CA - Newmont: Ignore The Weak Q2 Results

2023-07-20 11:50:40 ET

Summary

- Newmont Corporation reported a softer Q2 than expected, with gold production down 17% YoY and all-in sustaining costs for its gold segment rising to $1,472/oz.

- Despite a challenging quarter, Newmont's future remains promising, especially if it can close the planned Newcrest acquisition.

- Given the bright future for Newmont and the fact that H1-2023 was a kitchen-sink period with a strong H2 on deck, I would view pullbacks below US$41.00 as buying opportunities.

The Q2 Earnings Season for the Gold Miners Index ( GDX ) has finally begun, and one of the first companies to report its Q2 2023 results is Newmont Corporation ( NEM ). Unfortunately, the company had a slightly softer quarter than I anticipated, even when factoring in the strike at Penasquito, reporting quarterly attributable production of ~1.24 million ounces of gold (down 17% year-over-year) and quarterly co-product gold-equivalent ounce production of ~256,000 ounces (down 22% year-over-year).

Making matters worse, all-in sustaining costs [AISC] for Newmont's gold segment spiked to $1,472/oz, and AISC margins sunk to $493/oz despite the benefit of a higher average realized gold price. That said, while the headline results were ugly, H2 2023 should be much better, and the company's future remains very bright if it can close the planned Newcrest Mining ( NCMGF ) acquisition. Let's take a look at the results below:

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q2 Production

Newmont released its Q2 results this week, reporting quarterly production of ~1.24 million ounces of gold and ~256,000 co-product gold-equivalent ounces [GEOs], representing a 17% and 22% decrease over the year-ago period. However, while the magnitude of these declines might seem alarming, it's important to note that the company was without one of its largest contributors for much of the quarter due to the unresolved strike at Penasquito. Two other major contributors where Newmont holds a minority interest (Pueblo Viejo and Nevada Gold Mines) also had a softer Q2. In Pueblo Viejo's case, tie-ins were being completed to place the finishing touches on a major expansion to 14.0 million tonnes per annum, setting the asset up to produce ~870,000 ounces in 2024 to 2027 on a 100% basis, translating to nearly 90,000 ounces per quarter attributable to Newmont, or 70% above its much softer Q2 2023 contribution (~51,000 ounces).

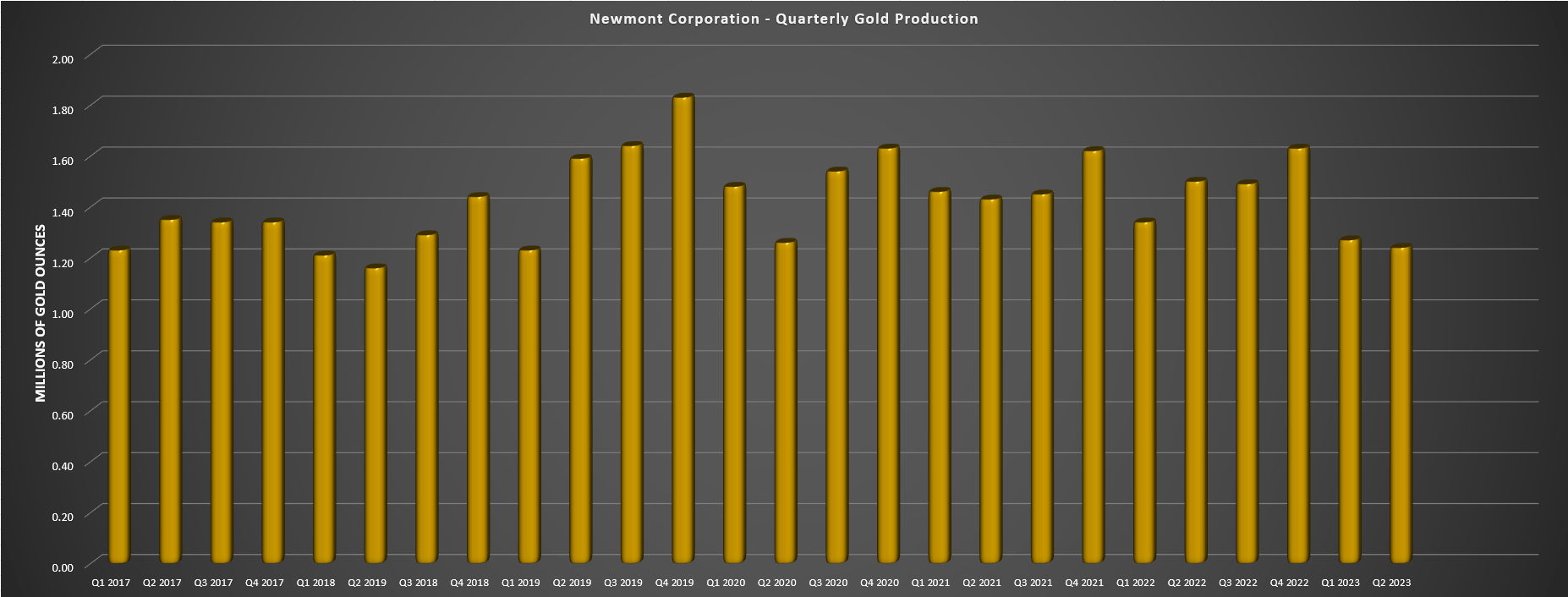

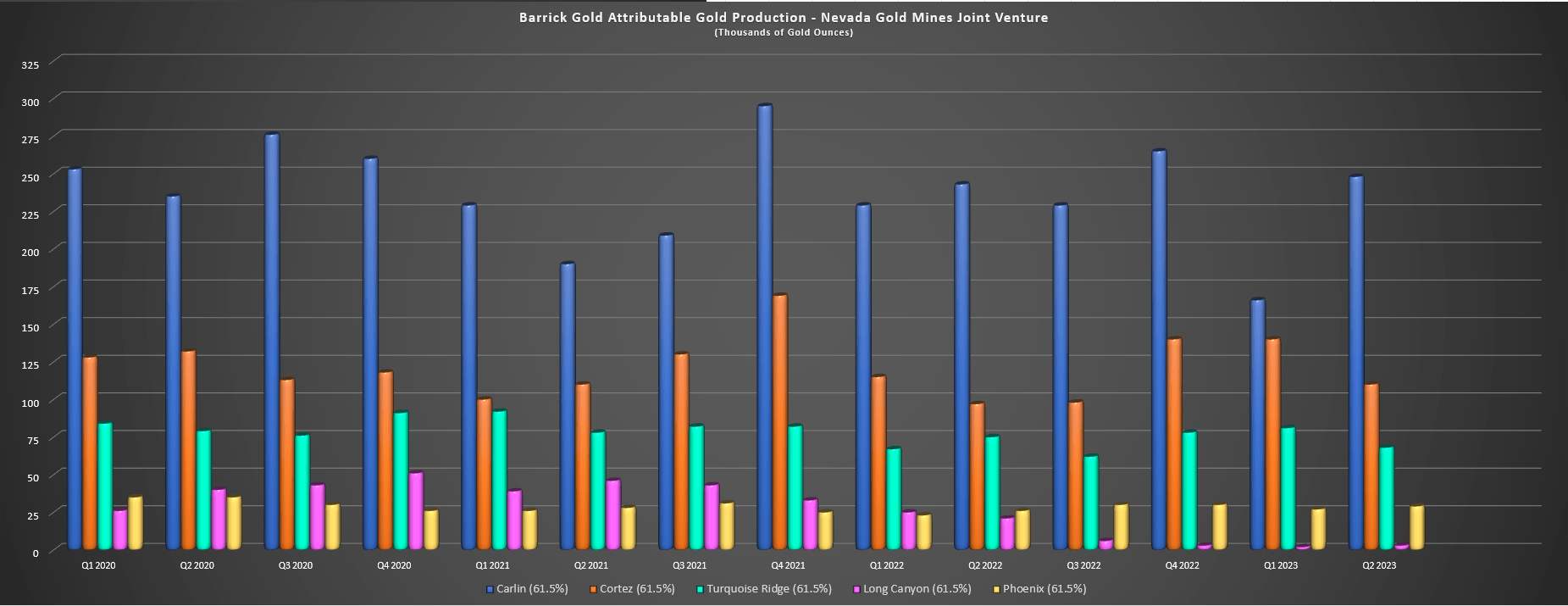

Newmont - Quarterly Gold Production (Company Filings, Author's Chart) Nevada Gold Mines Quarterly Gold Production (61.5%) Basis (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Moving over to Nevada Gold Mines, where Newmont holds a 38.5% interest, the Carlin Complex may have come roaring back in Q2 after a maintenance-heavy first four months of the year, but production was light at Cortez and Turquoise Ridge related to mine sequencing and autoclave maintenance, respectively. The result was that Newmont's interest in the Nevada Gold Mines JV contributed just ~287,000 ounces in Q2, over 4% below the three-year average attributable production of ~300,000 ounces. However, with the Goldrush ROD delayed and Robertson's first production on deck for 2027, Cortez Complex output will ramp up significantly later this decade at lower costs, helping Nevada Gold Mines to be a more material contributor that it has been in what was a very soft H1 2023.

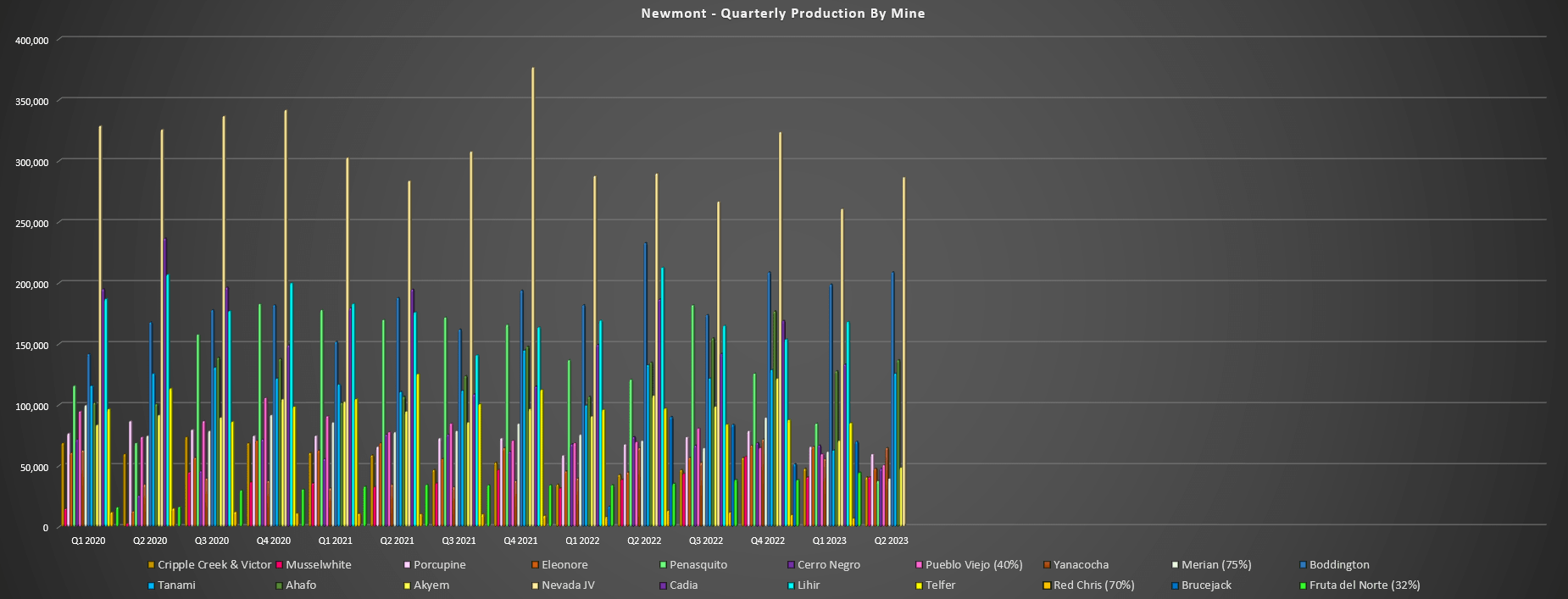

Newmont - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

Digging into Newmont's majority-owned portfolio, it was obviously a softer quarter at Penasquito due to the ongoing strike and planned lower gold grades due to the mining sequence (~38,000 ounces of gold produced vs. ~121,000 ounces in Q2 2022), which did not help from a cost or output standpoint given that Penasquito is one of Newmont's lower-cost assets. However, the performance at Eleonore wasn't great, either, with operations suspended temporarily to protect the workforce from the summer wildfires, and Cerro Negro also saw lower output to complete inspects in May, contributing to a weaker Q2 performance (~48,000 ounces vs. ~74,000 ounces). Finally, Penasquito's gold-equivalent production also fell off a cliff related to the strike, which impacted total sales, with GEO production of ~189,000 ounces, down from ~266,000 ounces in the year-ago period.

Finally, if we look across the rest of the portfolio, Tanami bounced back strong in Q2 with ~126,000 ounces produced, Ahafo had a monster quarter with ~137,000 ounces despite lapping tough comps from Q2 2022, and Yanacocha had a solid quarter with ~65,000 ounces produced. However, the outperformance from these assets wasn't able to offset significant declines in H1, which was largely signaled by Newmont and its partners by stating that it would have back-end weighted guidance in FY2023. So, while the ~2.51 million ounces produced might appear miles short of reiterated guidance of 5.7 to 6.3 million ounces of gold or the 6.0 million ounce guidance mid-point, H2-2023 should look entirely different with a big second half from Pueblo Viejo (expansion complete), higher grades from Subika Underground, Cerro Negro, and Tanami, and a strong H2 from Turquoise Ridge, Cortez, and Carlin.

Costs & Margins

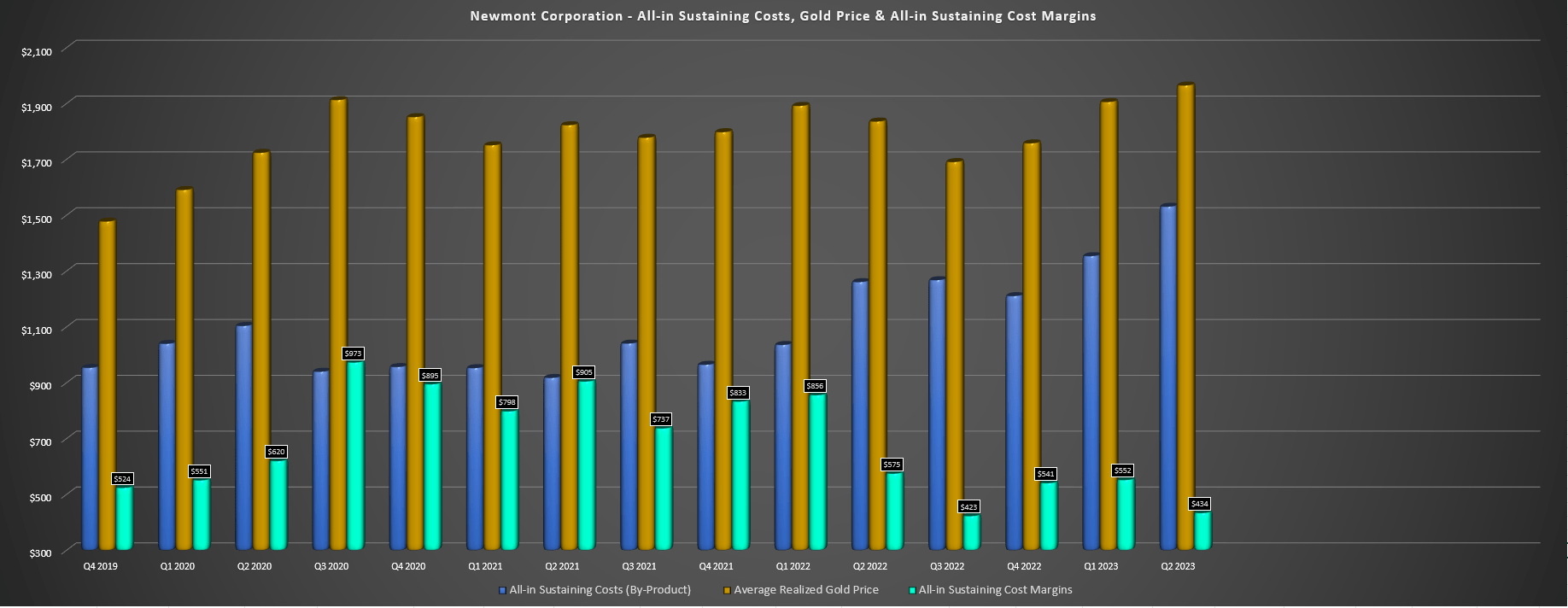

Moving over to Newmont's costs and margins, the headline results here were arguably even uglier, but there's a lot to unpack that contributed to these high unit costs, and reason to be optimistic going forward. Starting with the results, though, all-in sustaining costs came in at $1,472/oz (Q2 2022: $1,199/oz), impacted by higher sustaining capital spend at Boddington (five new autonomous haul trucks), Musselwhite (camp improvements), and Ahafo. Meanwhile, all-in sustaining costs on a by-product basis came in at $1,531/oz (Q2 2022: $1,261/oz), resulting in AISC margins on a by-product basis of just $434/oz despite the higher average realized gold price in the period ($1,965/oz). However, as discussed, lower-cost assets contributed less, sustaining capital was elevated in H1 due to timing of spend, and production was lower, all contributing to a spike in unit costs and an unfavorable setup from a cost standpoint.

Newmont - AISC (By-Product), Gold Price & AISC Margins (Company Filings, Author's Chart)

{kind=link}

The good news, though, is that Newmont noted that inflationary pressures have stabilized in the case of energy, fuel, and commodities, which confirms what Northern Star ( NESRF ) noted in its fiscal Q4 (CY-Q2) results. Hence, the worst of the inflationary pressures look to be behind the sector, suggesting that we have likely seen the worst of costs sector-wide for most producers with a better setup heading into H2-2023 and 2024. Plus, with a monster year from Pueblo Viejo in 2024 (one of Newmont's lowest cost contributors), what should be a trend of flat to lower sustaining capital vs. 2023 levels, and a return to more normal investment levels post-2024, it's likely that we're seeing trough margins and trough free cash flow generation for Newmont, with a much stronger 2024 and 2025 ahead even if we ignore the integration of Newcrest.

Unfortunately, the result of the lower sales and weaker margins combined with increased capital spending was that free cash flow fell off a cliff, coming in at $40 million, down from $514 million in the year-ago period. This led to trailing-twelve-month free cash flow crumbling to ~$300 million, down from ~$2.36 million at this time last year. That said, and as communicated earlier, this was a kitchen-sink quarter, and I would expect a much better second half of the year with the benefit of higher gold and silver prices, over 3.1 million ounces of annual gold production, and an improved cost profile with what should be slightly lower sustaining capital but significantly higher gold sales in the period. And from a bigger picture standpoint, the Newcrest acquisition will transform Newmont into a behemoth, with significantly higher margins and a near 10.0 million GEO profile.

Newcrest - Annual All-in Sustaining Costs (Company Filings, Author's Chart)

{kind=link}

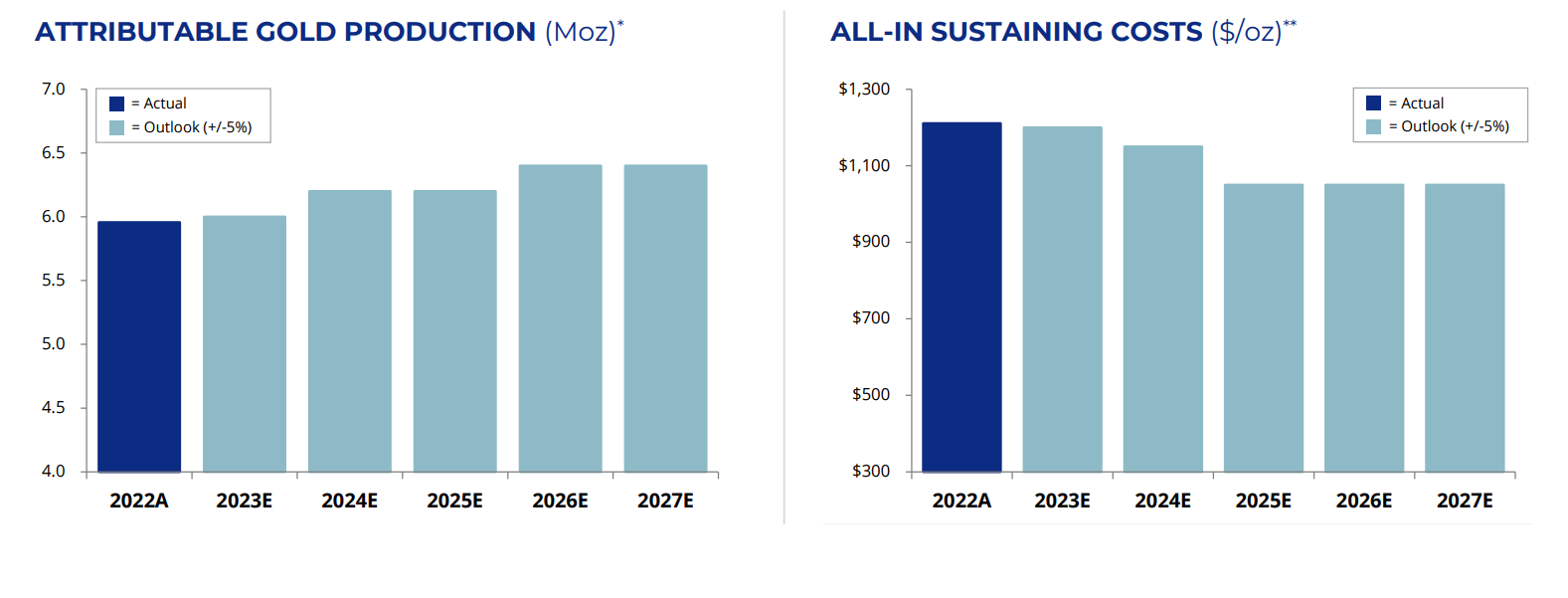

As the chart above highlights, while Newmont may be a high-cost miner today with $1,400/oz+ AISC in Q2, Newcrest is a low-cost producer, expecting to produce ~2.0 million ounces of gold on an attributable basis at $1,000/oz all-in sustaining costs. This will provide a significant benefit to Newmont when these low-cost assets (Brucejack, Cadia, Fruta Del Norte interest) are added into the portfolio, and at the same time, Newmont's own portfolio is expected to benefit from increased gold production at significantly lower AISC, with the company adding higher-margin ounces from Ahafo North and Tanami Expansion, where construction is underway with completion expected in H2 2025 for both projects.

Newmont - Production & Cost Outlook (Ex-Newcrest) (Company Presentation)

{kind=link}

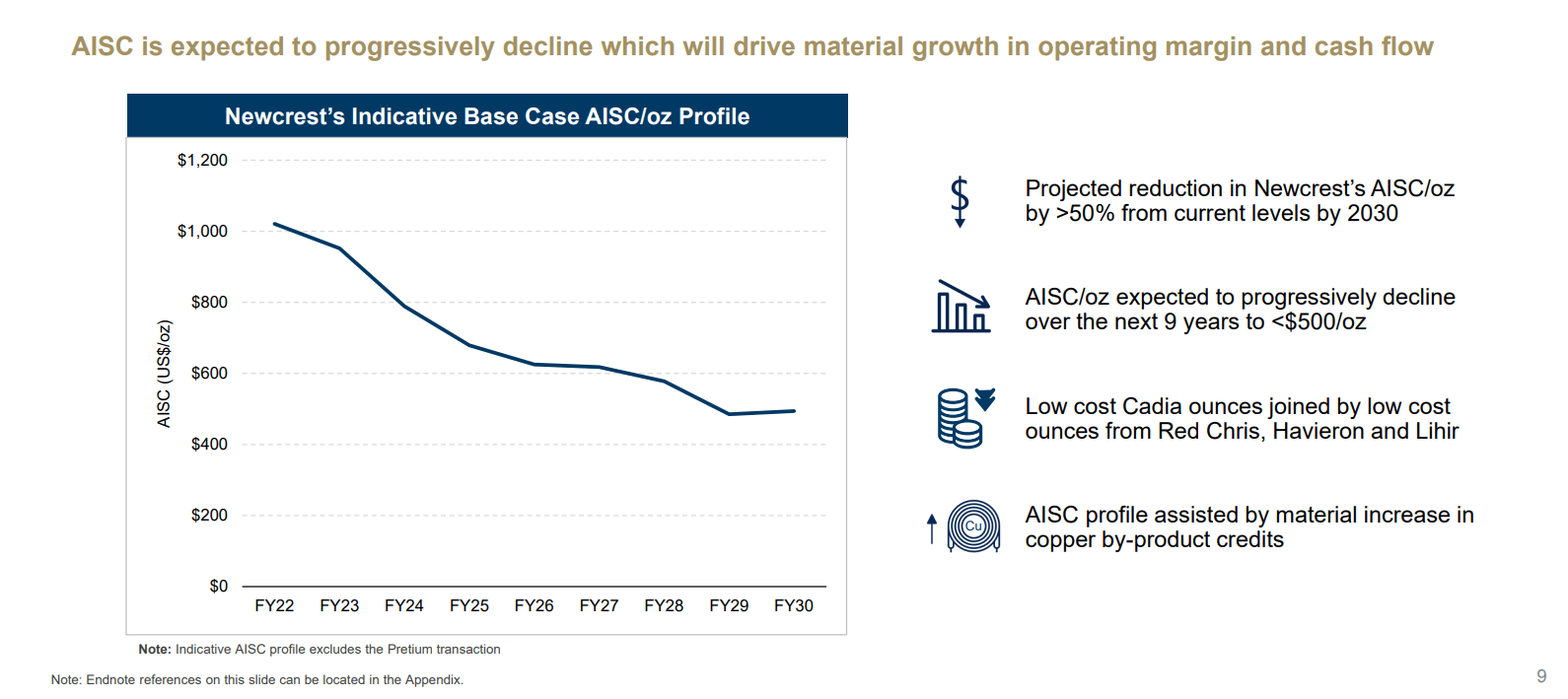

Finally, what investors appear to be missing as part of the margin equation is that while Newcrest is a low-cost producer today, it is graduating into a larger and even lower-cost producer later this decade. This is expected to be achieved through optimization at Brucejack, the benefit of what are already industry-leading costs at Cadia, plans for Red Chris Block Cave which should have negative all-in sustaining over a 30+ year mine life, and the addition of the high-grade shared Havieron asset. And while I think the company's projections of sub $600/oz are too ambitious (excluding Brucejack), I don't think it's unreasonable to assume that the Newcrest portfolio could enjoy sub $775/oz costs by FY2030, which would make this portfolio the closest we've seen to the previous Kirkland Lake Gold, which was an absolute cash cow with two ultra-low cost mines in Macassa and Fosterville from 2017 to 2020.

Newcrest - Indicative Base Case AISC Profile (excluding Brucejack Mine) (Company Presentation)

{kind=link}

To summarize, when we marry a low-cost portfolio with large-scale assets that is set to enjoy even lower costs with a Newmont portfolio that looks its worst in 2023 due to elevated capital spending, lower production due to one-time issues, and the residual impact of inflationary pressures, we have a company set to undergo a major transformation and turnaround looking out to 2025/2026 and even further if and when Red Chris Block Cave is approved.

Therefore, I see zero value in judging Newmont on its Q2 results, and believe it's best to ignore this weak quarter and look at the big picture, which will likely include portfolio optimization, meaningful synergies such as those enjoyed at Penasquito, and regular high-grade drill results from Havieron and Brucejack (including new discoveries like Golden Marmot), which is one aspect that Newmont has lacked with a portfolio of lower grade majority-owned mines on balance (exceptions are Cerro Negro, Porcupine Underground and Tanami) than some of its peers.

Valuation

Based on an estimated ~1.20 billion shares outstanding following the deal closure and a share price of US$41.00, Newmont would trade at a market cap of ~$51.6 billion, placing it well ahead of its #2 and #3 peers in the gold sector from a market capitalization standpoint. And while this might appear to be a steep valuation for a company that's generating no free cash flow year-to-date, it's important to note that H1 was not reflective of Newmont's overall business, with a strike at its massive and lower-cost Penasquito Mine (H1 2022 AISC: $1,013/oz), a softer quarter at its shared high-margin Pueblo Viejo Mine (40% interest) due to work to complete the expansion to 14.0 million tonnes per annum and elevated sustaining capital/lease related costs in the period ($706 million vs. $509 million) combined with fewer ounces sold.

However, Newmont has guided for a much stronger H2 at several assets and the combination of higher sales, reduced sustaining capital due to it being front-end weighted in H1, and this being a capital-intensive year already with near-peak capital spending for Newmont's portfolio. However, as highlighted above, Newmont has reiterated guidance of 5.7 - 6.3 million attributable ounces of gold (implying a very back-end weighted year for production), and also reaffirmed its guidance for all-in sustaining costs of $1,150/oz to $1,250/oz. And while I think AISC is likely to land above the top end of the guidance range, the higher production, higher margins, and what looks to be a minor tailwind from the gold price should help the company deliver a much better H2.

{kind=link}

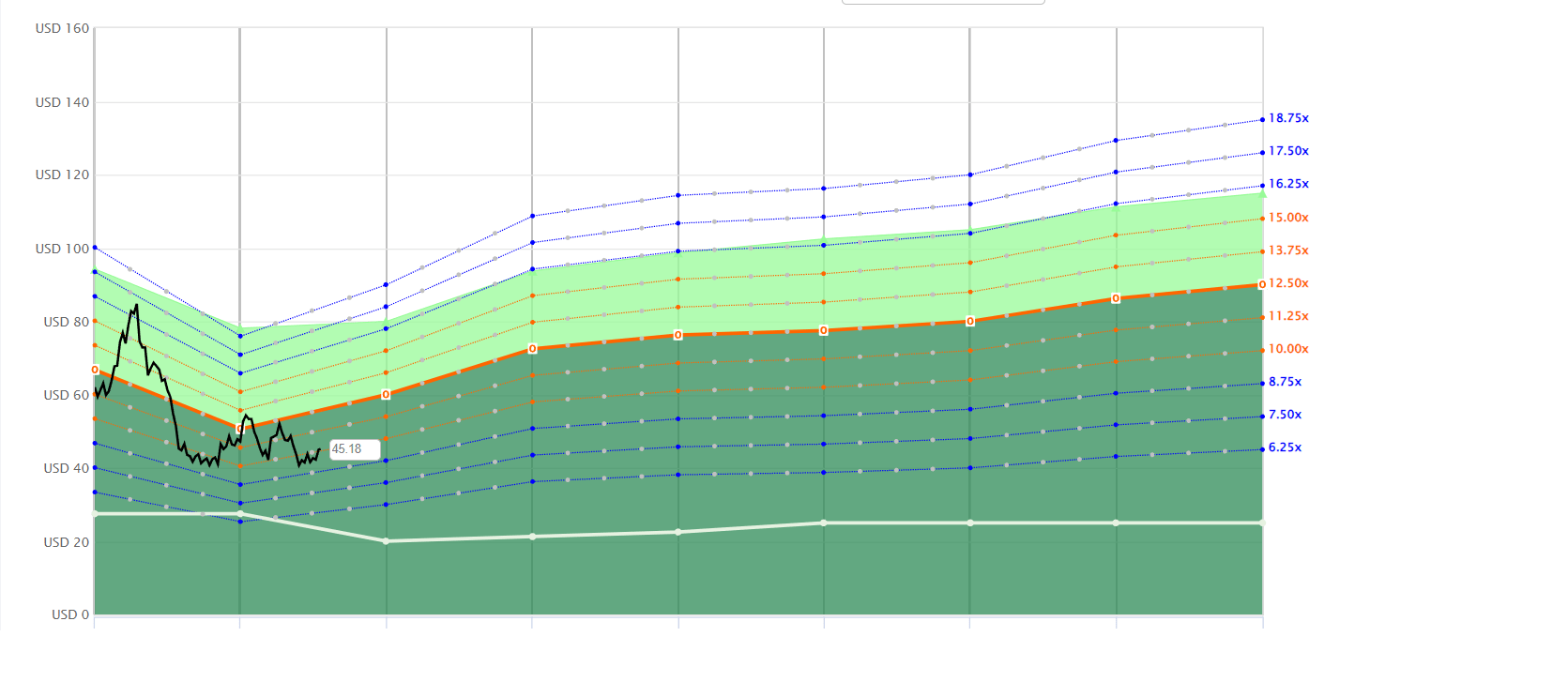

Meanwhile, from a bigger picture standpoint, Newmont 2.0 (combined with Newcrest) will be positioned to generate up to ~$7.5 billion of operating cash flow in FY2025, translating to cash flow per share of $6.00+. And with a larger and more diversified portfolio, an improved margin profile, and a significant development pipeline of high-margin assets (Red Chris Block Cave, Havieron, Wafi-Golpu, Yanacocha Sulfides), I believe Newmont could easily command a cash flow multiple of 11.5 - 12.0x, pointing to a 2-year target price of US$69.00 - US$72.00. Notably, this is only slightly above Newmont's long-term cash flow multiple of 11.0x, so I think it could end up being conservative if Newmont can execute successfully with its integration and synergies and become an 8.0+ million ounce producer with sub $1,050/oz AISC.

Newmont 2.0 - Different Cash Flow Multiple Assumptions & Forward Cash Flow Per Share Estimates (FASTGraphs.com)

{kind=link}

So, while Newmont may look expensive today after two rough quarters, this is a company on the eve of a major transformation if the Newcrest deal goes through successfully, with the Canadian Competition Bureau last week providing clearance for the acquisition of Newcrest. Per the most recent disclosure, the hope is that the deal should close in Q4 of this year.

In addition, Newmont itself is on track to see a significant improvement in its production and cost profile looking out to FY2026, guiding for mid single-digit production growth (6.1 to 6.7 million ounces) combined with a 15% plus drop in all-in sustaining costs ($1,050/oz midpoint vs. estimated AISC of $1,280/oz in FY2023). Hence, if the stock were to trade below US$41.00, where it would trade at just ~6.8X FY2025 cash flow per share estimates, I would view this as a buying opportunity.

Summary

Newmont may have had a rough quarter in Q2, and those with a rearview mirror approach might contend that the stock is fully valued and un-investable. However, I've never found any value in judging a company based on one of its worst quarters and projecting this forward, and this was certainly a kitchen sink H1 for Newmont, with minimal help from two of its high-margin contributors (Penasquito, Pueblo Viejo interest), front-loaded sustaining capital spend and elevated growth capital spend combined with significantly lower metal sales. The result? Ugly looking unit costs and limited free cash flow generation, which might make it seem like Newmont has a lower-quality portfolio.

That said, this couldn't be further from the case, with Newmont owning multiple Tier-1 assets in safe jurisdictions and having a minority interest in several of the most productive gold mines/complexes globally. Plus, as highlighted in my previous update, Newmont will add two more Tier-1 scale assets with its Newcrest deal (Red Chris, Cadia) and these assets will come with some of the best margins sector-wide, with Cadia reporting record AISC of negative $124/oz last year, and Red Chris having the potential to be a negative cost producer as well with by-product credits post-2027 with a 35+ year mine life. In fact, this asset alone could generate upwards of $5.0 billion in after-tax free cash flow.

To summarize, I see the multi-month correction in Newmont Corporation stock providing a rare opportunity to buy the stock at a very reasonable valuation. I would view any NEM pullbacks below US$41.00 as buying opportunities.

For further details see:

Newmont: Ignore The Weak Q2 Results