TSLA - Nine Energy Service: A Deeper Correction Is Possible

Summary

- NINE's rapid rise has mirrored the de-risking in the credit market which no longer prices the company for bankruptcy.

- The valuation is now a bit too rich.

- The company filed a shelf offering so some dilution may be forthcoming.

- Insiders sold during the recent peak and short interest remains high.

- If the stock corrects, I may consider adding, but right now I see better value in other oilfield service names.

Investment thesis

Nine Energy Service ( NINE ) is a small oilfield services company that in theory could fit nicely with my energy macro thesis for 2023. The stock has also attracted a lot of interest from the retail investment community as it appreciated a whopping 300% in the last three months alone:

The stock price rise has mirrored the credit markets which have significantly de-risked the November 2023 bonds. While NINE has indeed made remarkable progress towards a 2023 refinancing, the stock price may have gotten a bit ahead of itself. Recent warning flags include a shelf registration, some insider selling and an increase in the short interest.

Furthermore, NINE remains extremely volatile, so I wouldn't be surprised to see another significant correction after the multiple drawdowns we saw earlier in 2022:

If the stock corrects further, I may consider adding, but right now I see better value in other oilfield services names.

Background

Nine Energy has several oilfield offerings including completion tools on the product side and services including cementing, coiled tubing and wireline. The completion tools are actually largely from the 2018 acquisition of Magnum Oil Tools, a company that had been around for a while. Reportedly, NINE paid 10x EV/EBITDA for Magnum back then.

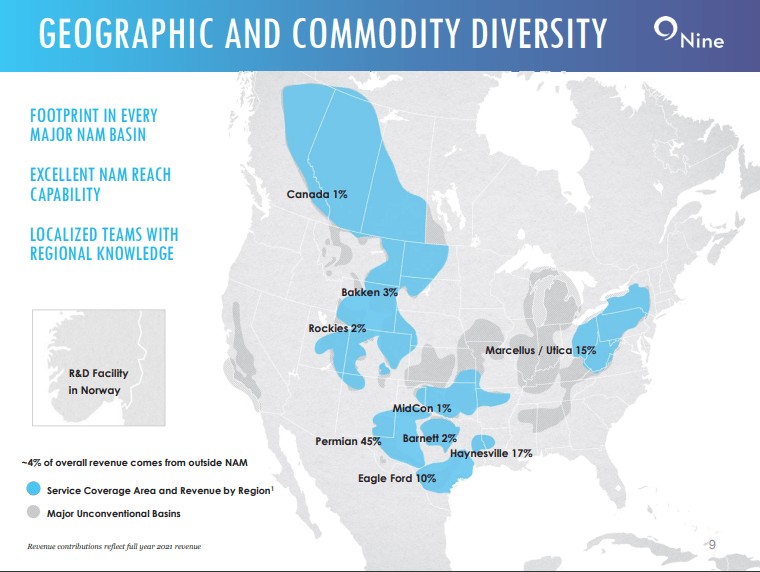

The shale basins of most importance to NINE are the Permian, Haynesville and Marcellus:

{kind=link}

Nine Energy Q3 Presentation

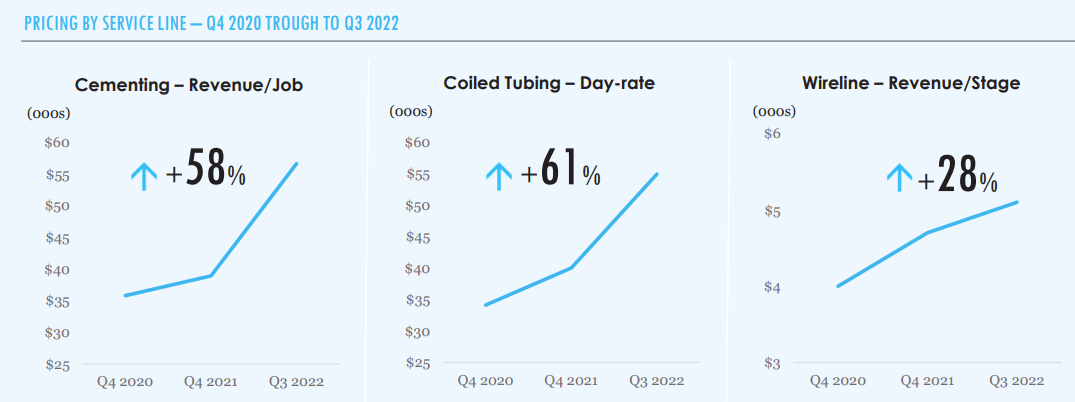

NINE posted strong Q3 results , with most improvement to the top- and bottom-line coming from better pricing on individual service jobs:

{kind=link}

Nine Energy Q3 Presentation

On the tools side, NINE's focus have been the dissolvable plugs that were inherited from Magnum. These plugs are said to reduce the need for well interventions and provide other operational efficiencies for operators as well.

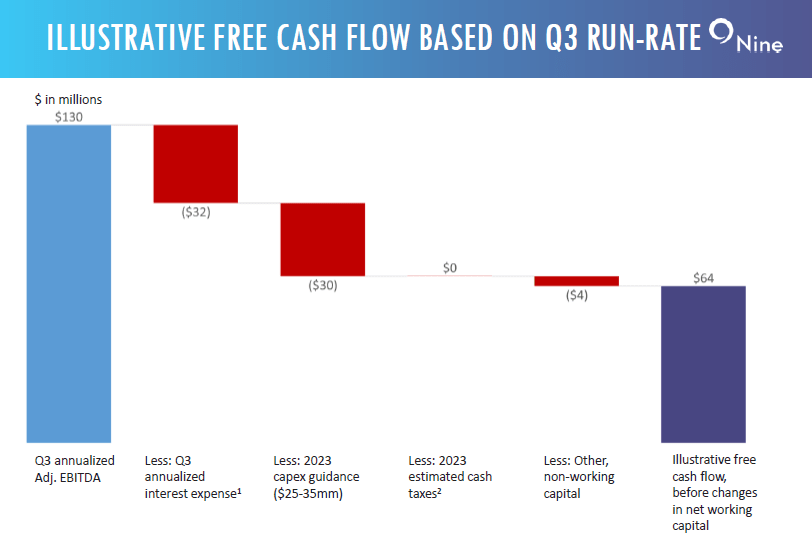

On the financial side, annualized Q3 EBITDA is at a $130 million run-rate (based on management adjustments) and reflects 19% EBITDA margin. This is pretty good profitability for a small oilfield services player if it can be sustained.

The 2023 bonds

While NINE seems to run a reasonable business, the 2022 year has been entirely about the senior notes maturing this coming November, with Q3 outstanding balance of $307 million.

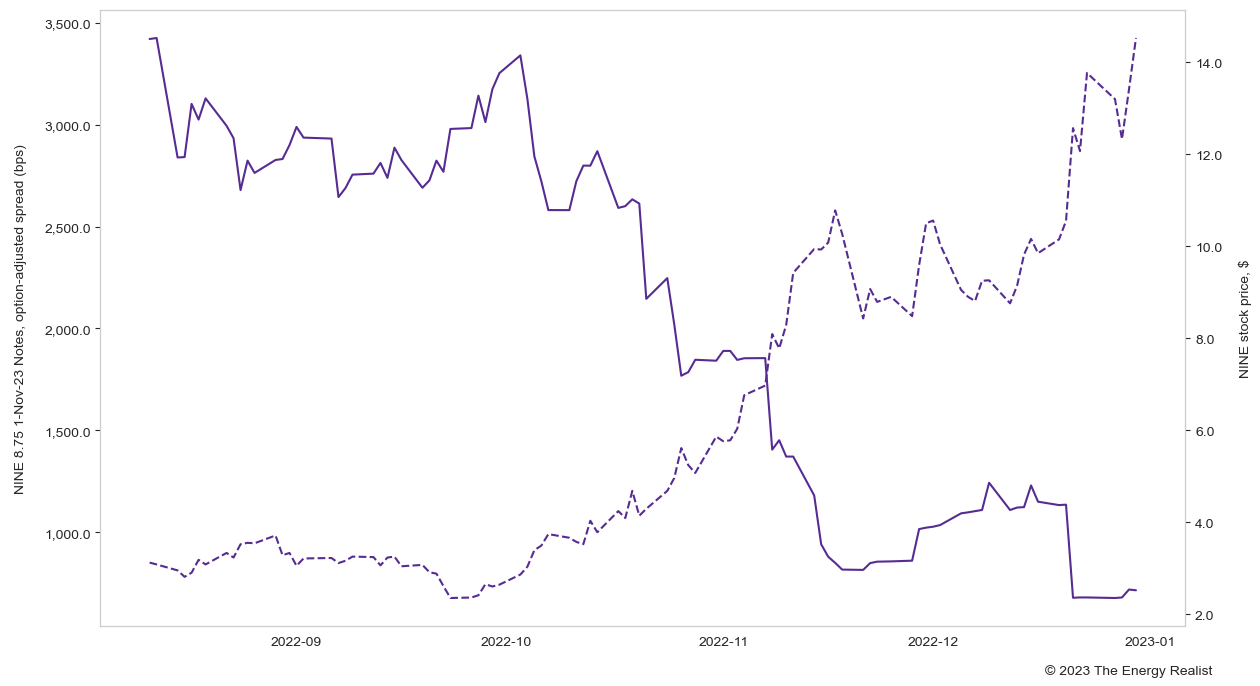

The market didn't foresee a chance these notes could be refinanced and NINE was essentially priced for bankruptcy. Besides the April 2022 highs which weren't sustained, the more gradual upward move in the stock started only when the credit markets began repricing the refinancing risk:

{kind=link}

Author's calculations

We went from 3000-4000 bps credit spreads for most of the year down to about 700 bps right now while the stock price went up from $2 to $14. The current stock move up should prove more durable than the blip back in April because now we also have validation from the bond market. The rating on the notes is still CCC, so we aren't completely out of the woods, but the narrowing of the credit spread was huge.

The Q3 earnings were definitely a pivotal moment, but the risk repricing started earlier, after NINE resolved the potential delisting threat from the NYSE. On November 10th NINE got a $15.50 target at EF Hutton Acquisition Co., and, interestingly, on January 4th, just recently, it was given a $18 target by ATB Capital Markets, raising their prior target of $9.5.

Valuation

After the run up, NINE's valuation appears a bit too rich:

Seeking Alpha

Forward EV/EBITDA of 8.4x is a bit too much when the debt issue hasn't been definitely resolved. Based on the same Seeking Alpha screen, Baker Hughes ( BKR ) is trading at 10.5x forward EV/EBITDA. However, Baker has $28 billion market cap vs. $400 million for NINE.

Potential headwinds

While I am very bullish on oilfield services companies, there are several specific factors that should be considered in view of NINE.

Business prospects

Rig count growth is stalling, even in the Permian, which generally nowadays grows faster than most other U.S. shale basins:

Rig count is also flat in other places and tanking natural gas prices ( NG1:COM ) probably won't help NINE much in the Marcellus and Haynesville either.

Some interesting comments of relevance for NINE were made by the Pioneer ( PXD ) CEO on January 5th:

We have the Permian – about a year or two ago, I stated it was going to go to about 8 million barrels a day to 2030. The EIA has it at 5.5 million barrels of oil per day. We have lowered that to about 7 million by 2030. The reason we've lowered it is that people – obviously, the effects of moving to what I call stack development in both the Delaware and also in the Midland basin. And that's combining either the Bone Springs or the Sprayberry, depending on which basin you're in, the shallower formation with the Wolfcamp zones. It's better to drill four wells or six wells, all at the same time to get the best performance. Also, there is a lot of companies that are moving – they're running out of inventory. They are moving to tier two and tier three inventory.

Also, I'll make a point. Chevron made a point recently that there were going to 1.2 million to 1.5 million barrels of oil equivalent per day by 2040. But the first time somebody put out a number that far, there's only three companies in my prediction that will be over 2030 in the Permian Basin over a million barrels of oil equivalent per day, that's Chevron, Conoco and Pioneer. They are the only three that have a inventory that deep, can take it over a million barrels of oil equivalent per day.

Now what's going to happen over time. The gas/oil ratios in the entire Permian Basin will continue to go up. We're seeing that. You'll see the percent oil drop for all those companies, most likely below 50% over the next 10 years. And the gas itself will get up to about 30 BCF. We're going to need a gas pipeline, at least about every 18 months to two years going forward.

This is one of the reasons I favor services companies with offshore or international exposure, but in any case it will be interesting to see how this plays out. It is possible that NINE has to continue growing more from pricing and less from volume as NINE CEO Ann Fox commented :

Service line pricing drove the majority of Nine's growth this quarter evidenced in our strong incremental margin. Undersupply of both equipment and labor coupled with supply chain constraints has shifted pricing leverage back to service providers with customer [indiscernible] focused more on availability than just price.

The problem I see is that inevitably NINE will have to share some of this better pricing with its oilfield employees and its own suppliers. So going above 20% EBITDA margins may prove difficult and NINE has its own capex to worry about too:

{kind=link}

Nine Energy Q3 Presentation

Lastly, it will also be interesting to see how far NINE can go with its flagship dissolvable plug product. The company prides itself in having 22% of the growing market for these plugs:

{kind=link}

Nine Energy Q3 Presentation

However, they conveniently omit the identity of competitors A, B and C. Well, I have some guesses who some of them might be. One is very likely NOV Inc. ( NOV ), an $8 billion market cap company with very broad oilfield offerings.

Another one is no one else but Schlumberger ( SLB ), the $70 billion gorilla in the oilfield space. With my finance background, I am far from the best person to evaluate how NINE's plug compares technologically its competitors' products, but I think that as a general rule larger companies have more means to push through their tool, especially when they can cross-sell by leveraging their broader product portfolio. And if NINE's plugs were truly unique, SLB would probably have already bought out the entire company already, as they have done multiple times in the past when seeking to acquire a technological competency they may have lacked.

Dilution threat

There is also the reminder that what is good for bondholders is not always good for the shareholders. NINE' stock price is still below its 2018 highs but the number of shares outstanding has also grown:

NINE's shelf registration statement that was just filed on December 23rd suggests the company may offer up to $350,000,000 in securities, which in theory could include common stock (which would make bondholders happy). Maybe the company is preparing to issue new debt to refinance the 2023 notes, but until some communication comes out that clarifies their plans, I would thread cautiously.

The shelf offering announcement did already skim 10%-15% off the stock price already, but more could be on the way if the dilution gets anywhere close to the full amount in the prospectus. To be fair, many companies may file these registrations just in case, without definite plans, but again some communication from management would be important.

Insider sales

A major shareholder who owns more than 10% of the company and is classified as an insider has been selling shares in December. According to the linked article from ETF Daily News, Warren Lynn Frazier sold 300,000 shares at an average price of $12.34, for a total value of $3.7 million, on December 22nd.

According to the same report, Mr. Frazier started selling in smaller batches on October 27th at a $5.53 price, and followed up with additional sales as the stock price kept going up. I infer that Mr. Frazier still holds a lot of shares, but if an insider decided that it's a good time to take some profits, smaller investors should consider the possibility too.

Short interest is rising again

Short interest has been high all year long, but is on the rise again:

Although bankruptcy is off the table, the shorter sellers may still succeed in pushing the price down.

Don't underestimate the volatility

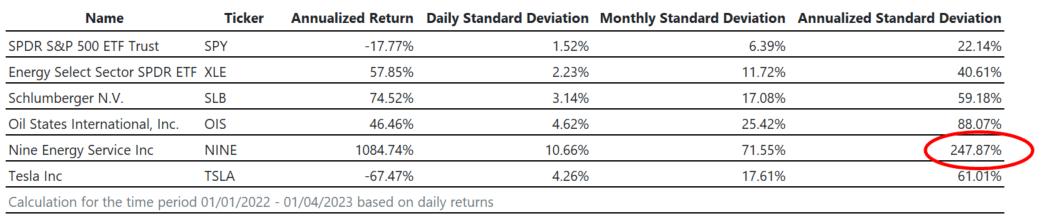

For context, I compared NINE to the broader market ( SPY ), the energy sector ( XLE ), a large oilfield services company ( SLB ), a small-cap services company I favor and have covered before (Oil States International ( OIS )), and Tesla ( TSLA ), a stock emblematic among other reasons for its volatility:

{kind=link}

Portfolio Visualizer; Author's calculations

With an annualized standard deviation of almost 250%, NINE makes even TSLA look like a boring stock. Volatility can cut both ways, but if you are a long-term investor, you generally would want to minimize it.

Of course, kudos to anyone who bought this a year ago and held so far for what is a 10-bagger. I personally had a small position opened at sub-$2 earlier in 2022 that I sold around $5 in April, but had not paid much attention to NINE since then.

Risks

I would also be hesitant to initiate a short position right now either. Clearly, the 15% short interest disagrees with me, but the market cap is still very small and NINE seems to be a popular name on WallStreetBets and other forums. Some type of squeeze is always possible with this set up.

For now, I prefer to stay on sidelines and invest instead in a company like Oil States International that has similar market cap, but 3x less the volatility and a cleaner balance sheet with no significant debt maturities until 2026.

The NINE setup is perhaps great for trading, but from a value investing perspective a stock like OIS makes a lot more sense to me.

Takeaway

If you aren't following a short-term trading strategy, the key takeaway is to stay on the sidelines until a more significant correction occurs. If you already hold some NINE, you may also consider taking some profits as it's likely you'll have the opportunity to buy it back cheaper. I would also be looking out for communication from the company on the shelf offering and if there are indeed plans to raise more equity.

For further details see:

Nine Energy Service: A Deeper Correction Is Possible