CA - Newcrest Deal: Solidifying Newmont's Position As The Largest Gold Producer

2023-06-15 11:50:37 ET

Summary

- Newmont Corporation's acquisition of Newcrest Mining Limited is valued at approximately ~$19 billion, and this will bring multiple large, low-cost, and Tier-1 jurisdiction assets into Newmont's portfolio.

- The acquisition will significantly increase Newmont's production, reserves, and margins, making it one of the lowest-cost million-ounce gold producers.

- With Newmont trading at less than ~7.0x forward cash flow and a much more reasonable P/NAV multiple following its correction, I would view any pullbacks below $40.40 as buying opportunities.

It's been a busy year for M&A in the gold sector. While there have been some larger deals in the developer space, with B2Gold Corp. ( BTG ) acquiring Sabina Gold & Silver, and Gold Fields Limited ( GFI ) announcing that it would acquire half of Osisko Mining's ( OBNNF ) Windfall Project , the most significant transaction was by far the Newmont Corporation ( NEM ) offer to acquire the multi-million-ounce Australian focused gold producer, Newcrest Mining Limited ( NCMGF ).

This deal is valued at ~$19.0 billion, with Newmont offering 0.40 shares of Newmont, and allowing Newcrest to pay a special dividend. And while Newmont is paying a rich price, the deal would be transformative, to say the least, with Newmont bringing multiple large, low-cost and Tier-1 jurisdiction assets into its portfolio, with a few of these having considerable exploration upside. Let's take a closer look at the deal below:

Red Chris Exploration Decline (Newcrest Presentation)

{kind=link}

All figures are in United States Dollars unless otherwise noted.

A Transformative Acquisition

There's no question that Newmont is paying a hefty price for its acquisition of Newcrest, especially given that it's having to use expensive currency (its own low-priced shares) to complete the acquisition. And compared to the Goldcorp deal in 2019, Newmont is paying approximately $360/oz per ounce on an enterprise value to attributable gold reserves basis vs. the ~$240/oz paid for Goldcorp's ounces.

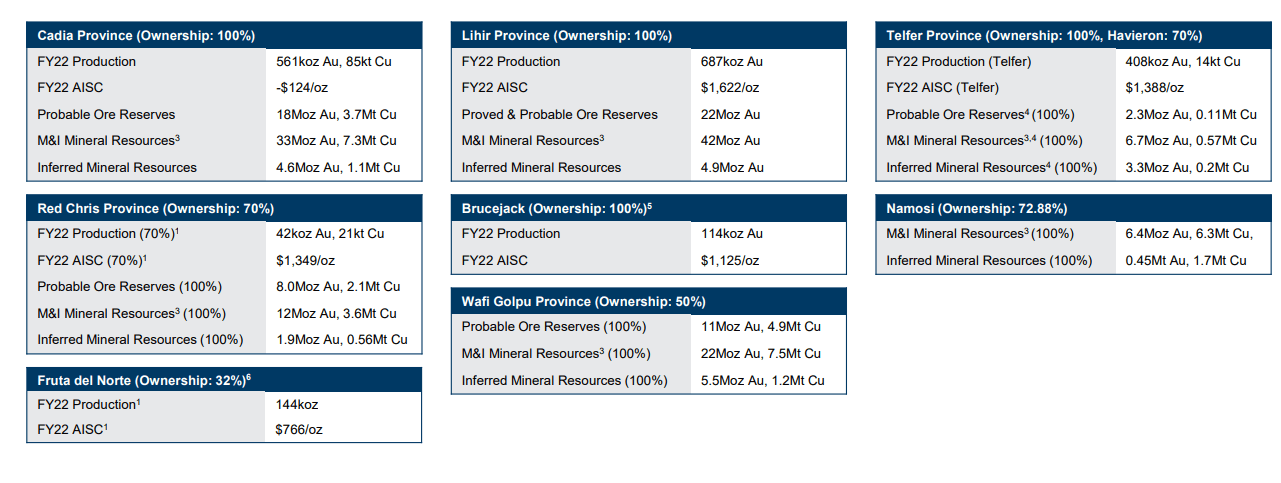

That said, if there were ever a company to pay up for in the sector in an acquisition, it would be Newcrest, with the company owning multiple world-class operating and development assets, including:

- Cadia : a ~600,000 ounce per annum operation with negative $124 all-in sustaining costs [AISC] in FY2022 with by-product credits.

- Havieron (70%) : a world-class gold-copper project with considerable mineral endowment.

- Fruta Del Norte (32%) : one of the world's most profitable mines with a 450,000 ounce per annum production profile at sub $850/oz AISC.

- Red Chris (70%) : a massive copper-gold project with the potential for negative all-in sustaining costs with copper by-product credits post-2027.

- Wafi-Golpu (50%) : an ultra-rich copper-gold porphyry with a grade of 0.86 grams per tonne of gold and 1.1% copper.

- Lihir : one of the largest gold mines by annual production (~800,000 ounces per annum) with a 20+ year mine life.

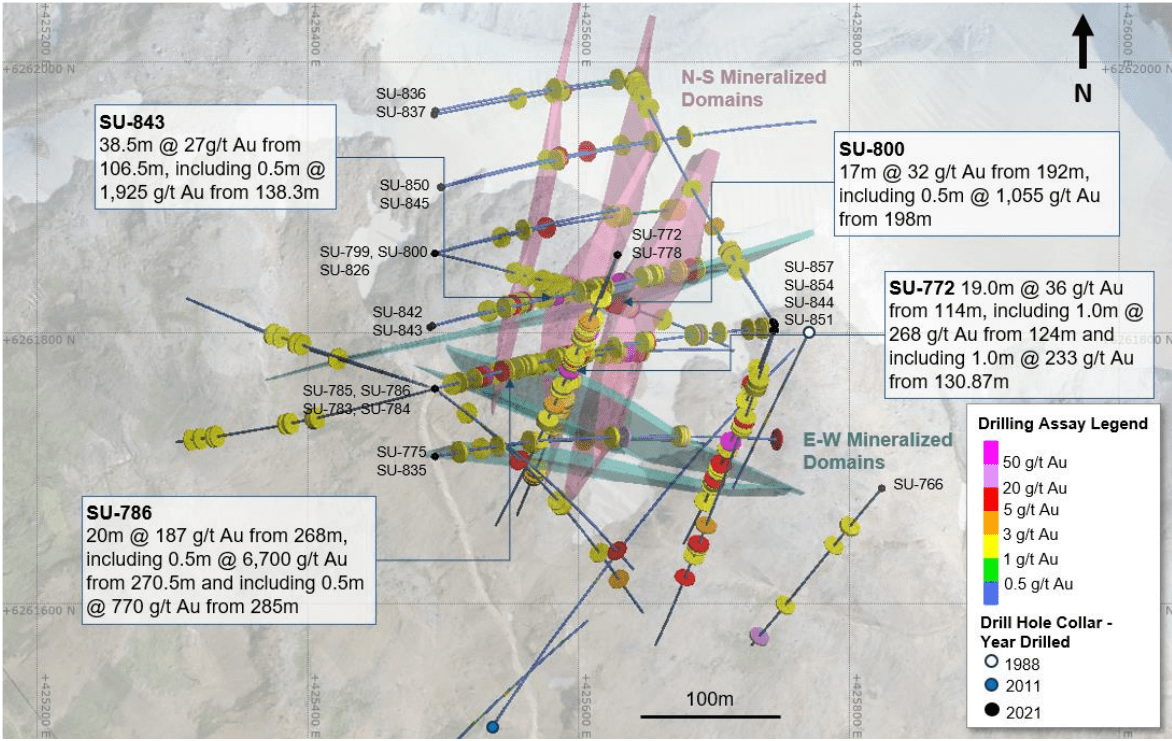

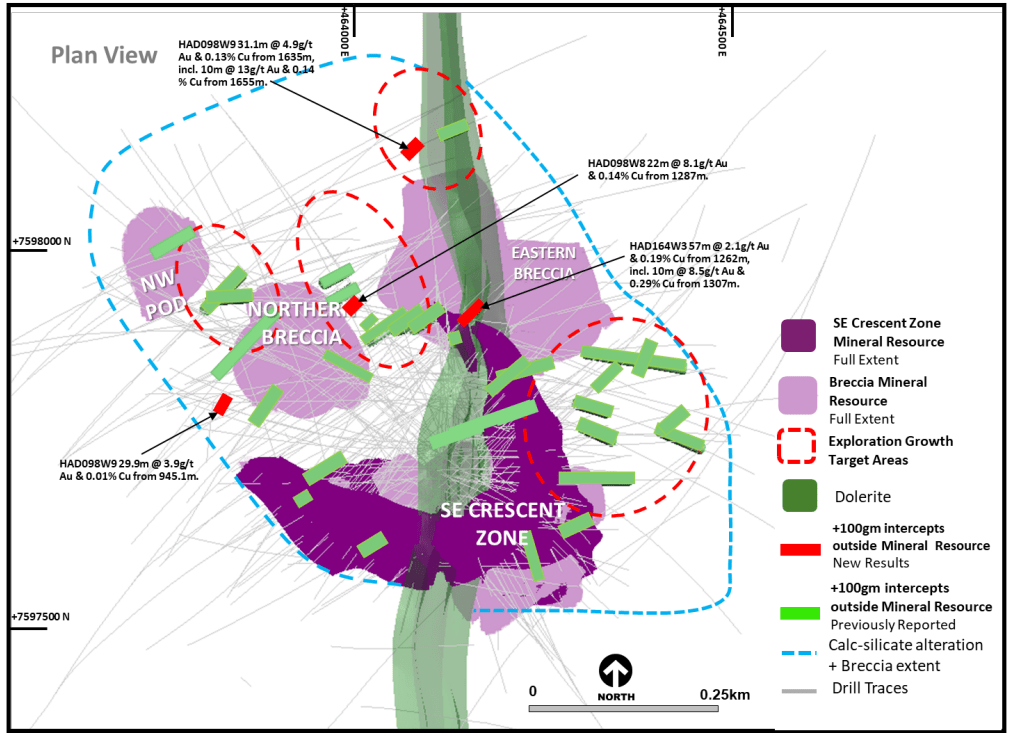

- Brucejack : one of the highest grade gold mines in North America with multiple new discoveries that could translate to mine life extensions, a throughput expansion, and lower overall operating costs.

Brucejack - Golden Marmot Regional Discovery Drill Highlights (Newcrest Presentation)

{kind=link}

Plus, while Newcrest's attributable gold reserve base comes in at ~53.0 million ounces or a ~$360/oz acquisition cost to Newmont on a purchase price of ~$19.0 billion, one could argue that this figure severely understates the reserve base, with a high likelihood of adding at least 3.5 million attributable gold reserves at Cadia East Ridge, an additional ~2.0 million attributable gold reserves at Havieron, and an additional 1.5+ million ounces of gold reserves at Brucejack (1080 Level, North Block, Golden Marmot). Hence, if we use a figure of ~60.0 million attributable gold reserves to highlight likely upside from exploration, the price paid per ounce drops to ~$317/oz, a very reasonable price for a primarily Tier-1 jurisdiction reserve base.

Newmont 2.0 - Operating Portfolio (Newmont Presentation) Newmont Goldcorp Transaction (Newmont Presentation)

{kind=link}

{kind=link}

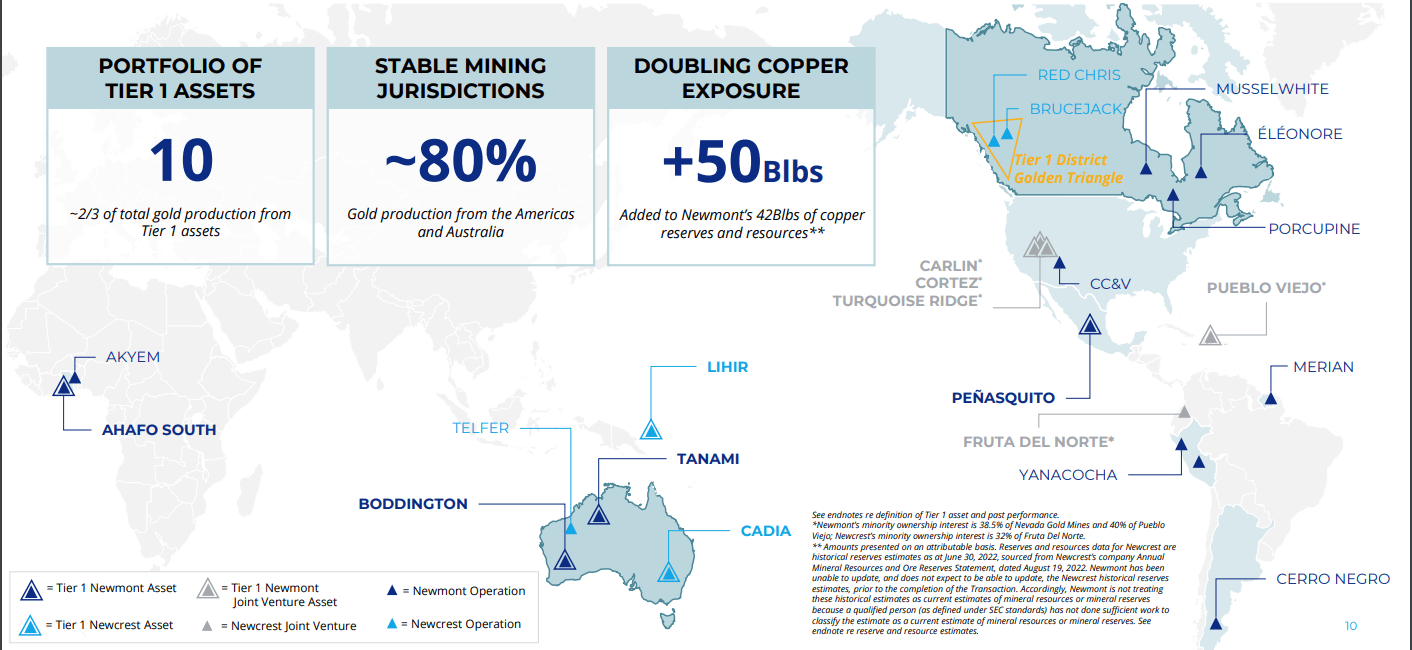

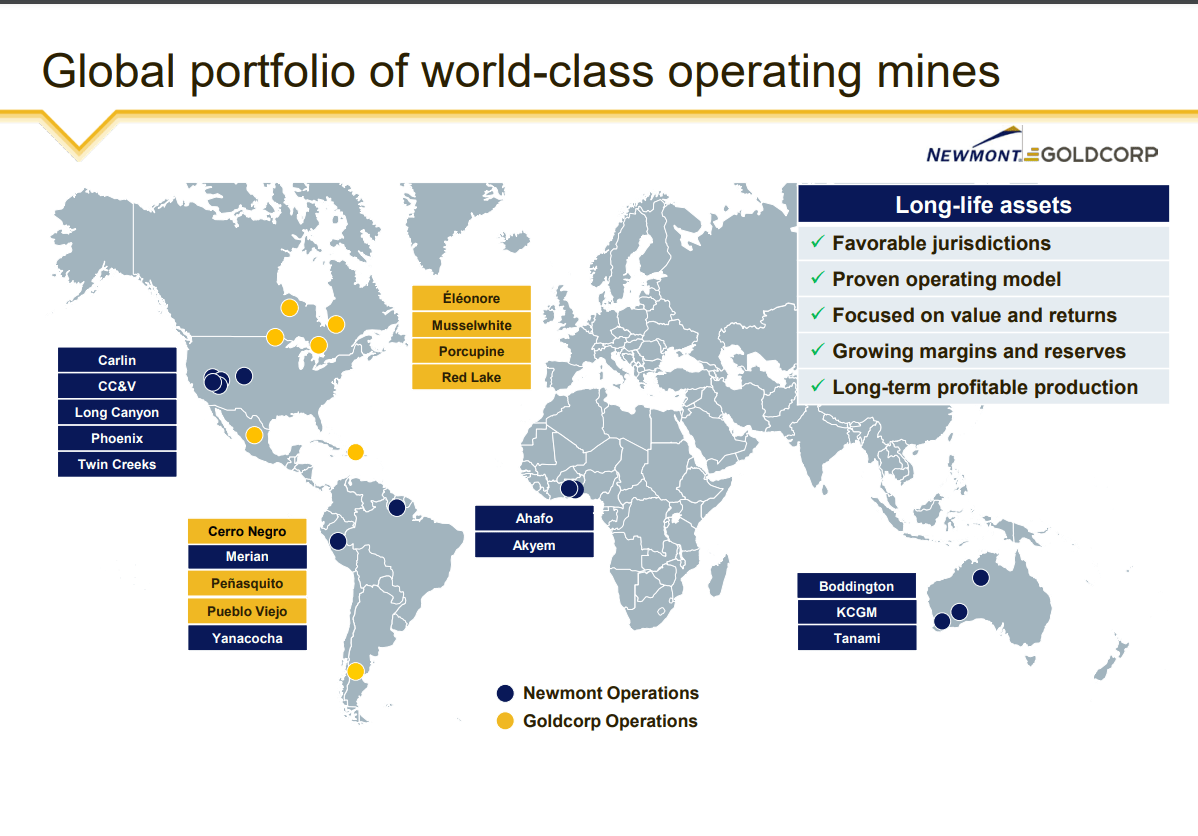

The above map highlights what Newmont 2.0 will look like, with a larger footprint in Tier-1 ranked jurisdictions (Canada and Australia) and a significant foothold in the well-endowed Golden Triangle (British Columbia), plus the entry into one new jurisdiction (Papua New Guinea), with Lihir and Wafi-Golpu (50%). It's important to note that compared to the Goldcorp acquisition, Newmont will add much higher-quality assets, with the two jewels in that transaction being Penasquito and a 40% stake in Pueblo Viejo vs. multiple world-class assets in this deal, with a few having enormous exploration upside. Plus, the integration should be smoother, with only one new jurisdiction (given that Newmont already has a significant presence in Newcrest's main operating jurisdictions (Canada and Australia) vs. three new jurisdictions in the Goldcorp deal (Canada, Argentina, Mexico). Plus, it will get a similar production profile increase, but with fewer mines (five managed mines with Newcrest vs. six managed mines with the Goldcorp deal).

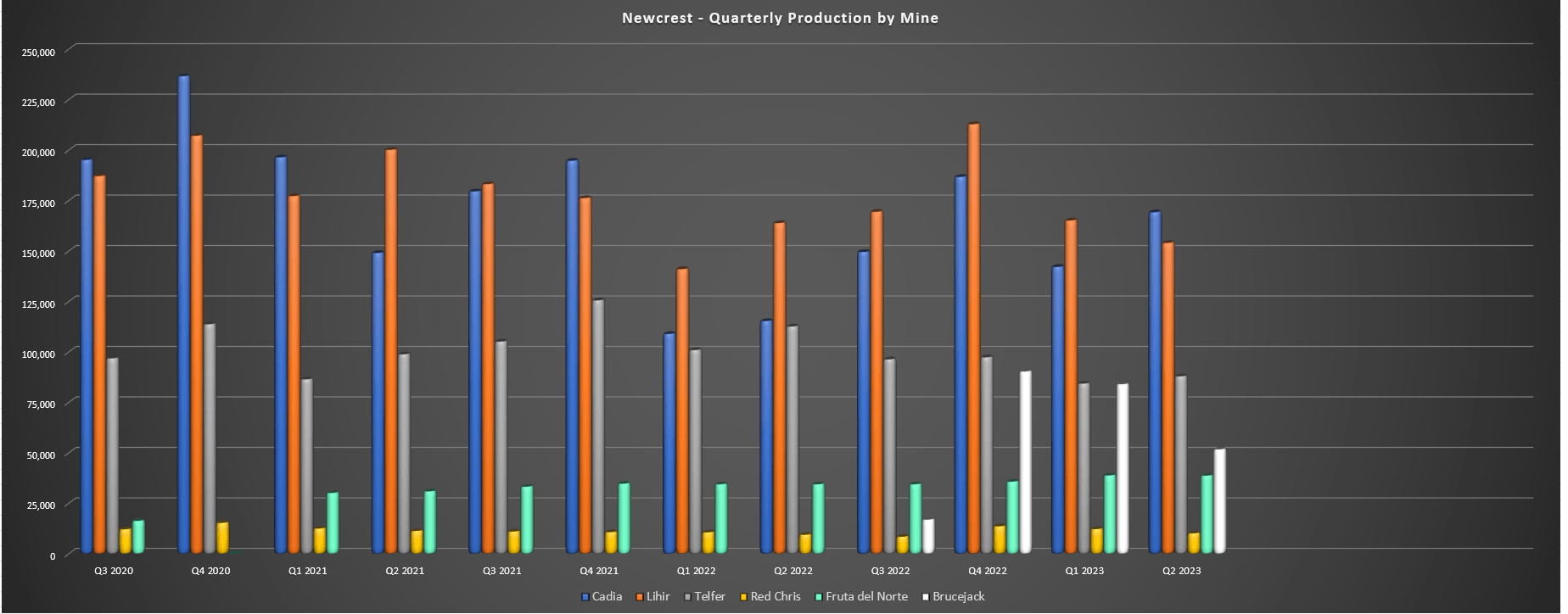

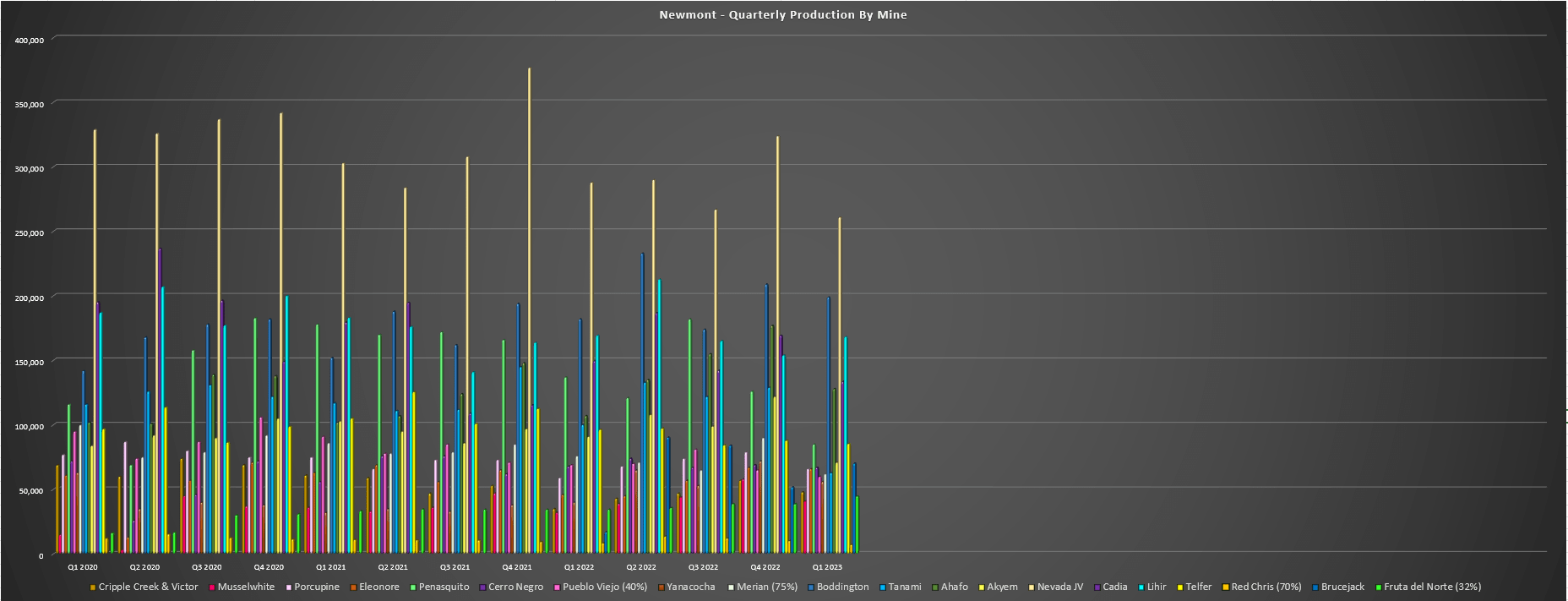

Newcrest - Quarterly Production Profile (Company Filings, Author's Chart) Newmont + Newcrest Production Profile (2020-2023) (Company Filings, Author's Chart)

{kind=link}

{kind=link}

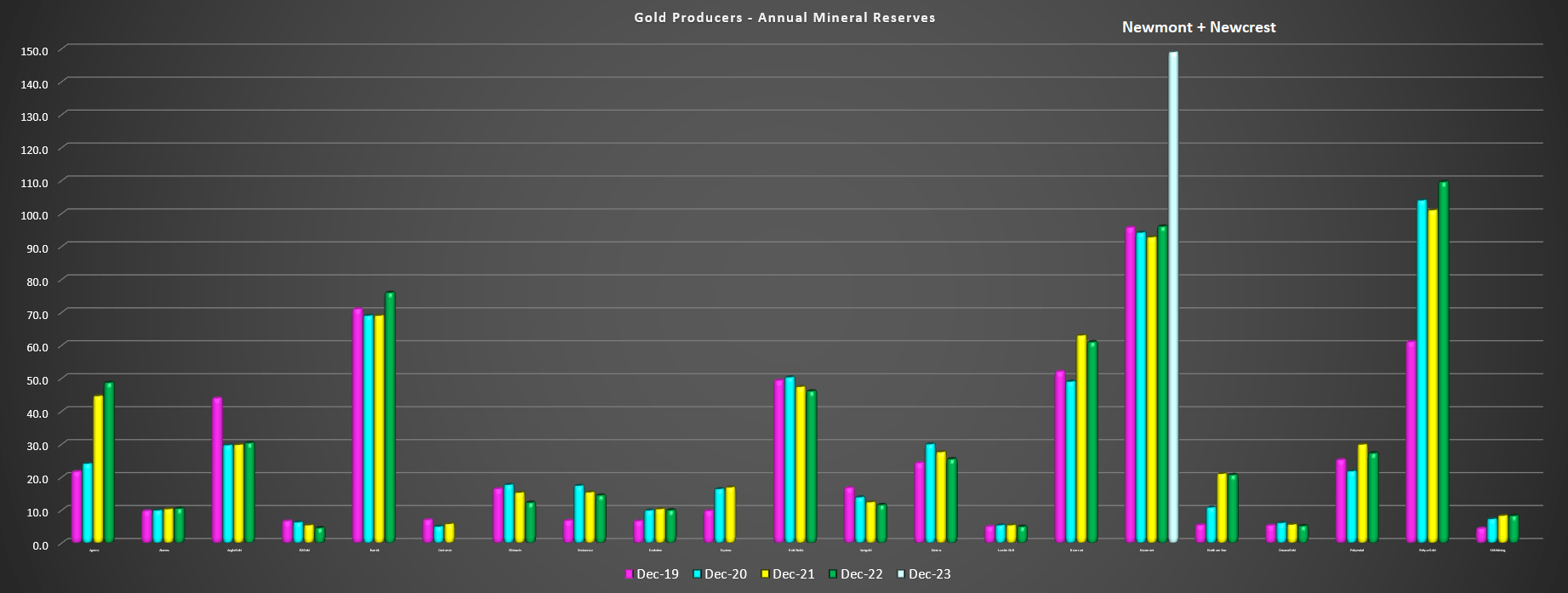

Looking at the above chart, we can see Newcrest's quarterly gold production profile dating back three years, and just below is Newmont's production profile if Newcrest were included in the portfolio. As shown, Newmont would see a significant increase in diversification with 20 assets (NGM joint-venture has multiple mining complexes but shown as one) vs. 14 previously, and the Newcrest assets would be some of the largest, with Lihir and Cadia being top-5 assets by total production next to Penasquito, Newmont's share in the NGM joint-venture, and Boddington. Meanwhile, from a jurisdictional standpoint, Newmont would see a slight improvement in its jurisdictional profile, with ~60% of Newcrest's production coming from Tier-1 ranked jurisdictions. Lastly, its reserve would grow materially, with an added ~53 million ounces of attributable gold reserves, and ~17 billion pounds of attributable copper reserves.

Newcrest Reserve Base (Newcrest Presentation) Newmont + Newcrest - Gold Reserve Base (Company Filings, Author's Chart)

{kind=link}

{kind=link}

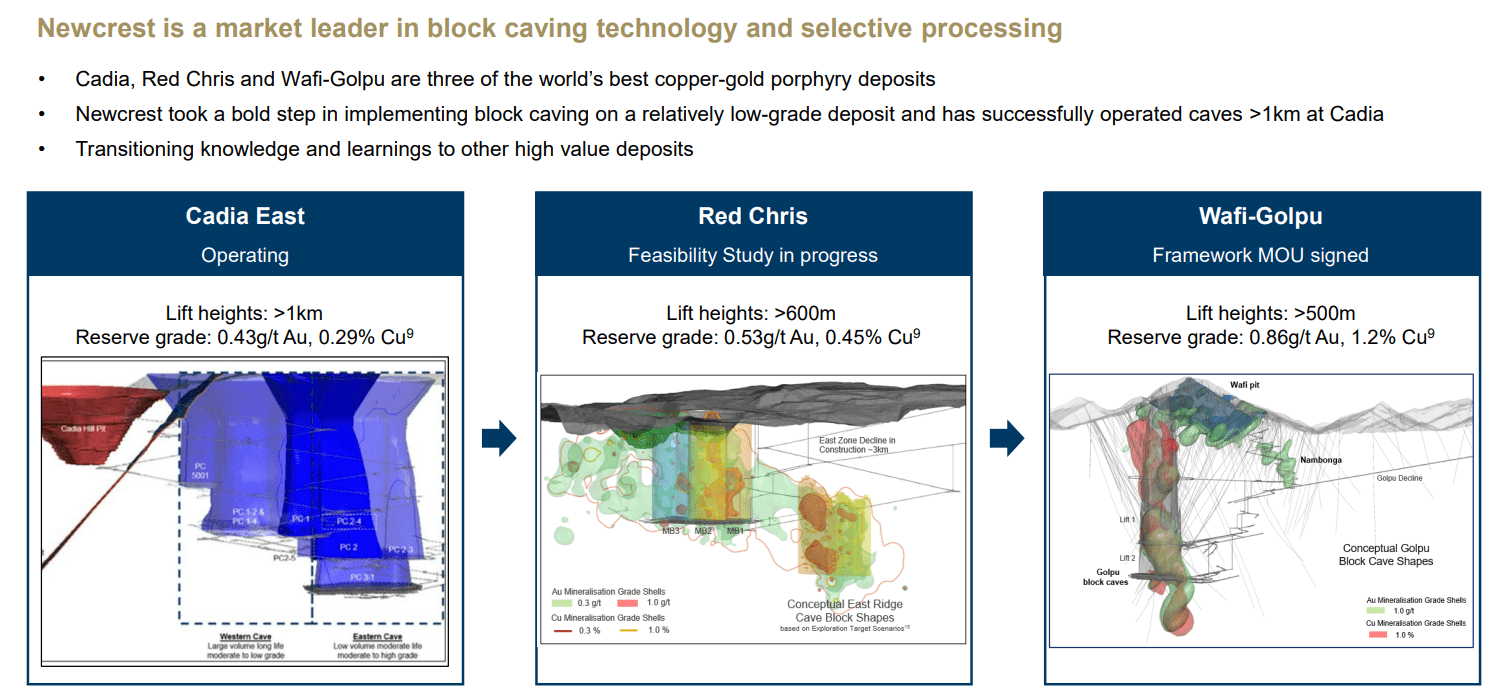

In addition to the material increase in production and reserves, Newmont will bring key block caving technology in-house with the addition of Newcrest, with the ultimate plan for Newcrest being to implement its block-caving expertise at Wafi-Golpu and Red Chris. This is because block caving provides the ability to exploit resources that are typically uneconomic due to being too deep for an open pit, but too low-grade for typical conventional underground mining methods. However, with block cave operations, costs are much more competitive, with costs below $30.00/tonne milled, a fraction of the ~$140.00/tonne milled for underground material at NGM's Carlin Complex.

So, with many of the best ore bodies already being discovered or in the hands of other majors, adding this technical expertise with one operating mine (Cadia) and two development projects gives Newmont the ability to significantly improve its cost profile vs. peers without relying on finding 1.0 ounce per tonne underground assets or one-quarter of an ounce per tonne open-pit assets that would be required to enjoy a similar operating cost profile.

Newcrest - Block Caving Technology (Newcrest Presentation)

{kind=link}

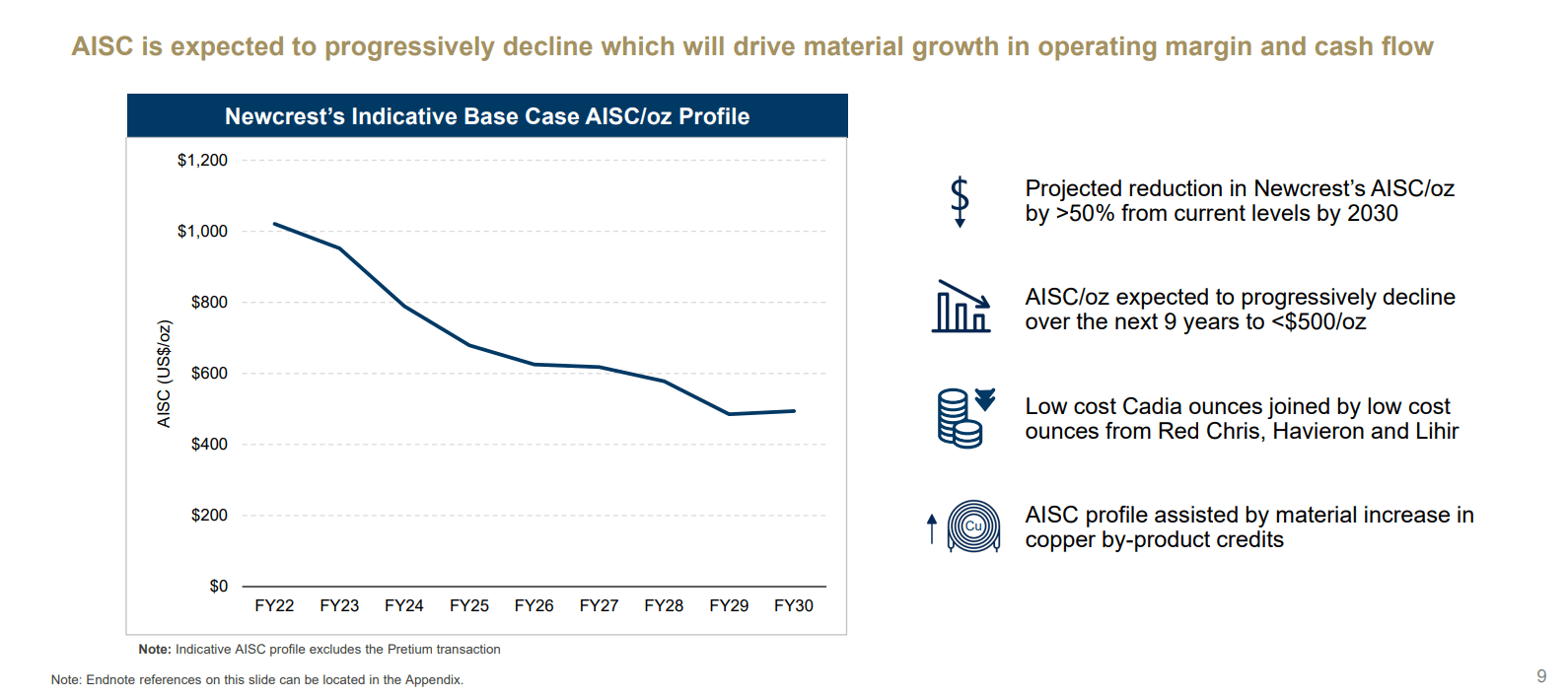

Finally, while Newmont will grow production (8.0+ million ounces of gold production), reserves (~150 million ounces of gold reserves) and add multiple new 350,000+ ounce per annum assets (Lihir, Cadia, Brucejack), the key benefit of this acquisition will come from a margin standpoint. This is because Newcrest already has one of the lowest cost profiles sector-wide and as of H2-2021, it was projecting a 50% reduction in all-in sustaining costs looking out to 2030. This was expected to be achieved by the addition of Red Chris Block Cave, low-cost ounces from Havieron (sub $800/oz AISC even assuming no throughput expansion), and an improving cost profile from Lihir. These projections were certainly ambitious, but even if we assume Newcrest was able to pull AISC below $850/oz by FY2025 and $775/oz by FY2030, this would lead to a dramatic improvement in Newmont's consolidated costs.

Newcrest - Indicative Base Case AISC Profile (ex-Brucejack) (Newcrest Presentation)

{kind=link}

As it stands, Newmont looks to be on track to report ~$1,250/oz AISC this year due to continued inflationary pressures, but even assuming higher costs at Penasquito due to the recent strike, I would expect Newmont's all-in sustaining costs on a stand-alone basis to improve to $1,140/oz or lower in 2025 with lower costs at Tanami and initial production from the high-margin Ahafo North Mine. However, this ~6.1 million ounce production profile at ~$1,140/oz AISC in 2025 could end up being ~8.0 - 8.2 million ounces of annual production at ~$1,040/oz with Newcrest, with further margin gains to come once Havieron and Red Chris are online, regardless of whether its stake in Fruta Del Norte is divested.

However, towards the end of the decade, with two mines online (assuming Red Chris Block Cave is approved) with negative all-in sustaining costs with by-product credits (Red Chris Block Cave, Cadia), it wouldn't be unreasonable to assume that Newcrest could meet 50% to 60% of its goal even when adjusting for the impact of inflationary pressures. This would translate to one-fourth of Newmont's gold production profile coming at costs more than 40% below the industry average, resulting in Newmont's all-in sustaining cost profile being closer to $1,000/oz potentially. This would give it one of the lowest-cost profiles sector-wide, hence why I believe it makes sense to ignore its current cost profile which is being impacted by elevated sustaining capital, what appear to be near-peak inflationary pressures, and a softer year from a production standpoint with no benefit yet from two higher-margin operations (Tanami Expansion, Ahafo North), and Newcrest's higher-margin portfolio.

Possible Portfolio Optimization?

With 20 total producing assets (3 being non-managed = Fruta Del Norte, Nevada Gold Mines, and Pueblo Viejo) and 17 managed assets with four of these assets producing less than 250,000 ounces of gold per annum (CC&V, Red Chris, Musselwhite, Fruta Del Norte), a case could be made for portfolio optimization with Newmont being spread a little thin and adopting a high-capex portfolio given that Newcrest had multiple major projects either started or in the wings (Havieron, Red Chris Block Cave, Cadia PC1-2, Brucejack optimization, Lihir Phase 14A). This could mean divesting its stake in Fruta Del Norte, and it could also mean looking at divesting what might be considered non-core assets (similar to what it did following the Goldcorp deal by selling its Continental Gold stake plus half of KCGM and Red Lake) and potentially re-sequencing some projects.

Given that Newmont is working through construction of its new Ahafo North Mine, contemplating a layback at Pamour, and also working through construction of its Tanami Expansion plus taking on a very busy Newcrest portfolio, it isn't likely to try to do everything all at once, and as we've seen from the company, it pays attention to execution risk and only taking on so many major projects at once. In addition, the company noted in its Q1 Conference Call that one of its key philosophies is value over volume , and that this would apply if the transaction is successful. So, while free cash flow could be pressured near-term with both companies having elevated capital expenditures in 2024, some portfolio rationalization and re-sequencing wouldn't surprise me. Even if free cash flow was pressured near-term, the company will be a cash flow machine later this decade, especially if it green-lights Red Chris Block Cave.

Newcrest - Red Chris Block Cave PFS Expected Production (Newcrest Website)

{kind=link}

Red Chris Block Cave is expected to produce ~150,000 ounces of gold and ~50,000 tonnes of copper at negative $100/oz all-in sustaining costs even assuming a conservative copper price of $3.30/lb over its mine life, with production of ~316,000 ounces of gold and ~80,000 tonnes per annum of copper from FY2029 to FY2034.

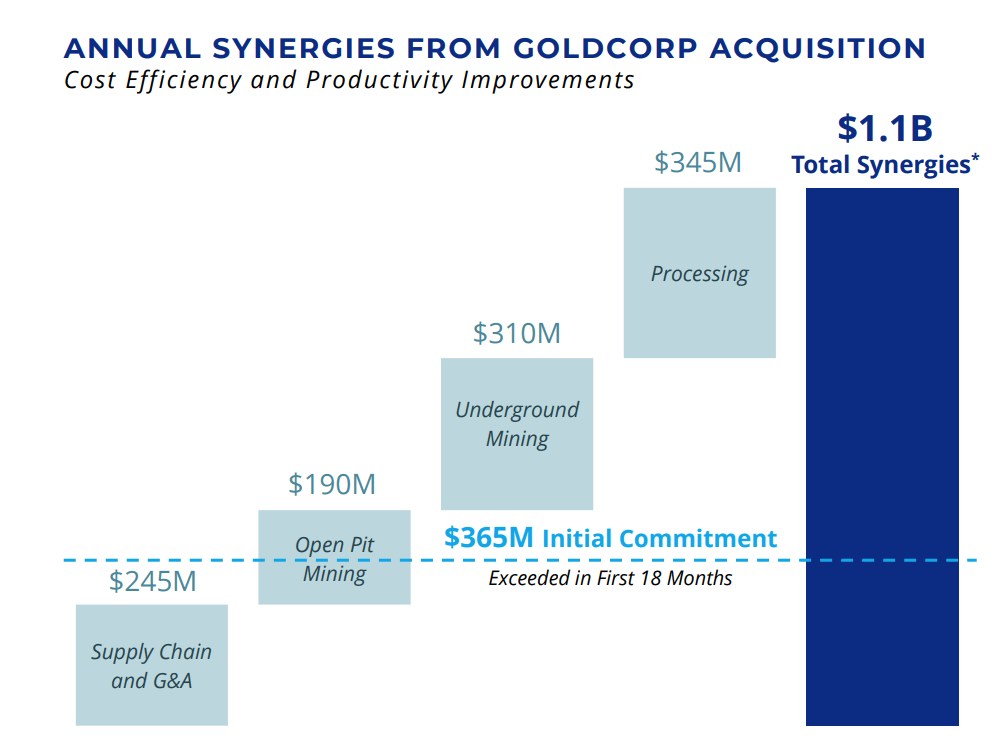

The last point worth noting is that Newmont is targeting $500 million in annual synergies from G&A, supply chain, and its full potential program, and it trounced its estimated synergies by ~200% in the Goldcorp transaction, delivering $1.1 billion in total synergies, above its $365 million initial commitment, helped primarily by mining and processing improvements. So, in addition to possible proceeds from portfolio optimization ($2.2 billion following Goldcorp transaction within 12 months), Newmont will benefit from significant annual synergies, and I would expect them to beat their target once again, with the company certainly being conservative in its most recent major transaction on upside that it might be able to unlock with its Full Potential improvements.

Annual Synergies from Goldcorp Acquisition (Newmont Presentation)

{kind=link}

Let's dig into Newmont's valuation and see whether investors are getting an attractive entry point into the stock despite the premium price being paid for Newcrest and the expected share dilution.

Valuation

Based on an estimated ~1.20 billion shares outstanding following the deal closure and a share price of US$41.00, Newmont would trade at a market cap of ~$49.2 billion, extending its lead by a wide margin vs. its two largest peers. And while this might seem like a rich valuation for Newmont today, I think it's worth looking at what the company will look like with the addition of Newcrest and once margins improve materially in FY2025 on a Newmont-only basis (Ahafo North, Tanami Expansion).

Based on the current production profiles and assumes no significant divestments, Newmont 2.0 would generate nearly $20.0 billion in revenue and upwards of $7.0 billion in operating cash flow, or ~$3.3 billion in free cash flow (assuming $3.7 billion in capex during this more capex-heavy period). Plus, and as noted earlier, it would move from being a high-cost million-ounce producer to one of the lowest-cost million ounce producers (and the largest) with a slightly more attractive jurisdictional profile.

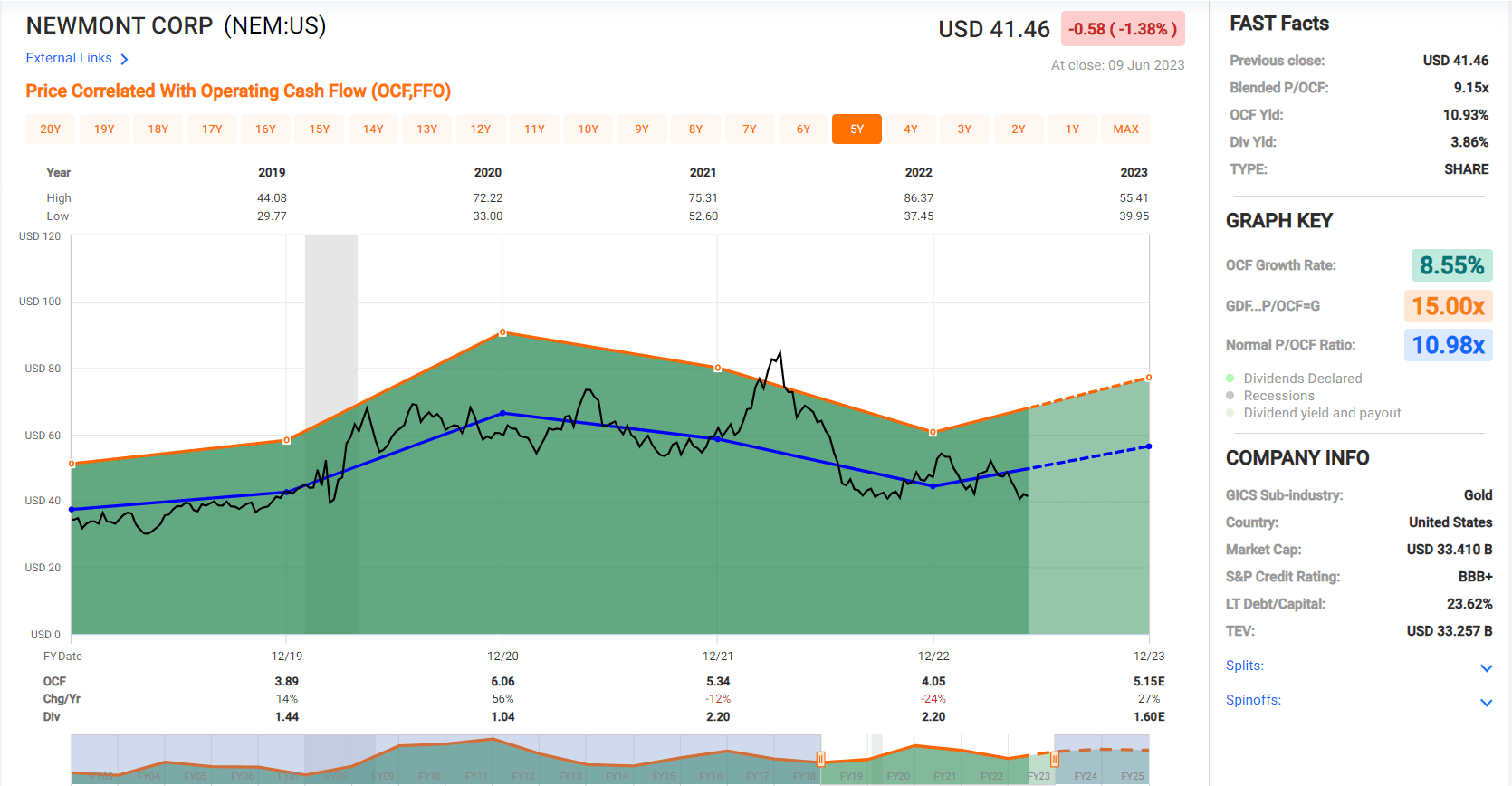

Newmont - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

As the chart above shows, Newmont has traded at an average cash flow multiple of 11.0 over the past five years, which I would argue is a very reasonable multiple for the world's largest gold producer with over 50% of its production coming from Tier-1 ranked jurisdictions. However, with Newmont's margins set to improve, its reserve base set to improve with three of the world's longest-life gold mines in its portfolio (Lihir, Cadia, Red Chris Block Cave), and its jurisdictional profile set to improve (an incremental ~1.2 million ounces of gold coming from Tier-1 ranked jurisdictions), I would argue that a fair cash flow multiple for Newmont is 11.5x - 12.0x, a slight premium to its 5-year average. And assuming the combined entity generates ~$7.2 billion in cash flow in FY2025 ($6.00 per share), and if we use the low end of this range (11.5x), this would translate to a fair value of US$69.00 (2-year price target).

And while Newmont will add three of the world's longest life mines if the Newcrest deal successfully goes through, it could arguably add five , with the 9-year mine life (2021 PFS) at Havieron based on just ~14 million tonnes of material (updated reserve base estimating ~25 million tonnes of material, with the potential for this to grow to ~40 million tonnes assuming continued exploration success) suggesting the possibility of a 13+ plus year mine life even with a potential throughput expansion to ~3.0 million tonnes per annum.

Elsewhere, the shared Wafi-Golpu Project envisions a 27-year mine life. While it may not head into production until 2031 or later, the project continues to make progress, with an MOU signed earlier this year with the independent state of Papua New Guinea.

Havieron - Exploration Success (Newcrest Website)

{kind=link}

Lastly, while Newmont 2.0 will be a completely different company by 2025, the longer-term future of the company is even brighter ,as highlighted above, with the potential for Newmont 2.0 to compete with low-cost producers from a margin standpoint. In fact, Newmont could Newmont from a $1,250/oz AISC producer in 2023 to a ~$1,040/oz producer in 2025 and a path to becoming a ~$1,000/oz gold producer by the end of the decade, even using more conservative copper price assumptions. So, while some investors might look at Newmont today as a relatively high-cost producer compared to million-ounce miner peers, a look into the future suggests that Newmont 2.0 will be a leaner and meaner company, with a portfolio of multiple world-class Tier-1 scale assets. This should command a premium, and that certainly isn't reflected in the stock today with it trading at ~6.8x FY2025 cash flow per share estimates.

Summary

It's been difficult to justify an investment in Newmont until recently. It traded at a premium to many of its peers, it was in a higher-capex period, and it was having a harder time keeping a lid on costs relative to Agnico Eagle ( AEM ), which was benefiting from Kirkland Lake transaction synergies and the addition of three low-cost assets (Detour Lake, Fosterville, Macassa).

However, the Newcrest Mining Limited acquisition is transformational for Newmont Corporation. It should help Newmont to enjoy meaningful margin expansion from 2023-2025 with the addition of Newcrest's assets. This is a big deal in a sector where miners are struggling to claw back margins. I would expect this to help to bring Newmont back in favor after a year of severe underperformance since it hit its April 2022 peak. Hence, I would view any Newmont Corporation stock pullbacks below US$40.40 as low-risk buying opportunities.

For further details see:

Newcrest Deal: Solidifying Newmont's Position As The Largest Gold Producer