NLCP - NewLake Capital Partners: I Don't See The Underpricing Here

Summary

- NewLake Capital Partners is a REIT that leases real estate assets to state-licensed cannabis operators.

- The company faces risks from potential regulation changes in the cannabis industry and the declining financial health of its tenants.

- Notwithstanding its high dividend yield and low P/FFO multiple, I do not find NLCP to be trading at a discount to its intrinsic value.

Despite having a dividend yield of 7.8% and a forward P/FFO multiple of 11.6x, both of which may sound compelling reasons to rate the stock a "Buy", I find NewLake Capital Partners ( NLCP ) to be fairly priced at the current price of $18.4/ share. The price falls within the range of my intrinsic valuations done using a traditional DCF approach and a net asset value approach. Adding on the risks of industry regulations and potential tenant defaults, I assign NLCP a "Hold" rating currently.

Company Overview

NewLake Capital Partners, Inc. is a triple-net equity REIT, providing real estate assets to state-licensed cannabis operators. It acquires industrial and retail properties through sale-leaseback transactions, 3rd party purchases and built-to-suit projects. NLCP was founded in 2019, merged with GreenAcreage in March 2021 and went public in August 2021.

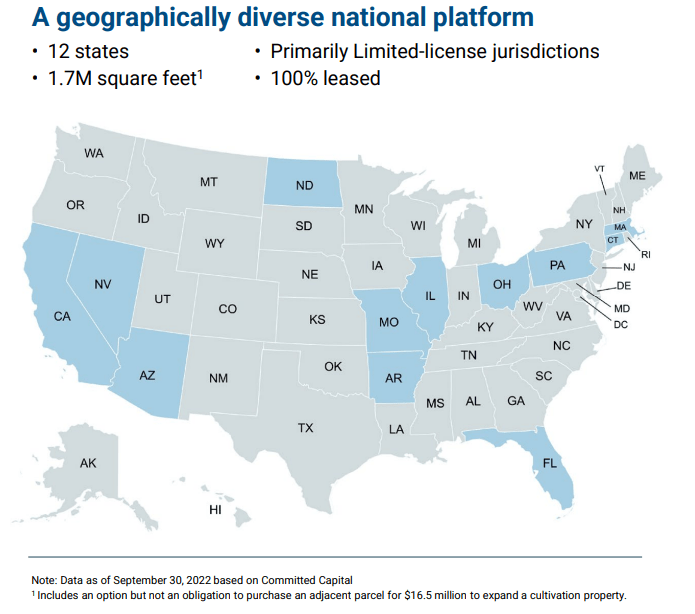

The company focuses on states limited cannabis licensing jurisdictions. Presently, it owns 31 properties totaling 1.7 million sq. ft. across these 12 states - CT, MA, PA, NV, MO, CA, IL, FL, ND, OH, AR, AZ. It has committed a capital of just over $420 million towards these properties.

Geographic footprint of NLCP properties (NLCP Investor Presentation)

{kind=link}

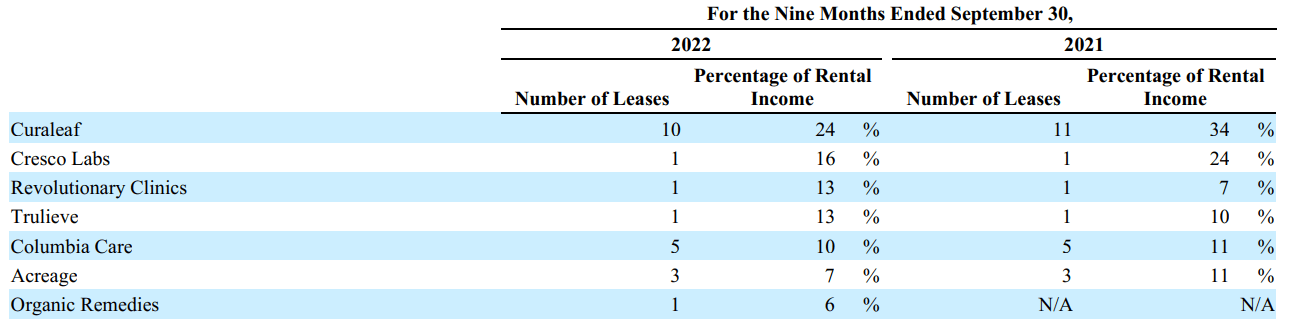

In terms of its current tenants, NLCP is heavily concentrated. For nine months ending September 30, 2022, its top 5 tenants account for 76% of its revenues . 65% of its tenants are public companies and the remainder 35% are private enterprises. Its weighted average yield of portfolio is 12.2%, with an average lease term of 14.9 years. 92% of NLCP tenants are cultivators and 8% are engaged in retail operations. Presently, it has been able to collect 100% of rent from its tenants. NLCP appears to be financially healthy at the moment, with only ~$3 million in debt and about $45 million in cash (primarily from its IPO).

Major customers (NLCP Q3 2022 10-Q)

{kind=link}

Industry Overview

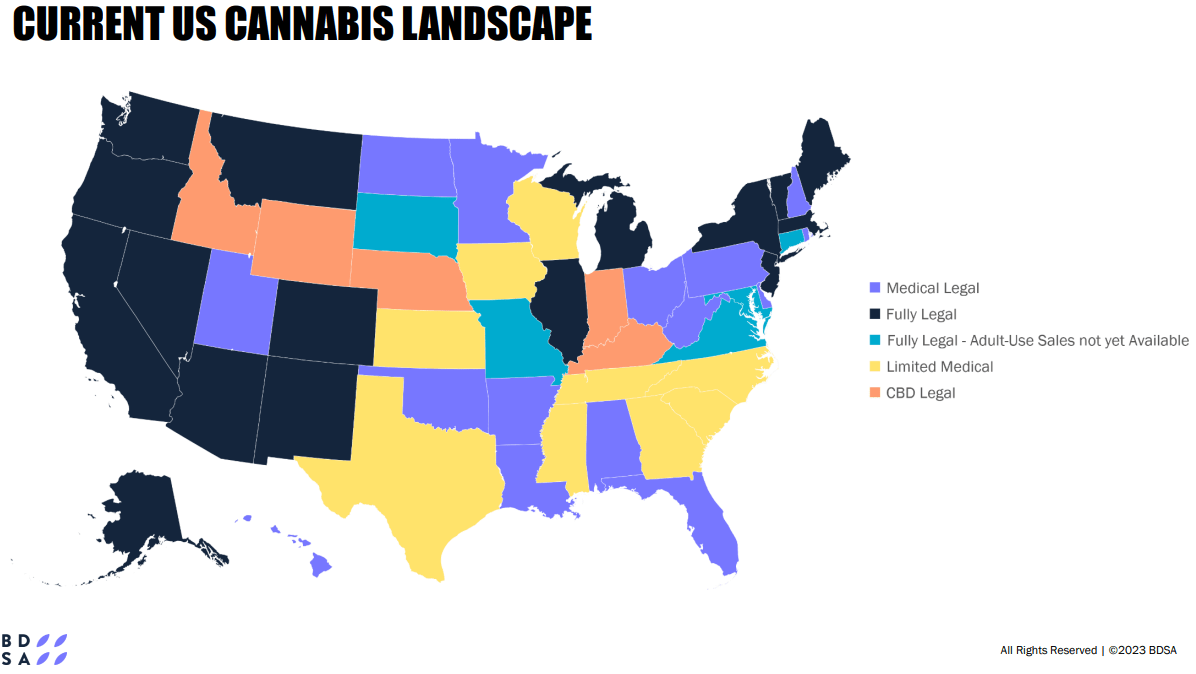

In the US, products derived from the cannabis plant are regulated under both federal and state law. On the federal level, marijuana is regulated under the Controlled Substances Act, making it illegal for use in medicinal or recreational applications. However, a majority of states have relaxed state law prohibitions to allow the use of cannabis products for medicinal or recreational purposes. Presently, 39 states have legalized cannabis for medicinal use and 21 for recreational use by adults. I reckon more states will continue to relax their prohibitions to allow some form of cannabis legalization. There has been some traction on the federal level legislations as well, though no concrete roadmap has emerged thus far. Hence, marijuana transport across state borders remains illegal currently. This lends favorability to cannabis industry REITs since the tenants will need to have cultivation facilities in the states they wish to sell.

BDSA predictions for the Cannabis industry, 2023 (BDSA)

{kind=link}

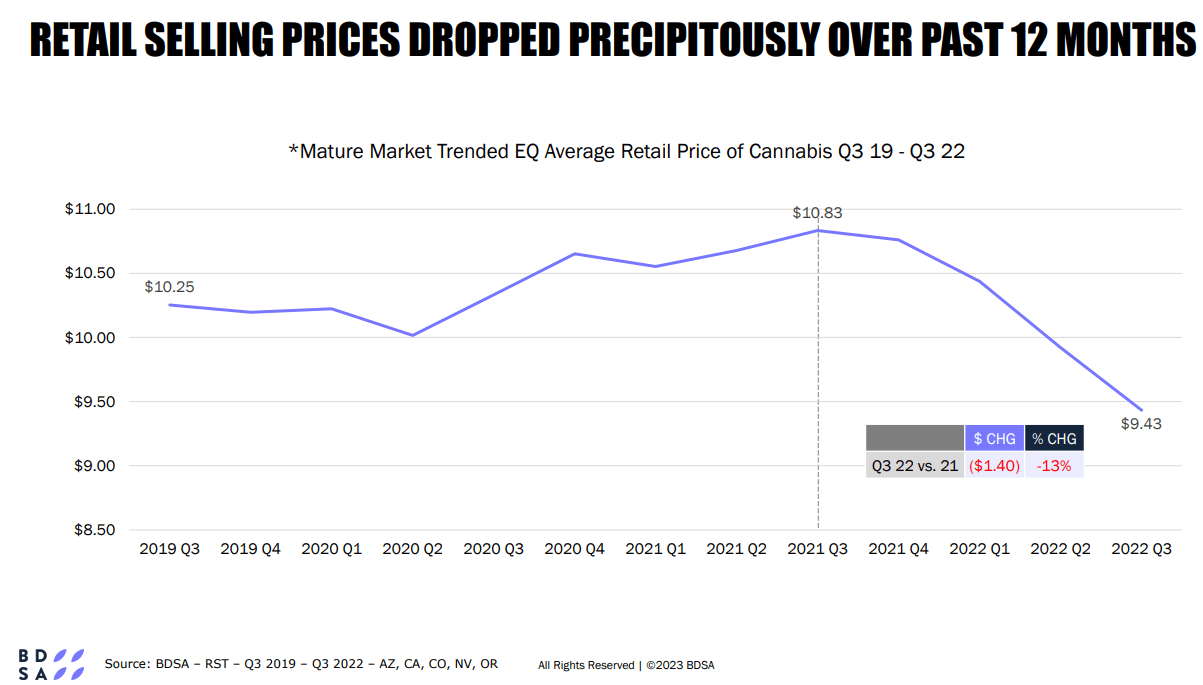

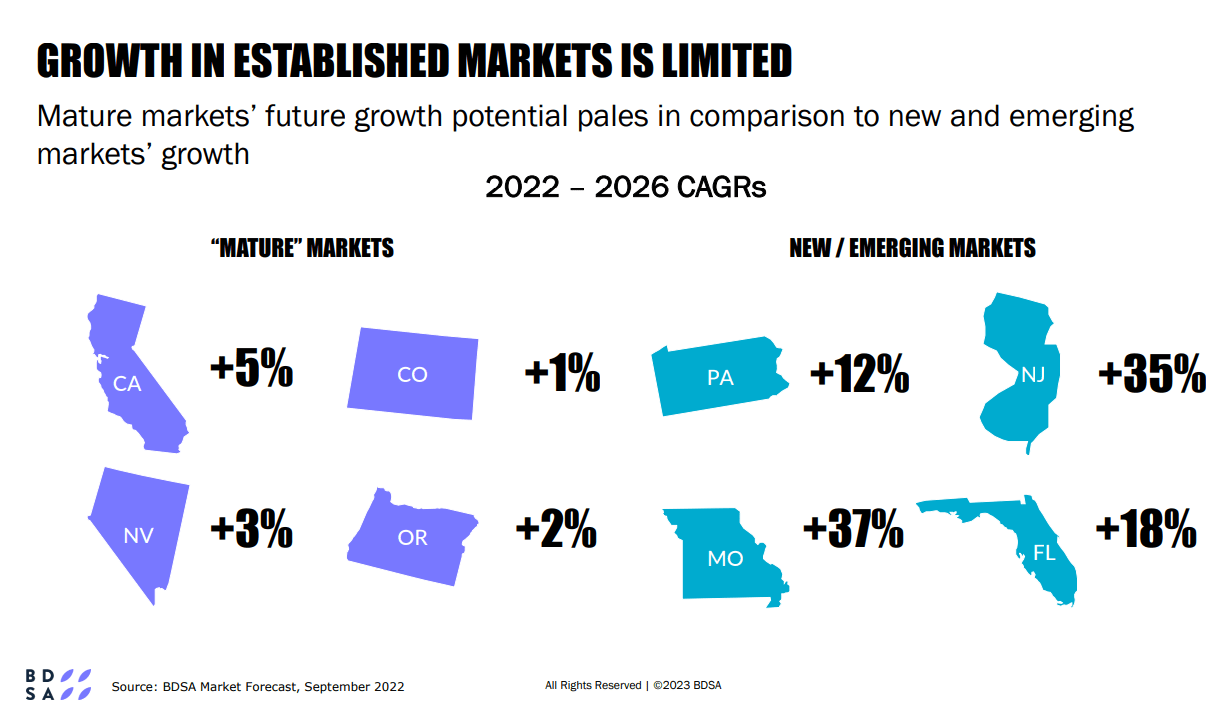

According to BDSA , global legal cannabis spending grew only 4.8% in 2022. Primary reason for this slowing growth has been the rapid price decline in the cannabis market as seen below. BDSA forecasts a CAGR of 13.2% from 2022 to 2027, with US sales expected to grow 14% in 2023. Most of the growth is projected to come from developing markets , particularly MO, NJ and NY. Strong growth is also expected in FL, IL, MA and MI while stunted growth is expected in mature markets like CA, CO, NV and OR.

{kind=link}

{kind=link}

NLCP already has presence in some of the high growth states like PA, FL and MO. It may need to acquire properties in other emerging states like NJ and NY, in order to sustain a high revenue growth rate in the near term. Overall, I think this picture bodes well for NLCP.

My Valuation of NLCP

Since NLCP is a REIT, I valued it using two methods - a Free Cash Flow to Equity ((FCFE)) method and a Net Asset Value ((NAV)) method. Further, I did a relative comparison of NLCP against its larger peer, Innovative Industrial Properties ( IIPR ). I wanted to include AFC Gamma ( AFCG ) , Power REIT ( PW ) and Chicago Atlantic Real Estate Finance ( REFI ) in the relative analysis as well, but I could not find the requisite and reliable data on these to offer a worthwhile comparison.

Free Cash Flow to Equity Valuation

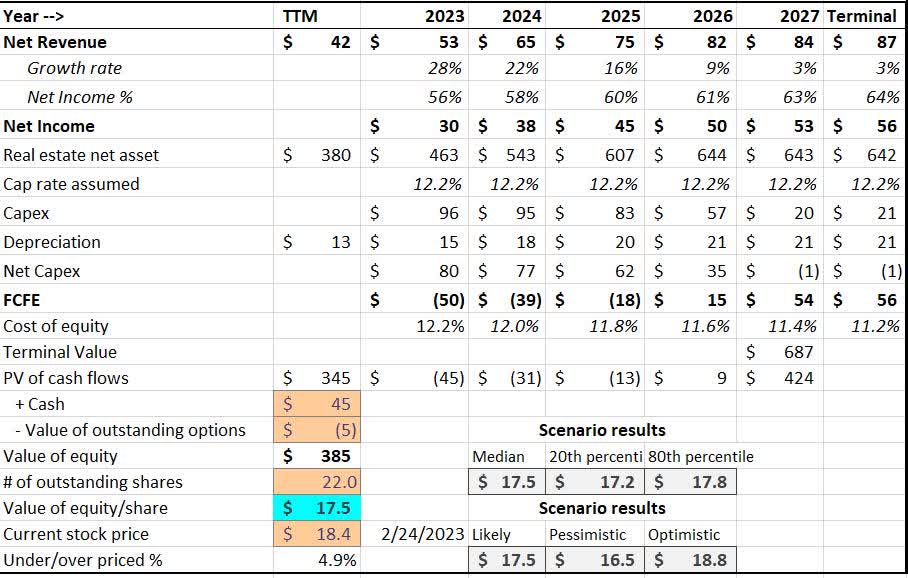

This was set-up as a traditional discounted cash flow model, using free cash flow to equity investors and a computed cost of equity. With NLCP being relatively small in size, I assume it will grow at a higher rate than industry expected CAGR of 13.2%. I start with a revenue growth rate of 28% for next twelve months, slowing to a rate of 3% over the course of next 5 years. This translates into a CAGR of 14.5% across these 5 years. I also assume SG&A costs, as a % of revenues, gradually reduce from current 15% to 12% since these costs are largely fixed and should not go up materially with increase in number of properties. Their current due diligence process of vetting properties and tenants is likely to be maintained, which means it's fair to assume a constant cap rate of 12.2% (same as current).

I computed the cost of equity as 12.2%. While this is fairly standard computation using current risk-free rate, equity risk premium and beta for the stock. Beta deserves some attention here. With its limited public history, the 24-month beta for NLCP is 0.37. I find this to be artificially low. Median beta for industrial REITs, which are much more stable, is 0.61. A more appropriate proxy would be to use the unlevered beta for IIPR and lever it up for NLCP. I believe this represents the risk of being a cannabis REIT more aptly. Using this approach, I get a beta of 1.48 for NLCP. I realize this can be contentious and I would welcome other thoughts on this.

Using these inputs, my valuation below results in an equity value of $17.5/share. This is about 5% lower than the current price.

FCFE Valuation Model ($ million)

FCFE Valuation Model (Author's analysis)

{kind=link}

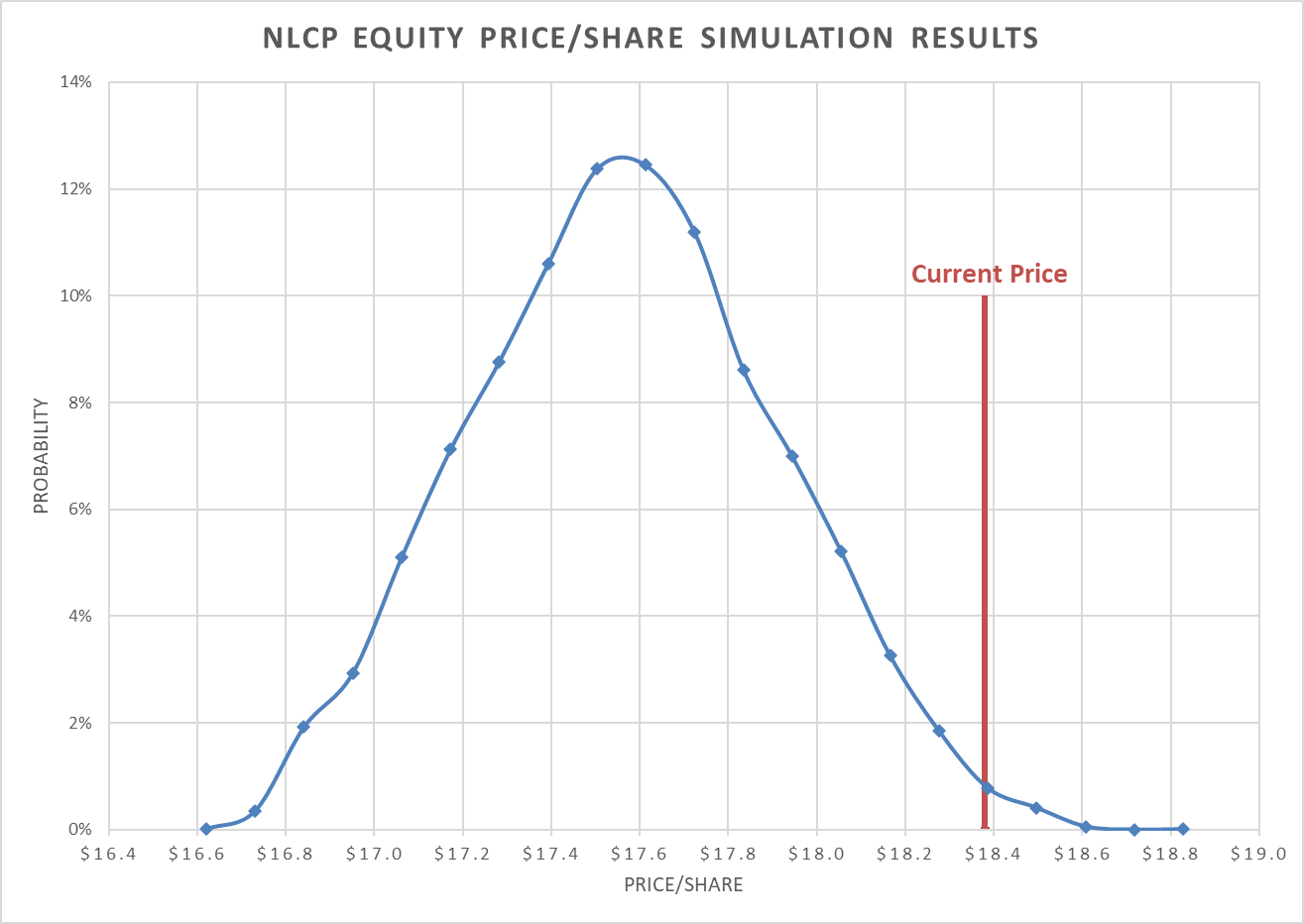

Simulation Results

Results from the DCF model are highly dependent on the key assumptions outlined earlier. Changing these assumptions and the associated storylines would results in materially different valuation results. Terminal revenues (or revenue growth rate) and final cap rates are the key variables here. Monte Carlo simulations were run on the DCF model with these two inputs as variables, with their values being picked from distributions shown in the table below. A set of 10,000 random iterations were performed and the results from this simulation are shown in the figure below.

Input Variables for Simulation

| Variable |

| Distribution |

| Baseline |

| Min |

| Max |

| Std. Dev. |

| Initial revenue growth rate |

| Normal |

| 28% |

| 3% |

| Terminal cap rate |

| Triangular |

| 12.2% |

| 11.2% |

| 13.2% |

Frequency Plot of Intrinsic Valuation from Monte Carlo Simulation

MonteCarlo simulation results (Author's analysis)

{kind=link}

My range for intrinsic value lies in tight band from 20th percentile of $17.2 to the 80th percentile of $17.8. With NLCP trading at $18.4 at close on 2/24/23, it lies at around the 99th percentile.

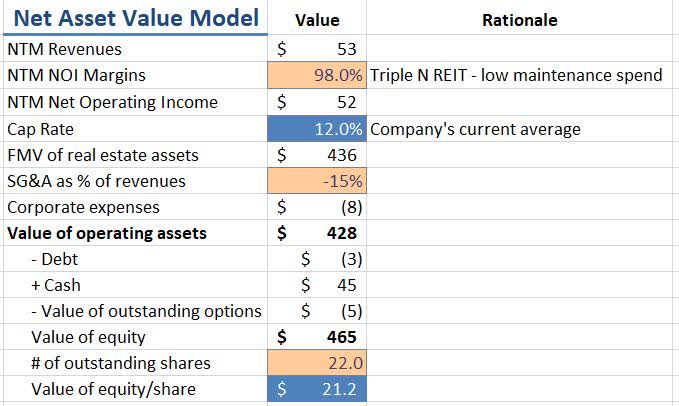

Net Asset Valuation

Assuming the same growth rate as in the FCFE model, I use the projected NTM revenues of $53 million. Since NLCP operates on a triple-net lease model, its maintenance expenses should be rather low. Therefore, I assume 98% of these revenues go towards it net operating income. Assuming the current average cap rate of ~12% is going to hold, I get a value of $21.2/ share for NLCP, which is about 15% than its current price.

Net Asset Valuation (Author's analysis)

{kind=link}

Relative Pricing

I compare NLCP and IIPR below on their fundamental and pricing metrics. NLCP has a higher multiple on both P/AFFO and P/FFO compared to IIPR. This can be justified based on the higher expected EPS growth rate and lower beta (due to lower debt ratio) of NLCP. So, I do not find any mispricing here.

Relative valuation (Author's analysis)

{kind=link}

Risks

There are some risks, both industry centric and company specific, that deserve some thought.

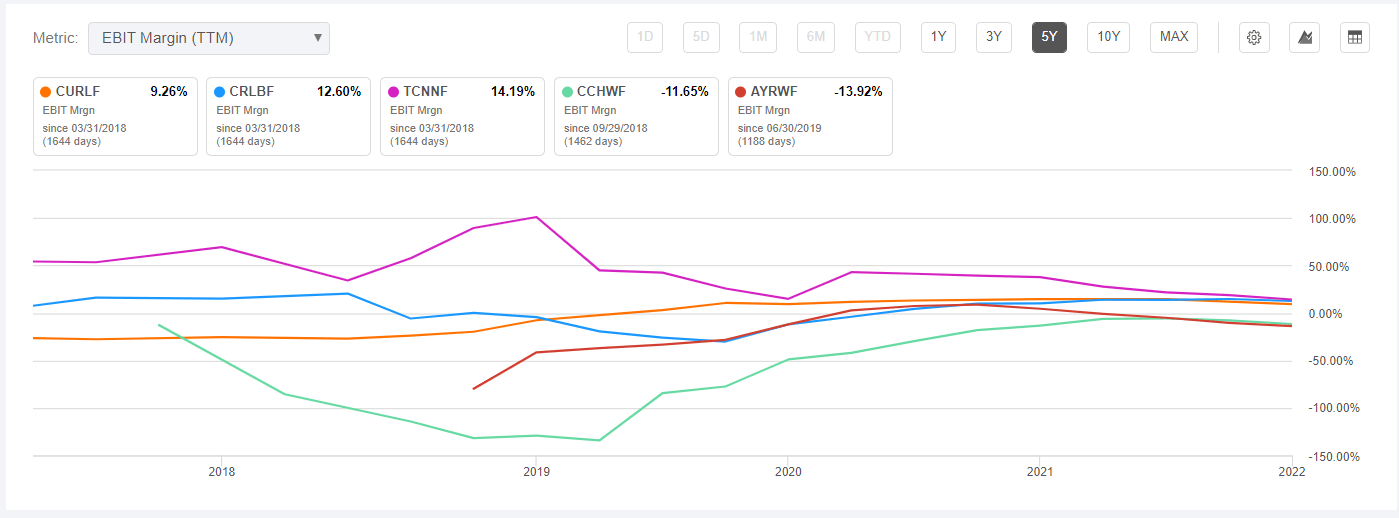

Tenant concentration and default risk - As previously mentioned, NLCP has a high concentration of tenants - top 5 tenants made up 76% of revenues for the first nine months of 2022. This tenant concentration risk is exacerbated by the fact many tenants have limited operating histories. As of now, none of the tenants have defaulted on their rents. However, given the general economic conditions, regulatory environment, their current indebtedness, and the decline in cannabis market prices, risk of default remains tangible. Looking at the historic EBIT margins of 5 of their major public tenants, the general decline in operating margins of these companies is evident. Therefore, I feel there is some risk of default here on rent payments from their tenants. Since these properties are hard to repurpose for non-cannabis operators, this risk could manifest itself in reduced rental income and/or properties remaining vacant for some time. Note that I have assumed 100% occupancy and no rental defaults in my valuations, so this risk has not been explicitly accounted for in the value computed.

{kind=link}

Federal legalization - While federal legalization of marijuana has encountered many setbacks, the idea has been gaining traction in the general public. I think the impact of federal legalization on a cannabis REIT like NLCP could have both positive and negative consequences. On the plus side, such legalization may pave way for a new growth wave in the cannabis industry, which would increase market demand for cannabis related real estate. On the other hand, it may spur changes in financial regulations (see below) that would materially deteriorate the landscape for current capital providers to the industry (the REITs).

Potential banking regulations - The Secure and Fair Banking Act ((SAFE)) was designed to protect financial institutions from penalties for lending to cannabis businesses. While this act has not been passed in Congress yet, if and when such an act is passed, it would allow traditional financial companies like banks to be a competitive source of capital for the cannabis operators. This would have a detrimental effect on the REITs operating in the sector, including NLCP by lowering the cap rates they may be able charge their tenants.

Liquidity - Note that NLCP trades on the OTC exchange currently. Hence, liquidity in the stock is relatively low. Until it gets listed on a major stock exchange, like its larger rival IIPR, investors might have to continue to pay this illiquidity discount. Its listing on a major exchange, however, can certainly act as a catalyst for its stock price to increase.

Conclusion

Several SA authors have rated NewLake Capital Partners as a "Buy" or a "Strong Buy". Primarily, their arguments rest on the current high dividend yield and the P/FFO (or similar) multiple at which the stock trades at. Based on my valuation, however, I find NLCP to be fairly priced currently to its intrinsic value. Therefore, I assign a "Hold" rating on it. With the trifecta of federal legalization, banking regulations, and increasing default risk of its tenants added to the thesis, I would seek a margin of safety to invest here. At a 20% margin of safety, I suggest an entry price of $14 or lower, similar to where it was trading in early Q4 of 2022.

For further details see:

NewLake Capital Partners: I Don't See The Underpricing Here