NEX - NexTier Oilfield Solutions: Another Value Proposition In The Discounted Pressure Pumping Segment

2023-05-21 04:34:41 ET

Summary

- NexTier is deeply discounted at 2.6x forward earnings; unlike other stocks trading at very low multiples, NexTier isn't financially distressed and revenue is growing.

- The demand for pressure pumping services may weaken in the short run, but NexTier's business model is resilient due to the long-term contracting and technological differentiation of its frac fleets.

- The stock sold off on macro fears, but there are few links between an adverse macro scenario and NexTier's fundamentals; the only major risk is further multiple compression.

- Other ideas in this space include LBRT, PUMP and CFWFF; possibly the more levered ACDC too.

- The aggressive buybacks announced in the sector could be a catalyst even against a negative macro backdrop.

I continue my coverage of the pressure pumping/hydraulic fracturing space with NexTier Oilfield Solutions Inc. ( NEX ), a U.S. land-based oilfield services (or "OFS") company that offers well completion and cementing services to E&P customers. Previously, I reviewed NexTier's competitors Liberty Energy ( LBRT ) and ProPetro ( PUMP ):

Weather The Recession With This 3x P/E Stock: Liberty Energy

ProPetro: Don't Write Off This Shale Fracker For 2023

My NEX thesis is similar:

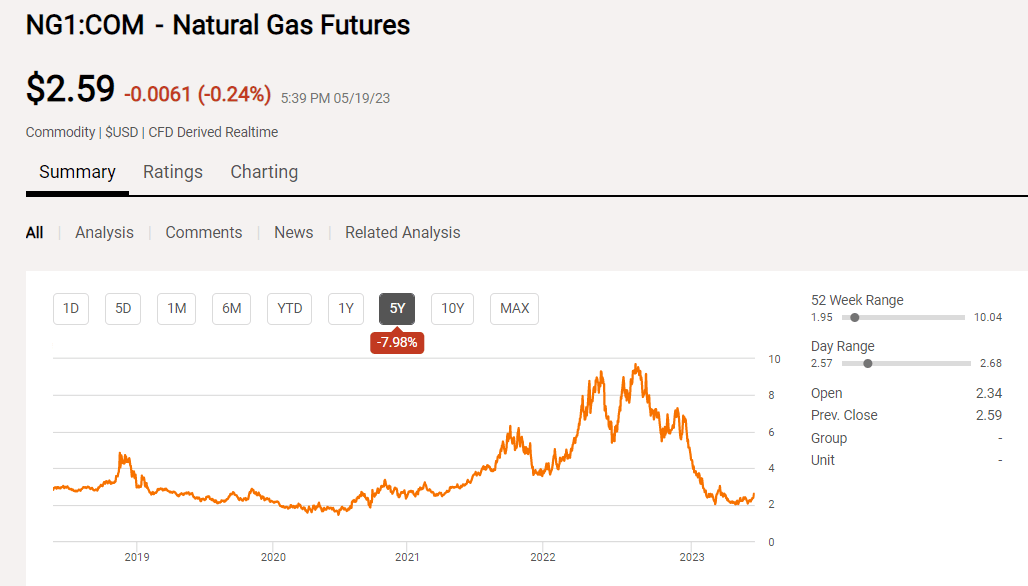

- Crashing natural gas prices ( NG1:COM ) and macro fears from the regional banking crisis drove a major selloff;

- Fundamentally, this wasn't justified because NexTier's frac fleets aren't exposed to spot contracts; the market may also remain tight even if dry gas activity moderates;

- Like LBRT and PUMP, NexTier differentiates itself technologically through next generation e-fleets that run on natural gas instead of diesel; this reduces E&P operators' fuel costs and carbon footprint.

Even if you buy into the prolonged OFS ( OIH ) slump narrative, it makes little sense that land drillers such as Nabors ( NBR ) trade at more generous multiples than completions players like NEX, LBRT or PUMP. E&P companies won't just drill new wells to leave them uncompleted.

I don't expect the valuation arbitrage to continue long, especially as the pressure pumping companies themselves see their shares as undervalued and are aggressively buying back stock. NEX already had a buyback program and just a few days ago PUMP authorized a buyback that could reduce its share count by a whopping 13%.

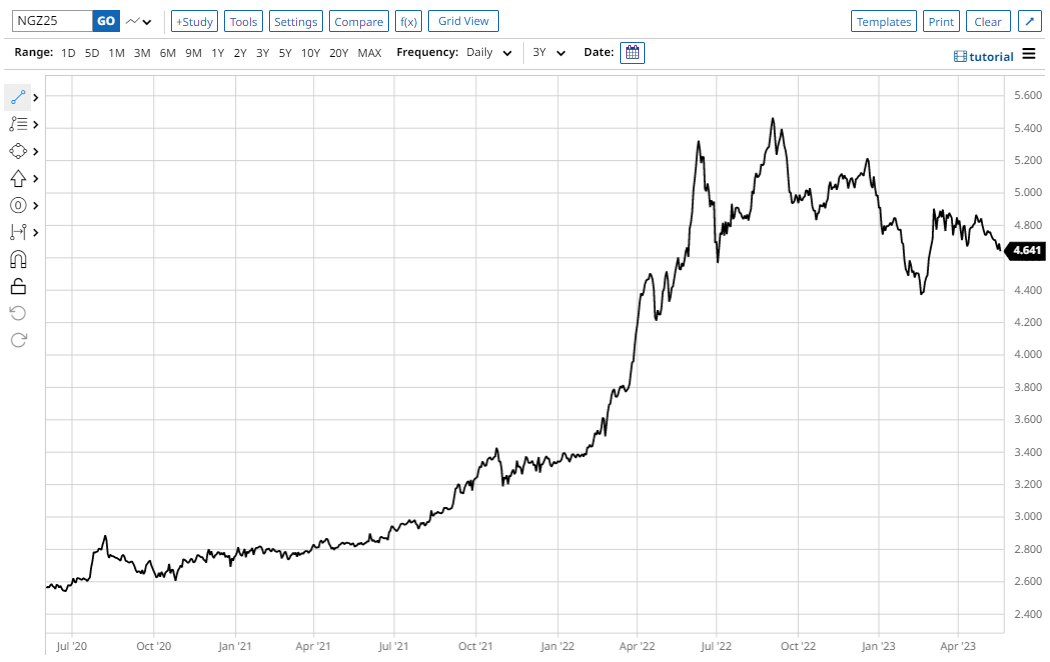

Natural gas crashed but is finding support

To level set, natgas fell from $9 to $2 per mmbtu due to a warm winter, Europe dodging the energy crisis and the Freeport LNG outage:

{kind=link}

There is also speculation that, as U.S. shale oil basins like the Permian mature, oil wells will get more gassy and put on the market humongous amounts of associated gas with zero breakeven cost. For example, Scott Sheffield of Pioneer ( PXD ) commented that the Permian alone could add 30 bcf/d, which would be about 30% increase from where total U.S. dry gas production stands right now. I think it's a valid concern looking to 2030, but probably not what caused the current weakness if we trust the futures curve.

In the near term, analysts think the market would have to be balanced by production cuts in dry gas basins like the Haynesville; producers in the Marcellus that has higher liquids yields can sustain their economics even with lower dry gas prices. Assuming this happens, the thought process is that Haynesville producers will let go of rigs and frac fleets; this freed up OFS capacity will move to oil basins where it will compete for work and erode the margins of companies like NEX.

It is a persuasive narrative, but not necessarily true.

Market participants look forward to 2024-2025

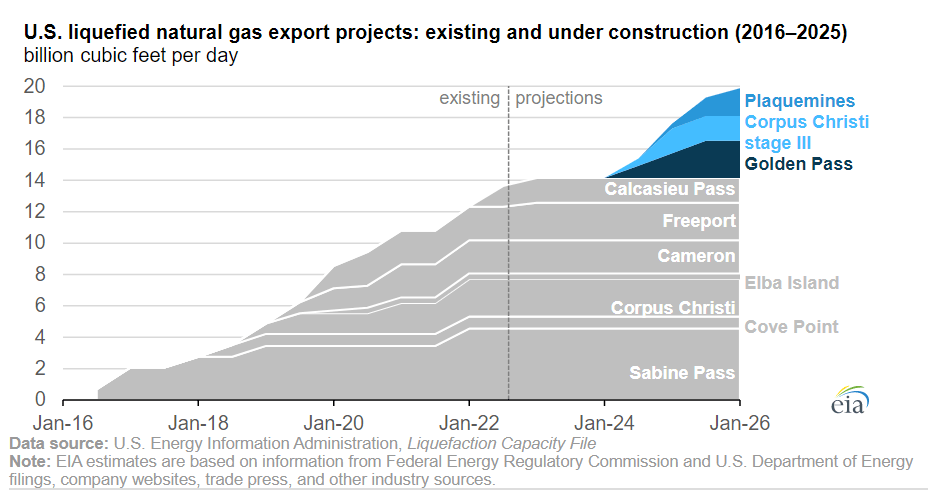

The natgas forward curve is in steep contango, with 2024 prices in the $3 to $4 range; this is when liquefaction capacity is expected to start increasing more meaningfully :

{kind=link}

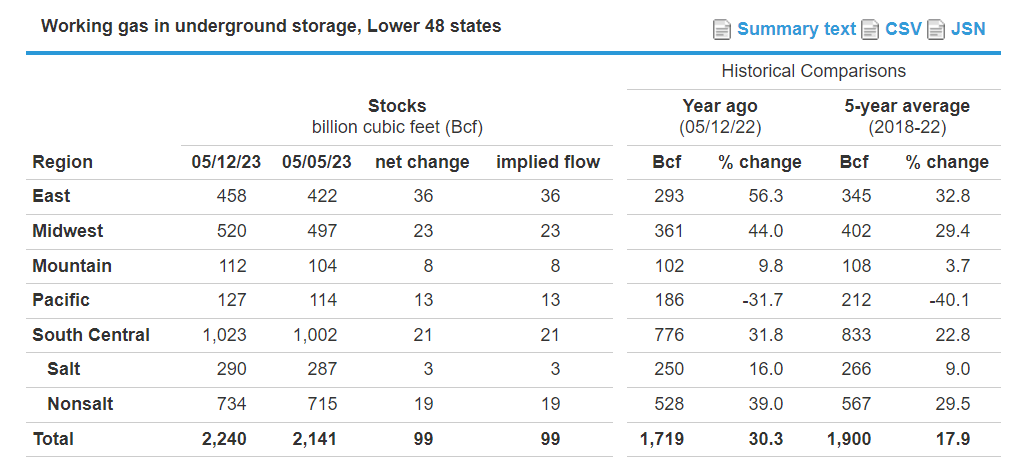

On one hand, the incremental 10 bcf/d from a shutdown Freeport to a Freeport at full capacity plus Golden Pass/Corpus Christi stage III/Plaquemines is only 10% of total U.S. production. On the other hand, U.S. natgas storage is just 300 bcf above the 5-year average (2,240 vs. 1,900 bcf):

{kind=link}

The incremental 10 bcf/d export capacity can clear up this surplus in 30 days. As long as the surplus stops widening, I am not sure the fact that in cumulative terms we are 18% above the 5-year average will matter much. Moreover, gas use may again rise in power generation, displacing coal ((BTU)) - a trend that was disrupted in 2022, but now the price response would have the opposite effect.

NEX management during the Q1 call:

On the natural gas side, LNG capacity additions through 2025 have the potential to create significant demand for incremental frac fleets. We still see U.S. shale struggling to meet both of these calls in tandem given constraints around equipment and capital with the availability of frac equipment likely remaining bottlenecked.

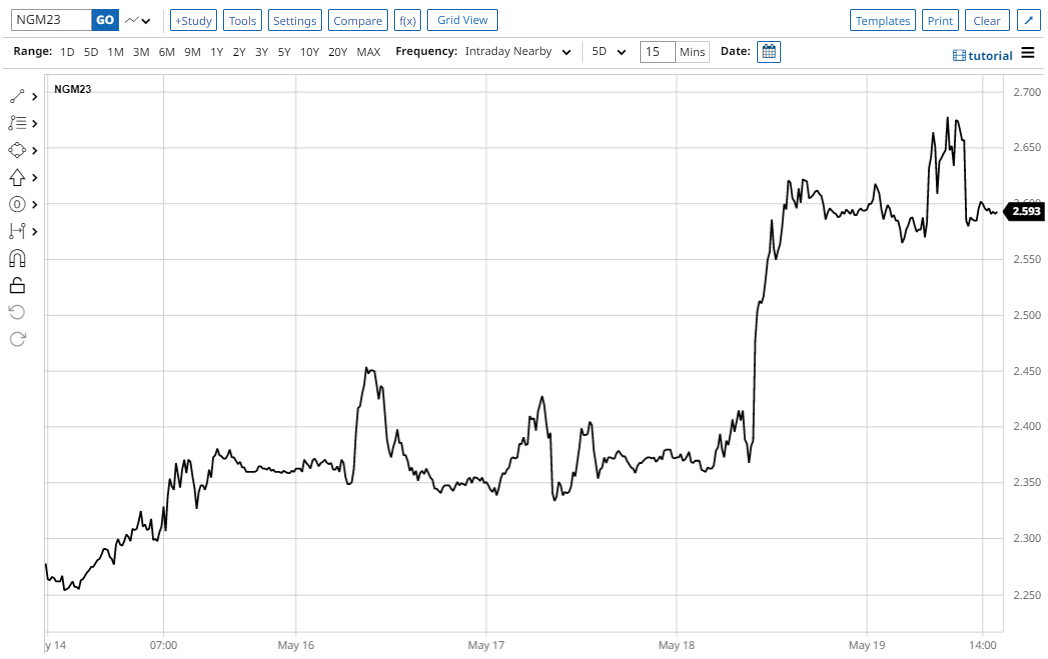

Front-month gas rallied this last week:

{kind=link}

I am not a technical analyst and can't tell you if we have already bottomed, but I find it instructive that further out the curve didn't go up as much when front-month gas was $9 and it hasn't crashed now to $2 either:

{kind=link}

My guess is the market thinks in the long run supply and demand will clear at around $4/mmbtu, which, in historical perspective, is a great price that will support even Haynesville activity. I find telling the April 2023 cover story from The American Oil & Gas Reporter, which features the CEO of Comstock Resources ( CRK ), one of the largest gas producers in this basin:

Allison claims Comstock now has the largest acreage footprint and the largest drilling inventory in the Haynesville with a strong balance sheet and a sector-leading low cost structure. He says Comstock's break-even Henry Hub price is $2.00-$2.10 an Mcf .

To borrow from Mark Twain, I view the reports about the end of the U.S. natgas boom as greatly exaggerated.

Gas supply-demand isn't the same as frac fleet supply-demand

Another frequently overlooked point is that NEX, along with LBRT, PUMP, Calfrac ( OTCPK:CFWFF ) and ProFrac ( ACDC ), compete in the frac fleet market, not in the gas market itself. E&P companies may lower their production plans and need less fleets, but if the supply of fleets falls too, the imbalance can still favor the service provider.

NEX made some excellent comments on this topic:

The oilfield services industry, and more specifically, the US land pressure pumpers have shown great discipline as this current cycle has unfolded..

..we see capital discipline lengthening the period for strong returns for oilfield service companies. We've been a factor in shifting the industry focus back to returns and free cash flow and we have a strong conviction that our capital allocation strategy is a winning formula..

..I think you have basically the need to account for every new fleet add with one out through attrition. And we've been boisterous about saying that we expected to see about 10% of the fleets attrition during this year, which is about 23 frac fleets on the current kind of 280, which balances very closely with the new build adds that we see coming into the market..

So I think that that demonstrates a very balanced market coming off of 2022, which was perhaps the most underbalanced market that I've ever seen in frac in my career. So all I would say there is that's very supportive for our margins to stay the same as we move into the back half of the year..

It is a similar to theme to what we see among offshore services providers like Transocean ( RIG ) or Tidewater ( TDW ) - no one is investing in new service assets, whether it is rigs, boats or something else. It looks the services industry learned from 2014, and land-based providers are on the same page too.

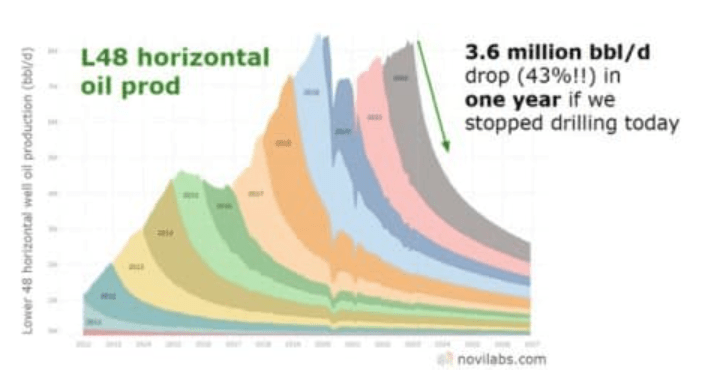

Lastly, let's not forget that shale, oil or gas, needs to do quite a bit just to maintain production flat; this chart via NoviLabs and oilprice.com makes the point clear:

{kind=link}

As much as they may not like it, shale producers may have to get used to sharing a bigger piece of the pie with OFS.

NexTier had a great quarter

For a company supposedly facing deteriorating market conditions, NexTier had a pretty good quarter:

We saw sequential growth in adjusted net income for the 10th consecutive quarter and had another quarter of strong free cash flow...

First, for the first quarter, we saw strong operating results even as the quarter was disrupted by winter weather. Adjusted net income of $156 million improved 7% for the prior quarter...

Total revenue of $936 million, was up 7% sequentially and was 47% higher than the same quarter last year.

The top line growth was a combination of an increase in pumping hours as well as higher sequential pricing . Adjusted EBITDA of $228 million was 7% higher sequentially and improved for the eighth consecutive quarter.

Management reiterated its guidance:

Our outlook is essentially unchanged from our last update. We continue to see topline growth and we've called out 40% to 50% of adjusted EBITDA growth in 2023..

.. We anticipate free cash flow will gather momentum as the year progresses and we will still expect to generate approximately $500 million in 2023, which is a free cash flow yield of over 20% based on current market capitalization.

By my math, $500m in FCF is now 25% of the current $2b enterprise value - not too shabby.

The business model is resilient

Let's also look into two specific positives of NexTier's business model that should provide further insulation against macro pressures.

First, focusing on headline frac fleet numbers (about 280 or so right now per Primary Vision) ignores the spot vs. longer term contract dynamics.

NEX management thinks any declines would come from spot or underperforming fleets:

Natural gas basin demand did soften as expected as the quarter progressed, with industry activity in the primary gas basins down roughly six fleets since the start of the year.

Consistent with our prior expectations linked to historic responses to natural gas cycles, we believe there are likely another eight fleets that could be released in natural gas basins, as the commodity seeks balance. The fleets that are most vulnerable are those that are underperforming and those that are working in the spot market. We have very little exposure to the spot market and oil or natural gas basins and our operational performance has been very strong.

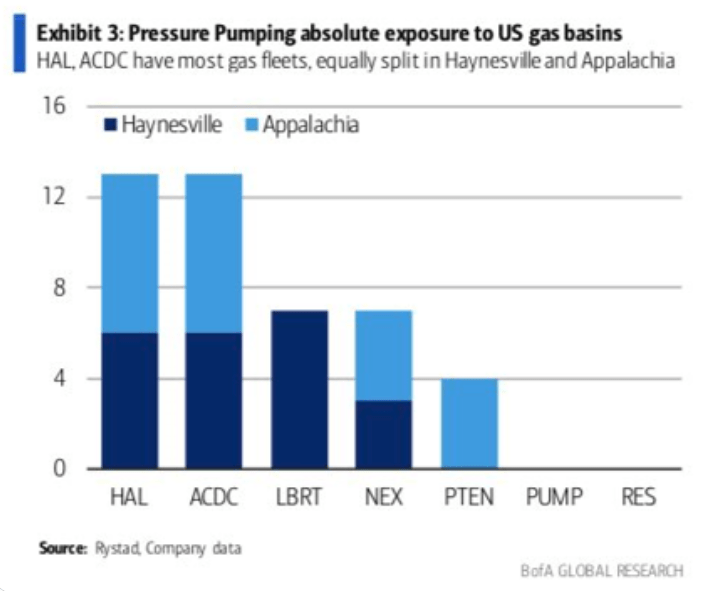

NEX isn't exclusively serving oil basins like PUMP, but it's exposure is relatively low, akin to LBRT. The players with greater gas exposure are ACDC and OFS major Halliburton ( HAL ):

{kind=link}

The second business model aspect to consider is technological differentiation. The industry is gradually retiring older, diesel-powered equipment and replacing it with new electric fleets that can run on natgas. The advantages include lower fuel cost, lower carbon footprint and less noise.

NEX management:

The frac industry has undergone a massive shift over the past several years. The commoditized service offerings from prior cycles are no longer a reality. We are already seeing bifurcation between the high-end and low-end competitors. Less efficient service providers will struggle to compete and we believe the differentiation will become more obvious in the coming years ..

We were industry leaders in the evolution of using natural gas, as a fuel source for frac. Our digital sensor has significantly lowered the cost to maintain our fleets and optimize our logistics. And our reservoir technologies, maximize the capital efficiency of completion designs..

.. The spread between price for any gas-powered unit versus diesel power is supported by that amount of displacement that occurs. And that's a math equation about how wide is that arbitrage and the customers understand it very well and so do we. We price it to get as much of that as you can in our fleet and they offset it with the arbitrage..

Similar to comments made by LBRT and PUMP, NEX management sees increasing bifurcation between high and low-quality providers that may provide support for LBRT/PUMP/NEX even if the headline numbers decline.

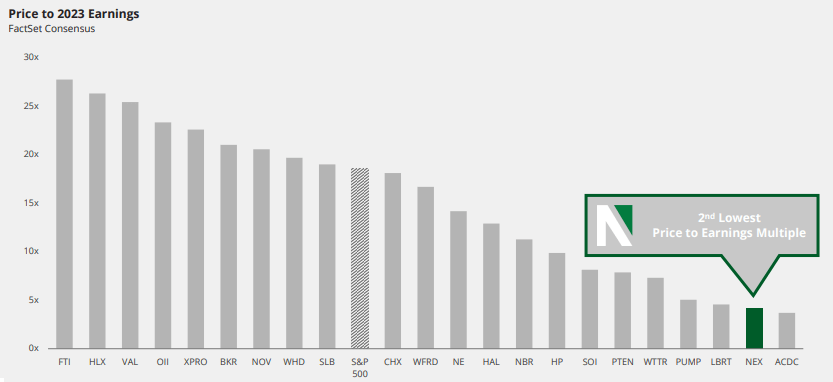

The valuations are compelling

What initially drew my attention to the pressure pumpers were the bargain basement valuations:

{kind=link}

The NEX presentation is from right before the regional banking crisis, but the valuations have only compressed further and the pressure pumping group remains the cheapest among all OFS. For more recent multiples, I would refer to my Liberty article .

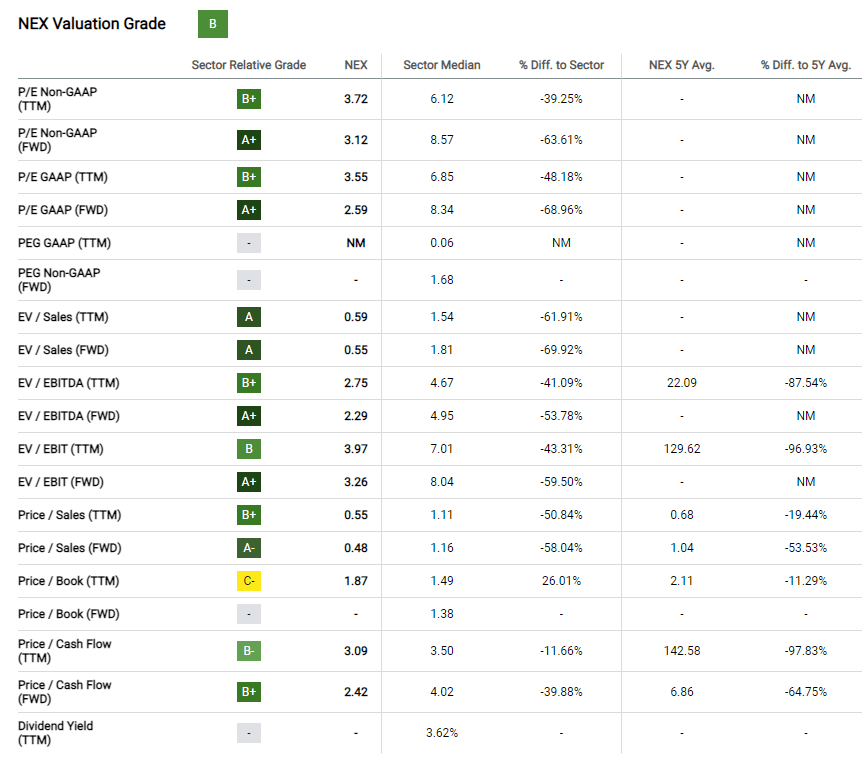

NEX looks good on Seeking Alpha's valuation metrics:

{kind=link}

I believe the only reason this is a "B" and not "A" is the price to book ratio. However, mind that NEX expanded recently through a couple of acquisitions. The assets acquired in the process are stepped up to fair value before getting recorded on the balance sheet; this would falsely make NEX appear more expensive on book basis. Forward EV/EBITDA is 2.29x and forward P/E is 2.59x. These aren't metrics you would typically see for a company with growing revenue and without distressed debt.

I would be perhaps more cautious if the valuations were consistent across the entire OFS sector, but it makes little sense that the completions companies are so discounted relative to drillers:

| Ticker |

| P/E GAAP (fwd) |

| NEX |

| 2.59x |

| PUMP |

| 4.41x |

| LBRT |

| 3.61x |

| NBR |

| 7.08x |

| Helmerich & Payne ( HP ) |

| 7.64x |

| HAL |

| 9.71x |

Source: Seeking Alpha

E&P companies do need to replenish their DUC inventory, but something still seems amiss here.

The buybacks may be a catalyst

NEX management agrees that its stock is undervalued:

Considering our outlook, we continue to believe our share price is significantly undervalued . We will always invest our capital dollars in the highest return opportunity that we believe will create the most long-term value for our shareholders, including through our sizable shareholder return program.

Share count decreased -1.3% during Q1. Debt is low so it won't compete as much for cash with shareholder returns:

We have no term loan maturities until 2025. Net debt at the end of the first quarter was approximately $139 million, down slightly from the end of the fourth quarter. Our share repurchases were funded entirely with our free cash flow during the quarter.

Support will also come from the buybacks announced by competitors like ProPetro:

Under the share repurchase program, the Company may repurchase up to $100 million of outstanding common stock through May 31, 2024. This authorization represents approximately 13% of ProPetro’s market capitalization based on the current share price.

The risks aren't fundamental

I think the fundamental case for NEX is quite strong, especially considering the specifics of its business model. Debt isn't a factor either, and I don't see what more a U.S. recession could do that will feed into NexTier's bottom line.

The risk is rather that a macro driven sell off across other sectors like tech, will also push the whole market down and may compress multiples further. Yet, given that NEX and its peers are so strong on opportunistic buybacks, I don't think future dips will last long.

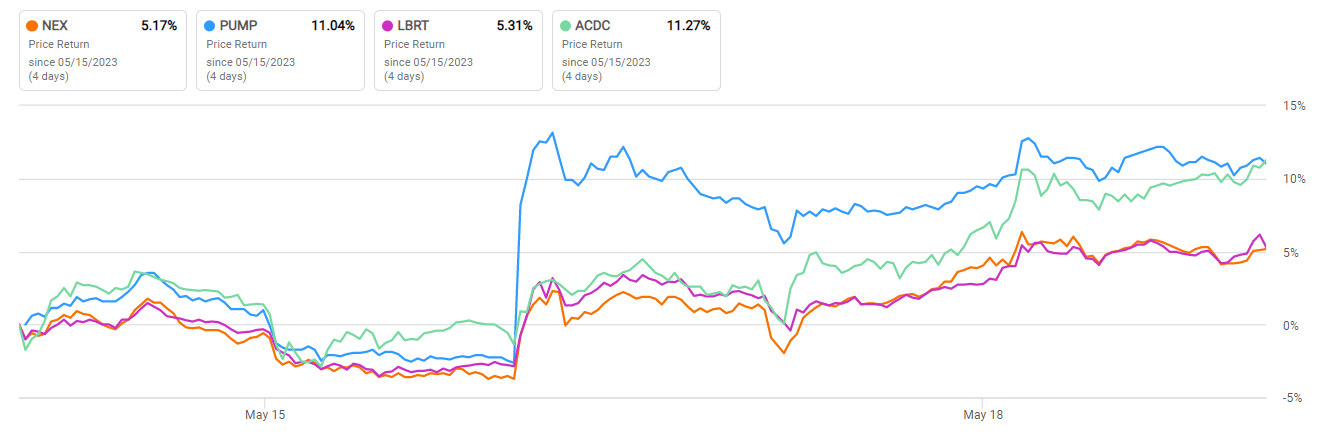

The peer group has gain 5% to 10% during the last week, off the recent lows:

{kind=link}

Bottom line

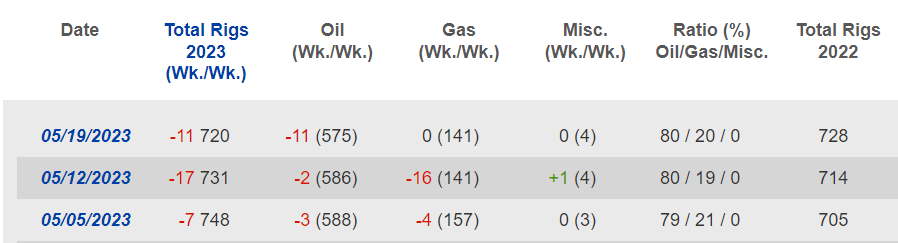

Last week's stock price action for NEX and its peers does coincide with apparent realignments in U.S. gas basins. For the week ended May 12th, the U.S. gas rig count fell by 16 (or 11 percent!), on the back of a drop of 4 the week before. However, for the May 19th week, the gas rig count was flat:

{kind=link}

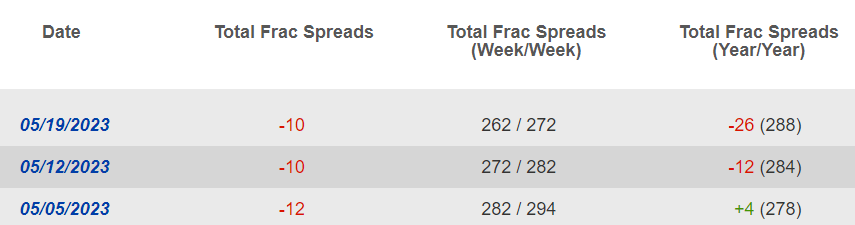

The gas breakout discussed above was also simultaneous to these events. Frac spreads have now seen three consecutive weeks of losses:

{kind=link}

Frac spreads would trail the rigs (you need to drill before you can complete) so this make sense. Was it the bottom? I don't know, but the bottom line is that if the losses were from fleets operating in the spot market, it may not matter for NEX. Of course, we won't have proof until Q2 numbers come out, but I think the explanations from NEX and PUMP's managements made a lot of sense.

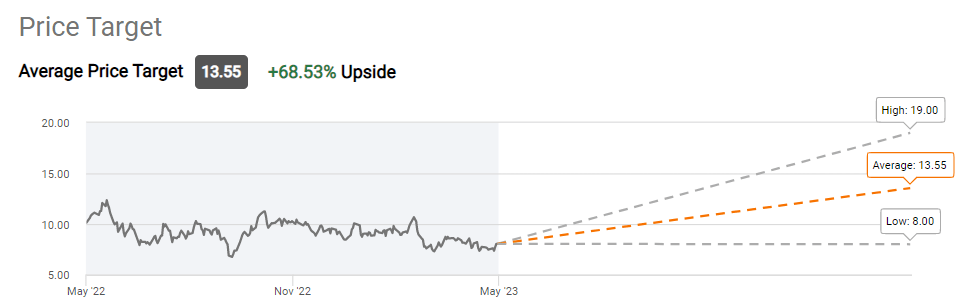

Wall Street analysts have an average target of $13 which is about 70% upside:

{kind=link}

I think this is achievable even without macro improvements, and can be attained just from repricing to where most land-based OFS stands now - and this doesn't even consider the possibility that OFS itself as a whole may also be undervalued.

For further details see:

NexTier Oilfield Solutions: Another Value Proposition In The Discounted Pressure Pumping Segment