NLCP - NewLake Capital Partners: Updating To 'Buy'

2023-08-14 18:41:14 ET

Summary

- NLCP stock has dropped 28% since February 2023 due to increased risk perception and tenant delinquency.

- Encouraging signs include share repurchases and discussions of exchange listing, leading to an undervalued stock with an 11.7% dividend yield.

- Based on my updated intrinsic and relative valuations, I find NLCP to be undervalued by about 20%. Hence, I am upgrading my prior “Hold” guidance to a “Buy”.

I had previously done a full valuation of NewLake Capital Partners ( OTCQX:NLCP ) in February 2023. The stock was trading at $18.4/share at the time and I found it to be fairly priced, with my valuation at $17.5/share. Consequently, I assigned a "Hold" rating to it at that point with my "Buy" trigger being at $14/share.

With more than 2 quarters since the initial evaluations, there have been some significant developments in the cannabis industry and at NewLake Capital Partners in particular that warranted me to take another look at NLCP. In this update, I expound on these changes and re-value NLCP stock in the wake of these developments. I find the stock to be an attractive "Buy" now, trading below its intrinsic value and relative value. The cherry on top is the current dividend yield of 11.7%

Stark price drop amidst modest risk increase

Since my last valuation in February 2023, NLCP stock price has dropped 28%, from $18.4 to $13.2. Some of this is due to an increase in risk perception given some of the recent developments.

Tenant delinquency

As I called out in my first valuation, one of the risks for NLCP was a default risk from their tenants given their highly concentrated portfolio with tenants who have had limited operating history. Coincidentally, Revolutionary Clinics, one of NLCP's tenants, has in fact defaulted. It has not paid any rent in either Q1 or Q2 of 2023. In each quarter, NLCP applied a portion of their deposits (approx. $315K each quarter) towards the rent, resulting in a revenue shortfall of ~$1MM/quarter. The good news, if any, in this is that the NLCP believes these issues with the tenant are temporary, and it hopes to long-term solution with this tenant by the end of Q3. This solution, in my opinion, may involve concessions in the form of payment delays, partial payments etc.

Slight decrease in US Cannabis market growth projections

According to the latest report from BDSA released in June 2023 , the legal US Cannabis market is expected to grow 12% in 2023, reaching $29.6B. Further, it is forecast to grow to $45B by 2027, representing a CAGR of 11.2%. This contrasts to the 11.3% CAGR projected by BDSA in February 2023 .

SAFE Banking Act passed in the House

Another one of the risks I had outlined previously has manifested itself, albeit partially. The SAFE Banking Act was passed in the House on July 14th. Among other provisions, this would allow banks to provide services to cannabis businesses, which I believe, would result in lower margins for cannabis REITs like NLCP. However, it is important to note that the bill is unlikely to be included in the Senate version of the National Defense Authorization Act or NDAA. While the risk remains, the Senate seems to be still reluctant on this proposal.

Encouraging signs from stock repurchase and listing discussions

Despite these risks, there are some encouraging signs emerging as well for NLCP.

Share repurchase

In FY2023, management embarked on their share repurchase plan. So far, they have repurchased approximately 105,000 shares at an average price of $12.62. This bodes well as the company seems to be making judicious use of its capital to repurchase stock when it has been depressed.

Initial talks of exchange listing

During the prepared remarks in Q2 2023 earnings call, CEO Anthony Coniglio referenced that NLCP has been watching the developments at TerrAscend ( OTCQX:TSNDF ). TerrAscend is a leading vertically integrated cannabis producer in the US, which has licensed production in Canada as well. TerrAscend has disclosed plans to get listed on the TSX exchange in Canada and is taking all the necessary steps in this direction. While it may require restructuring and/or some sort of operational presence in Canada for NewLake to follow this path, the very fact that they seem serious about getting listed on a major exchange is encouraging. Further, I think it would be a boost to NLCP if TerrAscend is able to complete its listing on TSX successfully.

Updated Valuation of NLCP shows undervalued stock

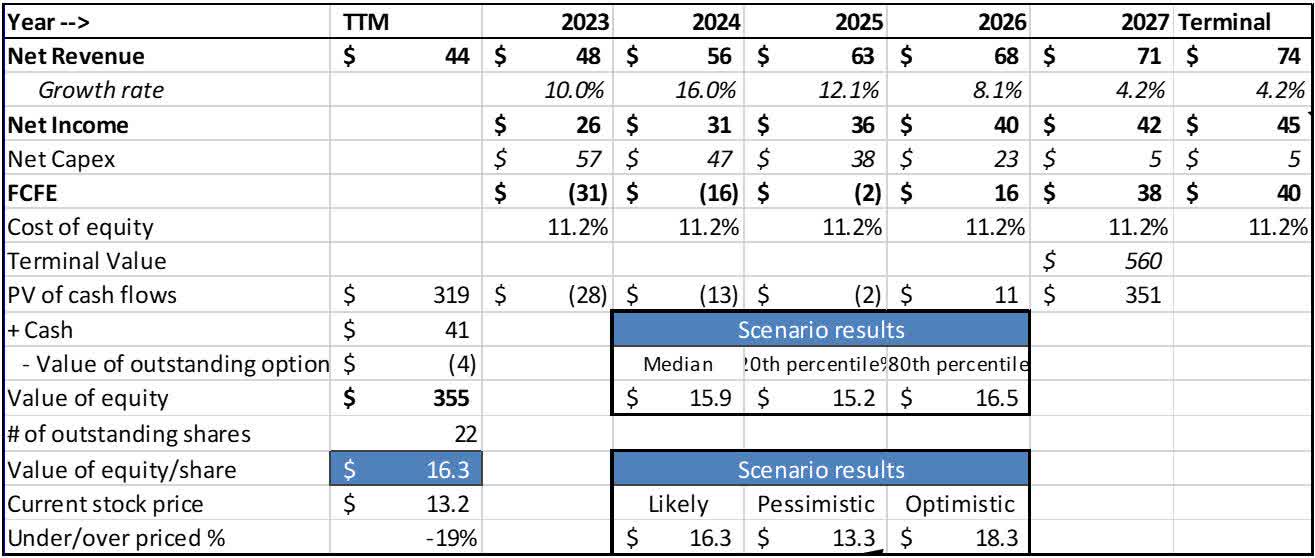

In light of the above developments, I updated my valuation of NewLake. I incorporated these important changes into my valuation inputs. As before, I valued NLCP using two methods - a Free Cash Flow to Equity ((FCFE)) method and a Net Asset Value ((NAV)) method. Further, I did a relative comparison of NLCP against its larger peer, Innovative Industrial Properties ( IIPR ).

Free Cash Flow to Equity Valuation

I made the following updates to my last valuation model that I ran in Feb. 2023:

- Revenue growth rate lowered to 13% CAGR - Considering the recent lower than projected revenue growth of NLCP, I lowered my projections from 14.5% CAGR to 13% CAGR (slightly higher than industry average). Furthermore, considering the delinquency of Revolutionary Clinics over the last 2 quarters which has been a hit of approximately $1M per quarter, I further lowered the revenue growth for NTM to just 10%.

- Increased SG&A costs from 15% to 16% in accordance with recent performance. In the same vein, I increased the terminal SG&A costs from current 12% to 14%.

- Cost of equity lowered from 12.2% to 11.2% - This came from the lower equity risk premium in the market than before.

Using these inputs, my valuation resulted in an equity value of $16.3/share down from $17.5/share in Feb. 23. With the sharp decline in price to $13.2, I find the stock to be undervalued now by ~20%.

FCFE Valuation Model ($ million)

{kind=link}

Monte Carlo simulations were run on the updated valuation model with the following inputs as variables, with their values being picked from distributions shown in the table below. A set of 10,000 random iterations were performed and the results from this simulation are shown in the figure below.

Input Variables for Simulation

| Variable |

| Distribution |

| Baseline |

| Min |

| Max |

| Std. Dev. |

| IIPR |

| 10% |

| 1.65 |

| 10.1 |

| 11.0 |

| 9.5 |

| 10.1 |

| NLCP |

| 13% |

| 1.47 |

| 10.7 |

| 11.8 |

| 7.1 |

| 7.3 |

Risks

As before, similar risks exist for NLCP that I had called out in my prior update. These include tenant concentration and default risk, federal legalization of marijuana, passing of the SAFE Banking Act by the Senate and liquidity in the stock. I would add another risk to this - that is of potential dividend reduction. However, given that the company is in a stock repurchase mode, I don't see it imminent anytime soon unless there is some material default amongst its tenants.

Conclusion

I find the recent stark drop is NLCP's stock price is an overreaction to the risks I have expounded upon. This makes NLCP a good buy at the current levels in my opinion. Though the intrinsic value of the stock has dropped approximately by $2 in my analysis, the drop in its price has been in excess of $5. My updated intrinsic valuation and relative valuation suggests that the stock is being undervalued right now by at least 20%. Therefore, I am updating my guidance from "Hold" to "Buy" at the current price level.

For further details see:

NewLake Capital Partners: Updating To 'Buy'