PPL:CC - NML: Strong Performance High Yield Very Attractive Valuation

2023-09-27 17:27:45 ET

Summary

- Neuberger Berman Energy Infrastructure and Income Fund Inc specializes in investing in midstream companies and has a yield of 10.16%.

- The fund has outperformed the S&P 500 Index over the past year and has a positive outlook for its holdings.

- The fund uses leverage to boost its returns and has a lower turnover compared to its peers.

- The fund has a higher yield than the Alerian MLP Index, so income-focused investors might favor this fund over the index.

- The fund is currently trading at an incredibly attractive discount to the net asset value.

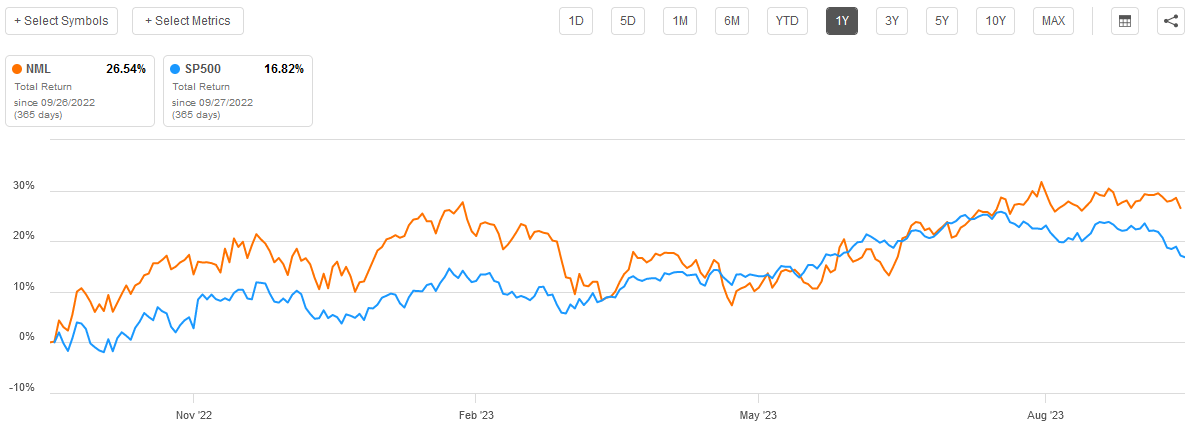

Neuberger Berman Energy Infrastructure and Income Fund Inc ( NML ) is a closed-end fund, or CEF, that specializes in investing in midstream companies, master limited partnerships, and other companies that provide the necessary services to ensure that society has available the energy to meet the needs of society. This has generally been a fairly good place to be recently as most of these companies are highly resistant to economic fluctuations, pay out very high distribution yields, and have benefited in the market as energy prices have once again begun to rise (and are likely to continue to do so ). Indeed, as of the time of writing, the Neuberger Berman Energy Infrastructure and Income Fund yields 10.16% and has beaten the S&P 500 Index ( SP500 ) over the past twelve months by quite a large margin:

{kind=link}

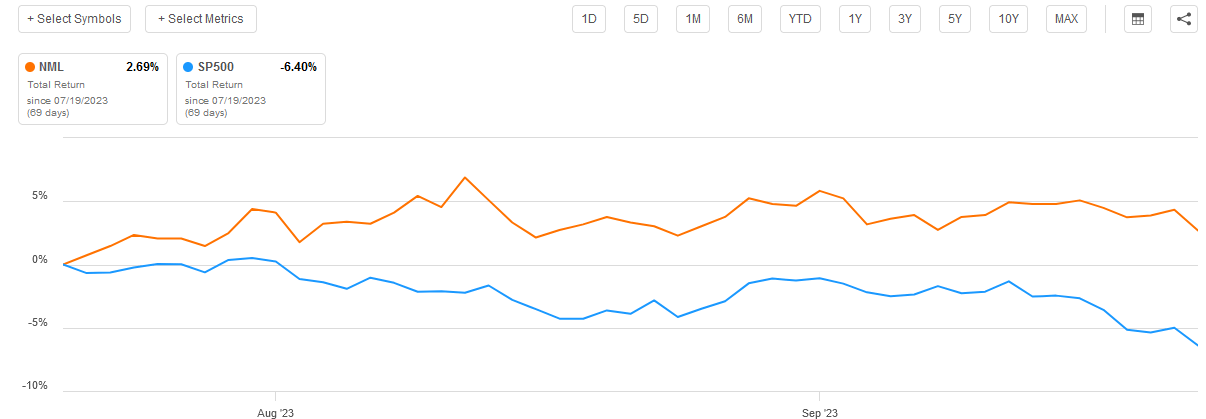

We last discussed this fund on July 19, which was right around the time that the energy market was starting to turn. After all, the Strategic Petroleum Reserve was finally tapped out around the middle of July so the Federal Government could no longer sell the nation’s strategic stockpile into the market in an attempt to hold crude oil prices down. As might be expected, the fund has delivered a very strong performance since that date. Investors who bought the fund on the day that article was published have made 2.69% on their money. For reference, the S&P 500 Index has delivered a loss to investors who bought on the same date:

{kind=link}

Naturally though, seeing where this fund has been is only part of our analysis and it is not the most important part. We are naturally much more interested in where it might be going. Fortunately, the future of the companies in this fund is quite positive, which should prove to be to the fund’s benefit. As is always the case with energy infrastructure funds, the Neuberger Berman Energy Infrastructure and Income Fund is substantially undervalued at the current price, so the price is certainly reasonable for anyone looking to add some shares of the fund to their portfolio.

About The Fund

According to the fund’s website , the Neuberger Berman Energy Infrastructure and Income Fund has the primary objective of providing its investors with a high level of total return and cash distributions. As is usually the case, the fund provides a much more detailed overview of its strategy and objectives on the webpage:

Neuberger Berman

This is very similar to the other energy infrastructure funds that we discuss here at Energy Profits in Dividends. The description above describes “energy infrastructure companies” as being those companies that provide transportation, storage, and processing of energy resources. This description would thus encompass all of the following businesses:

- Midstream companies that operate pipelines and storage facilities.

- Liquefied natural gas producers that convert natural gas into liquefied natural gas for export abroad.

- Tanker companies that transport resources such as crude oil, natural gas, and liquefied petroleum gas over the ocean.

- Utilities that transport electricity and natural gas to the homes and businesses of their customers.

- Renewable energy generation companies that produce electricity using wind, solar, hydropower, and other renewable electric generation technologies.

- Refiners that convert crude oil into gasoline, diesel fuel, airplane fuel, and other refined products.

- Companies that perform some combination of the above services.

With that said, it is incredibly rare to find refiners or tanker companies in most energy infrastructure funds despite the fact that these companies do technically fit the definition. We do frequently see liquefied natural gas producers though, and in fact, Cheniere Energy ( LNG ) is one of the ten largest holdings in most energy infrastructure funds (including this one). In short, these are the companies that are frequently overlooked by investors because the services that they provide are largely invisible and taken for granted even though they are either directly or indirectly used daily by almost everyone who lives in any developed country.

The fund’s objective of focusing on a high level of total return while primarily providing its returns in the form of distributions paid to the shareholders makes a lot of sense when we have a look at the fund’s portfolio. As we can see here, the fund’s portfolio currently consists entirely of common equity, although it does have a small allocation to cash:

CEF Connect

In this case, the term “common stock” refers to all forms of common equity as this fund does invest in master limited partnerships that do not technically issue common stock. The proper term for common equity issued by a master limited partnership is “limited partnership unit.” As I explained in numerous previous articles, common equity is by definition a total return investment. After all, investors typically purchase common equity in order to receive a cut of the company’s profits via a dividend or distribution while also benefiting from the capital gains that accompany the growth and prosperity of the issuing entity. In the case of most energy infrastructure companies, they tend to pay out the overwhelming majority of their cash flows to the investors as their low growth rates limit the potential capital gains that investors can receive. As such, it makes a lot of sense that this fund would deliver its total returns by paying out these profits to its shareholders.

As regular readers are no doubt well aware, I have devoted considerable amounts of time and effort over the years to discussing midstream companies, utilities, and other energy infrastructure companies here at Energy Profits in Dividends and on Seeking Alpha’s main site. As such, the majority of the largest positions in the portfolio will probably be familiar to most readers. Here they are:

Fund Fact Sheet

I have discussed all of the companies on this list except for Western Midstream Partners ( WES ) and Civitas Resources ( CIVI ) multiple times. Civitas Resources claims to be a carbon-neutral upstream oil and gas producer in Colorado’s DJ Basin, although it also operates in both the Midland and Delaware lobes of the Permian Basin. I will admit that I am having difficulty understanding why an upstream company would be included in an energy infrastructure fund, as usually these companies are reserved for upstream energy funds like the BlackRock Energy & Resources Trust ( BGR ). Actually, Civitas Resources seems like the perfect company for that fund given BlackRock’s propensity for ESG investments.

The same comments apply to Antero Resources ( AR ), which is also an upstream production company. It does not advance the same environmental sustainability claims that Civitas Resources does, but the basic business model is exactly the same. The fact that we see two upstream energy companies among the fund’s top ten positions makes me believe that the fund’s management sees the Neuberger Berman Energy Infrastructure and Income Fund as an all-encompassing energy fund, not just a traditional energy infrastructure fund. This is not necessarily a bad thing, especially considering the strong outlook for energy prices right now, but investors do need to keep in mind that some of the fund’s holdings may be more exposed to commodity prices than we would normally expect from a fund like this.

The remainder of the companies that we see above are pretty much what we would expect to see in an energy infrastructure fund. In fact, most of them are the same companies that we see in the portfolios of the fund’s peers. Five of the companies are traditional midstream firms that transport crude oil, natural gas, and natural gas liquids under long-term volume-based contracts. NextEra Energy Partners ( NEP ) is a yieldco that sells renewably generated electricity under long-term power purchase agreements. Cheniere Energy is the largest producer of liquefied natural gas in the United States, and it sells its products under long-term contracts that guarantee it a specific margin. Sempra Energy ( SRE ) is a major natural gas utility that mostly operates in Southern California.

In short, all of these companies enjoy the very stable and non-cyclical cash flow that we normally expect from companies held by a fund like this. This stability is good for investors because it provides a great deal of support for the distributions that these companies pay out to their investors.

There have been relatively few changes since the last time that we discussed this fund. Indeed, the only change of note is that ONEOK ( OKE ) was removed from its previous position among the largest positions in the fund. In its place, we have Civitas Resources. I will admit that I am of somewhat mixed opinions about this change as ONEOK was far more stable financially than any upstream company is likely to be and it had a substantially higher yield, so its presence resulted in more income for the fund than Civitas is likely to provide. On the other hand, as I mentioned in a previous article , the merger with Magellan Midstream Partners ( MMP ) was not a very good idea as it reduced ONEOK’s growth prospects. On the other hand, Civitas is likely to benefit from rising energy prices to a far greater extent than ONEOK and this could give it improved capital gains potential over the coming months. This could allow the fund to net some significant profits by realizing those capital gains as they accrue.

The fact that there have been so few changes over the past two months suggests that this fund does not have an especially high annual turnover. I discussed why this is important in my last article on this fund:

The reason that the low annual turnover is nice to see is that it costs the fund money to trade stocks or other assets. These expenses are billed directly to the shareholders and create a drag on the fund’s performance. They also make the management’s job much more difficult because the fund’s managers need to generate sufficient returns to cover these costs and still have enough left over to deliver a satisfactory return to the shareholders. There are very few management teams that manage to accomplish this on a consistent basis, which is one of the biggest reasons why actively managed funds usually underperform their benchmark indices.

The Neuberger Berman Energy Infrastructure and Income Fund only has an annual turnover of 19.00%, which is one of the lowest levels of any energy infrastructure fund. As such, its turnover does not appear to be a problem. Let us have a look at its performance, however.

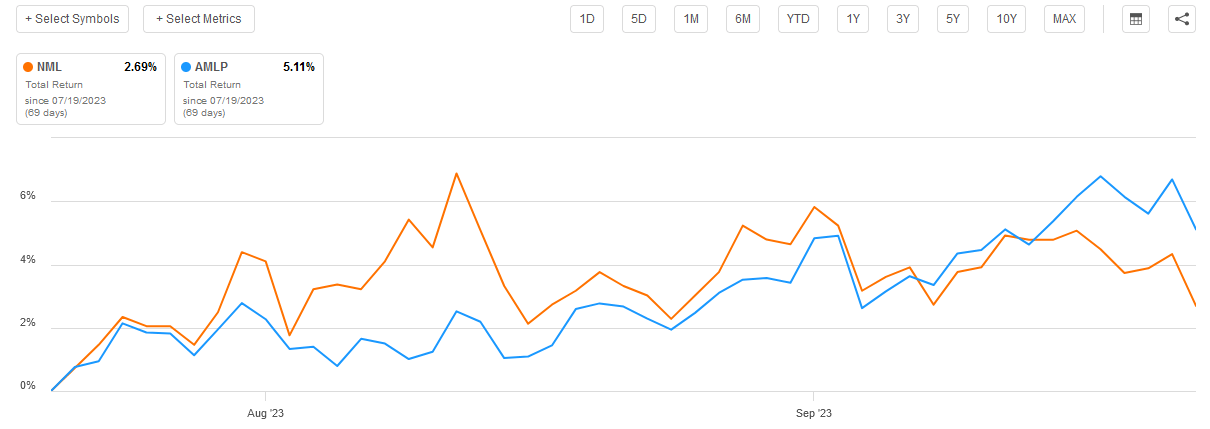

The Neuberger Berman Energy Infrastructure and Income Fund benchmarks itself against the Alerian MLP Index ( AMLP ). I am not sure that this is really a good idea as the fund has a very different portfolio than the index. However, this is the index that the fund’s managers have chosen to use so I will not start a debate about it.

The fund has underperformed the index since the date that the last article on this fund was published:

{kind=link}

However, the difference was scant, and we can see that the Neuberger Berman Energy Infrastructure and Income Fund actually beat the index over most of the period until the index took the lead earlier this month.

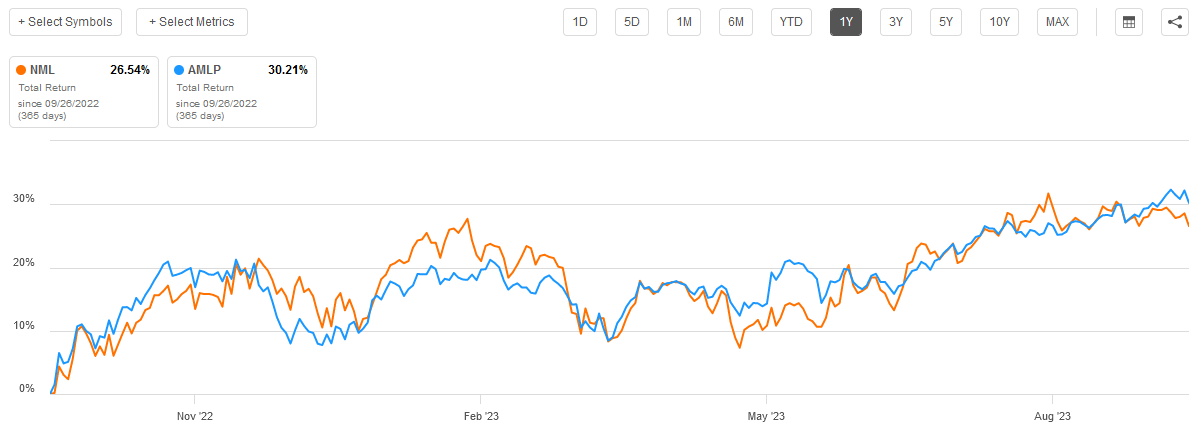

The fund also underperformed the index over the past year:

{kind=link}

Please note that all of the above charts are looking at the total return, not the price action of the fund’s shares in the market. This is important because the Neuberger Berman Energy Infrastructure and Income Fund is one of the few closed-end funds that actually has a higher yield than the index. This distinction might make some investors want to purchase this fund instead of the index, even though the index did deliver a stronger total return.

Leverage

As is the case with most closed-end funds, the Neuberger Berman Energy Infrastructure and Income Fund employs leverage as a method with which to boost its total returns well beyond those provided by the assets in the portfolio. I discussed how this works in the previous article on the fund:

In short, the fund borrows money and then uses that borrowed money to purchase common units of midstream partnerships and corporations. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case. With that said though, the beneficial effects of leverage are not as great today with interest rates at 6% as they were two years ago when interest rates were at 0%. Fortunately, most midstream partnerships have yields that are well above 6% so the strategy still works to boost the effective portfolio yield.

Unfortunately, the use of debt in this fashion is a double-edged sword because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage because that would expose us to an excessive amount of risk. I do not usually like a fund’s leverage to exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Neuberger Berman Energy Infrastructure and Income Fund has levered assets comprising 17.72% of its portfolio. This is well below the one-third maximum that I would normally like to see, and it is also below the leverage ratio possessed by most of the fund’s peers. Thus, this fund is striking an acceptable balance between risk and reward, and we probably do not need to worry too much about its leverage right now.

Distribution Analysis

One of the biggest reasons why investors purchase shares in midstream companies and other energy infrastructure firms is that these companies typically pay out a very high distribution yield to their investors. We can immediately see this by looking at the yield on the Alerian MLP Index, which is 7.94% as of the time of writing. Midstream corporations, which this fund also invests in, usually have lower yields but they are still well above those of most other companies in the market. For example, consider the yields of the following midstream corporations:

| Company |

| Current Dividend Yield |

| Enbridge Inc. ( ENB ) |

| 7.79% |

| Pembina Pipeline Corporation ( PBA ) |

| 6.62% |

| Kinder Morgan, Inc. ( KMI ) |

| 6.86% |

| The Williams Companies ( WMB ) |

| 5.33% |

| ONEOK |

| 5.92% |

As we can see, midstream partnerships will normally have a yield of around 8% while midstream corporations will have a yield of around 6%. These yields are still both well above the risk-free rate and substantially above that of pretty much any sector of the economy. After all, the S&P 500 Index (SP500) only has a 1.53% yield at the current price. Thus, we can see that the assets held by the Neuberger Berman Energy Infrastructure and Income Fund are going to have substantially higher yields than the average asset in the market.

The fund’s basic strategy is to collect the distributions and dividends from all of these companies and pay them out to its shareholders, net of any expenses. It may also be able to realize some capital gains that are added to the amount that can be paid out. The fund then adds a layer of leverage to boost the effective returns even higher. We can quickly see that this should all result in the fund having a very high yield itself.

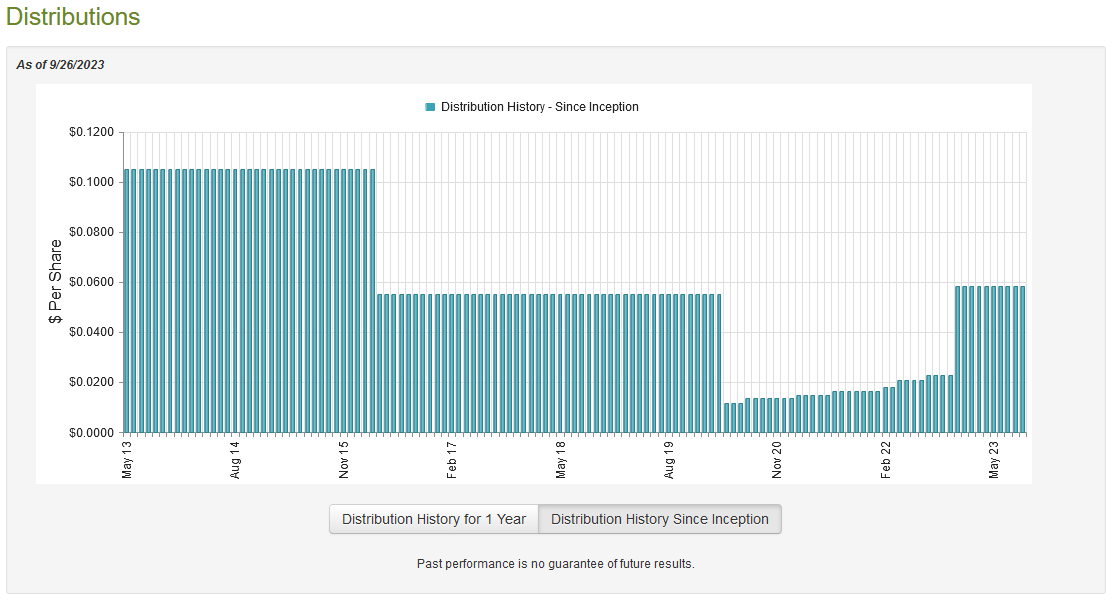

This is indeed the case as the Neuberger Berman Energy Infrastructure and Income Fund pays a monthly distribution of $0.0584 per share ($0.7008 per share annually), which gives it a 10.16% yield at the current price. The fund has unfortunately not been particularly consistent with its distribution over the years:

{kind=link}

We can see substantial distribution cuts in response to the energy market collapses of 2015 and 2020, but otherwise, the fund has been reasonably consistent. In fact, this is the only energy infrastructure fund that has restored its distribution back to the levels that it had prior to the pandemic. Actually, the current distribution is slightly higher than its pre-pandemic level ($0.0584 per month versus $0.0550 per month), which adds somewhat to its appeal. This current distribution came following a rapid series of hikes after the initial cut. This therefore probably makes this one of the more appealing distribution histories for those investors who are seeking a safe and secure source of income, but it is not perfect.

As I have stated numerous times in the past though, the fund’s history is not necessarily the most important thing for investors that are buying the fund’s shares today. After all, anyone purchasing shares today will receive the current distribution at the current yield and will not be adversely affected by actions that the fund has taken in the past. The most important thing is how well the fund can sustain its current distribution. Let us investigate this.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on May 31, 2023. This is a newer report than the one that we had available to us the last time that we discussed this fund, which is nice. As I have written about before, energy prices were suppressed throughout the first half of this year, which resulted in lower prices and a weaker market for these stocks than we saw in 2022. As such, the returns that an energy infrastructure fund such as this would be able to generate were weaker than in the preceding period. This report should give us a pretty good idea of how well the fund’s management was able to handle that situation.

During the six-month period, the Neuberger Berman Energy Infrastructure and Income Fund received $15,291,886 in dividends and distributions along with $51,510 in interest from the assets in its portfolio. However, a substantial portion of this money came from master limited partnerships and so is not considered to be income for tax purposes. As such, the fund only reported a total investment income of $5,255,662 during the period. This was not enough to cover its expenses, and the fund ended up reporting a net investment loss of $557,460 during the period. Obviously, this was not enough to cover any distributions, but the fund still paid out $19,853,288 to its shareholders. At first glance, this might be concerning as the fund’s net investment income was nowhere near enough to cover the distributions.

However, the fund has other methods through which it can obtain the money that it needs to cover its distribution. For example, the fund might be able to realize some capital gains and use that money to cover the distributions. It also received $10,069,552 in distributions from master limited partnerships that were not considered in the fund’s investment income but obviously still represent money that it can pay out to its shareholders. Unfortunately, the fund had mixed success in this area as it reported net realized gains of $20,214,120 but these were completely offset by $76,132,090 in net unrealized losses.

Overall, the fund’s assets declined by $76,328,718 after accounting for all inflows and outflows during the period. This is certainly concerning as it suggests that the fund did not manage to cover its distributions during the period. However, the fund’s net realized gains were almost enough to offset the net investment loss and cover the distribution. As we can see, the difference between the total decline in net assets and the net unrealized losses was only a little less than $200,000. In addition, the fund’s performance in the preceding year was stellar as it managed to cover its distribution and all other expenses and still increased its net assets by $136,603,785 after accounting for all inflows and outflows.

Thus, the fund did manage to cover all of its distributions over the past eighteen months. When we consider that it will probably be able to do better in the second half of this year due to the current strength in the energy market, we can conclude that we probably do not have anything to worry about here. The fund should be able to sustain its distributions at the current level.

Valuation

As of September 26, 2023 (the most recent date for which data is available as of the time of writing), the Neuberger Berman Energy Infrastructure and Income Fund has a net asset value of $7.99 per share but the shares only trade for $6.96 each. This gives the shares a 12.89% discount on net asset value at the current price. This is a very attractive discount, although it is not quite as good as the 13.33% discount that the shares have had on average over the past month. However, as I have pointed out numerous times, any time a fund manages to acquire a double-digit discount on net asset value, the price is quite reasonable.

Conclusion

In conclusion, energy infrastructure companies are non-cyclical companies that tend to have enormous yields, which is exactly what any conservative risk-averse investor should be able to appreciate. The Neuberger Berman Energy Infrastructure and Income Fund invests its assets into a portfolio of these companies with the goal of providing investors with a very high level of total return and income. It generally succeeds in this goal, as the fund has a much higher yield than competing funds yet has lower overall leverage. The fund is also one of the few to boast a higher yield than the Alerian MLP Index, albeit a slightly lower total return. When we combine this with a very attractive valuation, this fund might be worth adding to your portfolio today.

For further details see:

NML: Strong Performance, High Yield, Very Attractive Valuation