NLCP - NewLake Capital Partners: The Best Risk/Reward For 2023

Summary

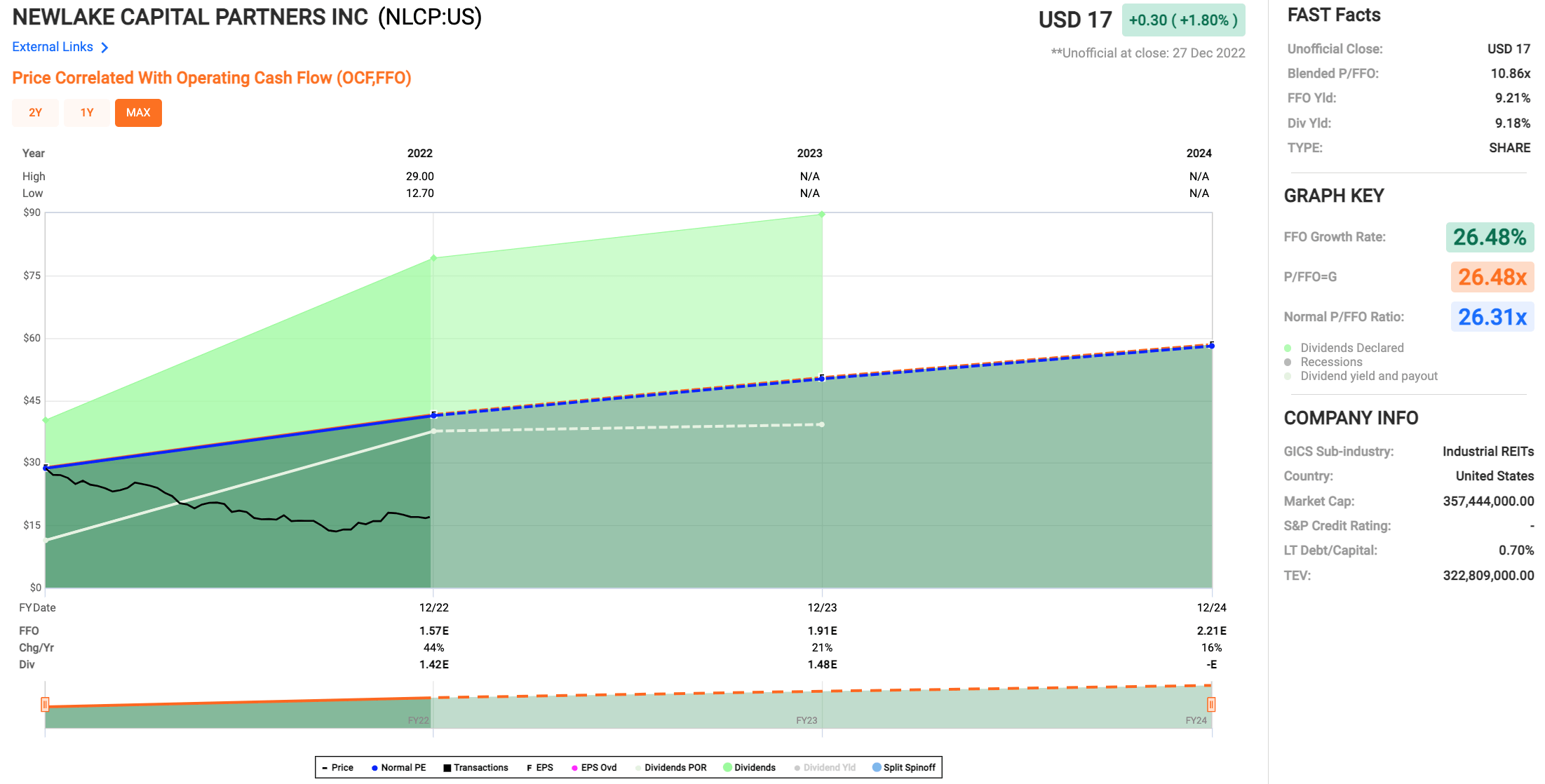

- NewLake Capital Partners is a small cap cannabis REIT with a market cap of $370. Despite strong fundamentals, shares are down over 40% YTD.

- Shares are dirt cheap at a price/FFO of 10.9x, which is cheaper than big brother IIPR's valuation, despite superior growth prospects.

- The yield sits above 9% after the most recent 5.4% dividend hike. The company also has a $10M buyback authorization which could take out over 2% of shares.

- I also discuss why I sold other REITs focused on the cannabis sector to add to my position in NewLake Capital Partners.

- NewLake Capital Partners started as a small position for me in 2021, but I have been adding aggressively in recent weeks and it is now my third largest position.

Over the last couple months, I have been cutting companies out of my portfolio and shrinking my number of holdings. Today I will be writing on NewLake Capital Partners ( NLCP ), a cannabis REIT that I have been buying pieces of for most of 2022. As long as shares are below $20, I think the risk/reward is very skewed to the upside.

Investment Thesis

NewLake Capital Partners is a small cap cannabis REIT with a market cap of $364M. The REIT has been able to put together an impressive portfolio of assets with double digit cap rates and rent escalators well over 2%. In the past I have focused on NewLake’s quarterly results and updates, but today I will be focusing on my justification for selling the other cannabis REITs to put the proceeds into buying more shares of NLCP.

The main problem with shares that I see is that they are traded OTC. It’s not a problem for small investors like myself (I tend to buy 100 shares at a time), but it has prevented some of the bigger players from investing. Shares are dirt cheap today at a price/FFO of 10.9x. This is cheaper than big brother Innovative Industrial Properties ( IIPR ), despite better growth prospects. The dividend has been hiked every quarter since going public, and the current yield is 9.2%. I have been adding in recent weeks and shares look like a strong buy below $20 to me.

Consolidating My Cannabis REIT Holdings

The first holdings I sold were the cannabis mortgage REITs, Advanced Flower Capital Gamma ( AFCG ) and Chicago Atlantic Real Estate Finance ( REFI ). While I’m still bullish on these two REITs due to mismatch in supply and demand for capital available to cannabis companies, there are a couple reasons I decided to sell both to reinvest in NewLake. The first is the external management of both REITs. I have touched on this in previous articles on both REITs ( here and here ), but all else being equal, external management is usually a drag on investor returns. The other reason is that I think NewLake has way more upside for long-term investors than the mortgage REITs, even if the risk/reward is still favorable for those two REITs.

The other one I decided to sell more recently is Innovative Industrial Properties, the largest cannabis REIT available to public investors. The main advantage to IIPR is that it is listed on the NYSE, which means it is more liquid than NewLake and has easier access to equity capital. It also allows many of the larger institutions to invest, as some are restricted from investing in OTC stocks. As a side note, investors should use limit orders when buying shares of NLCP, especially for larger transactions. Shares can be volatile, and they routinely move 2% or more in a day, so be prepared if you are buying shares for the first time. There are a couple other things that factored into this decision.

The first is that I think NewLake has a better portfolio of assets than IIPR due to its laser focus on restricted license states. I like IIPR’s strategy, but despite NewLake’s smaller size, I like the potential for their portfolio and its ability to generate impressive long term returns due to double digit cap rates and rent escalators of 2-3%. I also prefer NewLake’s balance sheet, which has no debt besides a revolving line of credit with a 5.65% interest rate and a capacity of $90M. IIPR also has a good balance sheet, but they also have a 9% preferred stock ( IIPR.PA ), which isn’t a huge issue, but all else being equal, I would rather not see it since they should be able to borrow or issue shares with better spreads to reinvest in acquisitions.

If I could simplify all of that into one concept, it comes down to opportunity cost. Every dollar invested in the other cannabis REITs is a dollar that could be invested in NewLake, and since I think the risk/reward is by far the best option of the four REITs, I decided to sell the others to add to my NewLake position. However, I still think the others should be able to generate solid returns due to the cheap valuations and large dividends.

I also think it is only a matter of time before NewLake can list its shares on a major exchange. I have talked about this in more detail in a previous article, but an uplisting should be a major catalyst for shares. It might take financial regulatory reform related to the cannabis industry at the federal level, but when it does happen, money should flow into NewLake due to the cheap valuation and sizable dividend.

Valuation

NewLake is dirt cheap today at a price/FFO of 10.9x. The normal multiple isn’t much help due to its short record as a public company, but I think multiple expansion is going to help lead to impressive returns over the next couple years. While IIPR is cheap as well at a price/FFO of 13.2x, NewLake has much better growth prospects due to its smaller size. IIPR doesn’t have nearly the same growth runway at a market cap just under $3B, and their FFO/share growth has been slowing over the last couple years.

{kind=link}

Part of the thing that has hurt the share price since the IPO is the rough market environment. Risk assets across the board have had a rough year, and NewLake is no exception. It’s not surprising that a volatile small cap like NewLake has had a large decline over 40% YTD, despite strong underlying fundamentals. I think it’s a reasonable thesis that we could see NewLake shares appreciate to the point where the yield is closer to 5-6% range, putting shares well above $20, all while paying a growing dividend.

Another Dividend Hike & Buybacks

NewLake announced another dividend hike, a 5.4% increase from $0.37 to $0.39. If you assume there won’t be any more dividend hikes for the next year (something that is highly unlikely in my opinion), that puts the forward yield at 9.2%. I wouldn’t be surprised to see NewLake continue to hike its dividend at a rapid rate for years to come. With a market cap of $364M and 31 properties in the real estate portfolio, they have plenty of room for future growth, especially considering the high margin nature of the business and the impressive lease terms of the portfolio. In addition to all the reasons I listed above, the superior potential for dividend growth is another reason I chose to sell the other cannabis REITs.

While both mortgage REITs have had impressive dividend growth since their IPOs, they didn’t hike their most recent quarterly payout. I will keep an eye on both since I think it’s an interesting sector, but I think NewLake has the runway for consistent dividend hikes and better risk/reward as an equity REIT compared to the mortgage REITs. IIPR, which had some of the best dividend growth out there since the IPO, has also slowed down their dividend growth. They have opted for raises every other quarter, and the most recent hike was only 3% , from a quarterly payout of $1.75 to $1.80.

Another thing that sets NewLake apart from the other cannabis REITs is their recently announced buyback program. It is a $10M buyback authorization that they announced a couple months ago with the Q3 results. If they use the whole program at current prices, they would be able to buyback well over 2% of the outstanding shares. I’ll be waiting patiently for the 10-K, because I’m curious to see if they started buying back shares in Q4. Due to the company’s small size, I would rather see them prioritize new acquisitions if they can be done at favorable terms, but I can’t complain about buybacks, especially if shares drop from here and put the yield over 10%.

Conclusion

My first purchase of NewLake Capital Partners was near the end of 2021, and it was mainly a flier to keep an eye on the company to see if it could mirror Innovative Industrial Properties’ growth as a publicly traded REIT. Since then, I have been buying in pieces all the way down and have added aggressively in recent weeks, and it is now my third largest position overall. While I’m still bullish on the other cannabis REITs, which also have cheap valuations and big dividends, I think NewLake represents the best opportunity. I listed out several reasons why I swapped the other REITs for shares of NLCP, but I can summarize it like this: Would I rather own AFCG, REFI, and IIPR, or should I sell those to buy more shares of NLCP?

As I thought about it, the answer became clear to me. The valuation is dirt cheap at a price/FFO of 10.9x, and you get paid over 9% to wait. Throw in a buyback program that could take out over 2% of shares, and it’s hard for me to see a reason to be bearish on NLCP. The OTC listing isn’t ideal, but it has created this opportunity for small investors like myself, and to me it looks like a fat pitch that doesn’t come around very often. As long as the price is below $20, shares look like a strong buy today.

Some investors have mentioned the idea that IIPR could make an offer to acquire NLCP, and while that would probably bring significant short-term gain, I would be very disappointed because I think the long-term upside for shareholders of NLCP is huge. Investors can look at NewLake as speculative due to its small size and the fact that it is a cannabis REIT, but I can’t think of many speculations with a 9% dividend, strong fundamentals, and a cheap valuation to boot. We will see how 2023 plays out, but I think impressive returns could be in store for investors in NewLake Capital Partners for years to come.

For further details see:

NewLake Capital Partners: The Best Risk/Reward For 2023