TSLA - Nissan Motor: Transformation In Progress

2023-12-24 23:49:31 ET

Summary

- Nissan is a global automotive manufacturer. The company has struggled for several years due in part to the loss of its infamous leader.

- Nissan is seeing improvement in its performance but still has a long way to go, with a key focus on innovation.

- The Alliance represents an opportunity, especially as the terms have been changed to be more favorable for Nissan. Further, its EV technology has scope to disrupt the market.

- Nissan is underperforming its peers currently while trading at a similar valuation. We believe the improvement required is already wholly priced in.

Investment thesis

Our current investment thesis is:

- Nissan is in a turnaround process, as several years of decline leave the business in a depression. Margins are poor and competitors have taken market share.

- The transformation looks to be sound foundationally, with strong vehicle interest and innovation underpinning the improvement.

- Nissan's position in the industry looks attractive. It is critical to further develop vehicle differentiation and extract greater value from the Alliance.

- Relative to peers, Nissan remains unattractive, however, and its valuation does not provide sufficient upside to make this a worthy valuation.

Company description

Nissan Motor ( NSANY ) is a global automotive manufacturer headquartered in Japan. It operates in the automotive industry, producing and selling a wide range of vehicles, including passenger cars, SUVs, electric vehicles, and commercial vehicles. The company has a presence in various regions worldwide and is known for its popular brands such as NISSAN, INFINITI, and Datsun.

Share price

Nissan's share price has performed incredibly poorly over the last decade, losing over 50% of its value, as the business has struggled to maintain its consistent financial performance achieved under Carlos Ghosn.

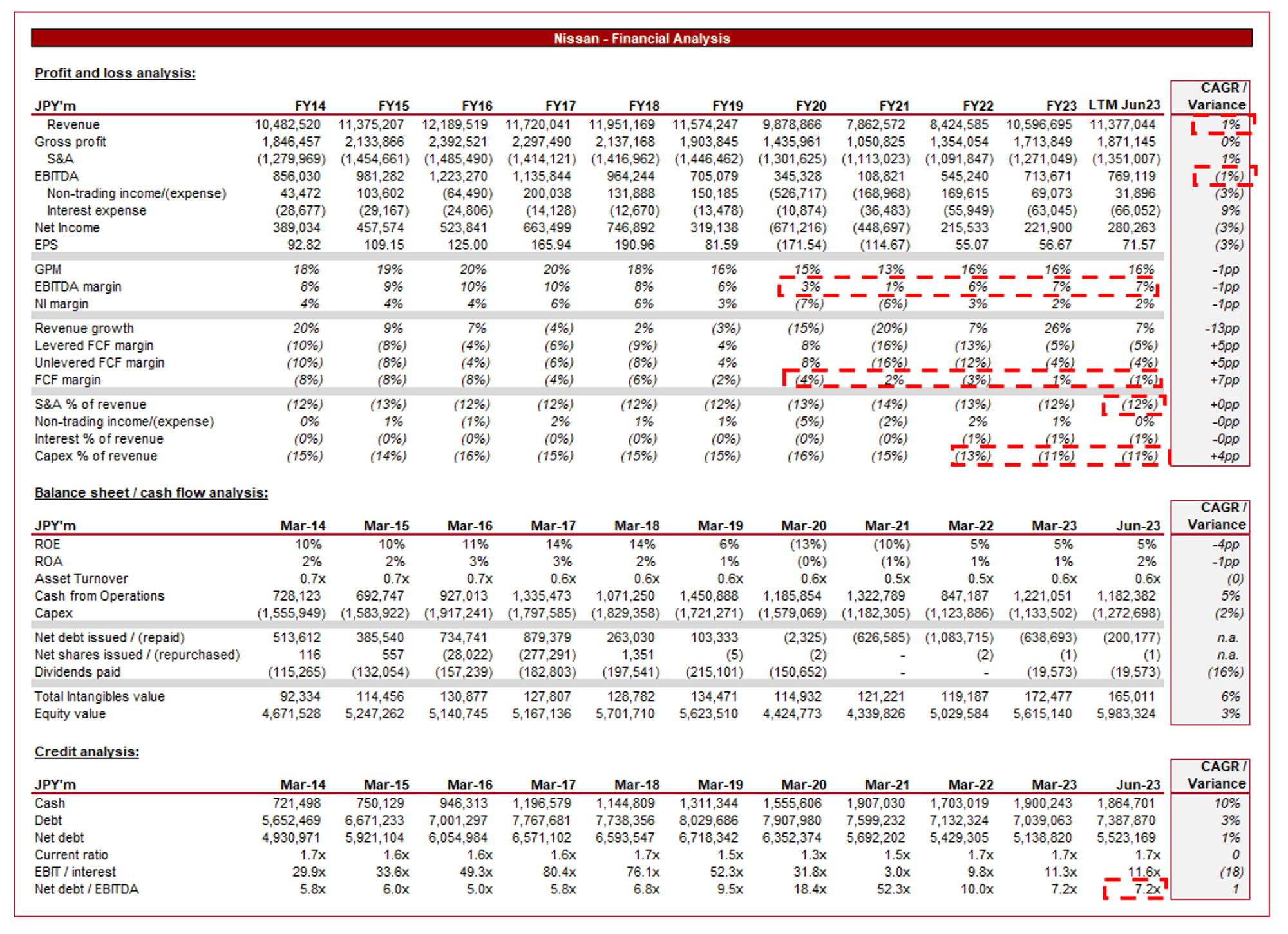

Financial analysis

Nissan financials (Capital IQ)

{kind=link}

Presented above is Nissan's financial performance for the last decade.

Revenue & Commercial Factors

Nissan's revenue has grown at an average rate of 1% in the last 10 years, as the business has experienced 4 years of decline in 11 years. The business is materially struggling with achieving consistency, creating negative sentiment around the business.

Business Model

Nissan designs, manufactures, and markets vehicles through its global production and assembly facilities. Similar to other car manufacturers, the company has global hubs from which to export its vehicles into key regions. The company sells its vehicles through an extensive network of dealerships and distributors across different markets.

Nissan's downward trajectory is driven by a number of factors that inherently reflect its loss of market share and identity among consumers, with consistent retail volume decline. Firstly, the Nissan CVT, although beneficial due to its fuel economy and driving experience, has seen multiple class-action lawsuits and complaints due to recurring safety issues, as well as maintenance requirements. The issues primarily covered this period c.2012-2018 , creating the association of unreliability with the brand, at a time when Japanese brands were hailed as the most reliable brands in the world, making Nissan the problem child.

Secondly, Carlos Ghosn. Carlos was an impressive leader and is arguably one of the greatest CEOs of all time, known for his ability to transform businesses in the automotive industry. Several leading businesses such as Ford ( F ) and GM ( GM ) had tried to poach him over the years. Following turnarounds at Michelin and Renault ( RNSDF ), he brokered an alliance between Nissan and Renault and joined Nissan, and later included Mitsubishi in this, with Nissan acquiring c.34% of its shares. Long story short, he took a struggling, debt-burdened Nissan, which only had 3 profitability vehicles, and completely transformed the business as part of his "Nissan Revival Plan". Ghosn was early in the development of EVs (Committed €4bn in 2007), believing it to represent a significant growth opportunity. The Ghosn leadership structure collapsed in 2018 following an arrest and subsequent scandals. This represents a pivotal moment in Nissan's history, with the business on a noticeable decline since.

The Alliance remains in place, although has been equalized with the end of its common purchasing agreement. The implications are that Nissan will further develop its own EV capabilities, with Renault reducing its ownership in Nissan to 15%, aligning with Nissan's ownership of Renault (as well as taking a stake in Ampere, the future Renault EV spin-off). In rebalancing talks, Nissan has pushed for the protection of its EV/battery technology, which it believes can be a key value driver going forward as the migration toward a fully electric new car market continues. As part of the Alliance, regardless of how it develops going forward, Nissan will continue to benefit from shared parts procurement with Renault, supporting operational excellence.

Although Nissan's financial performance has declined, the company looks to be leveling off, suggesting it has bottomed.

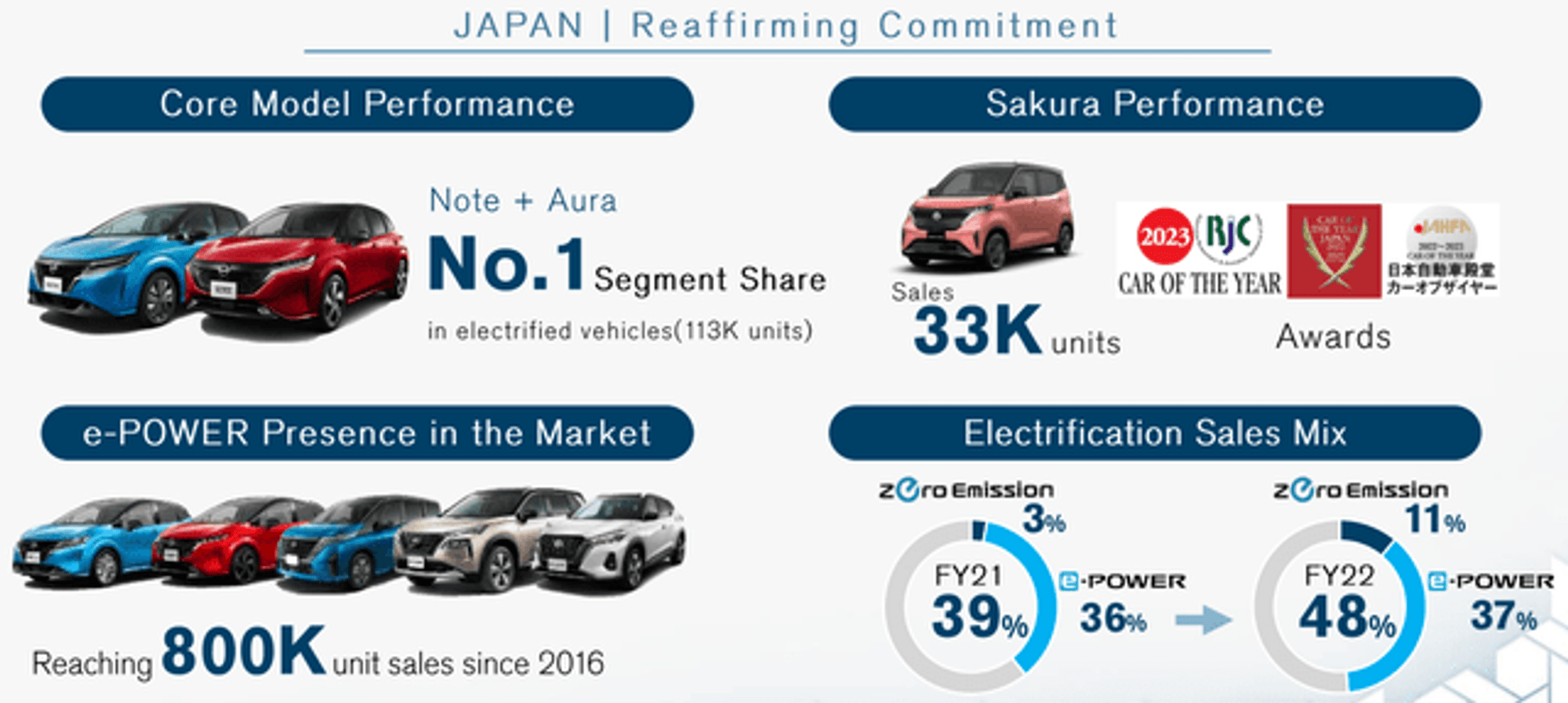

In the Japanese market, the Note and Aura are the number 1 vehicles in the segment, with its electrified fleet reaching almost 50% of sales, much of which is utilizing its proprietary e-power technology .

{kind=link}

Further, the US segment is seeing market share growth in traditional ICE-powered vehicles, implying brand and design strength, despite the weakness. The US is a key market for the business, especially given the strength in non-EV models, allowing the business to balance its transition in sales.

{kind=link}

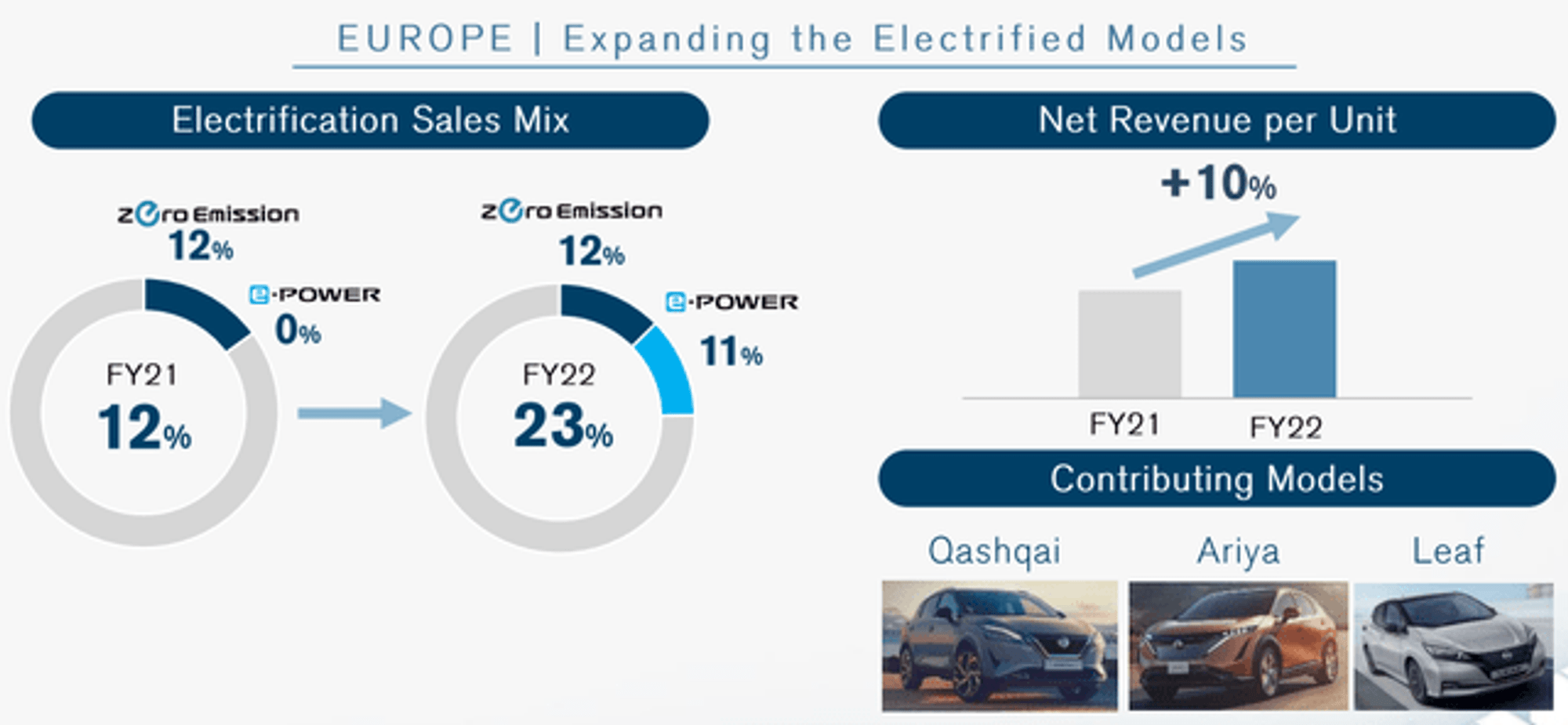

Europe continues to perform well, driven by Nissan's performance in the UK , a key country for the business. This region is dominated by the Qashqai, Nissan's compact SUV offering. Nissan has already developed an EV/E-Power version of this vehicle, which should support growth in the coming years.

{kind=link}

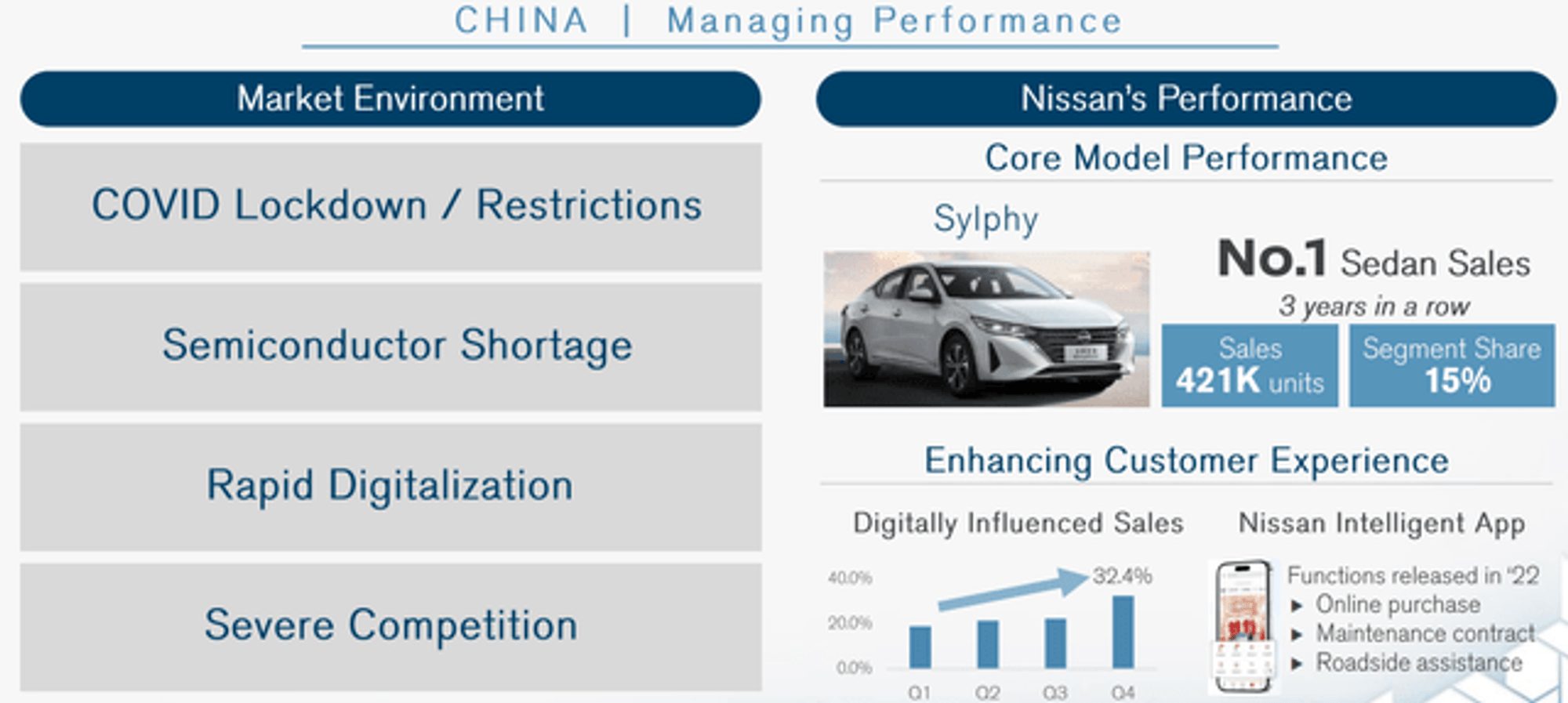

Finally, China. Similar to other operators in the country, the zero-Covid policy has materially impacted demand, as various lockdowns restricted the ability to achieve consistent sales. Again, Nissan has a strong presence in the region, as its Sylphy model is the number 1 sedan for 3 years running.

{kind=link}

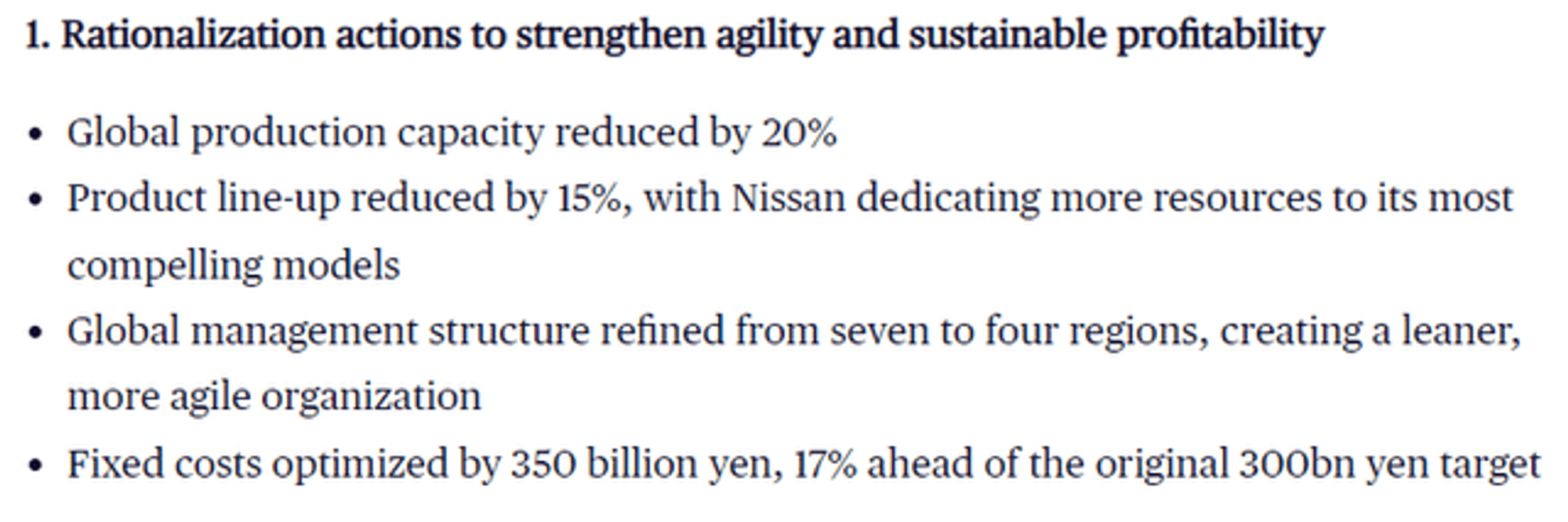

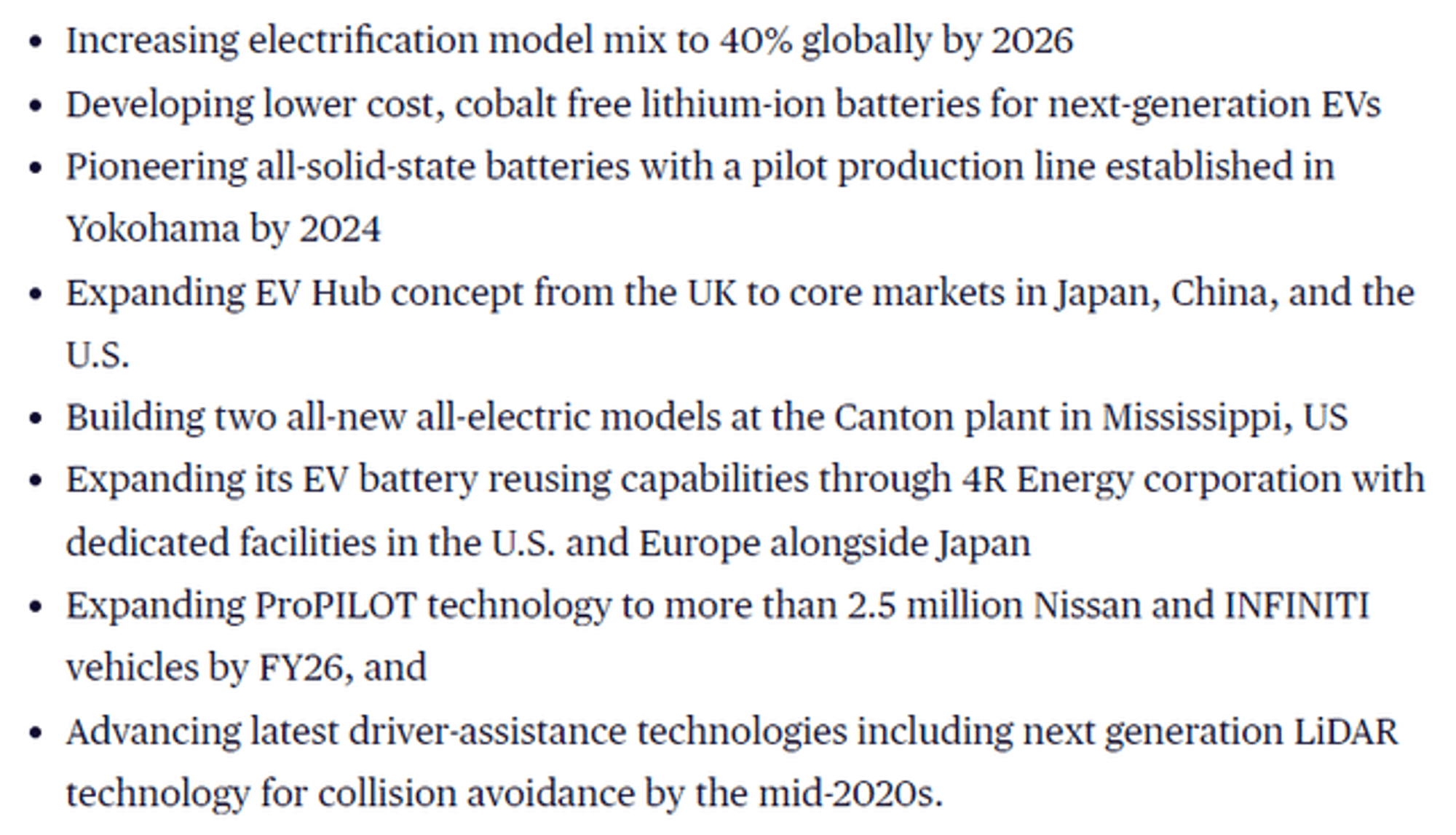

Nissan NEXT is the goal to rationalize capacity and streamline operations, prioritizing its core markets, models, and technologies, seeking to revitalize the business. This involves the following targets:

{kind=link}

{kind=link}

The company is essentially seeking to reduce its bloated operations following the decline in size, followed by a partial reinvestment in the business to support its new growth trajectory. On paper, this plan looks correct and should support financial improvement in the coming years.

The following vehicles have been launched as part of the transition to the second part of Nissan NEXT (second screenshot above).

{kind=link}

Automotive Industry

Firms compete based on factors such as brand strength, vehicle quality, pricing strategies, and technological advancements.

Major competitors of Nissan include Toyota ( TM ), Honda ( HMC ), Volkswagen ( VWAGY ), General Motors, and Ford, Stellantis ( STLA ), among others. Nissan also faces competition from EV specialists, including Tesla ( TSLA ), BYD (BYDDF), and NIO ( NIO ).

The automotive is forecast to grow at a CAGR of 7% into 2030 , driven by increased demand for EVs, as socio-economic factors, alongside regulation, encourage the transition to these vehicles. Global EV sales were up 32% YoY in Q1-23, reflecting the resilience of this growth trajectory.

There have been two key developments in the industry during 2023. Firstly, China eliminated its NEV purchase subsidy in China, contributing to reduced demand in the region, despite the end of its zero-Covid policy. Secondly, Tesla reduced its prices in February, contributing to a mini price war in the industry, as an estimated 40 automakers slashed prices in response.

The growing demand for electric vehicles and tightening emissions regulations has contributed to a large number of EVs entering the market. As a result of this, companies are increasingly pressured to diversify beyond just creating an EV alternative to their traditional vehicles. Nissan's focus on innovative features and technologies, including autonomous driving, represents an opportunity to capture market share through technological superiority. The market remains rife for disruption.

Economic & External Consideration

Current economic conditions represent a near-term headwind. With heightened inflation and elevated rates, consumers are deterred from making large purchases as finances are squeezed and the cost of financing purchases increases. This said, Nissan has navigated this well thus far, as it has experienced a + 15% increase in US sales during Q 3 and top-line production growth of +2.8%.

This is partially due to the overhang from the chip crisis, as production is comfortably increasing, allowing demand to be met. We expect a continuation of the downward trajectory of production, however, particularly as Sep 23 production was down (2.8)%. The improvement from production coming online has slowly been wholly offset by consumer demand.

Margins

Nissan has struggled with margin consistency, experiencing a noticeable decline in the last 10 years. In the most recent year, the company had an EBITDA-M of 7% and a GPM of 16%.

The decline in margins is a reflection of top-line weakness in conjunction with operational inefficiencies with a reduction in scale. The business has essentially lost any advantages from the Alliance, illustrating why Nissan's Management is unhappy with the situation. With the new agreement, we expect a change in fortunes, although it is far too early to quantify this.

The issue is that the business must improve the top-line before the bottom will follow.

Balance sheet & Cash Flows

Although the company has a large ND/EBITDA, interest payments represent 1% of revenue, with sufficient coverage at 12x. This gives us comfort that there is no near-term solvency risk but the balance is an issue. Fitch assigns a BBB- rating .

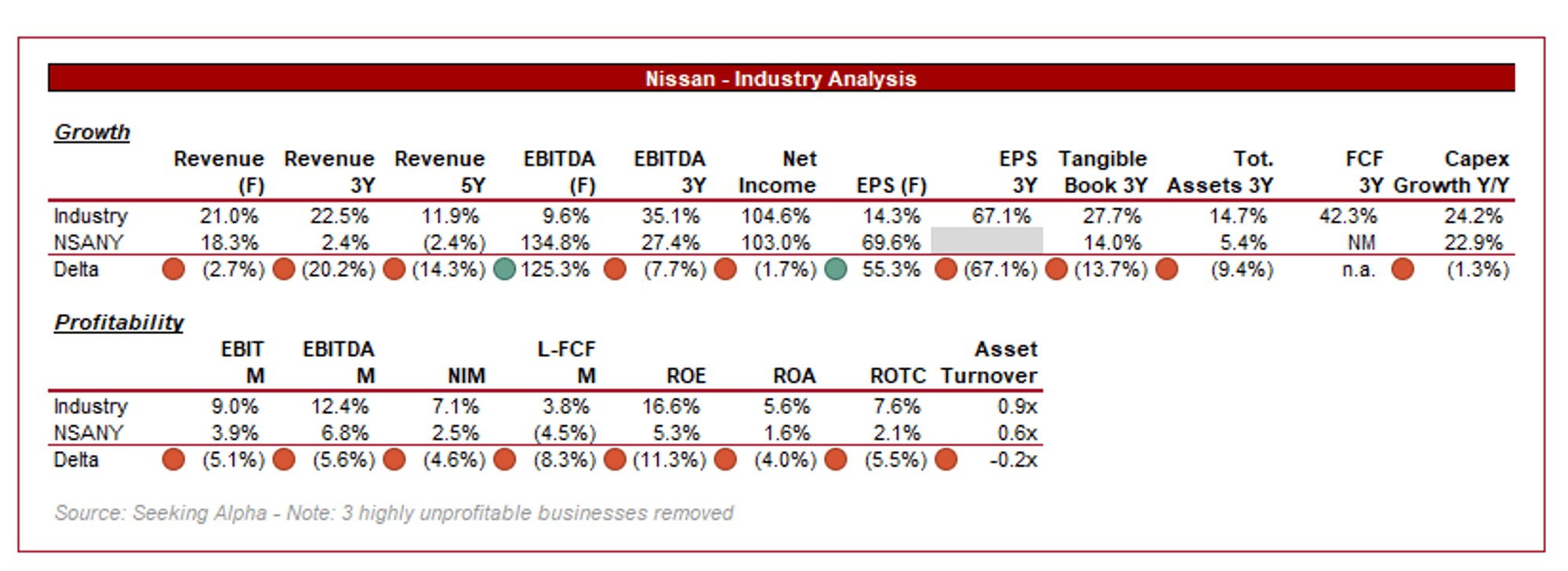

Industry analysis

Automotive industry (Seeking Alpha)

{kind=link}

Presented above is a comparison of Nissan's growth and profitability to the average of its industry, as defined by Seeking Alpha (29 companies).

Nissan's sluggish performance is reflected by its relative performance to peers. The company's growth is significantly below the industry average. The industry has generally performed well in the last few years due to the development of EVs, with Nissan unable to translate this to top-line performance.

Margins are unsurprisingly poor, especially given the scale Nissan has. Improvement does not need to be significant to reach parity but the business has a long way to go to return to its prior levels. Management is hopeful that the change to the Alliance’s terms should allow for an improvement in the coming years.

Based on this, and our prior analysis, Nissan should trade at a large discount to its historical average and peers.

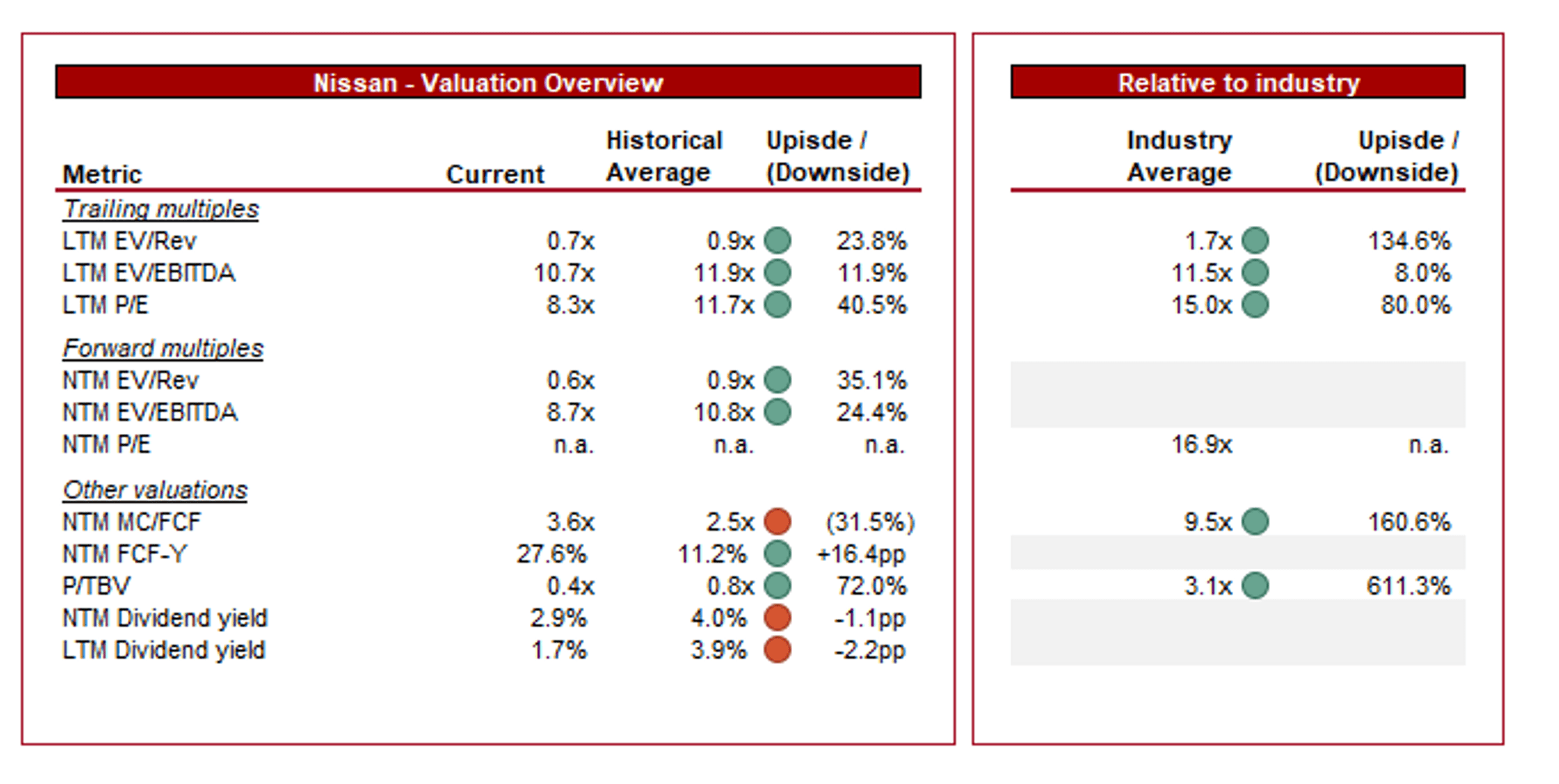

Valuation

{kind=link}

Nissan is currently trading at 11x LTM EBITDA and 9x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average and peer group is undeniably warranted in our view, owing to the company’s decline in financial performance and uninspiring EV transition, as well as loss of market share. This has contributed to a significant increase in its FCF yield, although with a corresponding heightened risk of growth declining.

Conversely, the industry is facing tailwinds into 2030 and Nissan looks to be on the up following an extended period of difficulty. However, we do not believe this is sufficient to suggest the stock is undervalued yet. We suggest investors remain patient for further evidence of improvement.

Final thoughts

We believe Nissan's brand is still highly regarded despite its weakness in recent years, supporting the resurgence efforts of Management. We believe the company is on an upward trajectory, as the Nissan NEXT strategy looks to be yielding results and will be compounded by the new Alliance agreement.

This said, the company still has much progress remaining, including substantially improving margins. We do not believe the valuation adequately prices in the risks around improvement and near-term risks.

For further details see:

Nissan Motor: Transformation In Progress