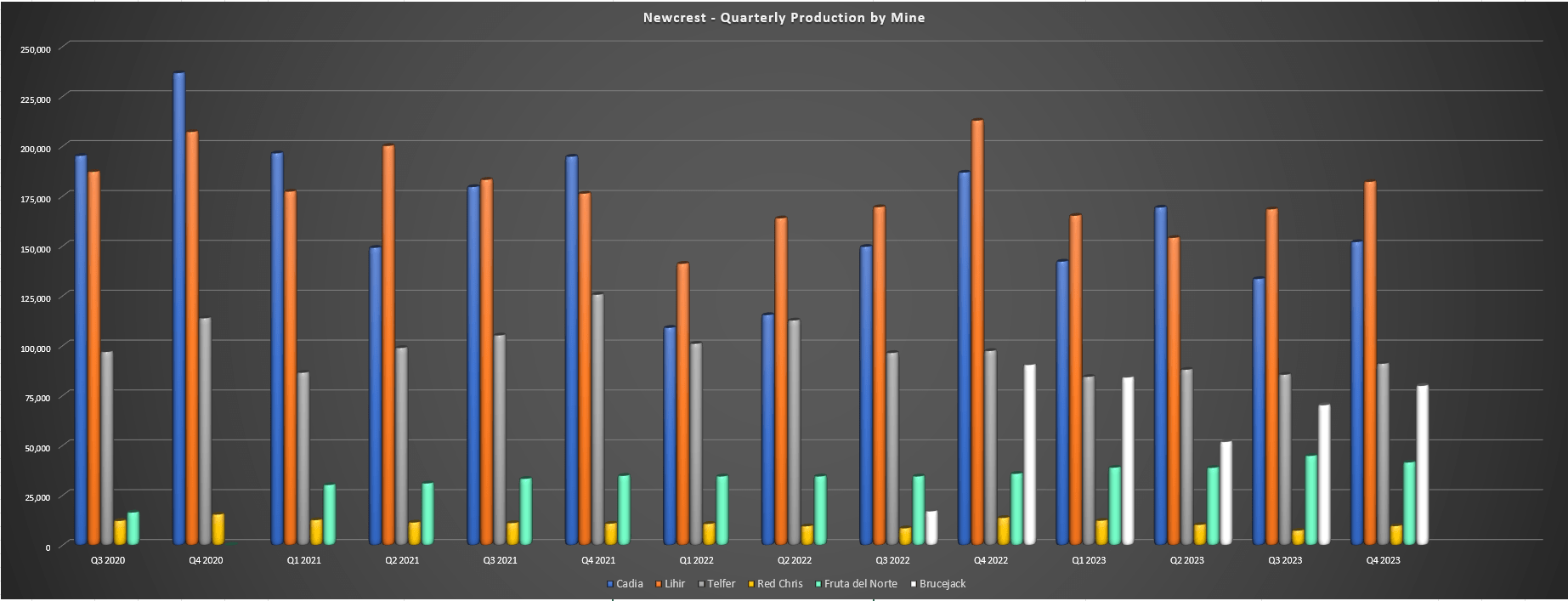

Newcrest Mining ("Newcrest") released its fiscal Q4 2023 and FY2023 results this week, reporting quarterly production of ~556,200 ounces of gold and ~35,000 tonnes of copper, a sharp decline from ~637,000 ounces of gold and ~38,700 tonnes of copper in the year-ago period. The significant decline in production was partially due to Newcrest being up against difficult year-over-year comparisons after a monster fiscal Q4 2022 for Cadia (~186,800 ounces of gold) and Lihir (~212,900 ounces), in addition to a strong quarter from Brucejack with 90,000+ ounces. And while production wouldn't have seen as significant of a drop if this was a normal quarter for Newcrest, gold production at Lihir came in well below plans due to severe rain at the Papua New Guinea asset, with unplanned outages, impacted material handling rates, reduced material movement and lower grades (inability to access high-grade ore in the Phase 14 orebody) all weighing on the asset's fiscal Q4 production.

Newcrest - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

As the chart above highlights, Lihir still managed to put up a solid fiscal Q4 report (~182,200 ounces) with this being the best quarter of the year, but production was nowhere near expectations for a robust finish in the June quarter. The result was FY2023 gold production came in 7% below the low end of guidance and costs came in well above expectations at $1,466/oz, even if they did improve on a year-over-year basis. That said, Newcrest noted that rainfall in the current quarter (July through September) is expected to be more in line with the long-term average, resulting in higher mining volumes, with a further benefit from two new shovels being dropped at site in fiscal Q1 2024 (current quarter). So, with higher-grade ore from Phase 14A set to contribute to feed this year, Lihir should bounce back in FY2024 despite the short-term setback that derailed the company's FY2023 production profile, and FY2025/FY2026 should be even better, helping to pull down costs at this Tier-1 scale asset.

{kind=link}

Moving over to the company's ultra-low cost Cadia Mine in Australia, the mine produced ~152,000 ounces of gold in fiscal Q4 2023 and ~25,200 tonnes of copper, down from ~186,800 ounces of gold and ~28,200 tonnes of copper in the year-ago period. The lower production was related to a decline in grades this year (as expected) with head grades of 0.78 grams per tonne of gold and 0.40% copper vs. elevated grades of 0.94 grams per tonne of gold and 0.43% copper in fiscal Q4 2022. That said, despite the lower production, AISC came in among the lowest levels sector-wide at $188/oz, translating to AISC margins of $1,740/oz in the period. Plus, on a full-year basis, Cadia delivered into the high of its FY2023 guidance and produced ~596,900 ounces of gold, a nearly 7% increase year-over-year, and copper production also up sharply. This resulted in industry-leading annual AISC of $45/oz, albeit down from [-] $124/oz in FY2022 with the impact of a lower average realized copper price that offset higher copper sales.

Just as importantly when it comes to the longevity of this asset, Newcrest noted that adjustments were put in place after receiving a letter from the EPA, with a reduction in mining rates, modifications to the ventilation circuit as well as additional dust sprays and spray curtains being installed. In addition, a 12-month study undertaken by the Australian Government's Australian Nuclear Science Technology Organization [ANSTO] concluded that air quality standards and Cadia and surrounding areas have been met, and that metals of concern (lead, nickel, selenium, chromium) did not exceed national standards and only occurred at low levels. This study supports the community water testing program which showed that water tested was safe to drink, and a lead fingerprinting analysis through ANSTO found no evidence linking Cadia to the lead sampled in district rainwater tanks.

Given that this is Newcrest's lead cash flow generator by a wide margin given its sub $100/oz AISC with a Tier-1 scale production profile (500,000+ ounces per annum), the conclusions from these studies are certainly positive for Newcrest and any future owner of the mine as they reduce the risk of any restrictions or major disruptions to operations. And with the Victorian Government EPA putting restrictions on the Fosterville Mine recently, restrictions by the government would not have been surprising if the studies came to less positive conclusions. For those unfamiliar, Fosterville's mining rates have been reduced temporarily due to it not being able to operate surface fans at the high-grade mine in Victoria for one-fourth of operating hours per day (midnight to 6 AM).

{kind=link}

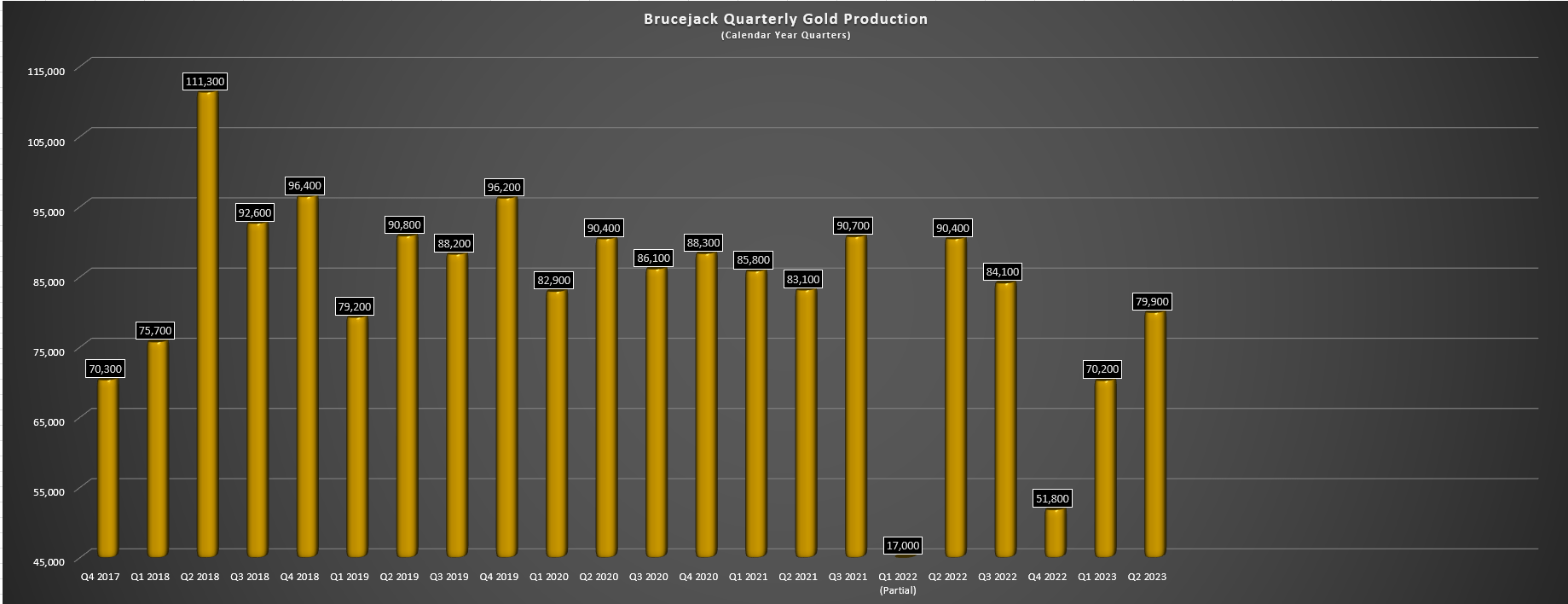

Finally, moving over to the Brucejack Mine in British Columbia, Newcrest reported gold production of ~79,900 ounces in fiscal Q4 2023 and annual production of ~286,000 ounces of gold. This was well behind the performance expected at the onset of the year, with production over 4% below guidance of 300,000 ounces. Newcrest noted that this was due to impacted production due to the fatality in October and lower than planned head grades in fiscal Q4 2023 which came in at 6.65 grams per tonne of gold, up from fiscal Q3 2023 but well below fiscal Q4 2022 levels (8.07 grams per tonne of gold). Given the lower production and the impact of inflationary pressures, all-in sustaining costs came in above planned levels at $1,135/oz in fiscal Q4 and $1,157/oz on a full-year basis, but these costs are still well below the expected FY2023 industry average of $1,320/oz sector-wide.

Brucejack Mine - Quarterly Production (Company Filings, Author's Chart)

{kind=link}

Although the FY2023 results at Brucejack weren't what investors might have expected, the company does have levers to pull when it comes to improving production and costs. For starters, half of the planned synergy benefits of $20 million (midpoint) have been delivered and the company is working on a de-bottlenecking study to potentially increasing plant capacity by up to 30%, which would help the asset to produce over 400,000 ounces per annum assuming a 7.8 gram per tonne head grade and recovery rates of 97%. This would help to significantly improve unit costs given the benefit of economies of scale, and there looks to be opportunities to lift grades with new high-grade discoveries near-mine (1080 HBx and North Block zones) and regionally at Golden Marmot (discovery hole of 53.5 meters at 72.5 grams per tonne of gold). Finally, Newcrest is also looking at an ore sorting concept study as well to improve operational flexibility and allow for more predictable and consistent feed grades at this high-grade asset.

Costs & Margins

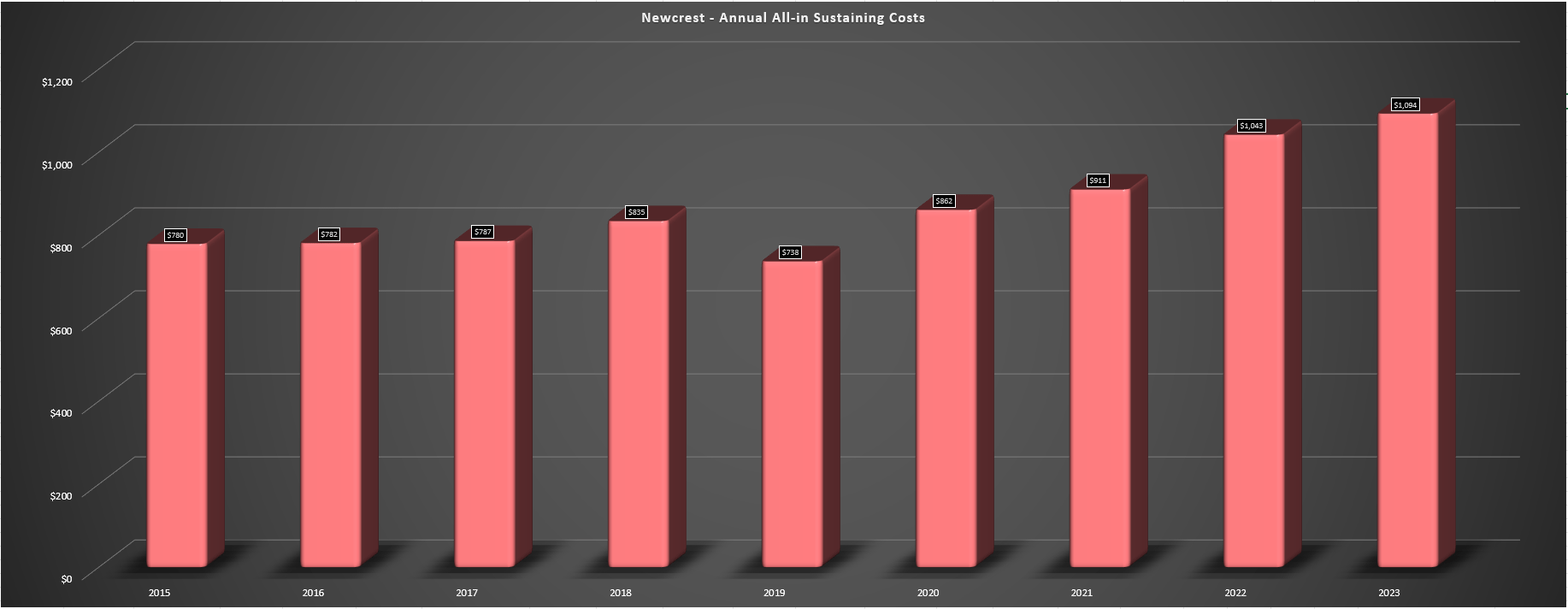

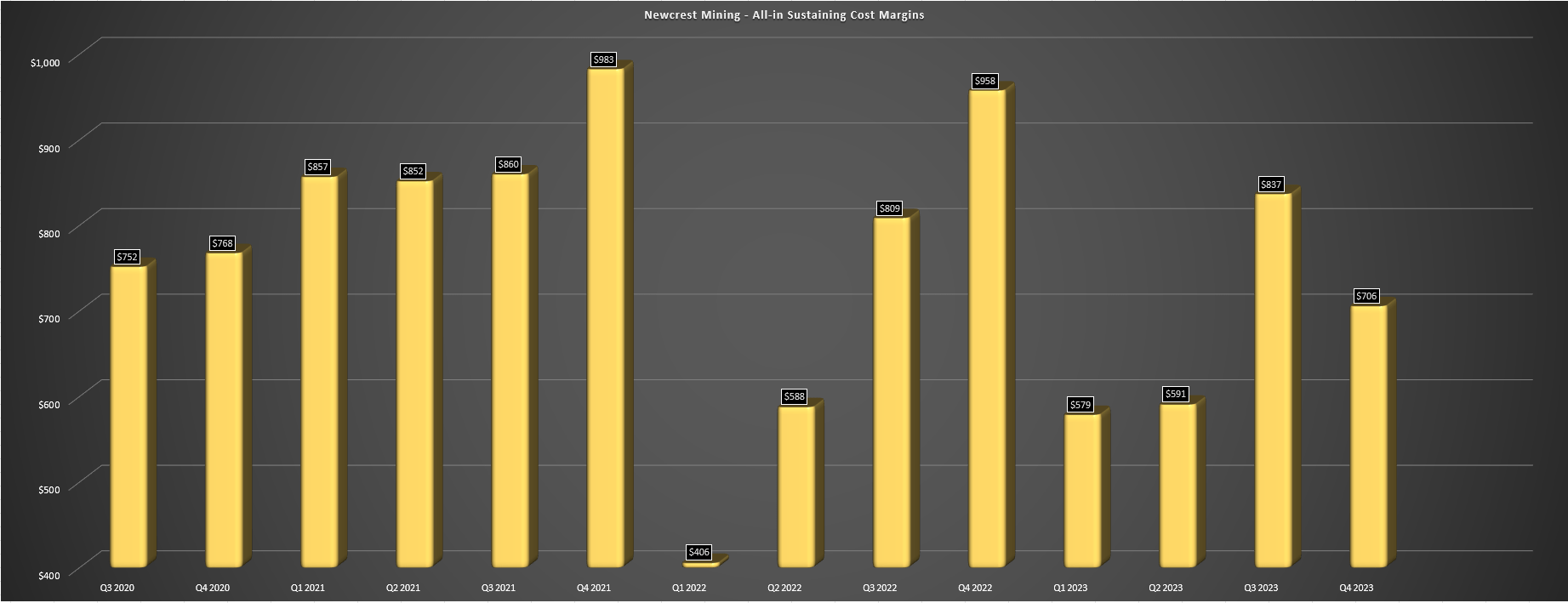

Digging into costs and margins, Newcrest's all-in sustaining costs [AISC] increased on a year-over-year basis to $1,196/oz vs. $896/oz in the year-ago period. And while this is disappointing, the company still managed to report industry-leading AISC of $706/oz (fiscal Q4 2023: $958/oz). On a full-year basis, Newcrest's AISC increased yet again to $1,094/oz which was due to reduced by-product credits from a weaker copper price ($3.76/lb vs. $4.36/lb), and AISC margins slipped to $678/oz, down from $732/oz in FY2022. However, FY2024 is expected to be a better year at Lihir and Brucejack, the AISC margins in FY2022 were based on a $1,795/oz gold price (currently ~$1,950/oz), and copper prices are also sitting higher above $3.90/lb, all pointing to what should be a much better FY2024 from a margin standpoint for the Newcrest portfolio (whether acquired or not). So, while it's easy to be negative about the margin compression, this looks temporary, especially with the potential for several cost improvements (Brucejack - higher throughput and synergies, Lihir - higher grades, Havieron - lower cost asset).

Newcrest - Quarterly AISC Margins (Company Filings, Author's Chart)

{kind=link}

{kind=link}

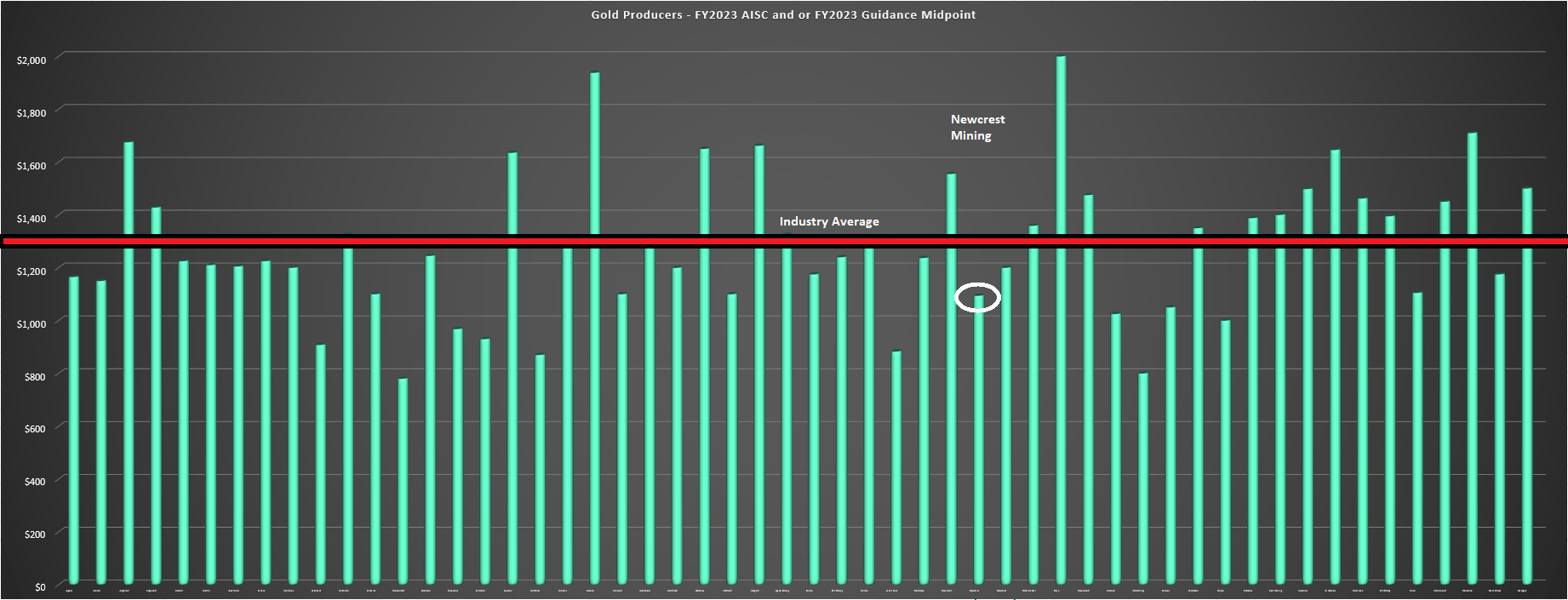

Finally, as noted, Newcrest's AISC may have been higher and above my expectations, but its cost profile is still well below the industry average and this was despite a year where the portfolio didn't perform as planned. So, if Newcrest can deliver AISC nearly 20% below the industry average in a bad year investors shouldn't be too concerned given that it should be able to pull costs back below $1,020/oz in a good year, and especially if copper prices can cooperate and get back above the $4.25/lb level. It's this industry-leading cost profile that makes me bullish on Newmont because while the Newmont portfolio may be struggling after a weak Q2 and with higher capex and one-time headwinds this year, it should look entirely different with new high-grade mines online (Tanami Expansion, Ahafo North), lower capex, and the addition of Newcrest's higher-margin assets.

Newcrest Annual AISC vs. Other Producers (FY2023 Costs & Or FY2023 Guidance Midpoint) (Company Filings, Author's Chart)

{kind=link}

Recent Developments

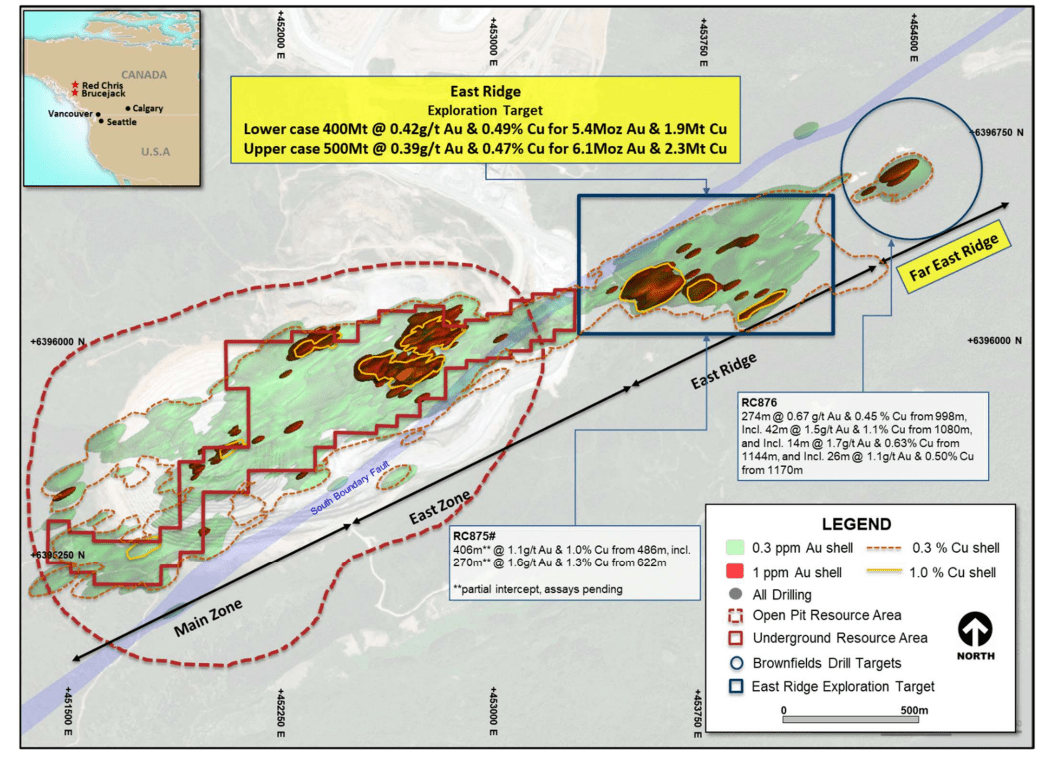

Lastly, I'd be remiss not to briefly discuss recent developments, with the major one being the updated exploration target at East Ridge, at its 70% owned Red Chris Mine in British Columbia. As shown below, the East Ridge Exploration target which lies outside of Red Chris' resources and reserves has been increased to ~500 million tonnes at 0.39 grams per tonne of gold and 0.47% copper or 6.1 million ounces of gold 2.3 million tonnes of copper. This is a major upgrade from ~300 million tonnes at 0.40 grams per tonne of gold and 0.40% copper at this time last year. And if we compare this potential resource to the current M&I resource base at Red Chris of ~12 million ounces of gold and ~3.5 million tonnes of copper, this would dramatically increase Red Chris' resource base at similar gold grades but higher copper grades, with a current resource grade of ~0.42 grams per tonne of gold and ~0.39% copper.

Newcrest - East Ridge Exploration Target & Far East Ridge Discovery (Company Website)

{kind=link}

During the quarter, Newcrest noted that it has "confirmed continuity of the higher-grade mineralization across the vertical extent of the deposit" at the East Ridge Exploration Target. As highlighted in its quarterly exploration report, a partial intercept in hole 875 hit 406 meters at 1.1 grams per tonne of gold and 1.0% copper from 486 meters, an incredible intercept with grades well above its current reserve grades and East Ridge Exploration Target. Just as importantly, drilling at Far East Ridge (a new discovery) intersected 274 meters at 0.67 grams per tonne of gold and 0.45% copper, which could become the fifth porphyry center along the Red Chris Corridor. Notably, this intercept was drilled 100 meters east of hole 860 which hit 66 meters at 0.53 grams per tonne of gold and 0.46% copper, a meaningful step-out that has confirmed elevated grades east of East Ridge. So, with East Ridge open to the east and at depth and a 30+ year mine life even without East Ridge or Far East Ridge that are higher grade, to say this asset has a very bright future would be an understatement, with it potentially being one of the best copper-gold assets globally.

{kind=link}

Summary

Newcrest may have delivered into the low end of FY2023 output guidance and reported costs slightly above my estimates ($1,094/oz vs. $1,050/oz), but its costs still came in over 20% below the industry average in FY2023 relative to what's likely to be industry average AISC of $1,320/oz plus this year. Plus, production affected by severe rainfall at Lihir (its #1 gold producer), a temporary suspension following a tragic fatality at Brucejack (#4 gold producer), and lower copper prices which reduced the company's by-product credits, which was obviously out of its control. However, FY2023 was not representative of the true potential of the Newcrest portfolio, with a declining cost profile as the decade progresses from key projects. These include:

- further synergies & potential throughput expansion at Brucejack.

- first production from Havieron, a low-cost operation with sub $800/oz AISC.

- higher output at Red Chris and the potential for negative AISC.

- higher grades from Phase 14A at Lihir.

- potential pour post-2030 from Wafi-Golpu, another negative AISC asset.

Assuming these opportunities ex-Wafi Golpu come to fruition, Newcrest has a path to improving costs by over 30% from FY2022 levels to sub $780/oz. However, if Wafi-Golpu (50%) can be successfully brought into production as well post-2030, we could see AISC drop below $730/oz potentially. This would make Newcrest the lowest-cost million-ounce gold miner in the sector by a wide margin, with costs only slightly higher than Kirkland Lake Gold in its prime, with FY2019 all-in sustaining costs of $564/oz. Hence, if Newcrest can execute successfully and shareholders approve the pending Newmont transaction, we will see a massive improvement in Newmont's cost profile and the combined company become a cash flow machine that sits in rare air from a scale, diversification, and margin standpoint.

For this reason, I see NEM as a steal during this period, where it remains out of favor after abnormally weak Q2 results, and given the attractive price offered to Newcrest shareholders (~11x FY2022 cash flow vs. the million-ounce producer peer average at ~7x cash flow), I see voting in favor of the deal as the best course of action.

For further details see:

Newcrest: A Solid Year Despite Slight Miss On Guidance At Midpoint